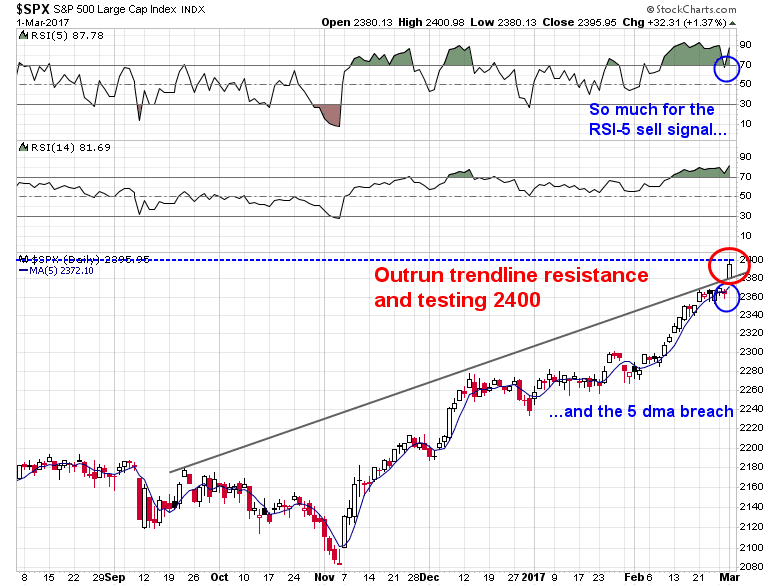

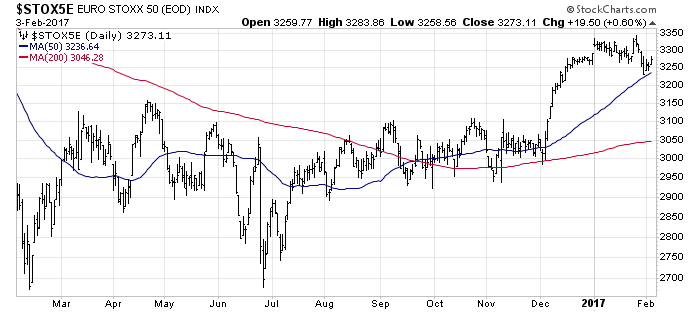

Mid-week market update: Boy, was I wrong. Two weeks ago, I wrote Why the S&P 500 won’t get to 2400 (in this rally). Despite today’s market strength, stock prices may be restrained by a case of round number-itis as the Dow crosses the 21,000 mark and the SPX tests the 2,400 level.

In addition, the market’s reaction to President Trump’s speech to Congress was at odds to the reaction from Street strategists. While the market went full risk-on in the wake of the Trump speech, this Bloomberg summary of strategist comments made it clear that the speech was long on themes and short on details. Perhaps stocks are rallying because Trump did not go off script and sounded statesmanlike and presidential. How long the market remains patient with his lack of the specifics on tax reform, which is Wall Street’s major focus, remains an open question.

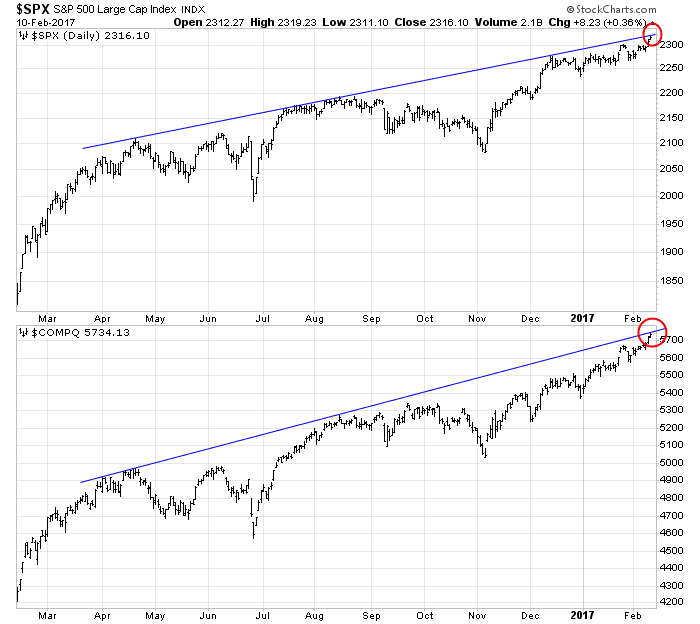

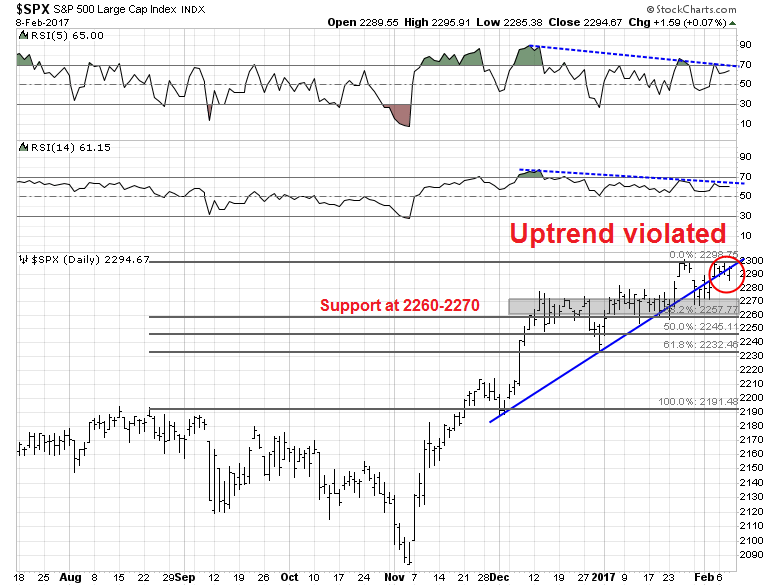

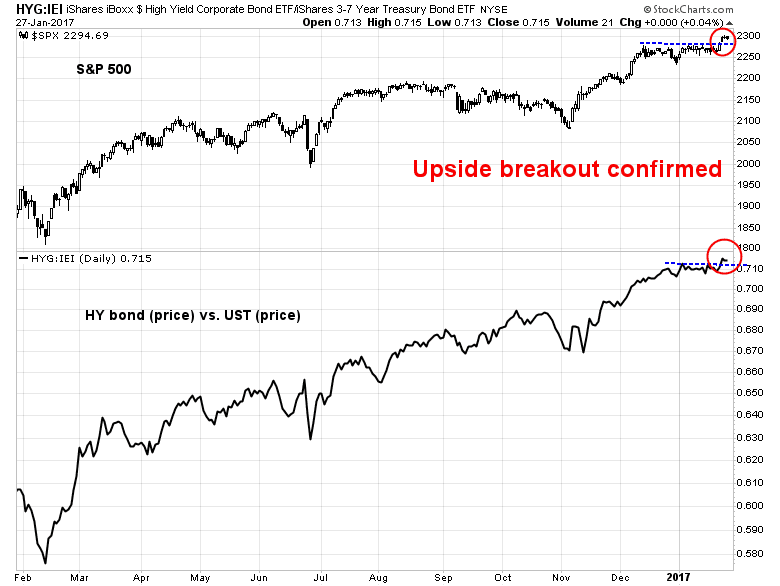

In the meantime, the SPX has broken above its trend line and appears to be staging an upside blow-off. When animal spirits start to stampede like this, you never know when the rally will end.

Does this mean it’s time to jump back on the bullish bandwagon? Not so fast. The week isn’t over and there are a couple of other major developments (other than the Trump speech) that warrant consideration.

The state of the (European) union

I suggested about a month ago that we may be nearing a peak in political populism based on the magazine cover indicator (see Peak populism?). The latest developments from Europe indicates that we may be nearing a political inflection point.

The populist Geert Wilders is losing ground in the upcoming Dutch election on March 15. Bloomberg reports that Wilders’ Freedom Party is running neck and neck with the establishment Liberals, which forms the current government:

Dutch Prime Minister Mark Rutte’s Liberals are making up ground on populist frontrunner Geert Wilders in the polls, suggesting that voter support is crystallizing in the final weeks of the campaign in favor of keeping Rutte in power.

Two polls released on Tuesday showed the Freedom Party with a one-seat advantage or even with the Liberals. That’s down from a lead of as many as 12 seats at the start of the year. A poll aggregator released Wednesday showed the Liberals narrowly ahead for the first time since November.

Business Insider also reported that Wilders has slipped to second place in one recent poll.

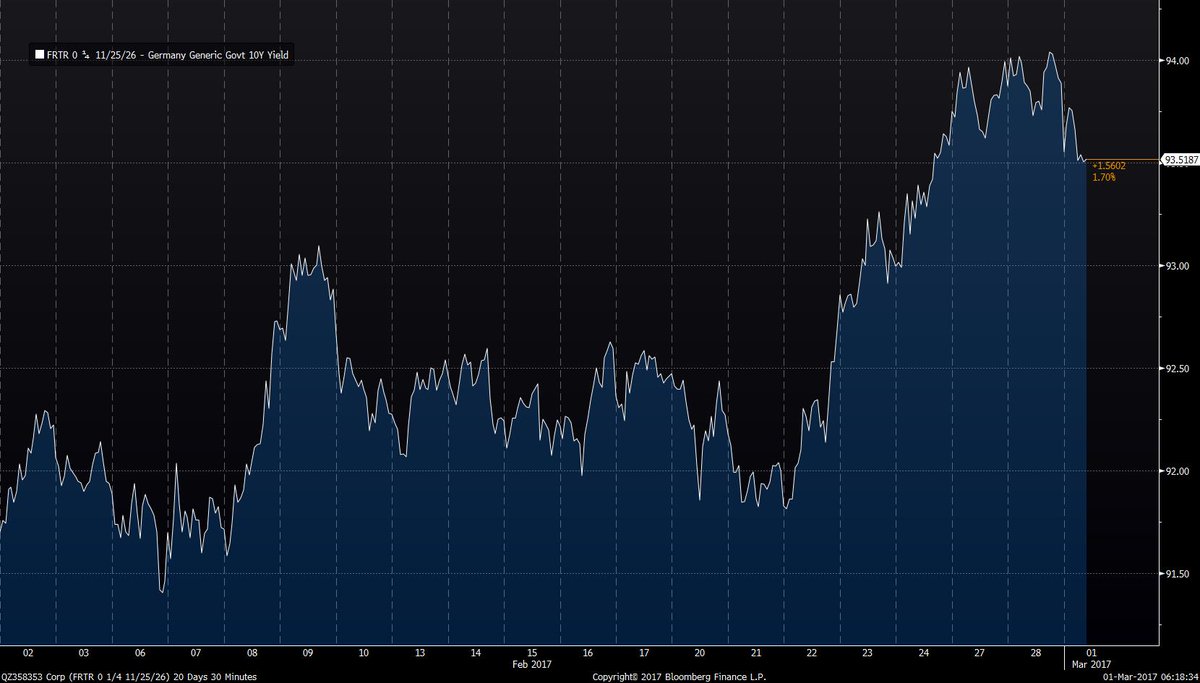

In France, conservative presidential candidate François Fillon’s political fortunes are imploding, based on the news that investigating magistrates have summoned him and his wife on charges that he put his wife on a government payroll for nonexistent work. In a press conference, Fillon decried the move as “political assassination” and vowed to fight on. This development has cleared a path for the centrist Emmanuel Macron to the French presidency. The latest Betfair odds shows Macron surging at Fillon’s expense. The anti-establishment and populist Marine Le Pen remains in second place, with little hope of winning the election.

As a consequence, the French-German yield spread has begun to narrow.

The state of the European Union is getting stronger.

A March rate hike?

In a Bloomberg interview on February 21, Cleveland Fed president Loretta Mester stated that the Fed does not like to surprise the market on interest rate decisions. At the time of that interview, the odds of a March rate hike was in the 20-30% range. It is now about 70% after one Fed speaker after another warned that not only is the March FOMC meeting “live”, there is a distinct possibility that they may raise rates at that meeting. San Francisco Fed president John Williams said that he expect that the FOMC will a rate hike will warrant “serious consideration” at the March meeting. In a CNN interview, New York Fed president William Dudley said that the Fed will raise rates “fairly soon”.

What does this all mean?

Fed watcher Tim Duy thinks that the question is whether the Fed wants to be preemptive, or it wants to wait to see how fiscal policy develops:

When I read the interview, it is hard for me to see that he has a strong conviction for drawing forward the rate hike to March. It seems odd to do so if he sees no change in the forecast and downplays the impact of the upside risks. If he does want to move in March, it tells me then it has little to do with either factor and is entirely about staying ahead of the curve. It is about the need for a preemptive rate hike. If his forecast is for three hikes and he wants to hike in March, then his patience has ended and he wants those hikes frontloaded. If for FOMC participants as a whole the forecast has yet to change much, then it is possible that the even if they raise in March, the median projection of three rate hikes this year remains steady.

Much of the data has been coming on the “hot” side, indicating a robust economy with rising inflationary pressures. By the book, the Fed should be thinking seriously about starting a rate hike cycle about now. Indeed, there were several data points that were released today that are supportive of that view.

The Beige Book, which released today, showed a lot of “modest to moderate” growth. Labor markets are tight, with “moderate” employment growth. Some districts reported labor shortages. These are the kinds of conditions that Dudley referred to when he described an “economy continues on the trajectory that it’s on, slightly above-trend growth, gradually rising inflation” as the prerequisites to the removal of monetary policy accommodation.

This morning also saw the release of the ISM Manufacturing Survey, which rose and came in ahead of expectations, as it continued a trend of beating market expectations.

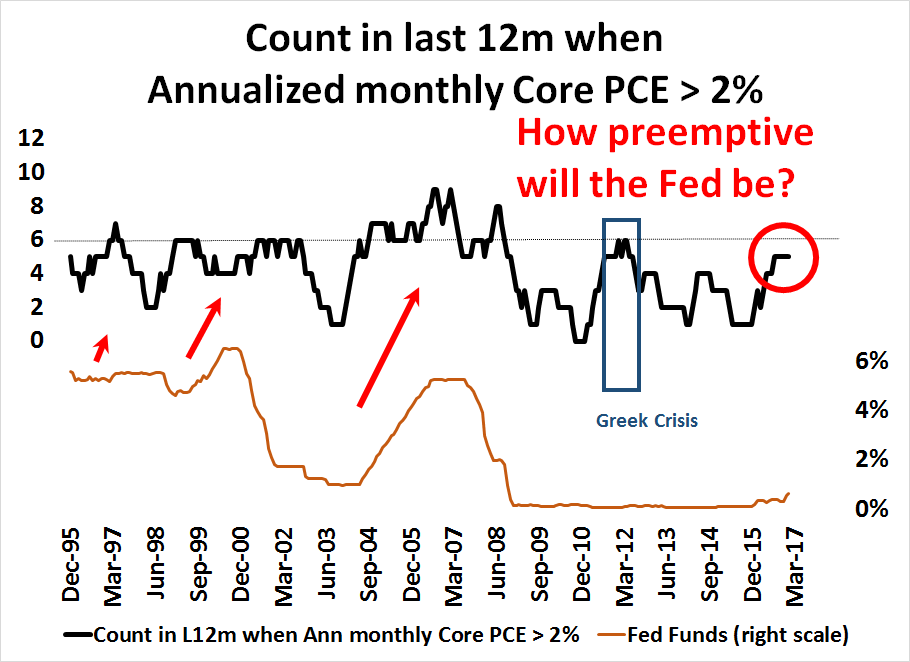

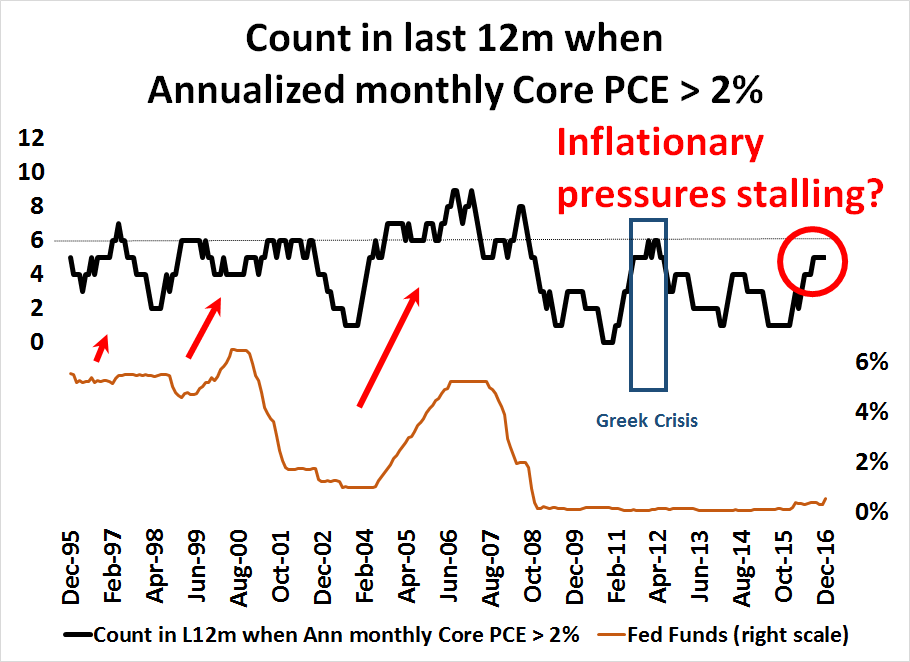

As well, month-over-month Core PCE, the Fed’s preferred inflation metric, was released this morning. It also came in ahead of expectations and surged to an annualized rate of 3.8%, well ahead of the Fed’s 2% inflation target.

To put this data point into context, I counted the times in the last 12 months that annualized m/m Core PCE has exceeded 2%. As the chart below shows, the Fed has historically begun a rate hike cycle whenever the count reached six (dotted line). The count currently stands at five, which begs the question, “How preemptive does the Fed want to be?”

Fed chair Janet Yellen and vice chair Stan Fischer are scheduled to speak on Friday. If they want to give the market further direction, we should get it then. In addition, Fed governor Lael Brainard is scheduled to speak a 6pm ET today (Wednesday). Brainard is one of the most dovish governors on the Board, if her tone sounds hawkish, then watch out!

A market blow-off

In summary, the stock market is undergoing a blow-off with no end in sight. We are starting to see bullish political developments out of Europe, but one wildcard is the possibility of a March rate hike. Should the Fed preemptively raise rates, not only would the normal macro effects of slowing the American economy be applicable, it would push up the US Dollar. A rising USD would be bearish in three ways. First, a strong greenback squeezes the margins and therefore the earnings of large cap multi-nationals companies. It would be supportive of the “America First” contingent within the Trump administration in their protectionist policies. As well, a strong USD would pressure the emerging market countries and companies with USD debt and raise the odds of an EM debt crisis.

My inner trader initiated a small SPX position on Tuesday. He is maintaining his position in view of the downside risks to the market.

Josh Brown had a terrific comment about the secret of Warren Buffett’s success. Buffett is unabashedly “permabullish” on America:

One of the hallmarks of Berkshire’s success has been its willingness to raise or lower its formidable cash hoard in response to the presence (or lack thereof) of viable investing opportunities. One of the other hallmarks of Buffett’s approach has been to tune out forecasts and de-emphasize the importance of them in general.

The one thing Buffett has never given up on is the idea that American productivity, innovation and economic dynamism will always lead to substantially greater prosperity in the future. And he’s been right for decades, through all sorts of setbacks, crises and challenges for the nation.

So if the choice is to be in the Buffett camp vs the David Stockman camp or the Peter Schiff camp, well, I regard that as no real choice at all.

Lastly, permabulls need not be blind to the possibility of market declines, economic catastrophes (real or imagined) and other momentary trials and tribulations. Buffett’s got these possibilities built right into his manifesto:

Charlie and I have no magic plan to add earnings except to dream big and to be prepared mentally and financially to act fast when opportunities present themselves. Every decade or so, dark clouds will fill the economic skies, and they will briefly rain gold. When downpours of that sort occur, it’s imperative that we rush outdoors carrying washtubs, not teaspoons. And that we will do.

That formula has worked out well. Stay bullish on the belief of the dynamism of America, and buy good businesses when they become cheap. In a post-election interview with CNN, Buffett expressed confidence in the supremacy of the American businesses (click on this link if the video is unavailable).

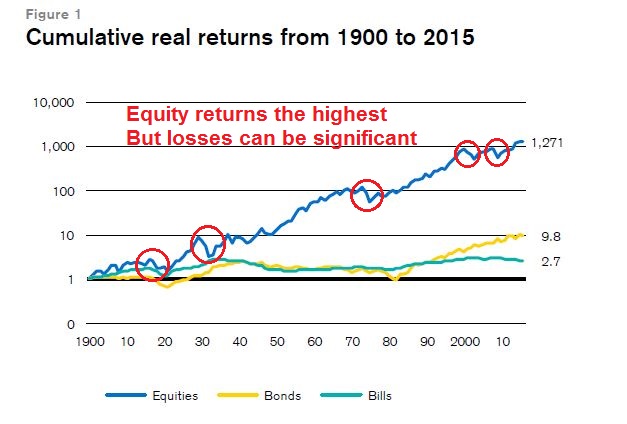

There is much to be said about the Buffett formula. According to Credit Suisse, US real equity returns has been the highest in the world. Though the stock market has experienced serious losses, prices have always come back.

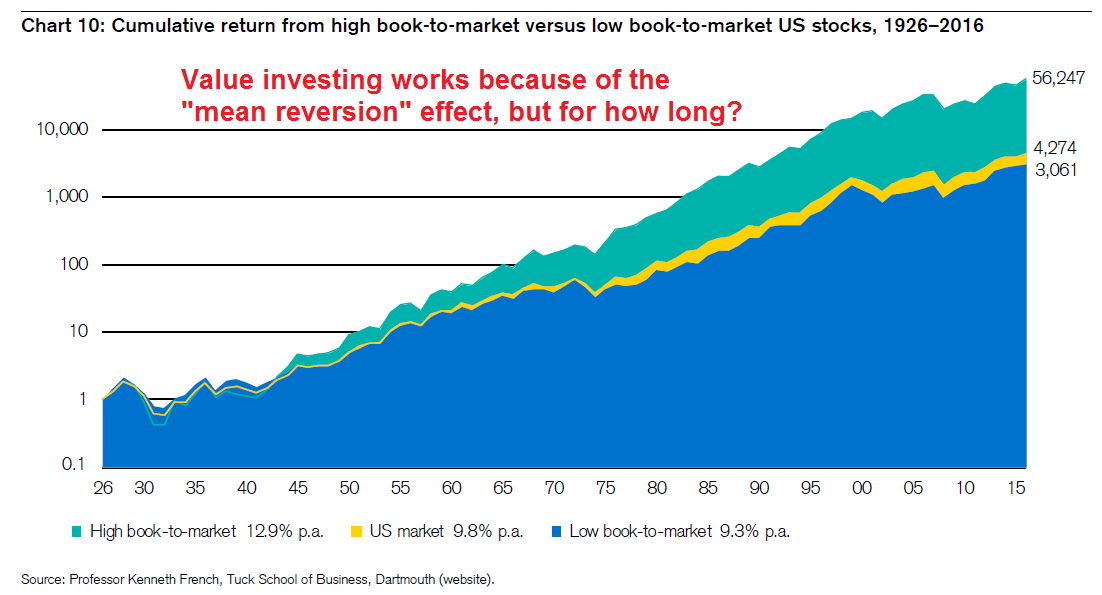

A value orientation, as proxied by a high price to book, outperforms the market. Buffett then couples the value discipline by buying companies with a moat, or a sustainable competitive advantage. The combination of buying value companies with a moat has been the secret of success.

However, we may be reaching an inflection point for Buffett`s brand of investing. In the Age of Trump, the tailwinds on Buffett`s value approach may be coming to an end.

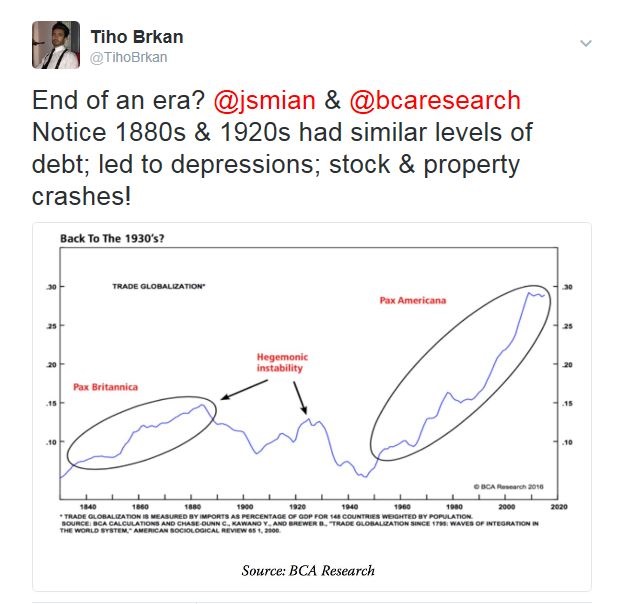

The end of Pax Americana?

This chart from BCA Research (via Tiho Brkan) tells the story. Buffett’s successful run coincides with the era of Pax Americana and rising global trade. What would happen if the growth in global trade were to come to a screeching halt? What kinds of stresses would the global economic system face?

Value investing depends on valuation a mean reversion effect, or the tendency of cheap stocks to return to becoming more reasonably priced. What if mean reversion were to stop occurring? What would happen to some of those business moats if global trade were to start shrinking?

Donald Trump’s America First policies certainly raises the risk level. Politico reported last week that Trump wants to re-negotiate trade treaties upon a moment’s notice whenever the US gets into trouble:

Trump has said he wants to include a clause in trade agreements that would allow the United States to get out within 30 days if the other country balks at fixing any problem that occurs. Last week, White House trade adviser Peter Navarro upped the ante by telling Senate Finance Committee members that the administration also wants to include a provision that would trigger a renegotiation whenever the United States runs a trade deficit with the partner country, Morning Trade has learned.

WTF? This is the same Peter Navarro who dismissed analysis from Citigroup outlining how retailers would be losers under a Border Adjustment Tax (BAT) as “fake news” (via Business Insider):

CNBC’s Melissa Lee pointed to a Citigroup estimate that said this new tax would be a massive hit to company earnings. That means people working in retail would likely lose their jobs as companies try to cut costs.

Navarro immediately got defensive.

“Well, first of all, this is a false narrative and a fake study,” he countered.

Lee was a bit surprised. “Let me get this right,” she said, “Citigroup did a fake study?”

“Citigroup has no credibility,” Navarro said. He called the bank’s analysis, and analysis from the Peterson Institute for International Economics, “garbage studies and scare tactics” and compared them to media outlets like MSNBC and CNN.

“We are not backing off,” he said.

Lee pointed out that Citigroup isn’t the media — it’s research written for investors looking to find out if companies are healthy. Navarro ignored that point.

“Yeah, well, the Dow just hit 20,000, how you like them apples?” he said. “There are winners and losers.”

America First Protectionism = EM debt crisis

If the Trump administration is intent on going down that trade policy path in the name of “America First”, then the risks are rising very, very quickly. Here is one immediate problem that market analyst and Texas Republican John Mauldin is worried about:

Paul Ryan and House Ways & Means Committee Chair Kevin Brady know everything I just said and probably agree with much of it. They believe the BAT’s negative effects will disappear quickly due to currency flows. As the trade deficit shrinks, fewer dollars will flow from the US to the rest of the world. That trend will make the dollar rise against other currencies, thereby nullifying the higher prices we will pay for imported goods.

That’s the theory. In fact, most economists do agree that the dollar is likely to rise significantly if this proposal is adopted. So, the theory is that Walmart shoppers really won’t pay higher prices, at least in dollar terms. I do not think things will work that way in practice, at least not as quickly as they hope…

Here we see once again how debt constrains us from doing what might otherwise make sense. Emerging-market countries own massive amounts of dollar-denominated debt. A stronger dollar means they must somehow come up with more of their local currencies to repay their dollar debts. And they will have to do it fast, even as their exports are shrinking because US consumers are being encouraged to “buy American.”

It gets worse. To whom is all that emerging-market debt owed? Primarily to Western banks and bondholders, who are often themselves excessively indebted. The potential financial contagion is massive. Ambrose Evans-Pritchard of the London Telegraph describes it in his characteristically colorful style:

Yet getting there constitutes a global shock of the first order. “This will trigger a series of emerging market crises,” said Stan Veuger from the American Enterprise Institute. He estimates that the burden for companies and states in developing countries with dollars debts will jump by $750bn. Turkish firms alone would face a $60bn hit.

It does not end there. Studies by the Bank for International Settlements show that a rising dollar automatically forces banks in Europe and the Far East to shrink cross-border lending through the mechanism of hedge contracts.

A dollar spike of anywhere near 20pc would send the Chinese yuan smashing through multiple lines of psychological resistance. The People’s Bank (PBOC) is already intervening heavily to defend the line of seven yuan to the dollar. Ferocious curbs would be needed to stop the Chinese middle classes funneling money out of the country if it crashed by a fifth.

Junheng Li from Warren Capital says the China’s exchange regime is more brittle than it looks. Official data overstates the PBOC’s fighting fund by $1 trillion, either because reserves are “encumbered” by forward dollar sales or because they must be held in reserve as a “fiscal backstop” for Chinese firms at risk of default on dollar debts. She expects the system to snap at any time, and without warning.

I strongly doubt whether the Trump-Ryan axis in Washington has any idea what could happen if they detonate a debt-deflation crisis in China, or if they ignite a short-squeeze on $10 trillion of off-shore dollar debt with no lender-of-last-resort behind it. Nor do they care.

A surging USD from the imposition of a BAT could spark another emerging market currency crisis. This time, the world won`t have the benefits of rising global trade to cushion the blow.

When confidence cracks

The blogger Jesse Livermore at Philosophical Economics wrote an insightful post last weekend about the interaction of valuation and cash in a low yielding world:

A useful way to estimate that value for a security you own is to ask yourself the question: what is the most you would be willing to pay for the security if you couldn’t ever sell it? Take the S&P 500 with its $45 dividend that grows at some pace over the long-term–say, 2% real, plus or minus profit-related uncertainty. What is the most that you would be willing to pay to own a share of the S&P 500, assuming you would be stuck owning it forever? Put differently, at what ratio would you be willing to permanently convert your present money, which you can use right now to purchase anything you want, including other assets, into a slowly accumulating dividend stream that you cannot use to make purchases, at least not until the individual dividends are received?

When I poll people on that question, I get very bearish answers. By and large, I find that people would be unwilling to own the current S&P 500 for any yield below 5%, which corresponds to a S&P 500 price of at most 1000. The actual S&P trades at roughly 2365, which should tell you how much liquidity–i.e., the ability to take out the money that you put into an investment–matters to investors. In the case of the S&P 500, it represents more than half of the asset’s realized market value.

Much of the valuation of equities in the current environment depends on confidence:

Now, here’s where the parallel to banking comes into play. As with a bank, a market’s liquidity is backed by a network of confidence among its participants. Participants trust that there will be other participants willing to buy at prices near or above the current price, and therefore they themselves are willing to buy, confident that they will not lose access to their money for any sustained period of time. Their buying, in turn, supports the market’s pricing and creates an observable outcome–price stability–that reinforces trust in it. Because the investors don’t all rush for the exits at the same time, they don’t have a need to rush for the exits. They can rationally collect the excess returns that the market is offering, even though those returns would be insufficient to cover the cost of lost liquidity.

When the network of confidence breaks down, you end up with a situation where people are holding securities, nervous about a possible loss of access to their money, while prevailing prices are still way above intrinsic value, i.e., way above the prices that they would demand in order to compensate for a loss of liquidity. So they sell whatever they can, driving prices lower and lower, until confidence in a new price level re-emerges. Prices rarely go all the way down to intrinsic value, but when they do, investors end up with generational buying opportunities…

The question comes up: in a low rate world, with assets at historically high valuations, offering historically low returns, what should investors do? Should they opt to own assets, or should they hold cash? The point I want to make in all of this is that to answer the question, we need to gauge the likely strength and sustainability of the market’s network of confidence amid those stipulated conditions. We need to ask ourselves whether investors are likely to remain willing to buy at the high valuations and low implied returns that they’ve been buying at. If the conclusion is that they will remain willing, then it makes all the sense in the world to buy assets and continue to own them. And if the conclusion is that they won’t remain willing, that something will change, then it makes all the sense in the world to choose hold cash instead.

Now imagine that global trade starts to unravel and EM countries experience a currency crisis, which morphs into a global financial crisis. What happens to confidence then?

If we want to get in front of things that are going to break a market’s network of confidence and undermine people’s beliefs that they’ll be able to sell near or above where they’ve been buying, we shouldn’t be focusing on valuation. We should be focusing instead on factors and forces that actually do cause panics, that actually do break the networks of confidence that hold markets together. We should be focusing on conditions and developments in the real economy, in the corporate sector, in the banking system, in the credit markets, and so on, looking for imbalances and vulnerabilities that, when they unwind and unravel, will sour the moods of investors, bring their fears and anxieties to the surface, and cause them to question the sustainability of prevailing prices, regardless of the valuations at which the process happens to begin.

Under that scenario, would buying the dip work? Could Berkshire Hathaway depend on the moats of these companies that Buffett purchased? How many of those moats would be breached if global trade tanks? Could you depend on the resiliency of a leaderless capitalist system when America is no longer willing to be its leader? What happens to the political systems of the leading industrialized countries in the world?

As per Credit Suisse, remember what happened the markets of major countries that underwent major political upheaval in the 20th Century:

Do you still want to bet on mean reversion and the sustainability of business moats under those kinds of scenarios?

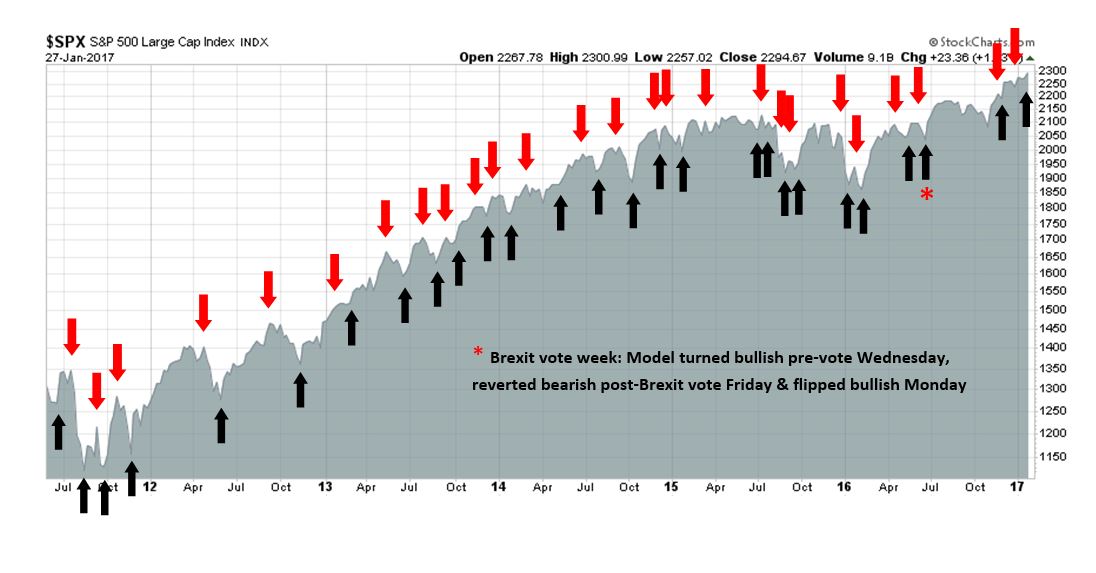

Preface: Explaining our market timing models

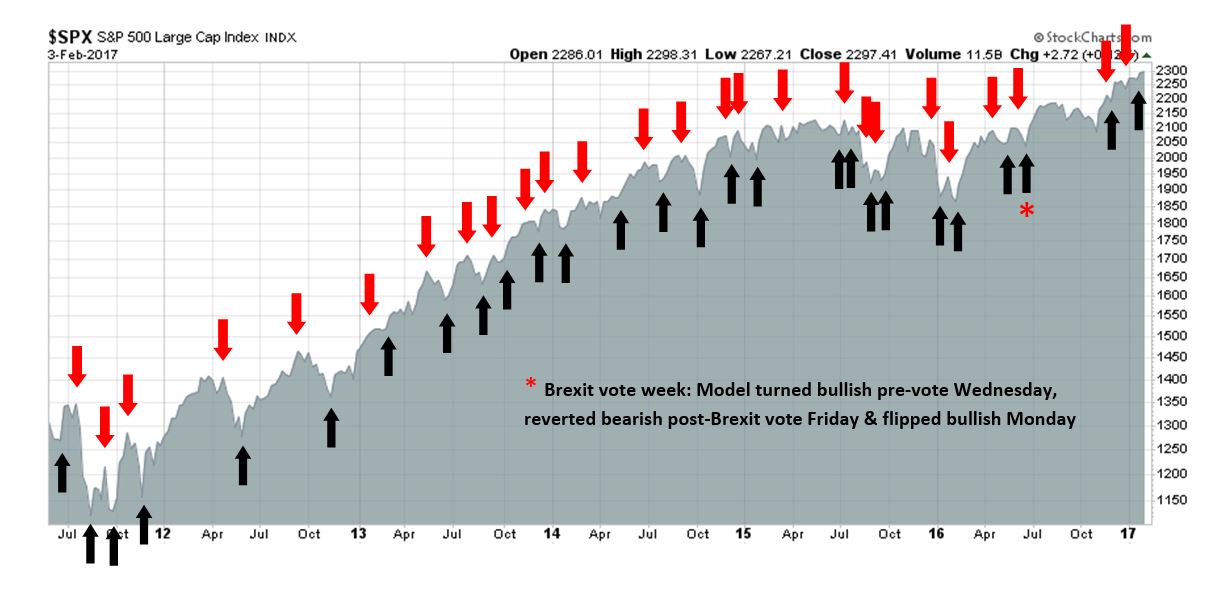

We maintain several market timing models, each with differing time horizons. The “Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Model is an asset allocation model which applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. In essence, it seeks to answer the question, “Is the trend in the global economy expansion (bullish) or contraction (bearish)?”

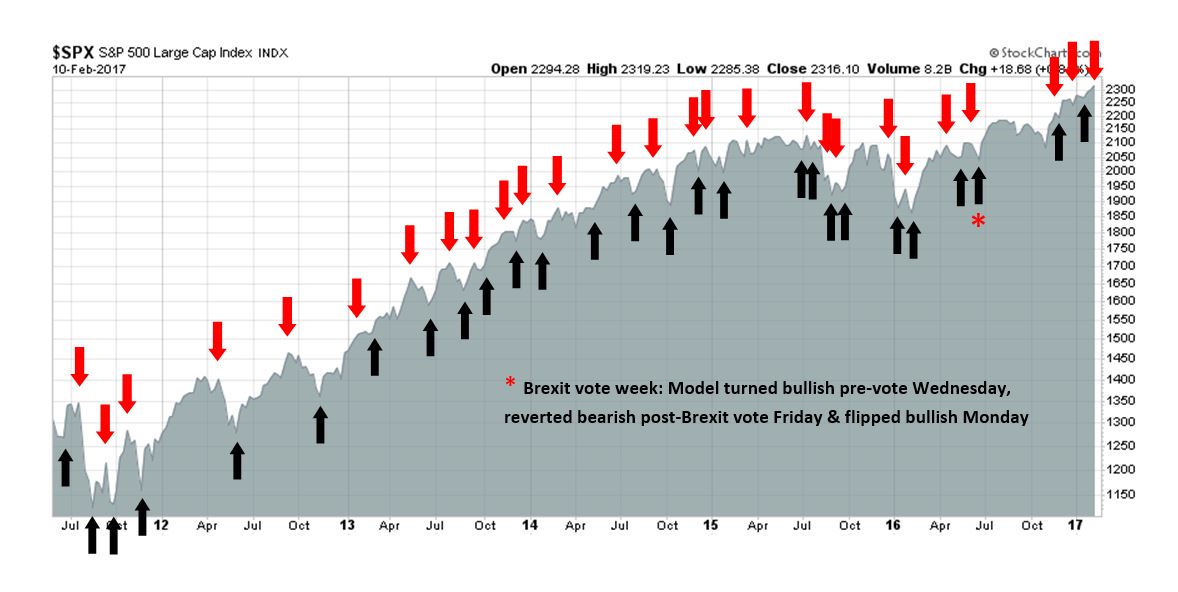

My inner trader uses the trading component of the Trend Model to look for changes in the direction of the main Trend Model signal. A bullish Trend Model signal that gets less bullish is a trading “sell” signal. Conversely, a bearish Trend Model signal that gets less bearish is a trading “buy” signal. The history of actual out-of-sample (not backtested) signals of the trading model are shown by the arrows in the chart below. Past trading of the trading model has shown turnover rates of about 200% per month.

The latest signals of each model are as follows:

Ultimate market timing model: Buy equities

Trend Model signal: Risk-on

Trading model: Bearish

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers will also receive email notices of any changes in my trading portfolio.

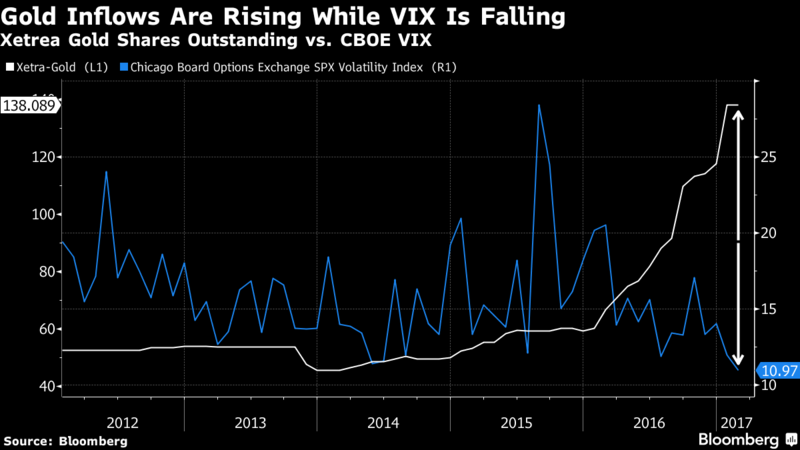

Sell the news?

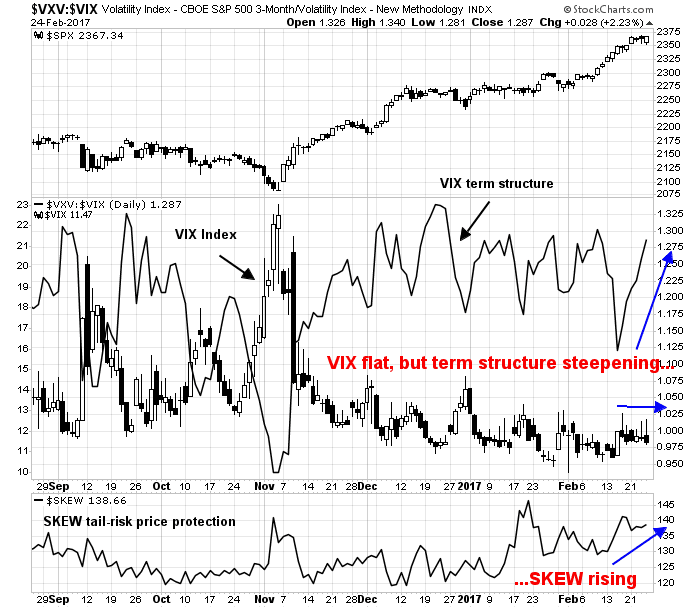

There has been much written lately about low level of stock market volatility, as measured by the VIX Index. It’s interesting that these concerns have even surfaced in the latest FOMC minutes:

Financial asset prices were little changed since the December meeting. Market participants continued to report substantial uncertainty about potential changes in fiscal, regulatory, and other government policies. Nonetheless, measures of implied volatility of various asset prices remained low.

A little noticed change has occurred in the markets since mid-February. Even though stock prices were grinding upwards, VIX term structure began to steepen as 3-month VIX futures rose but 1-month VIX remained stable. As well, the bottom panel shows that SKEW, which measures the price of tail-risk protection, is rising. These readings indicate that the market is anticipating a near-term volatility event.

The most likely spark for a volatility event is Trump’s address to Congress on Tuesday, when he is expected to outline his tax reform proposals. This speech has the potential to raise the “uncertainty about potential changes in fiscal, regulatory, and other government policies”.

The stock market has rallied substantially in anticipation of Trump’s proposal of tax cuts, tax holiday for offshore cash repatriation, and deregulation. As Trump’s tax reform proposals become more clear, it is becoming evident that there are two likely outcomes. Either Wall Street will have to swallow the bitter pill of the protectionist measures of a Border Adjustment Tax (BAT), or they will get delayed and bogged down in Congress.

As the market has bought the rumor of tax cuts, it may now be time to sell the news.

Waiting for tax reform

Here is where we stand right on tax reform. In a recent Reuters interview, here is what Donald Trump said when asked about the prospects for tax cuts and deregulation:

“We’re going to have a corporate tax cut … anywhere from 15 to 20 percent (as a target for the corporate tax rate). … We’re going to have other things that are very good and we’re going to have a tremendous regulatory cut because the regulations are piled up on top of each other and you’ll have many regulations for the same thing within different industries and it’s out of control. The regulations in this country are out of control. And it makes it hard for businesses to even open in the United States. We’re going to get rid of a lot of the unnecessary regulations.”

That’s the good news. The bad news is they will likely be accompanied by a BAT as a way to pay for the tax cuts:

“It could lead to a lot more jobs in the United States. … I certainly support a form of tax on the border because everybody else does. We’re the only country, we’re one of the very few countries, possibly the only country, that has no border tax. And that’s not a tax to the consumer, because that’s going to be a tax to companies and it’s going to be a tax to other countries much more so than it is to the consumer. That’s a tax to other countries. And what will happen is, don’t forget there is no tax if we make our product in the United States. So I don’t consider it a tax. That’s a tax if companies are buying their product outside of the United States. But … if they make their product in the United States, there is no tax. So what is going to happen is companies are going to come back here, they’re going to build their factories and they’re going to create a lot of jobs and there’s no tax.”

For readers who are unfamiliar with the BAT concept, here is a discussion of BAT from market analyst and Texas Republican John Mauldin:

Under the BAT plan, imports will be penalized and exports rewarded, which, theoretically, in a perfect world without pushback, would leave our economy nicely balanced and undisrupted. That’s the idea. But I doubt it will happen that way, because the importers and exporters are not the same businesses.

A vast number of businesses import products from other countries and sell them to Americans. Toy companies are a good example. Virtually all the shiny presents under your Christmas tree were made outside the US. The companies that import them could be border-adjusted right out of business under the Better Way plan.

Here’s an example. Suppose you are a toy company and you spend $1 million to bring in toys from China. You package and distribute them to retailers around the country, generating an additional $500,000 in costs for yourself. You sell them at wholesale for $2 million. What’s the tax consequence?

You just spent $1.5 million to generate $2 million in revenue. But the $1 million you spent on the imports is no longer deductible on your tax return. So your taxable profit isn’t $500,000, it’s $1.5 million. At 20%, your corporate income tax is $300,000 instead of $100,000. This plan triples your taxes…

At best there will be an adjustment period, which will be far longer than those who propose this plan think, as workers retrain for new jobs. We’ve heard this story before, and it didn’t work out as advertised. So count me skeptical.

The problem is that the importers and exporters don’t all operate in the same states and counties, so the people who lose their jobs because of the import tax will end up having to move to where the exporting jobs are. How did that work out for the Rust Belt when the steel jobs left? For whatever reason, the data clearly shows we are moving less than we ever have before.

Liberty Street Economics, a blog run by the New York Fed, which believes that a BAT is unlikely to substantially promote exports:

How will U.S. exporters fare? An unintended consequence of the proposed border tax is that it is likely to depress rather than stimulate exports. As export prices are also invoiced in U.S. dollars, the tax exemption on export revenue will mostly boost exporters’ profit margins rather than increase their export sales. And with the accompanying partial appreciation in the U.S. dollar, the prices of U.S. exports in foreign currencies will rise. This will provide incentives for our trading partners to switch their demand away from U.S.-produced goods, resulting in lower U.S. export sales.

Those are just the first order effects. John Mauldin thinks that a BAT will set off a global trade war:

When you talk to Republican leaders and ask them why other countries wouldn’t react to the BAT and impose larger tariffs or sanctions on US goods, they respond with a question of their own; and it’s a logical one: “But why would they? We’re only doing with the BAT what they’re already doing to us.” And they are correct. US corporations are at a massive competitive disadvantage today because we have high corporate taxes and no VAT. Other nations do not charge a VAT tax when their companies export products. That means a German car sold in Asia or a Japanese car sold in Europe has a competitive tax advantage over a car made in the US and on sale in those countries. The Republicans are simply trying to rectify that competitive disadvantage.

The problem is that other countries are simply not going to say, “Oh, the United States finally figured it out that we were taking advantage of its silly, complicated tax system. There’s really nothing we can do, so let’s just get on with the program.” No, they are going to protect their own businesses. In international trade, it’s every country for itself. They are all going to react to losing anything that they think is a competitive advantage. If you don’t get this, go back to kindergarten and study children trading toys in their sandbox. This behavior is ingrained in every human being.

Mauldin concluded (remember, he is a long-time Texas Republican):

I know this is going to offend a few of my friends, but I’m going to say it anyway: I am afraid that this border adjustment tax, if implemented, will throw the world into a global recession. All of the wonderful tax cuts and beautiful plans that are being proposed along with the BAT will not be enough to keep the US from participating in that recession as well.

Understand, I’m a believer in free markets, and I know that the American enterprise and entrepreneurial system, when given an opportunity, can respond and create growth in this country. But the BAT is not the way to do it.

That’s just the pushback from the “moderate” wing of the GOP. Here is an example of the opposition to BAT from the right wing of the party (via Breibart):

The latest solution from GOP “leadership” grab bag of bad ideas is the ill-conceived proposal to “help” America with her huge ($491 billion) global trade deficit with the Border Adjustment Tax (BAT).

The idea goes like this: The U.S. will tax all imports at 20 percent and provide a rebate of 20 percent on American exports sold abroad. That is not only counterproductive from a trade deficit reduction standpoint; it is skewed to help large American corporations over small and mid-sized American producers…

The solution is the scaled tariff. The tariff looks at the trailing twelve months (TTM) of trade balance between other nations and the United States. The tariff would only be applied to countries that have a significant or chronic surplus with the United States. The tariff would be adjusted quarterly up or down based upon the (TTM) figures. As trade heads toward balance, the tariff will self-adjust downward for that country. If a trading partner retaliates with counter-tariffs or currency manipulation that drive a greater deficit, the tariff will rise in direct relation to the (TTM) figures.

Any BAT will be a bitter pill for the equity market to swallow in order to get its tax cuts. A scaled tariff will even be worse.

Legislative chaos

The other likely scenario is a delay of the tax reform as it gets bogged down in Congress. The Hill reported that Ryan’s tax reform plan won’t get more than ten votes in the Senate:

Sen. Lindsey Graham (R-S.C.) says the House GOP tax plan that Speaker Paul Ryan (R-Wis.) tried to sell to Senate Republicans won’t get 10 votes in the upper chamber.

If Graham is correct, it’ll be a blow for Ryan and House Ways and Means Committee Chairman Kevin Brady (R-Texas), who are pushing a 20 percent across-the-board tax increase on imports to pay for comprehensive tax reform.

The idea has run into staunch resistance in the Senate, which bodes ill for President Trump’s hopes of passing tax reform this year.

The Trump administration is still not fully staffed, which is going to slow down its legislative agenda. Business Insider reported that Trump will delay its proposals for infrastructure spending to next year’s legislative calendar. In addition, AP (via Business Insider) reported that the Trump administration also faces a looming debt ceiling fight and possible government shutdown this spring:

Add a potential government shutdown to embattled President Donald Trump’s growing roster of headaches.

Beneath the capital’s radar looms a vexing problem — a catchall spending package that is likely to top $1 trillion and could get embroiled in the politics of building Trump’s wall at the US-Mexico border and a budget-busting Pentagon request.

While a shutdown deadline has a few weeks to go, the huge measure looms as an unpleasant reality check for Trump and Republicans controlling Congress.

Despite the big power shift in Washington, the path to success — and averting a shuttering of the government — goes directly through Senate Democrats, whose votes are required to pass the measure. And any measure that satisfies Democrats and their new leader, Sen. Chuck Schumer of New York, is sure to alienate tea party Republicans. Trump’s determination to build his wall on the US-Mexico border faces a fight with Democrats, too.

In effect, the market is faced with the unpalatable choice of BAT, or a delay of expected tax cuts until next year, with no idea of how the water down the proposals will be.

Good news, and bad news

If investors had bought the rumor of the tax cuts, does that mean that they should now sell the news?

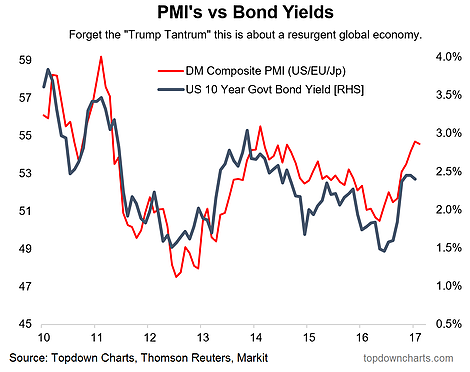

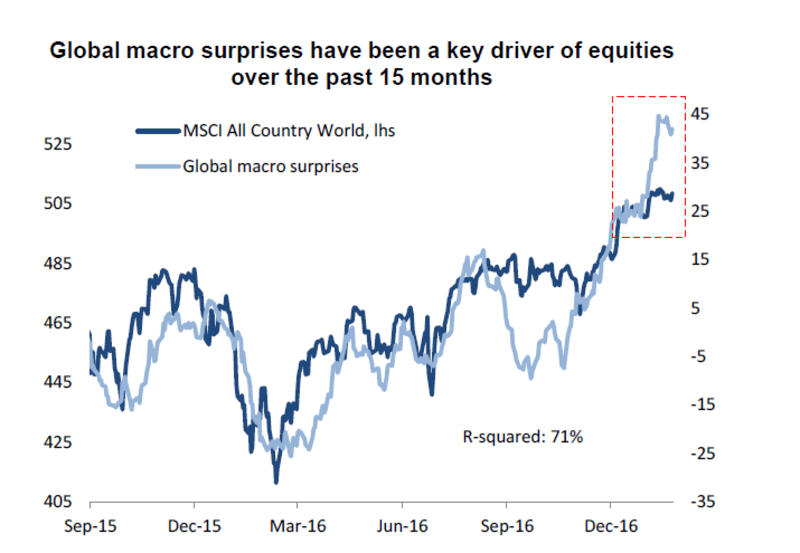

Before making a decision on that question, there is some good news and bad news about the market. Here is the good news. The market rally was sparked mainly by a reflationary growth rebound. As these charts from Callum Thomas of Topdown Charts show, the rebound is broad and global in scope.

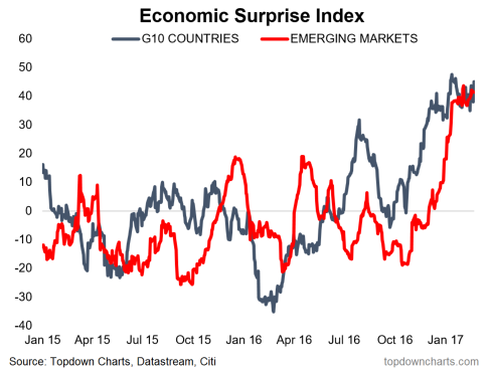

There has also been a surge in global Economic Surprise Indices, which measure whether top-down economic indicators are beating or missing expectations.

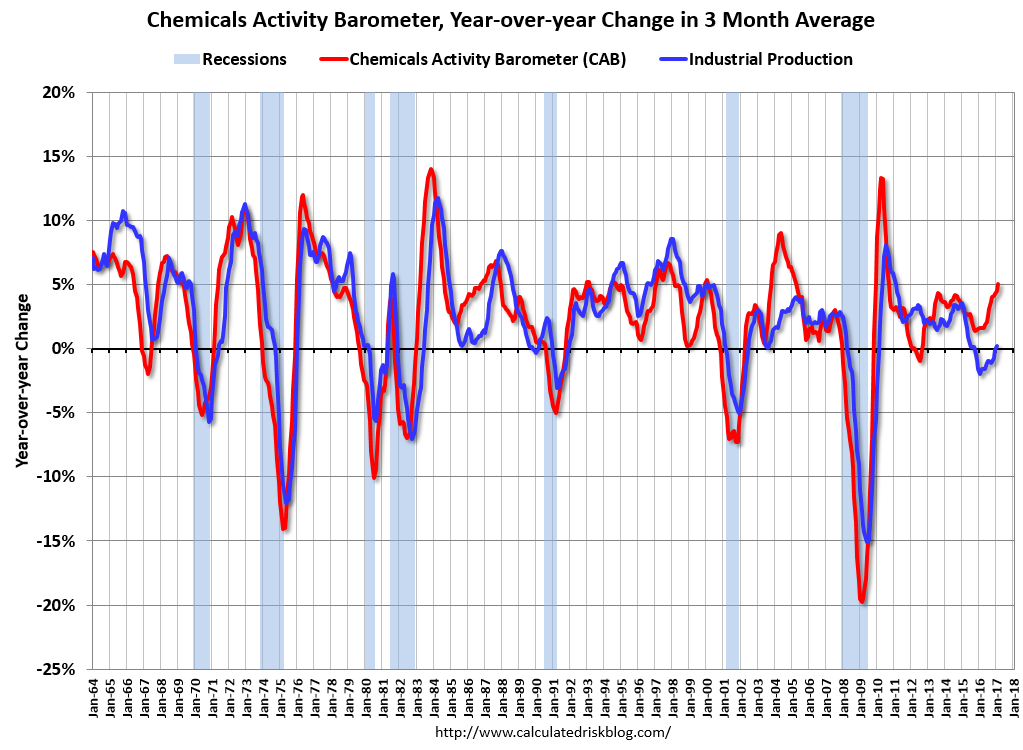

Specific to the US, the Chemical Activity Barometer, which leads industrial production, is also rising strongly (via Calculated Risk):

The good news is global macro momentum is pointed upwards.

As good as it gets?

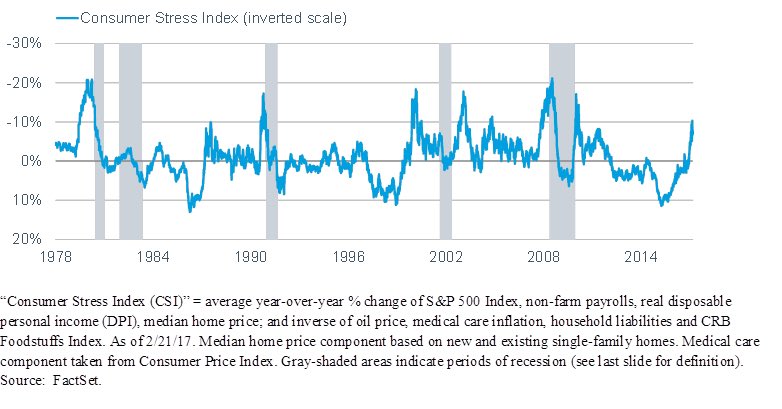

The bad news is conditions may be as good as they get. Liz Ann Sonders observed that consumer stress is rising. While readings are not at danger levels, it does hint at a loss of positive momentum.

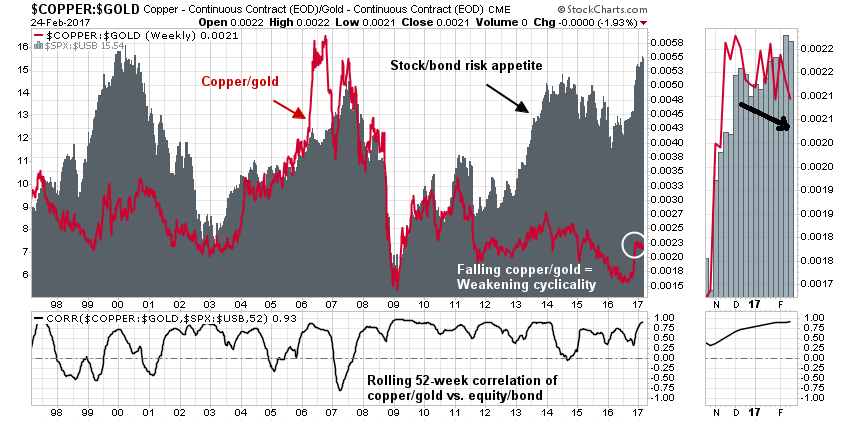

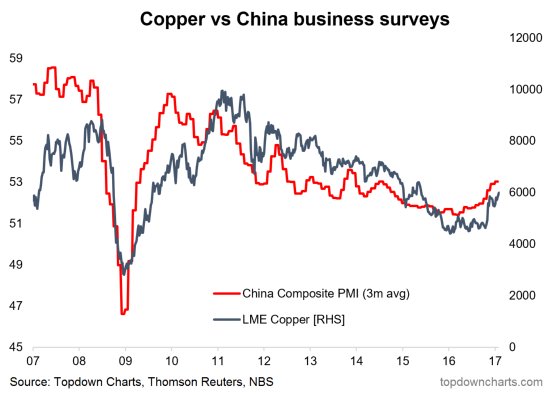

Copper prices, which is an indicator of the global cycle, are starting to weaken. The chart below shows the copper/gold ratio (red line) and the equity/bond ratio (grey bars). While both copper and gold are hard assets, copper has a greater cyclical element and therefore the copper/gold ratio is a sensitive barometer of global cyclical demand. The stock/bond ratio is a measure of market risk appetite, and it has historically been highly correlated to the copper/gold ratio (bottom panel).

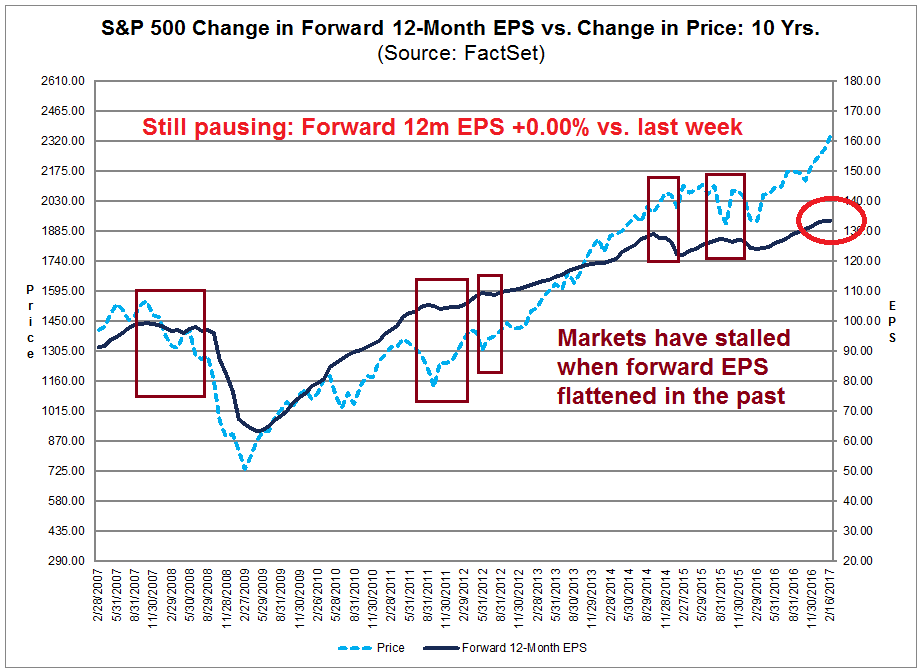

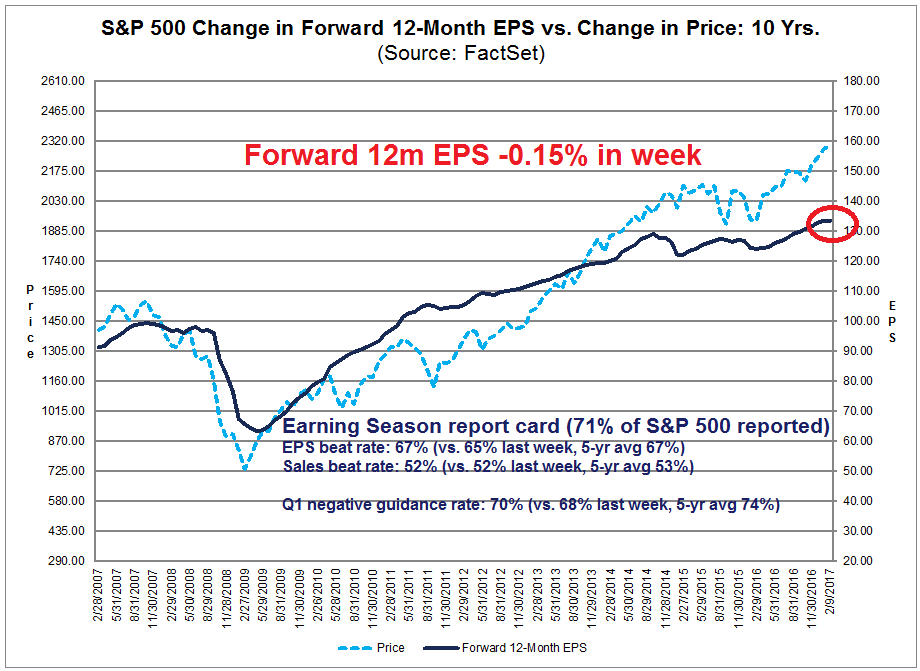

The latest update from Factset shows another sign of stalling momentum Forward 12-month EPS was flat compared to last week and fell compared to two and four weeks ago (annotations are mine).

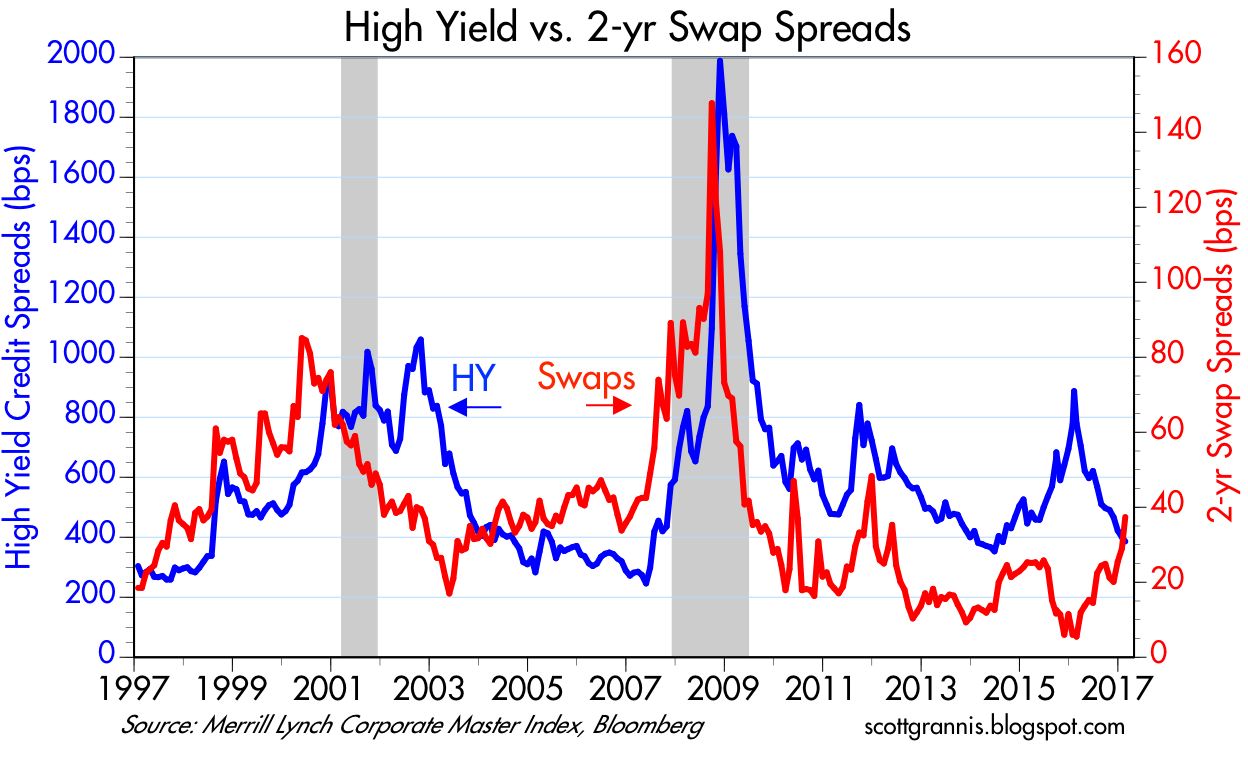

Scott Grannis also pointed out that the 2-year swap rate is starting to rise, indicating higher stress levels. Again, these are not panic levels, but this is another warning sign of declining risk appetite.

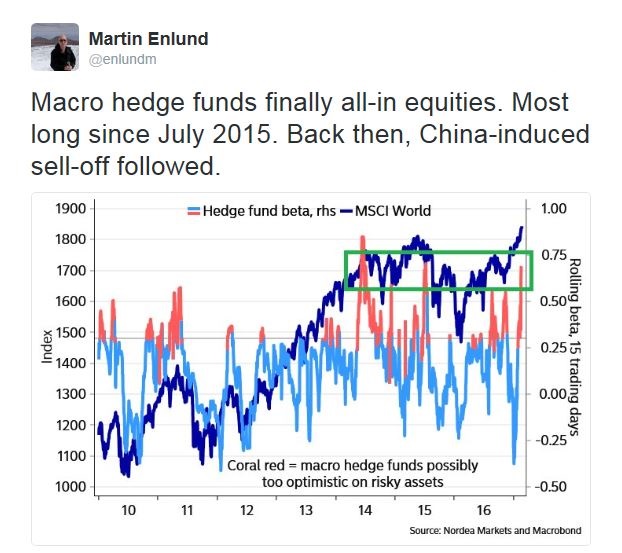

What’s more, global macro hedge funds are all-in on their risk exposure.

Bloomberg reported that analysis by Novus Partners showed that equity holdings favored by hedge funds are showing low levels of liquidity. So what happens if we get a “volatility event” and they all try to head for the exit?

Is it any wonder why demand for tail-risk protection is rising?

Estimating downside risk

I believe that the prudent course of action for investors would be to prepare for some near-term equity weakness. In that case, the question the becomes, “What’s the downside risk?”

I offer a number of scenarios to answer that question. Urban Carmel pointed out that, from a technical perspective, the stock market has exhibited a period of strong positive momentum. Such episodes tend to resolve themselves with only minor pullbacks before powering higher:

When the current uptrend ends, it is not likely to lead directly into a more significant downturn. Momentum like this weakens before it reverses. In each of the cases highlighted above, after a 3-5% drawdown, SPX either continued higher or retested the prior high before falling lower. Mid-2011, 2012 and 2014 are recent examples of the latter case (shown below). That would be our expectation now as well.

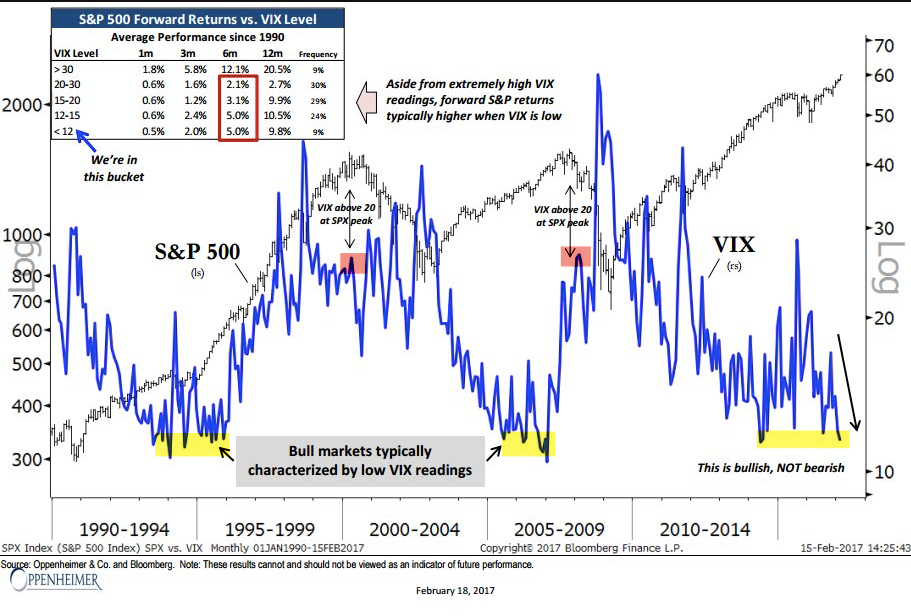

He also highlighted research from Ari Wald, indicating that low VIX levels tend to be bullish market environments, not bearish:

Much has been made of the persistently low level of the Vix. The three most recent bull markets have each been characterized by a persistently low Vix. Historical instances are severely limited, but a low Vix has been a positive sign for the SPX. The market did not peak in either 2000 or 2007 until Vix had climbed, over the course of years, to more than 25. Since 1990, when the Vix has been below 12, SPX has returned 5% and 10% over the next 6 and 12 months, respectively (from Ari Wald).

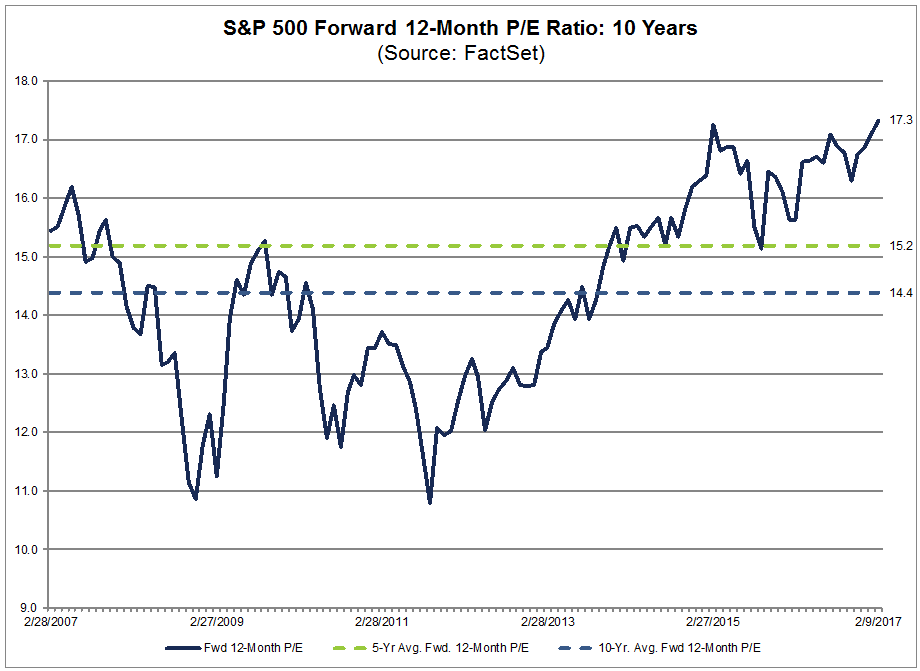

The fundamental answer to the downside risk question depends on how the tax reform measures get resolved. If the tax cuts were to be delayed until next year, then forward P/E ratios may have to adjust downwards. Analysis from Factset shows the forward P/E ratio at 17.6, a 14-year high. Forward P/E is well above its 5-year average of of 15.2 and 10-year average of 14.4. If the global reflation story were to remain intact, a 10-15% retreat in prices would represent a valuation floor for equity risk. I would add, however, that 10-15% represents the probable maximum downside potential, but any pullback could stop well short of that estimate.

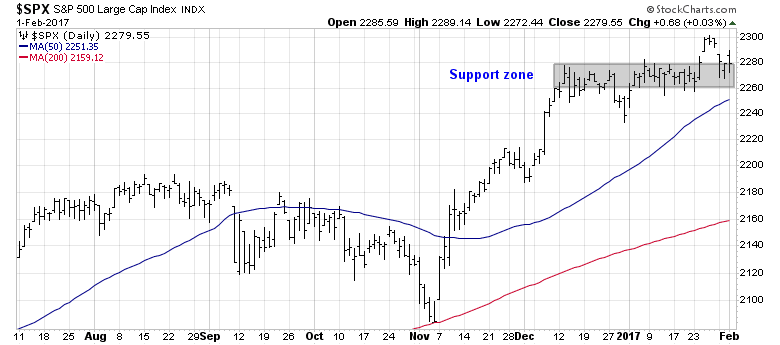

Confused? The following SPX chart offers some technical perspective. There is initial support at about the 2280 breakout point, which roughly coincides with the 50 day moving average (dma). Secondary support is at 2190, which also coincides with the 200 dma. If those support levels break, then long-term support can be found at 2135, which corresponds to about a 10% pullback. Viewed view a technical prism, a 10-15% pullback seems unlikely, unless total panic were to set in.

If, on the other hand, tax reforms were to pass with a BAT, then it could signal the start of a major bear market. As the chart below shows, global PMIs are closely correlated with global trade. Both have been rising strongly. Imagine the global macro conditions and growth outlook if trade flows were to tank. Earnings estimates would also fall, and would likely spark a major bear market, tax.

The week ahead: Waiting for the bearish break

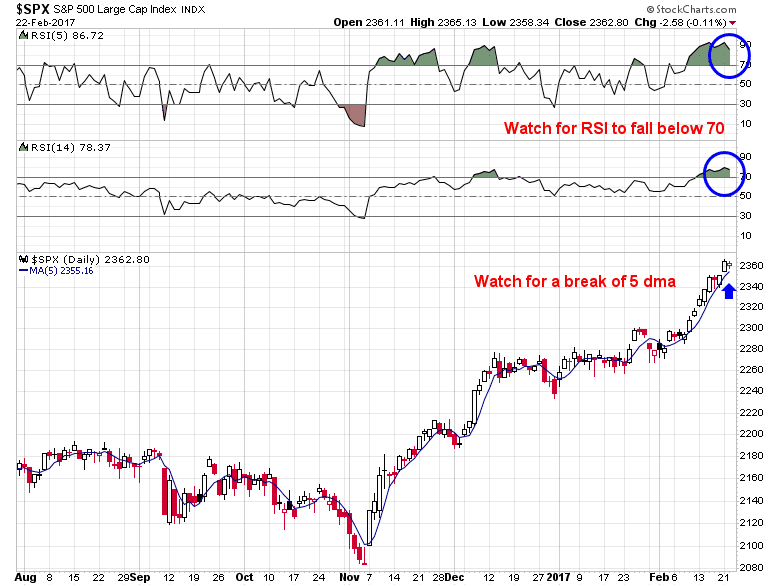

Looking to the week ahead, my inner trader continues to wait for the break in the equity market uptrend. While many technical and sentiment indicators are in the bearish zone, there is no obvious bearish trigger.

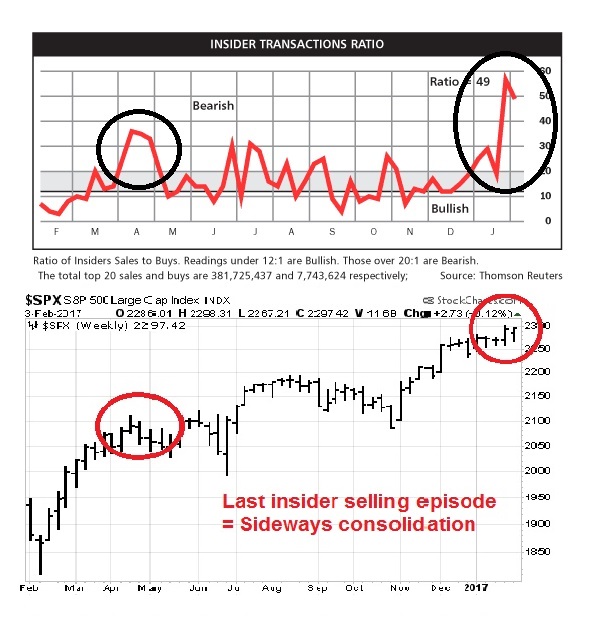

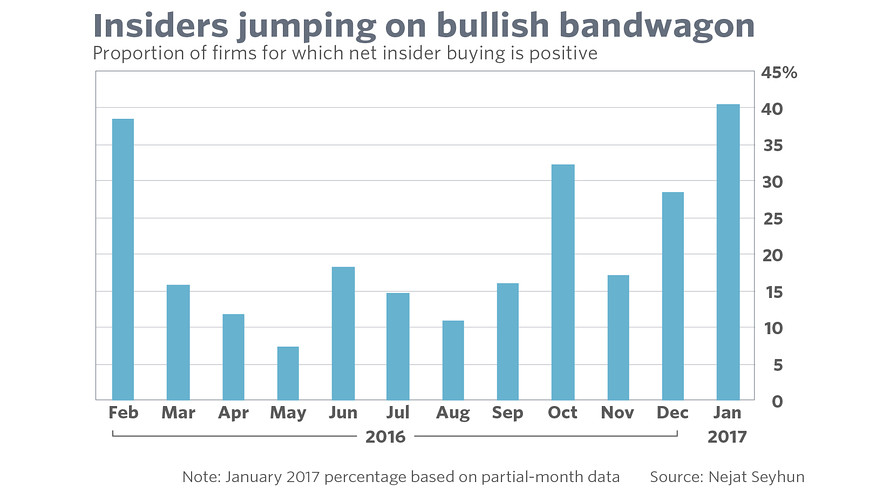

The latest update from Barron’s shows that insiders have resumed their heavy selling.

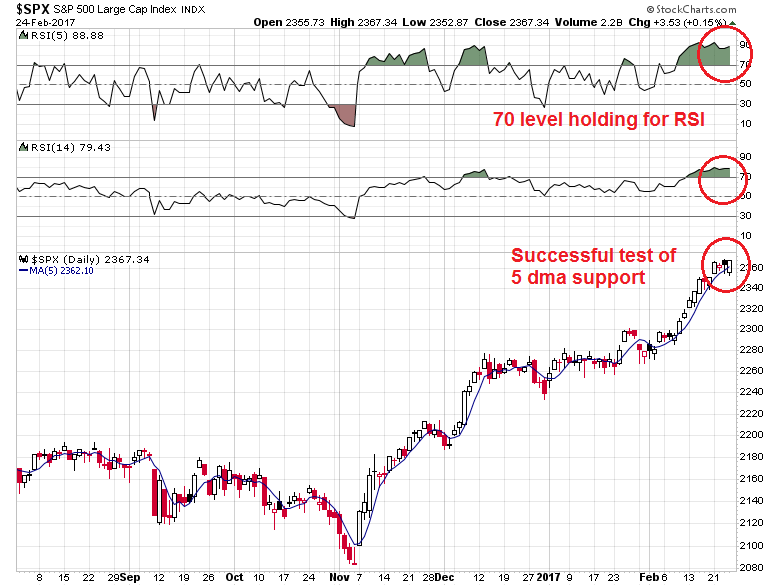

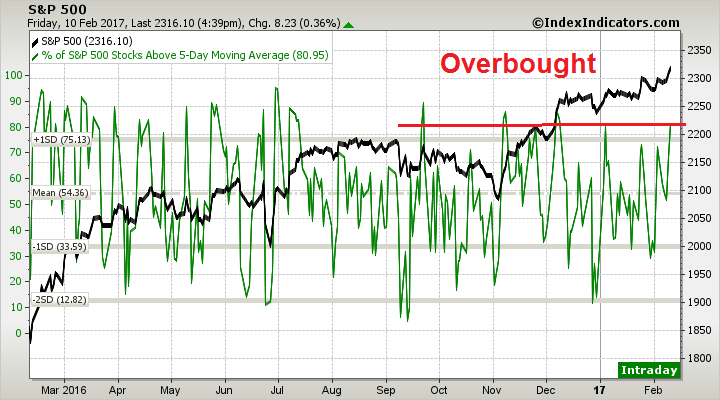

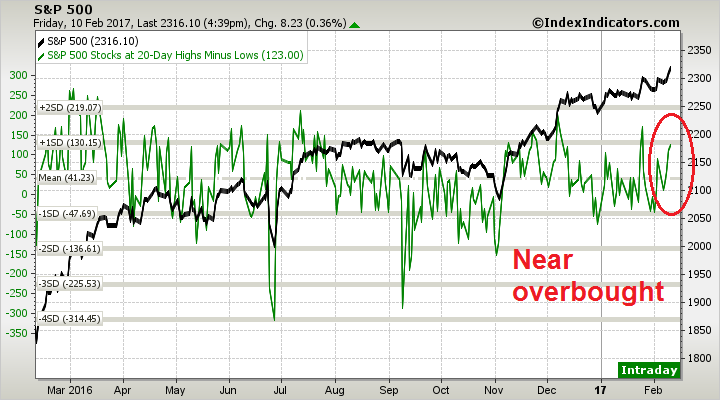

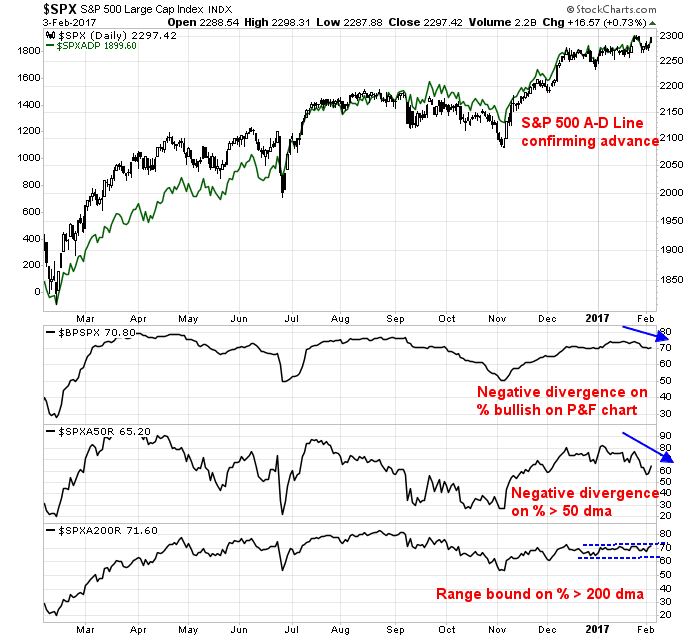

While these technical indicators are supportive of the near-term bear case, we haven’t seen technical breaks of the uptrend that marks a bearish break. Neither the SPX has fallen below its 5 day moving average, nor has its RSI-5 or RSI-14 have declined below the overbought reading of 70.

My inner investor remains constructive on stocks. He is not worried about 5-10% price squiggles when he invests in equities. On the other hand, he will take action to de-risk his portfolio should the more dire scenario of a trade war come to pass.

My inner trader remains in cash. He is still waiting for a technical break before he shorts the market.

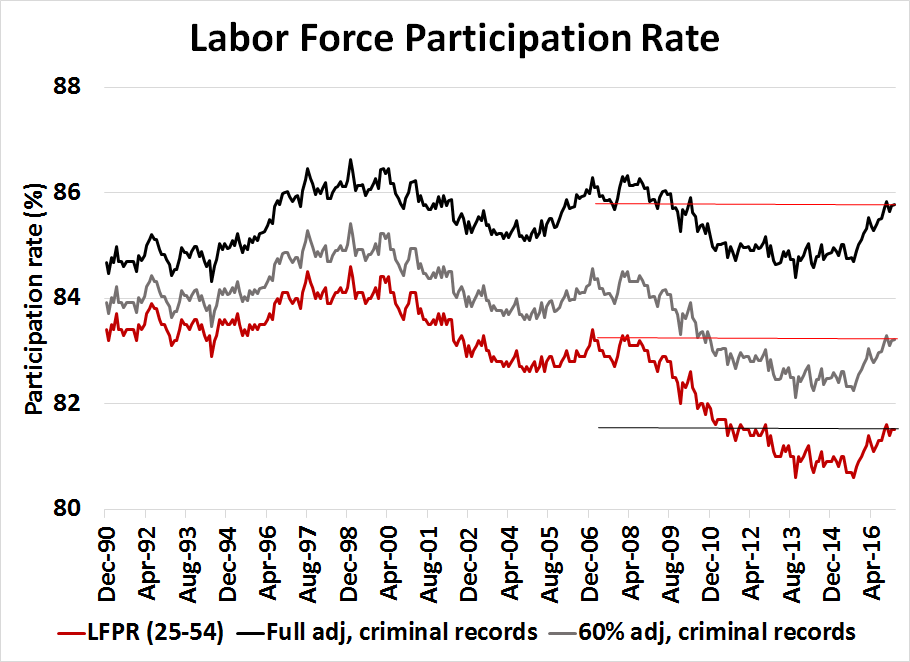

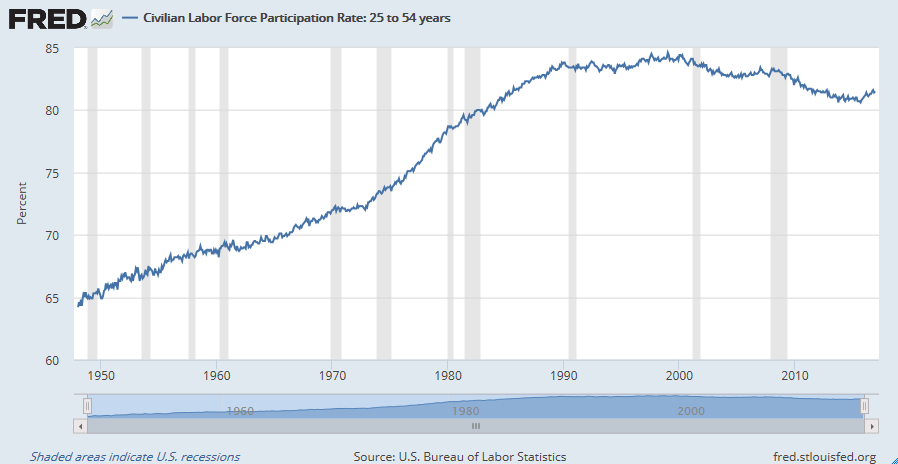

There has been much hand wringing by economists over the falling labor force participation rate (LFPR). As the chart below shows, the prime age LFPR, which is not affected by the age demographic effect of retiring Baby Boomers, have not recovered to levels before the Great Recession.

The lack of recovery in LFPR has caused great consternation over at the Federal Reserve. These readings suggest that there is still considerable slack in the labor market, despite the sub 5% unemployment rate.

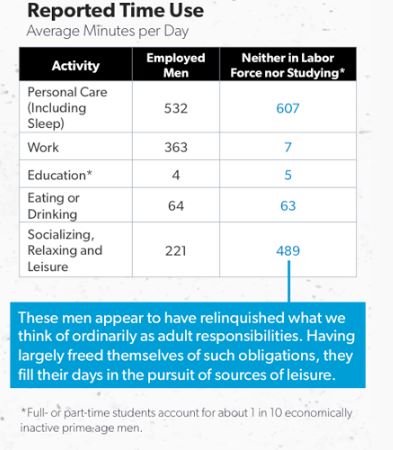

A number of explanations have been advanced for this phenomena, such as jobless Millennials spending all their time playing video games in their parents’ basement instead of looking for a job (via Nicholas Eberstadt of the American Enterprise Institute).

Another possible explanation is the growth of disability as a shield against unemployment payments run out. As the Great Recession hit, disabled workers became discouraged and chose to rely on their disability payments instead of trying to find another job.

There may be another very simple alternative explanation for the collapse in LFPR. The answer is so simple, it’s criminal that anyone missed it.

It’s criminal!

Nicholas Eberstadt of AEI, who advanced the theory of the lazy Millennials, suggested an very simple explanation. The explosion in the incarceration rate in the United States has rendered a segment of the population virtually unemployable, which consequently depressed LFPR (via Bloomberg):

A single variable — having a criminal record — is a key missing piece in explaining why work rates and LFPRs [labor-force participation rates] have collapsed much more dramatically in America than other affluent Western societies over the past two generations. This single variable also helps explain why the collapse has been so much greater for American men than women and why it has been so much more dramatic for African American men and men with low educational attainment than for other prime-age men in the United States.

The idea has some merit. Consider that the US has the highest incarceration rate of the major countries in the world, beating the likes of Russia, South Africa, and other industrialized countries (via Wikipedia):

Prison and jail populations have exploded over the years (via Wikipedia).

The problem isn’t just the number of people in prison and jail, but what happens to them when they are released. Research from the Sentencing Project found that 60% of former inmates could not find work a year after release.

That’s just people with criminal records. What if you were arrested but never convicted. The WSJ reports that the proliferation of private databases have created employment barriers for people with arrest records. These are people who were arrested, but not convicted. It could be something as simple as a misdemeanor offense, or a case of mistaken identity.

When Precious Daniels learned that the Census Bureau was looking for temporary workers, she thought she would make an ideal candidate. The lifelong Detroit resident and veteran health-care worker knew the people in the community. She had studied psychology at a local college.

Days after she applied for the job in 2010, she received a letter indicating a routine background check had turned up a red flag.

In November of 2009, Ms. Daniels had participated in a protest against Blue Cross Blue Shield of Michigan as the health-care law was being debated. Arrested with others for disorderly conduct, she was released on $50 bail and the misdemeanor charge was subsequently dropped. Ms. Daniels didn’t anticipate any further problems.

But her job application brought the matter back to life. For the application to proceed, the Census bureau informed her she would need to submit fingerprints and gave her 30 days to obtain court documents proving her case had been resolved without a conviction.

Clearing her name was easier said than done. “From what I was told by the courthouse, they didn’t have a record,” says Ms. Daniels, now 39 years old. She didn’t get the job. Court officials didn’t respond to requests for comment.

Could something like this happen to you?

Estimating the “criminal class” effect

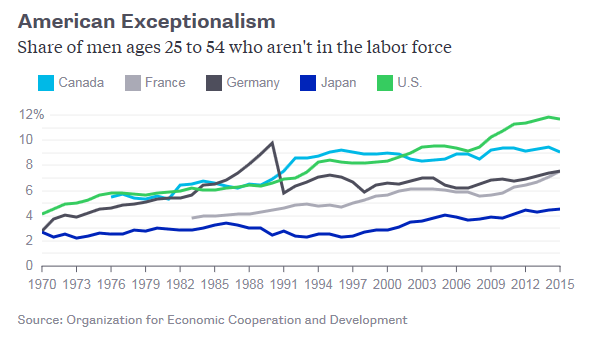

I have a couple of rough ways of estimating the “criminal class” effect on the LFPR. Using top-down data, the chart below from Bloomberg shows the differences between the “not in labor force” rate (NILF) between the US and other major industrialized countries. The latest data (2015) shows a 2.6% spread in NILF rate between the US and Canada. The NILF rates of those two countries last crossed in 2007. Before that, they crossed in 2001.

What if the American NILF rate fell to the Canadian rate due to an equalization of incarceration rates? As the chart below shows, if we add back the 2.6% US-Canada NILF spread, the US prime LFPR would jump to 84.1% (red dot), which is above the rate seen before the Great Recession, and slightly ahead of 2001 and 2007, when the NILF rates of the two countries last converged (black dots).

Bottom-up estimates

Another way I used to estimate the “criminal class” effect on the LFPR is to ask the question, “What if all former inmates found jobs as easily as the rest of the population?”

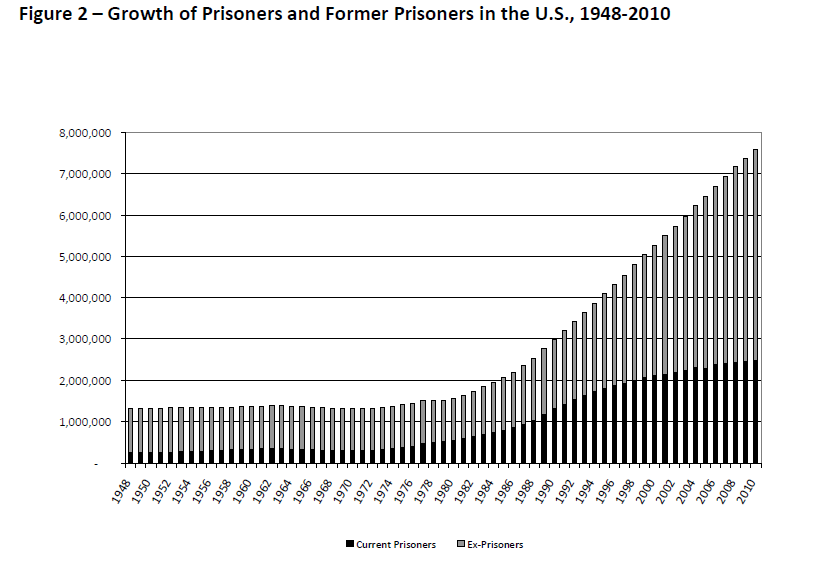

To answer this question, I used estimates by the academics Shannon, Uggen, Thompson, Schnittker and Massoglia in the paper “Growth in the US ex-felon and ex-prisoner population, 1948 to 2010“. I took the grey bars in this chart (ex-prisoners) as estimates of the former prisoner population.

The chart below adjustments to the LFPR, assuming different levels of difficulty for former inmate participation in the labor force. The red line shows the actual prime age LFPR (data from FRED). The black line assumes that all former inmates re-entered the labor force and none were discouraged. The grey line assumes that 60% of former inmates get discouraged and left the labor force (see Sentencing Project analysis above).

Based on this approach, the LFPR would have fully recovered from the Great Recession if we assume a full adjustment for people with criminal records. Assuming a 60% discouragement rate among former inmates, the LFPR has significantly recovered from the Great Recession effects, and the recovery is better than the unadjusted LFPR rate.

A feature, not a bug

I would add that this analysis assumes that there was no employment discouragement effect on people who were arrested but not charged. In reality, this “arrested but not convicted” category undoubtedly also had a depressing effect on the participation rate, as that population would have had sufficient difficulty in finding work that they would be more likely to leave the labor force than the general population.

In conclusion, using two separate approaches, I estimate that the surge in incarceration rate in the United States in the last couple of decades has dramatically affected labor force dynamics. The plunge in labor force participation rate is an unintended consequence of the country`s law-and-order focus. In other words, falling LFPR is a feature of past policy, not a bug.

As a result, the economy is likely far closer to full employment than standard unfiltered statistics, which has bullish implications for cost-push inflation. The slightly more hawkish tone of the latest FOMC minutes should therefore be taken as a welcome sign that the Fed will not fall behind the inflation fighting curve:

Many participants expressed the view that it might be appropriate to raise the federal funds rate again fairly soon if incoming information on the labor market and inflation was in line with or stronger than their current expectations or if the risks of overshooting the committee’s maximum-employment and inflation objectives increased.

Based on the results of this study, it could be argued that monetary policy should be on an even hawkish trajectory than three hikes in 2017.

Mid-week market update: Markets behave different at tops and bottoms. Bottoms are often V-shaped and reflect panic. Tops are usually slower to develop. Hence the trader’s adage, “Take the stairs up, and escalator down.”

I have been writing that the US equity market appears to be extended short-term and ripe for a pullback, but that was last week and about 1% lower (see Why the S&P 500 won’t get to 2400 (in this rally)). I stand by those remarks.

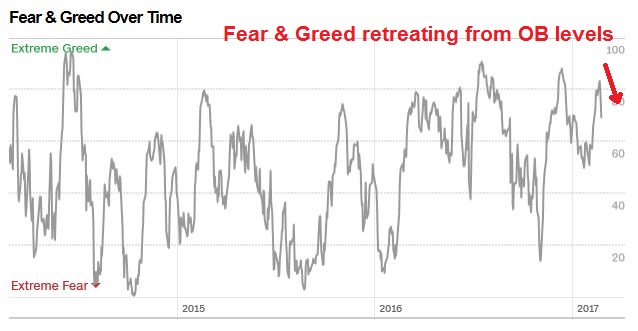

I could say that the Fear and Greed Index appears to be extended and historically stock prices have had difficulty advancing further with readings at these levels.

I could also say that Ned Davis Research Crowd Sentiment Poll is also extended. Historically, stock prices have exhibited a negative bias at these levels (via Tiho Brkan).

None of this matters much to short-term traders. That’s because sentiment and overbought/oversold indicators are less useful at tops than bottoms. While it may be timely for traders to tilt to the long side when panic starts to appear, market euphoria are not good trading signals of market tops. Savvy traders know to wait for a bearish break when the market gets overbought and giddy.

I am seeing some limited signs of a bearish break, but the trading sell signal is incomplete.

CBOE put/call sell signal

I recently highlighted the euphoric condition where the CBOE equity-only put/call ratio (CPCE) had fallen to below 0.60 for four consecutive days. A study showed that such overbought conditions resulted in subpar returns, but they were still positive.

The same study showed that when the market becomes overbought and mean reverts, CPCE rises above 0.60, forward returns tend to far more negative. That`s the bearish break that traders should be waiting for.

The signal appeared as of Tuesday’s close, when CPCE rose to 0.61 and Wednesday’s preliminary equity put/call ratio came in at 0.82. Those are sell signals.

Still waiting for other breaks

While the CPCE sell signal is encouraging for the bears, other short-term technical indicators have not flashed signals for my inner trader to commit funds to the short side. I am waiting for the SPX to fall below its 5 day moving average, which currently stands at about 2355. In addition, I am waiting for RSI-5 and RSI-14 to decline below 70 as signs of faltering momentum.

I would add that my cautiousness is tactical. Any pullback should be regarded as a correction within an uptrend unless proven otherwise.

My inner investor remains bullishly positioned. My inner trader is in cash, but he is waiting for a technical break to go short.

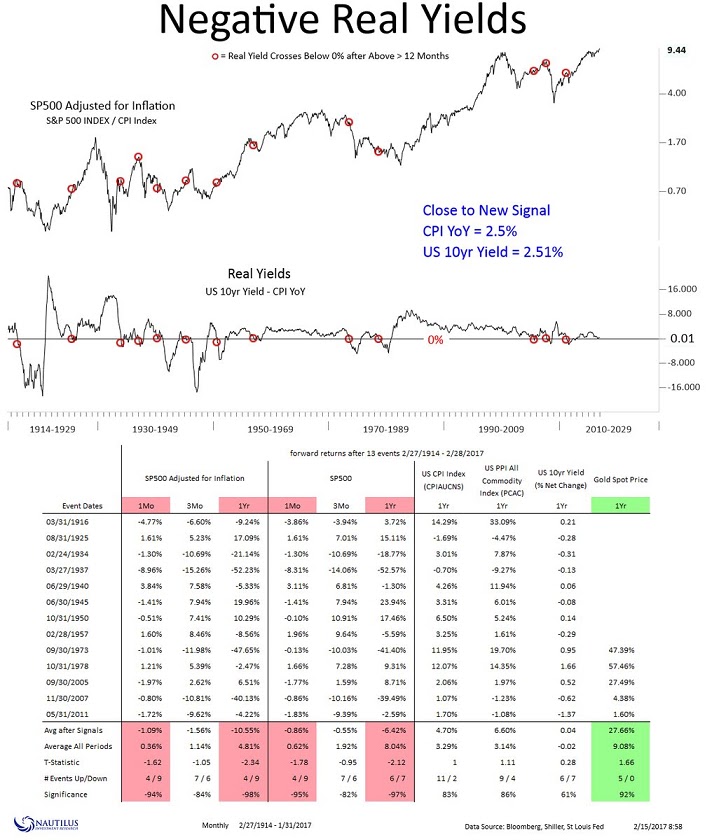

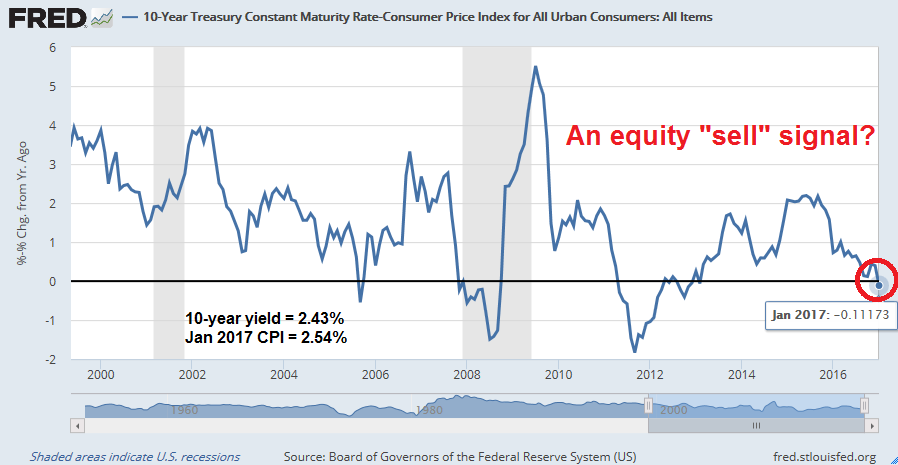

A reader asked me my opinion about this tweet by Nautilus Research. According to this study, equities have performed poorly once the inflation-adjusted 10-year Treasury yield turns negative. With real yields barely positive today, Nautilus went on to ask rhetorically if the Fed is behind the inflation fighting curve.

Since the publication of that study, The January YoY CPI came in at 2.5%, which was surprisingly high. The higher than expected inflation rate pushed the 10-year real yield into negative territory. So is this a sell signal for equities?

Well, it depends. The interpretation of investment models often depends a great deal on their inputs. In this case, the questions is how does we adjust for inflation? Do we use the headline Consumer Price Index (CPI), core CPI, which is CPI excluding volatile food and energy prices, or some other measure?

As I go on to show, how we adjust for inflation dramatically alters the investment conclusion for a variety of asset classes, like equities, gold, and the USD.

As is the case in the application any quantitative model, the devil is in the details.

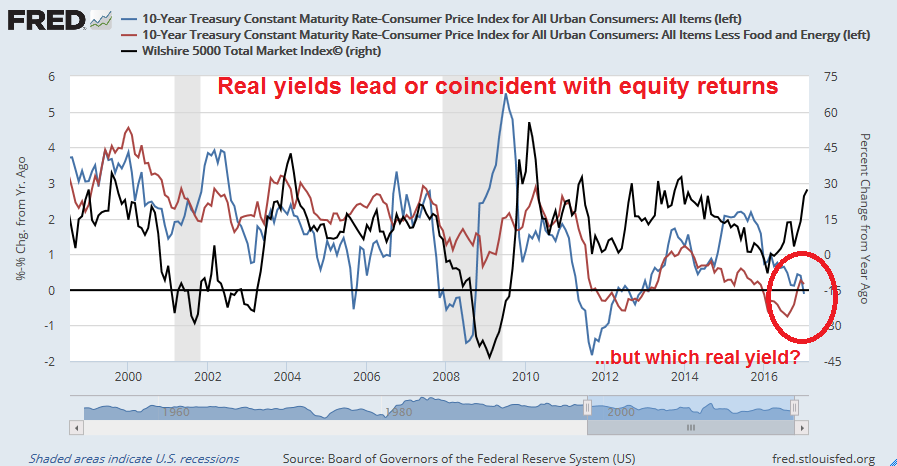

Real yields and equity returns

Consider the evidence. As the FRED chart below shows, history shows real yields indeed either lead or are coincidental with equity returns. If we adjust for 10-year Treasury with headline CPI, the outlook is equity bearish. On the other hand, adjusting with core CPI leads to a bullish conclusion.

Which inflation measure should we use?

Real yields and the USD

There is a more direct empirical relationship between real yields and the level of the US Dollar. As real yields rise, it puts upward pressure on the USD. So which inflation rate should we use?

Real yields and gold

Historically, the price of gold has been inversely correlated with the USD. Since gold is thought of as an inflation hedge, it is therefore no surprise that low real yields are gold bullish and high real yields are bearish (note the inverse scale for the gold price, right axis).

Our intermediate term outlook for these asset classes therefore crucially depend on the correct interpretation of the inflation adjustment factor. Do we use headline CPI, or the less volatile core CPI?

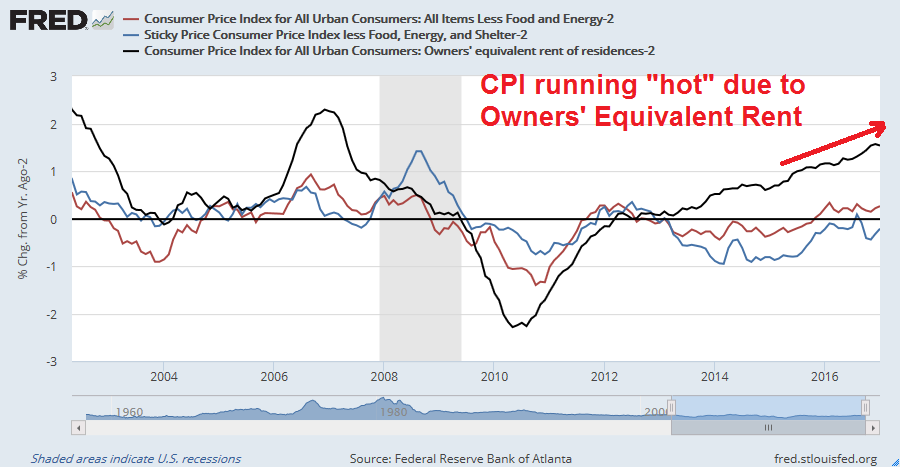

A “hot” CPI print

The CPI print last week came in ahead of expectations. YoY CPI was 2.5% (vs. 2.4% expected), and core CPI was 2.3% (vs. 2.1% expected). As I showed in my previous post (see Watch what they do, not just what they say), most of the strength in CPI was attributable to rising Owners’ Equivalent Rent (OER), which comprises of 25% of the weight of CPI and 31% of core CPI, according to the latest BLS figures. (Note that the chart subtracts 2% from each CPI metric so that we can easily see whether each is above or below the Fed’s 2% inflation target.)

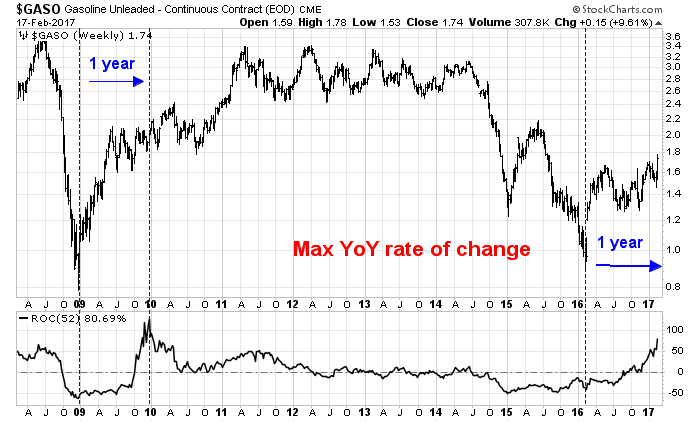

Much of the recent boost to headline CPI compared to core CPI is attributable to surging gasoline prices. As the chart below shows, YoY gasoline prices are due to peak and headline inflation should start to moderate in the months ahead.

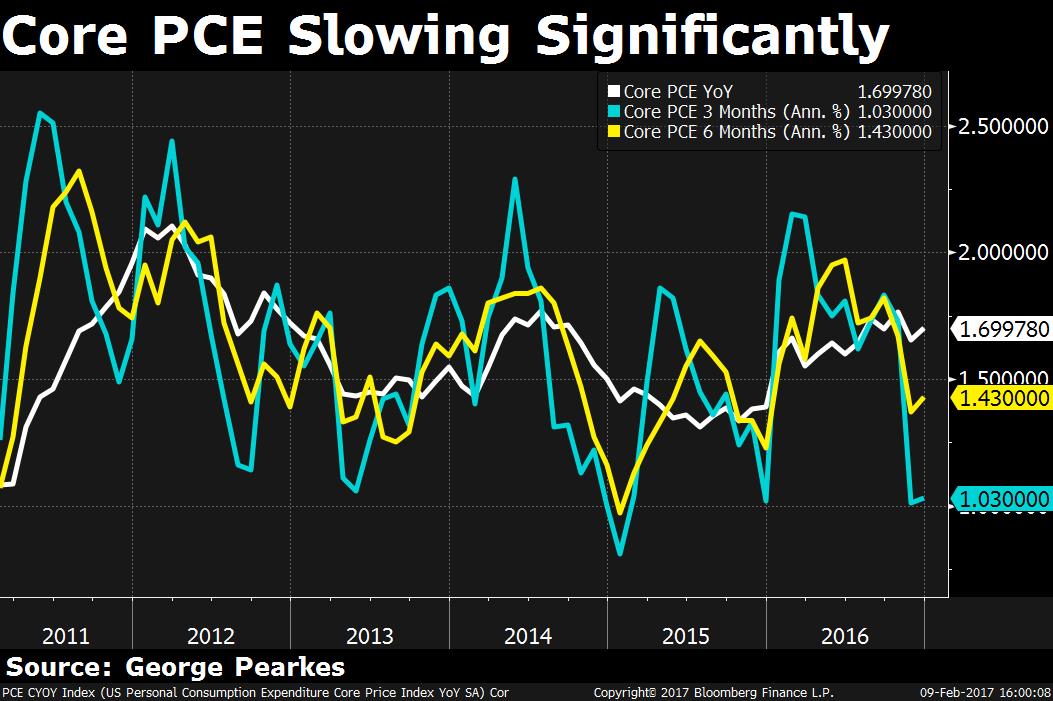

After dissecting the components of CPI, my conclusion is that inflation remains tame after stripping out the more volatile components and OER, which can be ignored for the purposes of this analysis. I have also highlighted past analysis from George Pearkes that core PCE, which is the Fed’s preferred inflation metric, has been slowing.

In conclusion, investors shouldn’t panic about negative real yields based on an erroneous interpretation of inflation. Unless conditions change dramatically, the intermediate term outlook for the USD and equities is bullish. Conversely, gold bulls will face headwinds from positive real yields.

Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Model is an asset allocation model which applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. In essence, it seeks to answer the question, “Is the trend in the global economy expansion (bullish) or contraction (bearish)?”

My inner trader uses the trading component of the Trend Model to look for changes in the direction of the main Trend Model signal. A bullish Trend Model signal that gets less bullish is a trading “sell” signal. Conversely, a bearish Trend Model signal that gets less bearish is a trading “buy” signal. The history of actual out-of-sample (not backtested) signals of the trading model are shown by the arrows in the chart below. Past trading of the trading model has shown turnover rates of about 200% per month.

The latest signals of each model are as follows:

Ultimate market timing model: Buy equities

Trend Model signal: Risk-on

Trading model: Bearish

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers will also receive email notices of any changes in my trading portfolio.

Great expectations

Bloomberg recently highlighted the huge gap between expectations and reality. As the chart below shows, soft (expectations) data has been surging, but hard (actual) data has risen, but it has not caught up with expectations.

The markets are pricing for perfection, which sets up a situation where minor disappointments could spark a market sell-off. BCA Research found that such divergences between “soft” expectations data and “hard” economic data has seen equity corrections in the past.

This week, I examine the details of how expectations have diverged from actual data on a number of dimensions.

Small business confidence

Corporate confidence

Consumer confidence

Federal reserve expectations

Wall Street’s tax reform expectations

Small business euphoria

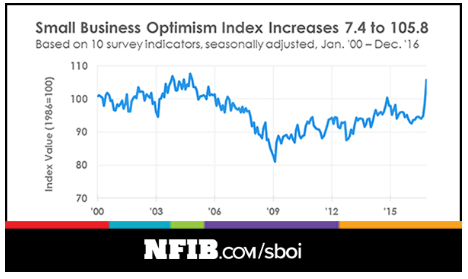

Last week`s release of the NFIB January small business confidence survey showed another upside surprise. Small business optimism continued to surge and rose to multi-year highs. As small business owners tend to be small-c conservatives who tend to tilt Republican, the election of Donald Trump has undoubtedly sparked a resurgence in business optimism.

However, the outpouring of optimism has not been matched by actual sales results. Even though sales ticked up last month, their rise lagged expectations. Since 1974, there have been five other episodes where expectations have surged. In two of those cases, sales rose to match expectations; in two others, they did not; and in 2009-10, sales saw eventually rose, but the surge was delayed by about a year (chart annotations are mine).

Small business capital expenditure plans have been relatively muted despite the surge in small business optimism.

One reason for the cautiousness could be attributable to rising labor costs. While labor costs have risen, business owners have not been able to raise prices to pass through higher compensation rates, which results in a margin squeeze.

I am keeping an open mind as to whether small business optimism will translate into more hiring and capital expenditures. But watch what small business owners do, not just what they say.

Corporate optimism

It’s not just the mood of small business owners that has become more upbeat. A simple word count of the word “optimistic” in earnings calls has surged to all-time highs.

But if management is so optimistic, then why have insiders been selling so much of their company’s shares (via Barron’s)?

Watch what corporate insiders do, not just what they say.

Can the consumer MAGA?

If Donald Trump is to Make America Great Again, then one of the key ingredients is strength in consumer spending. As the chart below shows, the US economy is seeing a divergence between rising consumer confidence (black line) and real wage growth (blue line). How can the consumer spend when real wages are stagnant? More worrisome is the observation that falling real wages have been precursors to recessions in the past, not booms.

Even though January retail sales rose and beat expectations, consumer spending is likely to disappoint in the short-term. That’s because after adjusting for inflation, real retail sales actually fell from December to January. In addition, Bloomberg reported that this year’s IRS anti-fraud tax refund procedural changes are delaying the timing of refund payments. This is likely to depress current consumer spending and push it out by several months.

New Deal democrat is becoming concerned. He wrote about the ways consumers cope if real wages don’t grow. When the consumer runs out of coping mechanisms, the economy slides into recession:

The theory is that if real average wages are not increasing, which for a long time beginning in the 1970s they were not, average Americans use a variety of coping mechanisms. From the 1970s through the mid-1990s, spouses entered the workforce, adding to total household income. Other methods have included borrowing against appreciating assets, and refinancing as interest rates declined.

Borrowing against stock prices ended in 2000. Borrowing against home equity ended in 2006. When interest rates failed to make new lows, the consumer was tapped out, and began to curtail purchases. Thus in September 2007, with the stock market peaking, house prices falling, interest rates having not made new lows in over 3 years, and real wage growth having stalled, I wrote that a recession was about to begin: http://www.dailykos.com/story/2007/09/25/389903/-Why-American-consumers-are-signaling-recession

So far, mortgage rates have not made a new low for quite some time, so forget housing prices as an ATM to fuel consumer spending. Another way of maintaining consumer spending is to reduce savings. The savings rate is dropping, but it is not at levels that have signaled recessionary conditions in the past. As major stock indices reach all-time highs, another way of coping is by taking profits on their stock portfolios , but only a small minority of households are invested in the equity market.

NDD concluded:

So the consumer fundamentals nowcast indicates that the expansion should continue for awhile, but if inflation eats up wage gains and the savings rate this year, then all we will need for the consumer to signal a recession is for asset prices to peak. I do not think that will happen until at least next year.

Don’t panic just yet, but risks are rising. Watch what the consumers do, not just what they say.

A hawkish Fed

What’s going on at the Fed? George Pearkes recently observed core PCE, the Fed’s preferred inflation metric, has been slowing.

So why did Janet Yellen take on a decidedly more hawkish tone in her Congressional testimony last week? In fact, the WSJ reported that Fed officials have fanned out across the country to reinforce the message that to expect three rate hikes in 2017, which is more hawkish than the market expectations.

To be sure, the Consumer Price Index (CPI) came in a bit “hot”, or ahead of expectations, both in the headline number and core CPI. But as the chart below shows, much of the increase can be attributable to Owners’ Equivalent Rent (OER). Core sticky price CPI, ex-OER has remained below the Fed’s 2% target (note I have subtracted 2% from all CPI figures in order to better graphically show how far different inflation metrics are from the Fed’s 2% target).

What’s going on? What is the Fed seeing that the rest of us don’t see? Is the Fed reacting in anticipation of the Trump administration’s fiscal stimulus plan? Sure that can’t be the case. Ben Bernanke recently penned a thoughtful essay about the FOMC’s decision making process. He indicated that Fed officials focus on the medium term outlook. While the effects of fiscal policy plays a part in the Fed’s deliberations, they tend to take a wait-and-see attitude to see the full details of the legislative proposals before modeling the effects.

Watch what the Fed does, not just what they say.

Where’s my tax cut?

Over on Wall Street, they are still waiting for Trump’s “tremendous tax plan”, which will probably get unveiled in Trump’s joint address to Congress on February 28, 2017. Equity markets have rallied partly in anticipation of Candidate Trump’s tax cut and offshore tax repatriation proposals. It is not clear, however, whether any tax cuts would actually materialize this year, or what kind of bitter pill the economy would have to swallow in order for the tax cuts to get passed.

So far, it seems that the only way that Trump can pay for his proposed tax cut would be through the imposition of a border adjustment tax (BAT). Without a BAT, the Trump tax cuts could cost up to $7 trillion, according to the Tax Policy Center (via CNN Money). Bloomberg reported that the latest tax reform proposal has been stalled in Senate because a lack of Republican support:

Not long after House Speaker Paul Ryan offered a full-throated affirmation of his tax-overhaul plan, an influential conservative group announced a grassroots campaign against it and a Senate leader said a key part of the proposal is “on life support.”

Senate Majority Whip John Cornyn was diagnosing Ryan’s plan to replace the U.S. corporate income tax with a new, “border-adjusted” levy on U.S. companies’ domestic sales and imports. The proposal has stirred sharp divisions among businesses: Retailers, automakers and oil refiners that rely on imported goods and materials oppose it, while export-heavy manufacturers support it.

So far, the opponents are winning, interviews with lawmakers, lobbyists and tax specialists show. As Congress prepares to depart Washington for a one-week break, Cornyn said he didn’t see the votes lining up for the House leaders’ plan.

Even if a BAT were to pass, I highlighted analysis by Barclay’s last week (via Sam Ro) showing the net effects of a tax reform package. The sheet size of the BAT would, by necessity, be extremely protectionist and such an initiative would invite a debilitating global trade war.

Here is what’s at stake for equity investors. John Butters from Factset pointed out that the market’s forward P/E of 17.6 is at levels last seen in 2004, a 13-year high. Investors would have to include the dot-com bubble era to make the case that the current forward P/E looks reasonable on a historical basis. In short, market expectations for tax cuts and offshore cash repatriation are extremely high and prone to disappointment.

Watch what Trump administration and Congress do, not just what they say.

The week ahead: Be a patient bear

Looking to the week ahead, I don’t want to repeat what I’ve have written over the past week. The points I made in my last post (see Why the SP 500 won’t get to 2400 (in this rally)) still stands. Fundamentals still look wobbly, sentiment remains excessively bullish and short-term technical indicators are flashing overbought readings.

The latest update from Factset shows that forward 12-month EPS stopped falling and rose last week, which is a positive sign for stock prices. But the 2 and 4 weeks rates of change remain negative. In the past, stock prices have struggled whenever forward EPS has been flat to down.

The 10-year weekly SPX chart below illustrates how overbought the market is. I have marked past instances when RSI-5 has risen to similar levels. The red vertical lines when the market has declined, and the blue lines when the market has continued to advance. In the last 10 years, there were six red lines and three blue lines. We now have another overbought signal, play the odds.

On a shorter term time frame, this Index Indicators chart of stocks above their 10 dma is starting to roll over from overbought territory. That’s a classic technical trading sell signal.

As well, these market internals of risk appetite look very iffy.

Tactically, bearish traders may want to be patient. Helene Meisler observed that the CBOE equity only put/call ratio (CPCE) has spent four consecutive days under 0.60. The market is certainly overbought on this metric.

I conducted a study of past episodes, which indicates that such overbought markets don’t necessarily decline. Short term returns have been weak, but still positive.

Returns are tilted to the downside once CPCE mean reverts and breaks up above 0.60.

My inner investor remains bullishly positioned, though he is getting a little nervous. Should the market correct, he will be watching to see the nature of the bearish catalyst before making any further investment decisions.

My inner trader moved to cash a couple of weeks ago and he is standing aside from this market volatility.

Mid-week market update: As the major market averages make new all-time highs, I conducted an informal and unscientific Twitter poll. I was surprised to see how bullish respondents were.

Let’s just cut to the chase – forget it. Neither the fundamental nor the technical backdrop is ready for an advance of that magnitude. Even though the earnings and sales beat rates for Q4 earnings season is roughly in line with historical averages, Factset reports that the 12-month forward EPS growth is stalling. Past episodes has seen stock price struggle to make significant advances under such conditions.

In addition, the technical condition of the market shows that it is vulnerable to a pullback.

Breadth deterioration

This rally has raised a number of red flags. Schaeffer’s Research pointed out that the advance has been accomplished on deteriorating breadth, as measured by 52-week new highs.

If history is any guide, expect subpar returns pattern for the next couple of weeks.

Independent of the analysis from Schaeffer`s, this chart from Trade Followers shows that bullish Twitter breadth is also not advancing even as the market made new highs, indicating a different form of negative breadth divergence.

Sentiment too bullish

In addition, there are numerous instances of excessively bullish sentiment, which is contrarian bearish. The CNN Money Fear and Greed Index is at a level where stock prices have shown difficulty rising in the past.

The CBOE put/call ratio has fallen to levels that can only be described as giddy. Urban Carmel observed that short-term returns tend to be negative after such readings.

The option market is flashing other anomalous signals. Even as stocks rose today, both the VIX Index rose and the VIX term structure, as measured by the VIX/VXV ratio, flattened. Such behavior by the VIX are normally signs of rising caution. I did a study that went back to November 2007, when data for the VXV was first available. I found 117 non-overlapping similar instances. As the table below shows, historical returns were disappointing for the following week.

Overbought markets

As stock prices have risen, it is no surprise that most overbought/oversold models are showing overbought readings. Consider, for example, this chart from Index Indicators of the 5-day RSI above 70, which is a short-term (1-2 day) trading model

This chart of net stocks at 20 day highs-lows, which is a model with a longer term (1-2 week) time horizon, is also in overbought territory.

Overbought readings like those are to be expected as the market advances. There is nothing that says overbought markets can’t stay overbought. However, an alert reading sent me the following chart, which showed that the NASDAQ 100 is reaching overbought levels not seen since 1999, which was the top of the Tech Bubble.

Don’t get too bearish

Despite the combination of overbought and excessively bullish sentiment readings, my inner trader is not wildly bearish. Anecdotal evidence from independent sources of discussions with investment managers indicate that there is a lot of nervousness beneath the surface. This suggests to me that while stock prices may pull back in the near-term, any correction is likely to be shallow and should be bought.

Be cautious, but don’t go overboard on your short positions. My inner trader remains in cash and he is inclined to stay on the sidelines, for now.

The WSJ reported that the Trump administration is considering a new tactic in managing its trade relationship with China. Here is the Bloomberg recap for those without a WSJ subscription:

Under the plan, the commerce secretary would designate the practice of currency manipulation as an unfair subsidy when employed by any country, instead of singling out China, the newspaper reported. American companies could then bring anti-subsidy actions to the U.S. Commerce Department against China or other countries, it said.

The discussions are part of a strategy being pursued by the White House’s new National Trade Council to balance the goals of challenging China on certain policies while keeping broader relations on an even keel, the paper said. The Trump administration would avoid, at least for now, making claims about whether China is manipulating its currency, it said.

While such an approach may seem clever, it has the risk of sideswiping American relations with a whole host of other countries other than China. As well, the imposition of countervailing duties is subject to a challenge under WTO rules.

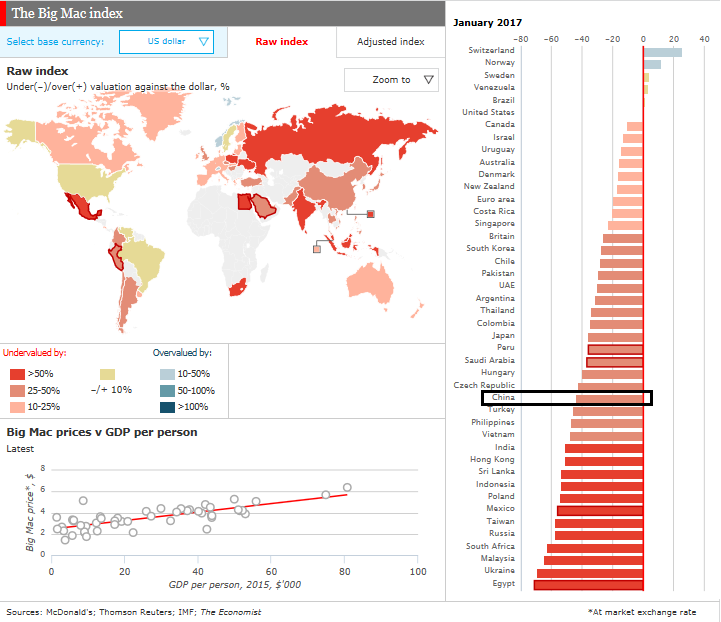

The Big Mac Index

One of the key questions is how you define an undervalued currency. There are many metrics, but consider the popular Big Mac Index, as compiled by The Economist.

If the idea of this initiative is to target China, then there are many other countries with undervalued currencies that will have to be targeted under this initiative. Starting from the bottom, the list includes the following countries before we get to China: Egypt, Ukraine, Malaysia, South Africa, Russia, Taiwan, Mexico, Poland, Indonesia, Sri Lanka, Hong Kong, India, Vietnam, the Philippines, and Turkey. A blanket rule that imposes countervailing duties on the exports from this list risks destabilizing a number of important geopolitical relationships, and it would signal the start of a global trade war.

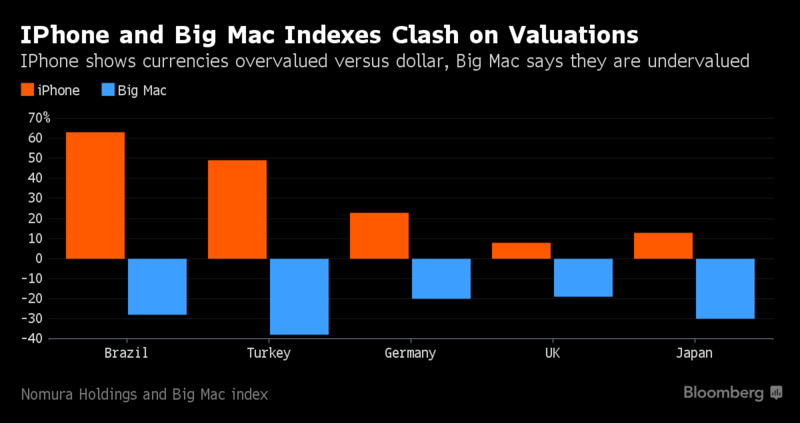

To be sure, the Big Mac Index has a number of flaws and it is not the only measure of purchasing power parity (PPP). Bloomberg reported that Nomura compiled an iPhone index because the price of Big Macs in poor countries can be distorted by low labor costs.

For years, many traders have used the Big Mac index — which is based on the price of a McDonald’s Corp. hamburger — along with an OECD gauge and measures based on consumer and producer prices, to determine currencies’ relative value. All of these show the dollar as broadly overvalued.

The iPhone index is better than its traditional peers because it uses the “defining product of the digital era,” Hafeez said. “IPhone is high-end tech,” he said. “That’s going to be the bigger driver in the future.”

Nomura found a number of notable differences between iPhone and Big Mac prices (data as of July 2016).

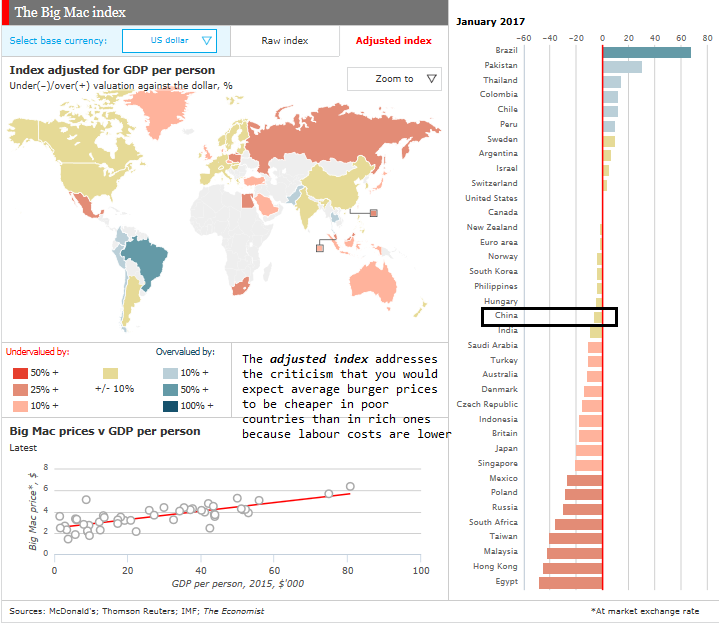

In response to these criticisms, The Economist unveiled the Big Mac Adjusted Index, which adjusts for labor costs in each country. Suddenly, China`s currency doesn’t look that undervalued anymore. On the other hand, a whole host of other countries would get targeted using this methodology: Egypt, Hong Kong, Malaysia, Taiwan, South Africa, Russia, Poland, and Mexico. While having Mexico on both the unadjusted and adjusted lists may serve the Trump administrations political aims, what about the other countries?

A trade war brewing?

I recognize that the “currency manipulation as unfair subsidy” represents a trial balloon by the Trump administration as a way of fulfilling its campaign promise of addressing the damage from “unfair trade”. The fact that the White House is even thinking about such broad based solutions are raising the risks of a global trade war.

Edward Harrison at Credit Writedowns believes that Donald Trump’s entrepreneurial risk taking personality makes him far more likely to start a trade war:

Now when you look at Trump the Entrepreneur through this prism, it explains not just his behavior on the campaign trail and in using Twitter, it also explains his “grab them by the pussy” mode of operating. I think it also explains how Trump the entrepreneur saddled four different businesses with so much debt that they were forced into bankruptcy. in short, Donald Trump is a man of action, who often leaps before he looks. That can mean unexpected success. But it means he is prone to getting things very wrong, and then having to improvise to clean up the mess.

This isn’t how traditional politicians operate, by the way. First of all, most politicians are frightened to death by uncertainty and assiduously avoid it to prevent tail risk. If you think about it from a decision tree perspective, a politician that has a choice between guaranteed but moderately bad outcomes and uncertain but potentially catastrophically bad outcomes is going to feel a lot of loss aversion pressure. Even a supposed maverick like Greek Premier Alexis Tsipras caved in 2015 – and went with a bad outcome to prevent a catastrophic outcome when the ECB threw down the gauntlet and threatened to collapse the Greek banking system.

But Trump is not that kind of guy. His overarching strategy is just the opposite – create uncertainty, be as unpredictable as possible and hopefully profit from this. He has even said this himself – multiple times.

By floating this trial balloon, the Trump administration has in effect let “slip the dogs of (trade) war”. Once you accept the principle of imposing countervailing duties on currency manipulation, why not border adjust for other reasons? FT Alphaville outlined a number of other proposals that have been floated, such as a carbon tax border adjustment:

So it’s interesting to read a proposal from Republican eminences arguing the government should tax carbon dioxide emissions, including from imported goods, and rebate the revenues to the public:

Border adjustments for the carbon content of both imports and exports would protect American competitiveness and punish free-riding by other nations, encouraging them to adopt carbon pricing of their own. Exports to countries without comparable carbon pricing systems would receive rebates for carbon taxes paid, while imports from such countries would face fees on the carbon content of their products.

How about labor standards in the name of “fair trade”?