I have had a number of discussions with subscribers asking for more “how to” posts (see Teaching my readers how to fish). This will be one of a series of occasional posts on how to build a robust investment process.

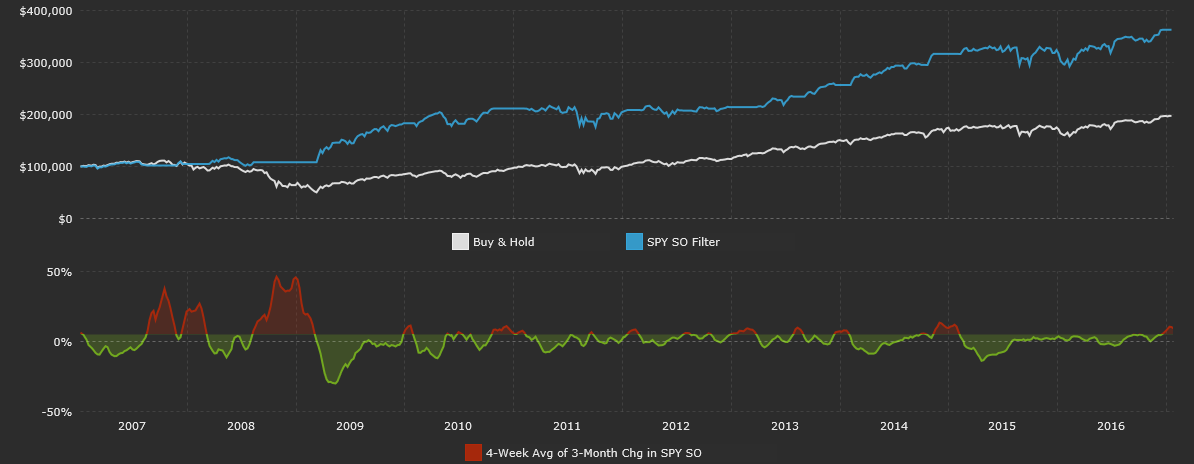

For traders and investors, one of the challenges is how to build a robust discipline that works well through different market regimes. As a case study, consider this study from Simple Stock Model that generates signals based on the cash flows in and out of the SPY ETF as a sentiment signal. The trading rule is: “If the 4-week average of the 3-month change in SPY’s percentage of shares outstanding is greater than +5%, be out of the market.”

The chart below shows the equity curve from this trading system (white line = buy and hold, blue line = trading system). The results look pretty good, especially for a relatively low turnover model. (Incidentally, it’s on a sell signal right now).

SPY shares outstanding trading system

Not so fast! Don’t jump to conclusions before digging into the data and reading the fine print.

One big call

If you look at the details of the equity curve, you will see that the trading system made its money by avoiding the devastating bear market of 2008-09, but the market kept rising when it flash its other “sell” signals. If we were to restart the equity curve from the time this trading system flashed the all-clear buy signal after the 2008-09 bear market, it underperformed its buy-and-hold benchmark.

This is the first lesson. Evaluate the success rate, or batting average, of any trading system to see if the results are acceptable. In some cases, you may decide that a system with a low success rate with outsized gains is acceptable – just be aware of its characteristics and manage your risk properly.

Asymmetric signals

This trading model is a sentiment model and I used it as an example to illustrate another point. The market response to model readings don’t always behave the same way at buy and sell extremes. Model signals can be asymmetric, especially for sentiment models.

Consider this chart of NAAIM exposure, which measures the sentiment of professional RIAs. In this example, I have arbitrarily set the trading rule to buy when the NAAIM exposure falls below 20 and to sell when it rises above 95. The “buy” signals are marked with blue vertical lines and the “sell” signals are marked with red lines. As the chart shows, the “buy” signals have tended to be pretty good, as they have tended to mark panic market bottoms. On the other hand, “sell” signals, which indicate complacency, have been less than effective.

As these are backtested results, it could be argued that when I set the buy and sell signals at 20 and 95 respectively, I was torturing the data until it talked. As an alternative, I set the buy and sell signals when the NAAIM exposure reading penetrated its 2 standard deviation Bollinger Band with a one-year moving average. The conclusions are similar. Buy signals work much better than sell signals.

That is the second lesson. Measure the effectiveness of both your buy and sell signals. They may not be the same.

In a post next week, I will address some the issues that face the professional and institutional investor.

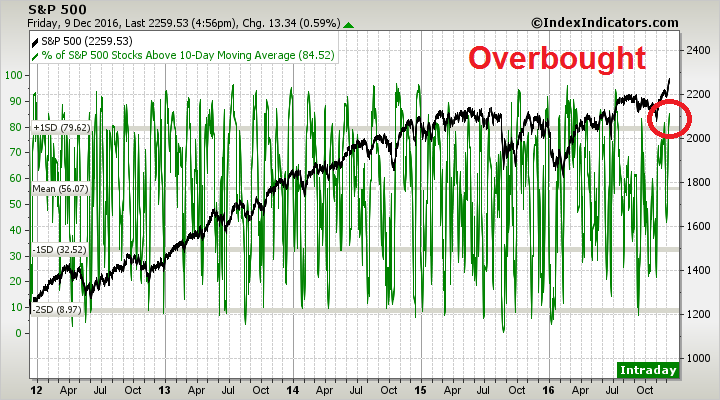

Mid-week market update: Since the time I issued a correction warning in late December (see A correction on the horizon?), the US equity market has traded sideways in a narrow range. Moreover, the SPX has alternated between a seesaw up-and-down pattern since early January – until today.

As the SPX breaks upwards to a new all-time high, and the DJIA breaches the psychologically important 20,000 mark, it’s hard to argue with price and momentum.

Overbought and vulnerable markets can correct in two ways. It can correct through price, with lower prices, or through time, with a sideways consolidation. The latter scenario is often accompanied by an internal rolling correction characterized by weakness in market leaders and nascent strength from laggards, which seems to be what has happened (see The contrarian message from rotation analysis).

The turmoil beneath the surface

Even as the stock market traded sideways for most of January, an anomaly began to develop in the option market. The VIX Index, which is a measure of index volatility, fell as expected, but SKEW rise dramatically (chart via Bloomberg). In other words, the cost of hedging a tail-risk event such as a market crash rose dramatically even as stock prices flattened and volatility fell. In fact, tail-risk fear is at levels not see since the correction last June, which stock prices actually fell.

What gives? Has the market been that nervous about the Trump administration? If so, shouldn’t the VIX Index be rising in anticipation of heightened market volatility? Who is right? The VIX or the SKEW Index?

It turns out that there are perfectly reasonable explanations for the low level of the VIX Index. As this chart of implied (orange line) and historical (blue line) volatility from iVolatility shows, historical, or realized, vol has been falling and therefore it is no surprise that implied vols have followed suit.

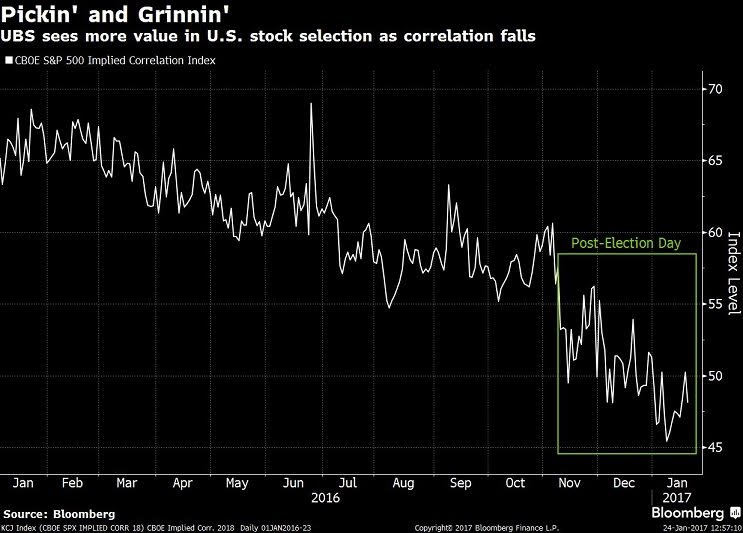

In addition, Julian Emanuel of UBS pointed out that the correlation between stocks have been falling since the election. Lower correlations between stocks create a greater diversification effect, which leads to lower index volatility and lower realized historical volatility. In addition, lower correlations can create the sorts of conditions where rolling corrections can occur, which is precisely what seems to have happened.

I have been wrong before and I am wrong now, as Mrs. Humble Student of the Markets have pointed out to me on numerous occasions. I mis-interpreted the rolling corrections, where cyclical sectors weakened and defensive sectors began to outperform as signs of weakening internals (see The contrarian message from rotation analysis). Instead, they turned out to be a healthy rolling correction.

Markets are breaking out

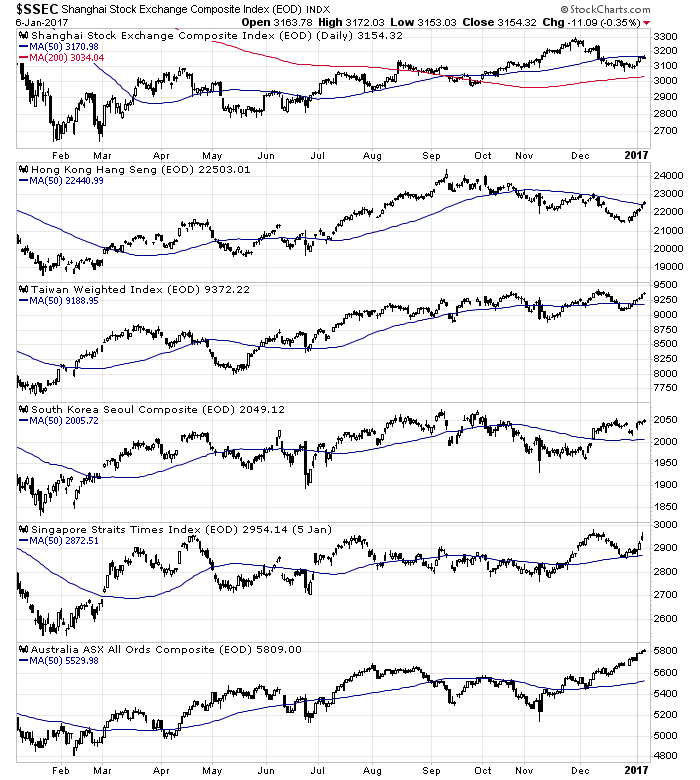

In the meantime, the markets have staged a broad based rally. The chart below shows that the DJ World Index has risen to new highs, just like the SPX. Even though the European averages have not rallied to new highs, they are displaying signs of strength.

Similarly, the Asian markets of China and her major trading partners are all well above their 50 day moving averages.

The cyclically sensitive industrial metals are also in a healthy uptrend.

What’s not to like?

Key risks

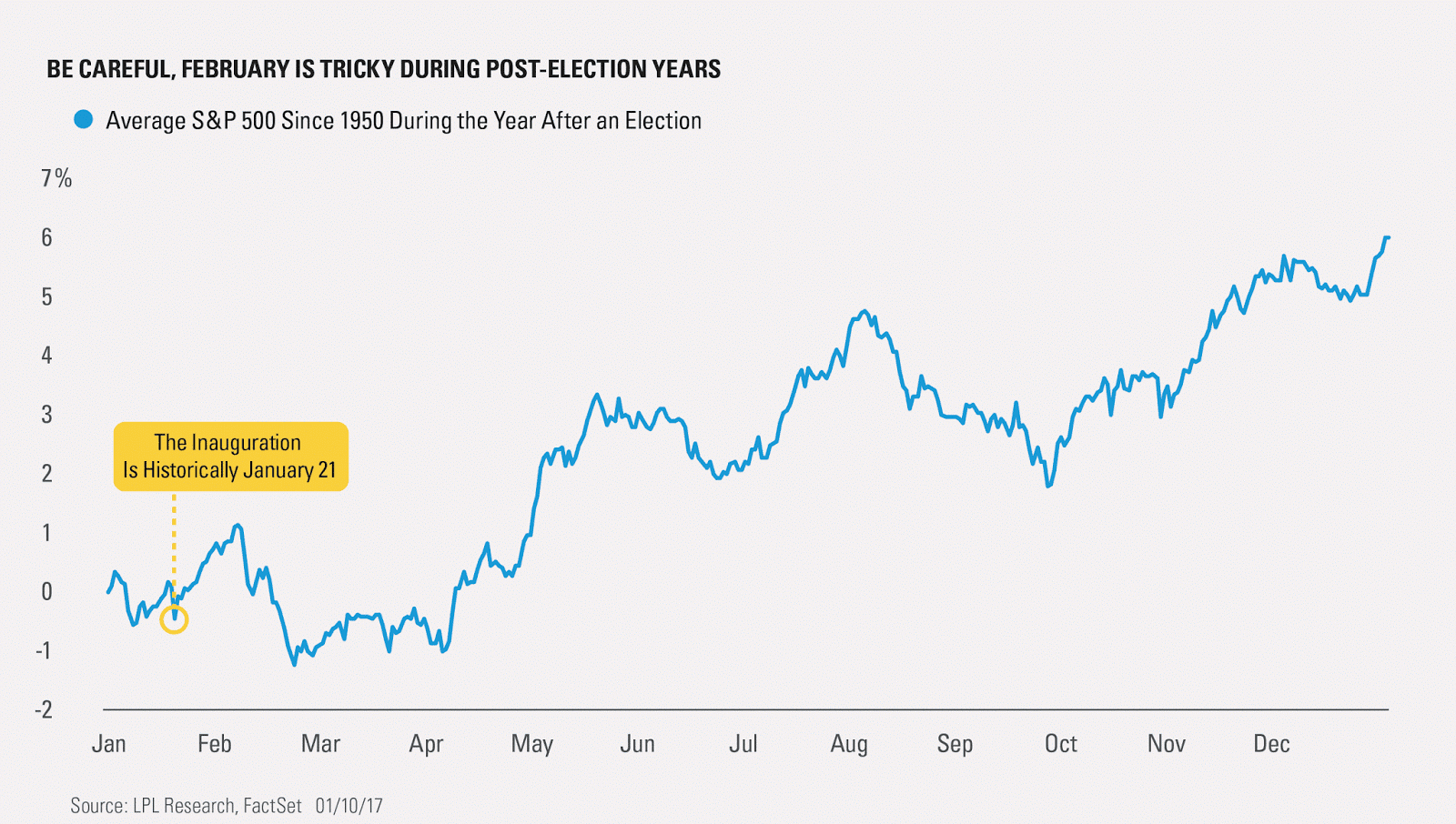

One of the key risks is this rally could turn out to be a bull trap. Ryan Detrick of LPL Financial observed that the market tends to rally after Inauguration Day, with a peak in early February. Could history repeat itself?

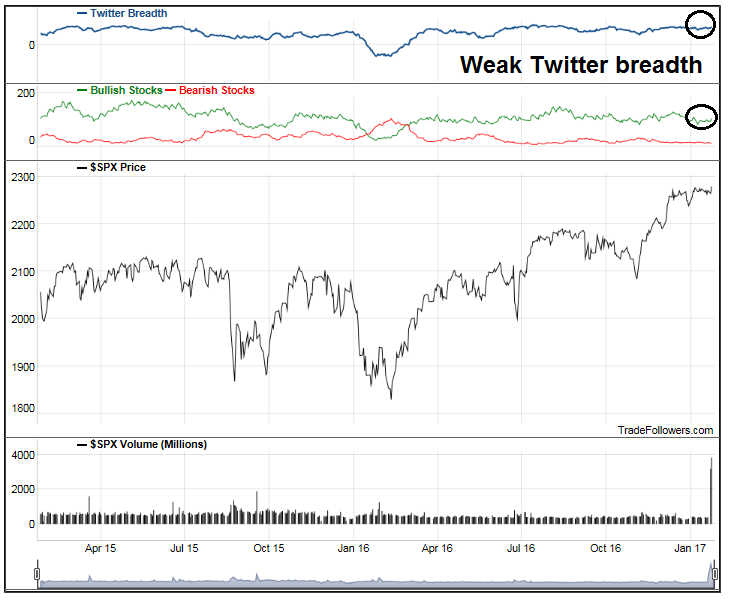

In addition, this chart from Trade Followers shows that Twitter breadth remains weak, which does not exactly inspire a great deal of confidence in the current upside breakout.

My inner trader has changed from a small SPX short position to a small long SPX position with a tight stop (don’t ask me how tight, because my pain threshold will be different from yours). Should the market rally further and VIX Index breach its lower Bollinger Band, that will be an overbought signal to realize profits and take some chips off the table.

Now that the Trump team has moved into the West Wing of the White House, investors still one big Trump policy question mark that overhang the market. Who will Trump appoint to the two vacant governor seats at the Federal Reserve?

CNBC reported that David Nason is a leading contender for a board seat, but he is rumored to be considered for a regulatory role. Such an appointment gives us no hints about the likely future direction of monetary policy and who might replace Janet Yellen, should Trump choose not to re-appoint her as Fed chair in 2018.

Bloomberg reported that the latest rumor mill has the leading candidates for Fed chair, namely Glenn Hubbard, John Taylor, and Kevin Warsh, advocating a tighter monetary policy than the current Fed:

Potential candidates to head the Federal Reserve in 2018 suggested that monetary policy would be tighter if they were in charge.

Speaking at the annual American Economic Association meeting that ended Sunday, Glenn Hubbard of Columbia University, along with Stanford University’s John Taylor and Kevin Warsh, criticized the central bank for trying to do too much to help an economy struggling with problems that monetary policy can’t solve.

“The Federal Reserve is a little behind the curve” in raising interest rates, Taylor, a Treasury undersecretary for international affairs under the last Republican president, said Saturday during a panel discussion in Chicago.

Hubbard, who headed the Council of Economic Advisers under Bush, said he agreed with what he perceives as Trump’s stance that the U.S. has depended too much on the Fed to support the economy in recent years.

Is that what Trump really wants? There is a battle going on for the hearts and minds of the Federal Reserve. The outcome will have profound implications for the direction of monetary policy, the likely trajectory of economic growth for President Trump’s next four years, and the stock market.

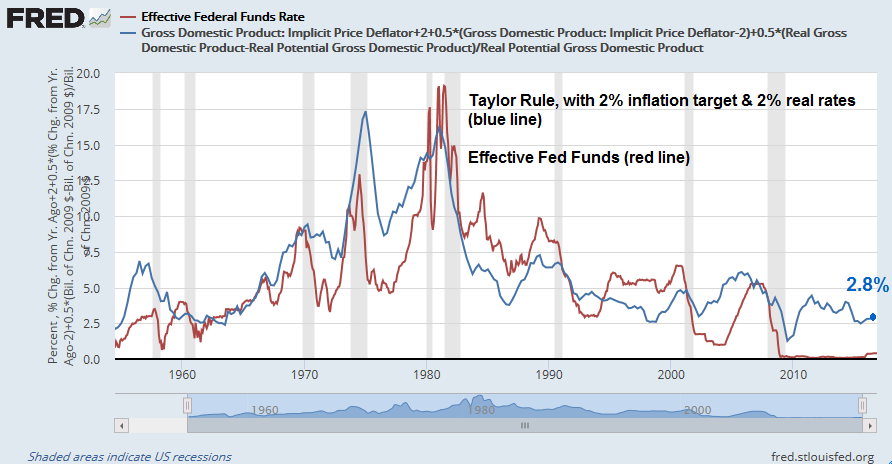

War at the Fed

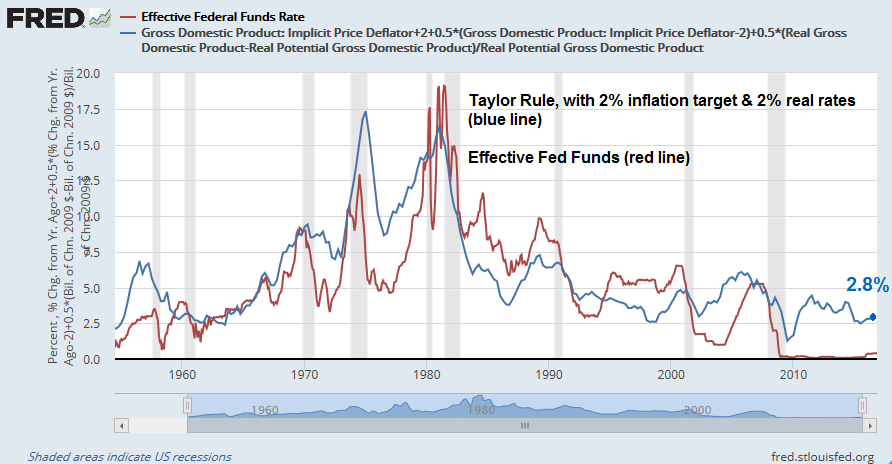

Current members of the FOMC have pushed back against proposals by the hard money crowd to impose a rules based approach to setting interest rates. Neel Kashkari, president of the Minneapolis Fed, shot back that using a Taylor Rule to set interest rates would have kept millions out of work:

In December, I wrote an op-ed in the Wall Street Journal explaining that forcing the Federal Open Market Committee (FOMC) to mechanically follow a rule, such as the Taylor rule, to set interest rates can cause tremendous harm to the economy and the American people. My staff at the Minneapolis Fed estimates that if the FOMC had followed the Taylor rule over the past five years, 2.5 million more Americans would be out of work today. That’s enough to fill the seats at all 31 NFL stadiums simultaneously, almost 6,000 more people out of work in every congressional district.

To sum up, simple policy rules can serve as useful benchmarks to help assess how monetary policy should be adjusted over time. However, their prescriptions must be interpreted carefully, both because estimates of some of their key inputs can vary significantly and because the rules often do not take into account important considerations and information pertaining to the outlook. For these reasons, the rules should not be followed mechanically, since doing so could have adverse consequences for the economy.

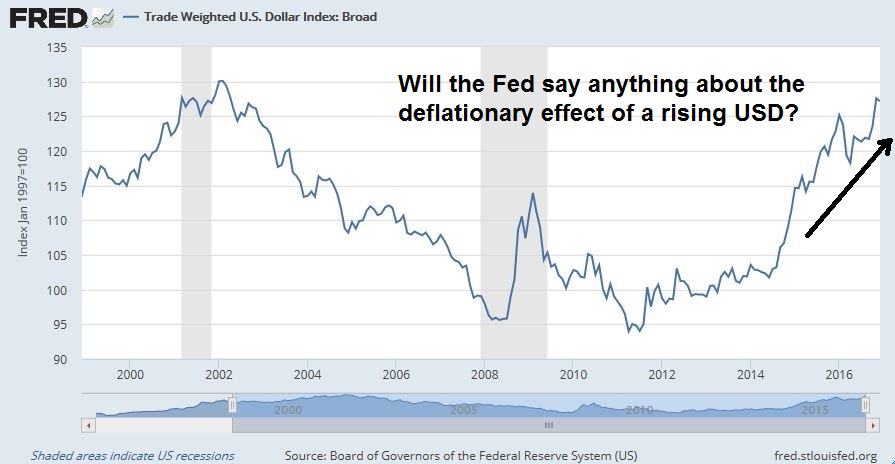

Hawkish Fed = USD bullish

Everything else being equal, a hawkish Fed would tend to put greater upward pressure on the US Dollar, which would be contrary to Trump’s trade policy objectives. I pointed out that Trump had already expressed his preference for a weak USD (see Weaken the USD to Make America Great Again). Therefore it makes no sense for him to appoint a hard money economist to be Fed chair and steer monetary policy.

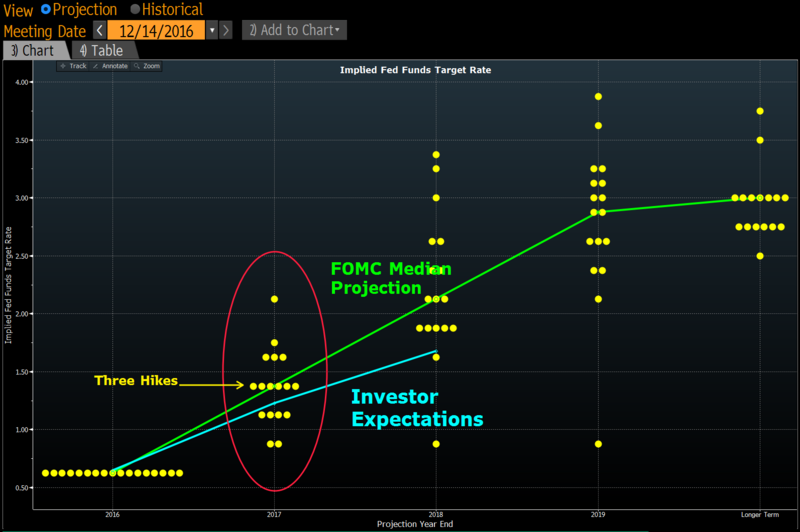

If the Trump administration were to turn away from the likes of John Taylor, who would be a more likely Fed chair? For this exercise, let`s peg the Yellen Fed`s monetary policy as the neutral position. Janet Yellen has said that she expects to continue raising rates in 2017. In a January 18, 2017 speech, Janet Yellen made it clear that her dovish tilt has limits.

In a nutshell, the Fed’s goal is to promote financial conditions conducive to maximum employment and price stability. And I have offered broad-brush definitions of each of those objectives. So where is the economy now, in relationship to them? The short answer is, we think it’s close…

Nevertheless, as the economy approaches our objectives, it makes sense to gradually reduce the level of monetary policy support. Changes in monetary policy take time to work their way into the economy. Waiting too long to begin moving toward the neutral rate could risk a nasty surprise down the road–either too much inflation, financial instability, or both. In that scenario, we could be forced to raise interest rates rapidly, which in turn could push the economy into a new recession.

She expects to raise rates “a few times a year” until the end of 2019, when Fed Funds gets to the neutral rate of 3%:

Now, many of you would love to know exactly when the next rate increase is coming and how high rates will rise. The simple truth is, I can’t tell you because it will depend on how the economy actually evolves over coming months. The economy is vast and vastly complex, and its path can take surprising twists and turns. What I can tell you is what we expect–along with a very large caveat that our interest rate expectations will change as our outlook for the economy changes. That said, as of last month, I and most of my colleagues–the other members of the Fed Board in Washington and the presidents of the 12 regional Federal Reserve Banks–were expecting to increase our federal funds rate target a few times a year until, by the end of 2019, it is close to our estimate of its longer-run neutral rate of 3 percent.

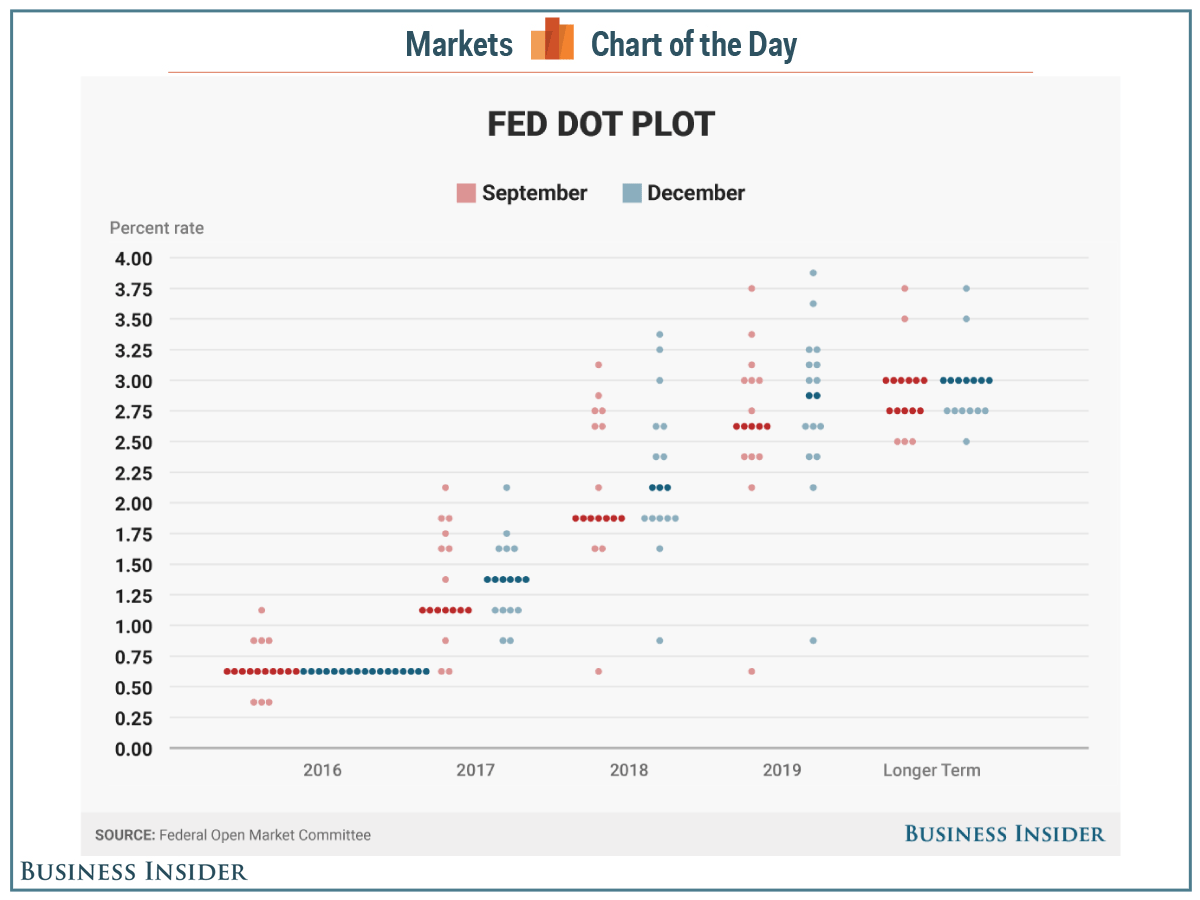

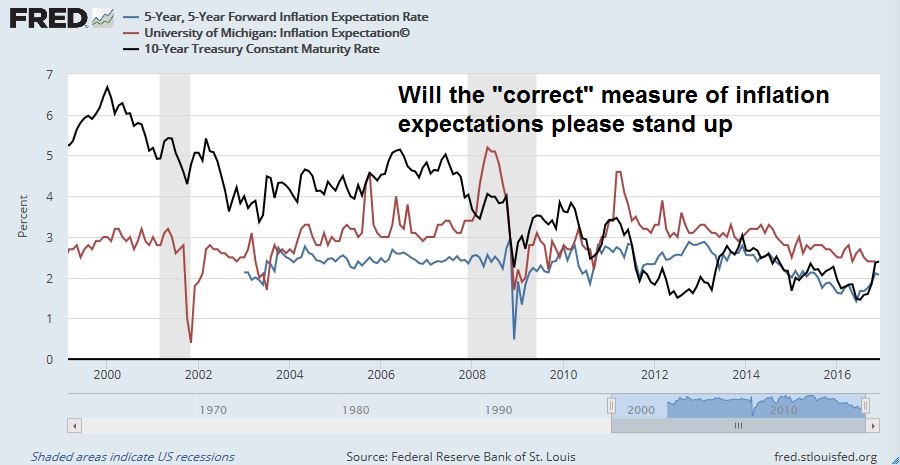

Forgive me if I am parsing this incorrectly, but if “a couple” is two, then doesn’t “a few” mean more than two? It sounds like Yellen is signaling that she expects at least three rate hikes in 2017. Indeed, Bloomberg reported that former Fed governor Laurence Meyers deduced that Yellen is forecasting three rate hikes on the “dot plot” for 2017:

Meyer is playing a game of elimination popular among investors and economists that revolves around the so-called dot plot. That’s a graphic layout that the Fed publishes every three months to show where policy makers think interest rates should go if their forecasts for the economy prove accurate. The quarterly rate projections don’t identify the author of each forecast, which is represented by a dot on a chart…

Atlanta Fed President Dennis Lockhart told reporters on Jan. 9 that he had forecast two hikes this year. His Chicago counterpart Charles Evans suggested he’s also looking at two, saying on Jan. 6 that a couple of moves were “not an unreasonable expectation.” Next, Governor Daniel Tarullo, who in the past has advocated a decidedly cautious approach to raising rates, also got ranked at two hikes by several economists.

With a single two-hiker remaining, there is one more firm clue: In December, in the run-up to the FOMC meeting, the board of directors at the Minneapolis Fed was alone among the regional banks when it voted against increasing the so-called discount rate, which establishes interest rates for direct loans from the Fed. They did so to support the labor market and allow inflation to rise, according to minutes published on Jan. 10.

A reserve bank’s position on the discount rate typically reflects its president’s view with respect to the benchmark federal funds rate, suggesting Minneapolis Fed President Neel Kashkari isn’t hawkish enough to forecast more than two hikes this year on the dot plot.

If that’s correct, Yellen and New York Fed President William Dudley are among the six policy makers forecasting three hikes in 2017.

Wow! Three 2017 rate hikes for a reputed dove like Janet Yellen. Trump won’t like that!

Even doves have limits

What about Lael Brainard? Even though Brainard supported Hillary Clinton in the election and was rumored to be in the running for the post of Treasury Secretary in a Clinton administration, could the ȕber-dove Lael Brainard be a candidate for Fed chair?

In a recent speech made on January 17, 2017, Brainard made it clear that even doves have limits when faced with an expansionary fiscal policy. Fiscal policy that provide only a temporary boost to demand (read: tax cuts) spur inflation, especially when the economy is running near capacity, as it is now:

Focusing first on policies that affect only aggregate demand, temporary demand-based fiscal expansions can speed recovery when the economy is some distance from full employment and target inflation, particularly if conventional monetary policy is constrained by the effective lower bound. But when the economy is either close to or at full employment and inflation is converging to or at its target, additional fiscal demand will more likely result in inflationary pressures. Thus, fiscal expansions that affect only aggregate demand and are enacted when the economy is near full employment and 2 percent inflation are relatively less likely to sustainably boost economic activity and relatively more likely to be accompanied by increases in interest rates.

These kinds of fiscal policies are actually counterproductive, as the government has to incur debt without a corresponding boost to long-term growth. In addition, the Fed is weakened because it has little ammunition to fight the next downturn:

Policies that persistently raise aggregate demand alone can lift the neutral rate, but that may come at substantial cost. Because these policies do not affect the economy’s long-term growth potential but do result in persistent fiscal deficits, they can lead to substantial increases in the debt-to-GDP ratio. The greater space for monetary policy to respond to adverse shocks provided by a higher neutral rate comes at the expense of reducing the space for fiscal policy to stabilize the economy in the event of future adverse shocks.

At the end of her speech, she did sound a dovish tone by giving a nod to her thesis that the Fed has to consider the global implications of its policy:

Against this uncertain backdrop, monetary policy will continue to be guided by actual and expected progress toward our goals, the level of the neutral rate, and the balance of risks. A gradual approach will remain appropriate as long as inflationary pressures remain muted, the economy remains short of our objectives, the neutral rate remains low, and downside risks from abroad remain, although this will depend on the fiscal trajectory, as it evolves, and its uncertain effects on the economy and financial markets.

Will that be enough for Trump looking for a dovish Fed chair? Probably not.

The rise of inflation

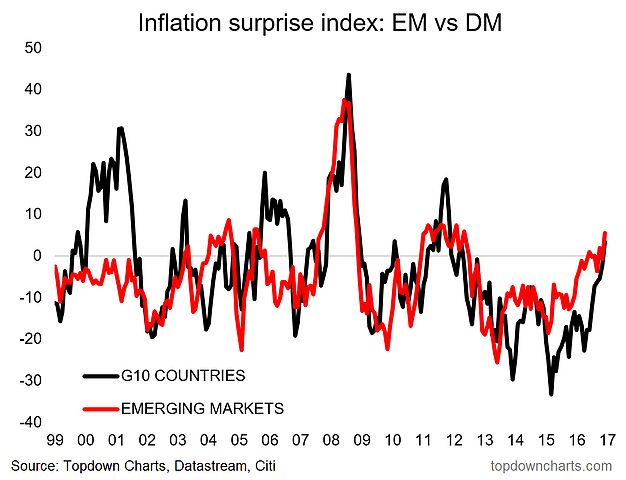

Regardless of who Trump appoints to the Federal Reserve’s board of governors, or to next Fed chair, the inescapable fact is inflation is rising. As one of the Federal Reserve’s mandate is to fight inflation, monetary policy will become tighter. This chart from Callum Thomas of Top Down Charts shows that not only are the inflationary pressures building, they are global in nature.

Indeed, BIS recently put out a paper entitled The globalisation of inflation: the growing importance of global value chains. The authors concluded that the globalization of manufacturing has also globalized inflation dynamics, which makes it more difficult for central banks to control inflation locally. The conclusions of this paper is supportive of Lael Brainard’s thesis that the Fed needs to pay greater attention to the global effects of US monetary policy. Here is the abstract of the BIS paper:

Greater international economic interconnectedness over recent decades has been changing inflation dynamics. This paper presents evidence that the expansion of global value chains (GVCs), ie cross-border trade in intermediate goods and services, is an important channel through which global economic slack influences domestic inflation. In particular, we document the extent to which the growth in GVCs explains the established empirical correlation between global economic slack and national inflation rates, both across countries and over time. Accounting for the role of GVCs, we also find that the conventional trade-based measures of openness used in previous studies are poor proxies for this transmission channel. The results support the hypothesis that as GVCs expand, direct and indirect competition among economies increases, making domestic inflation more sensitive to the global output gap. This can affect the trade-offs that central banks face when managing inflation.

Kyle Bass believes that financial markets are at the beginning of a major tectonic shift towards inflation from deflation:

Texan hedge fund manager J. Kyle Bass, the founder of Hayman Capital, says that global markets are at the “beginning of a tectonic shift.”

“Today, global markets are at the beginning of a tectonic shift from deflationary expectations to reflationary expectations. What happens to economies at maximum leverage when interest rates begin to rise? Reconciling the potent strengths of the world’s largest economies with their inherent weaknesses has revealed various investable anomalies. The enormity of the apparent disequilibrium is breathtaking, making today a tremendous time to invest,” Bass wrote in a year-end letter to investors seen by Yahoo Finance.

If Trump wants a dovish Fed, and if he decides to pack the board with like minded appointees who are willing to tilt towards an easier monetary policy (and therefore a weaker USD), a major war will likely erupt within the FOMC on policy, especially when well-known doves like Brainard and Yellen have become more hawkish.

Three steps and a stumble?

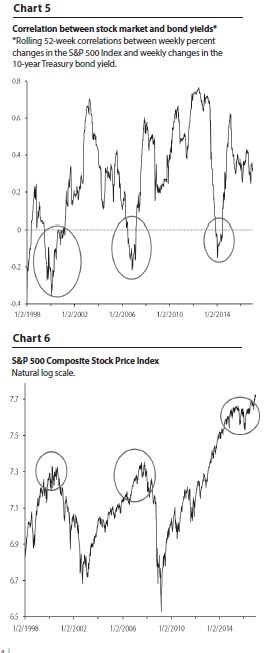

Under the scenario I outlined, the three steps and a stumble rule, where the market tops or corrects after three consecutive rate hikes, will inevitably come into play. But it’s probably too early too panic. Jim Paulsen of Wells Capital Management observed that equity markets typically don’t pull back in the face of rising yields until market psychology changes from disinflation to inflation:

Charts 5 and 6 illustrate how important the relationship portrayed by this correlation has been for stocks in recent years and when the recent rise in bond yields might finally cause a correction in the stock market. Specifically, it suggest the stock market may continue to rise despite higher yields until the correlation switches from positive to negative. That is, higher interest rates may not restrain the stock market until the primary investor anxiety shifts from deflation to inflation.

As shown, since the late-1990s, the stock market has suffered either a correction or a bear market each time the stock-bond correlation has declined below zero (i.e., each time investor mindsets have switched from deflation to inflation concerns). The 2000 collapse occurred after the correlation turned negative in late-1999, the 2007-2008 collapse happened after the correlation dropped below zero in the second half of 2006 and the correlation again fell below zero at the end of 2013 followed by two separate 10% corrections and an essentially flat stock market during the ensuing couple years.

The risk stock investors face in 2017 from rising bond yields may have less to do with how much they rise or how high they are, as it does with the surrounding attitude of investors concerning inflation/deflation as yields rise. Currently, the consensus investor mindset is viewing the recent rise in yields as a positive for the economy and the stock market (as suggested by a strong positive correlation in the last year from Chart 5). Fears of deflation and anxieties surrounding another potential crisis are diminishing as commodity prices recover, as U.S. and global economic growth improve, as the Federal Reserve finally begins to normalize monetary policy and as the interest rate structure around the globe moves back above zero.

It sounds like that “three steps and a stumble” is a late 2017 investment story. Tactically, I would hesitate about getting overly defensive just yet. The bond market is currently poised for a counter-trend rally as large speculator, or hedge funds, remain in a crowded short in both the 10-year note and the long bond (chart via Hedgopia).

Bloomberg also pointed out that while the fast money, or hedge funds, are in a crowded long in the bond market, the patient and big money institutions are extremely long. In the end, big money fund flows have tended to overwhelm the fast money.

Leveraged funds that use borrowed money to boost returns see even more losses ahead. As of Jan. 10, their short positions — futures that pay off if five-year notes lose value — exceeded longs by a record 1.1 million contracts, data compiled by the U.S. Commodity Futures Trading Commission show.

While it’s been the winning strategy over the past several months, institutional buyers are undaunted. Not only did they boost their long positions for five-year notes to an all-time high this month, but they’ve also stepped up bullish bets on 10- and 30-year Treasuries as well. (Most recent data as of Jan. 17 showed a slight pullback in both institutional net longs and leveraged net shorts.)

When real-money investors do go all-in, they tend to overwhelm the fast-money crowd because of their sheer size.

In the end, “real money always wins,” said Tom di Galoma, the managing director of government trading and strategy at Seaport Global Holdings. “Speculators tend to get taken out. We’ve seen this occur several times in the last 10 to 15 years, where everybody thinks rates are too low.”

By all means and enjoy the party, but don’t go overboard and be selective with your risk appetite.

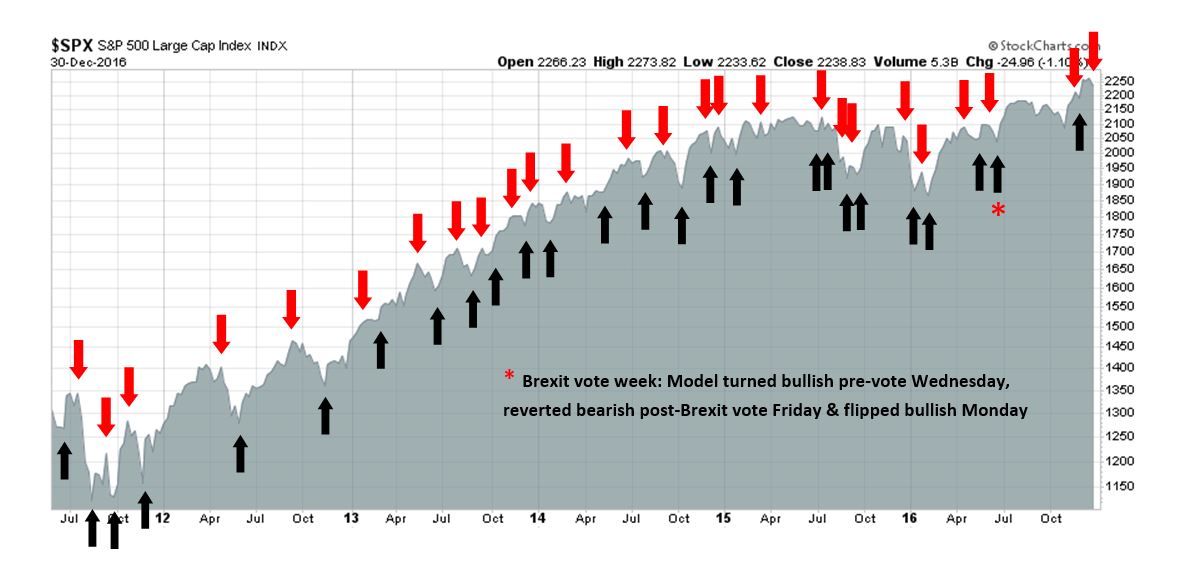

Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Model is an asset allocation model which applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. In essence, it seeks to answer the question, “Is the trend in the global economy expansion (bullish) or contraction (bearish)?”

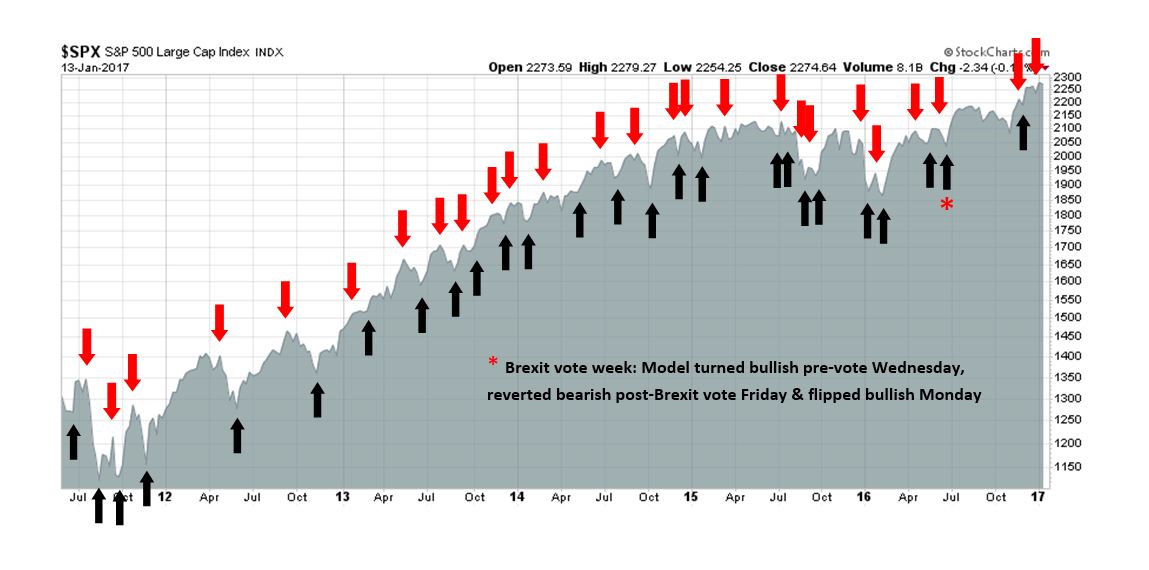

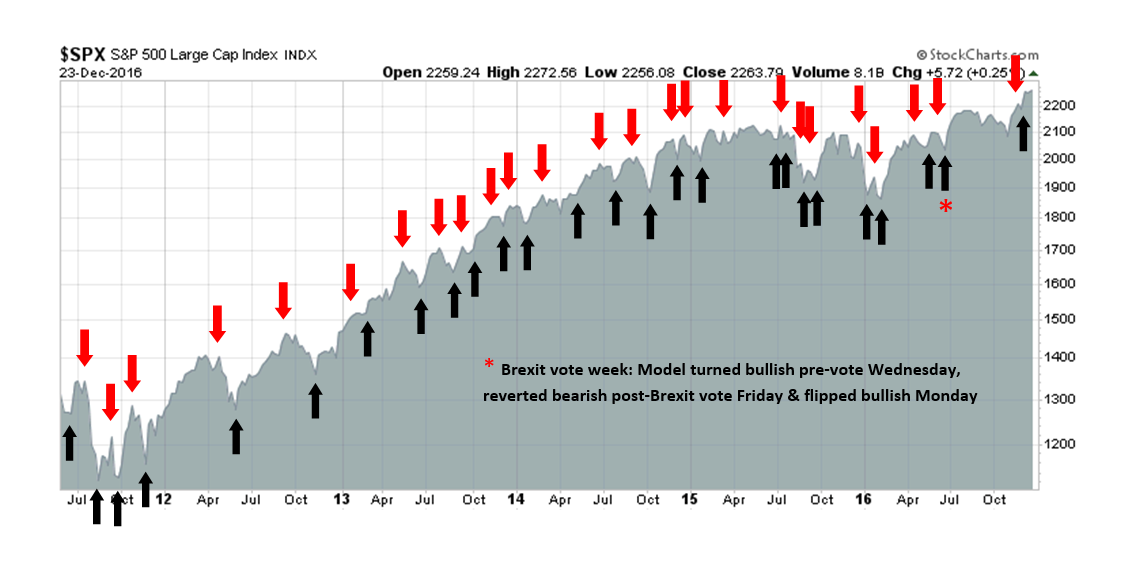

My inner trader uses the trading component of the Trend Model to look for changes in direction of the main Trend Model signal. A bullish Trend Model signal that gets less bullish is a trading “sell” signal. Conversely, a bearish Trend Model signal that gets less bearish is a trading “buy” signal. The history of actual out-of-sample (not backtested) signals of the trading model are shown by the arrows in the chart below. Past trading of the trading model has shown turnover rates of about 200% per month.

The latest signals of each model are as follows:

Ultimate market timing model: Buy equities

Trend Model signal: Risk-on

Trading model: Bearish

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers will also receive email notices of any changes in my trading portfolio.

Trump’s challenge

Now that Donald Trump is the President of the United States, the real work of his administration begins. In inauguration speech, he invoked the spirit of Horatio Alger as a way to take America to new heights:

Finally, we must think big and dream even bigger. In America, we understand that a nation is only living as long as it is striving…

Do not allow anyone to tell you that it cannot be done. No challenge can match the heart and fight and spirit of America. We will not fail. Our country will thrive and prosper again.

Ray Dalio of Bridgewater Associates was optimistic about this “can-do” attitude of Americans:

This new administration hates weak, unproductive, socialist people and policies, and it admires strong, can-do, profit makers. It wants to, and probably will, shift the environment from one that makes profit makers villains with limited power to one that makes them heroes with significant power.

Despite inheriting an economy that is in the late stages of an expansion, Dalio believes that the incoming president can spark a second wind of growth by reviving the economy’s “animal spirits”:

This particular shift by the Trump administration could have a much bigger impact on the US economy than one would calculate on the basis of changes in tax and spending policies alone because it could ignite animal spirits and attract productive capital. Regarding igniting animal spirits, if this administration can spark a virtuous cycle in which people can make money, the move out of cash (that pays them virtually nothing) to risk-on investments could be huge.

Bob Shiller went further and postulated a speculative stock market blow-off, followed by a crash (via The Telegraph):

America should brace for a final blow-off surge in stock markets akin to the last phase of the dotcom boom or the “Gatsby” years of the Roaring Twenties, followed by a cathartic crash and day of moral judgment, according to a Nobel prize-winning economist.

Prof Robert Shiller said the psychological “narrative” behind Donald Trump is powerful and likely to carry Wall Street to giddy heights before the aging business cycle finally rolls over.

“I think there will be a Trump boom for a while. Stocks look high, but they are not yet super-high. In 2000 the (Cape Shiller) price-earnings ratio was over 45 and we may see a repeat of that,” he told The Daily Telegraph.

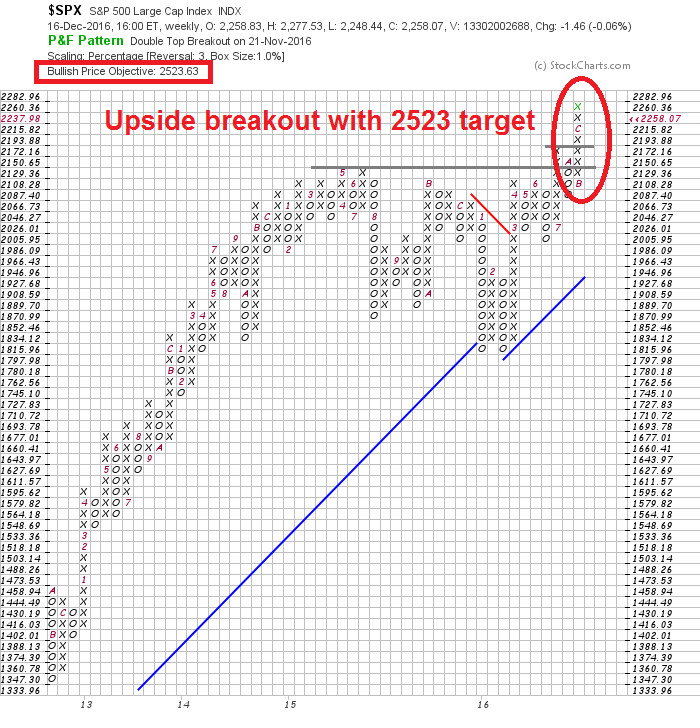

For investors, the stakes are high. Under this scenario, a Trump inspired “animal spirits” revival could spur the SPX to its point and figure target of 2523 or more.

The question is, can Trump spark the “animal spirits” to Make America Great Again?

A mature expansion

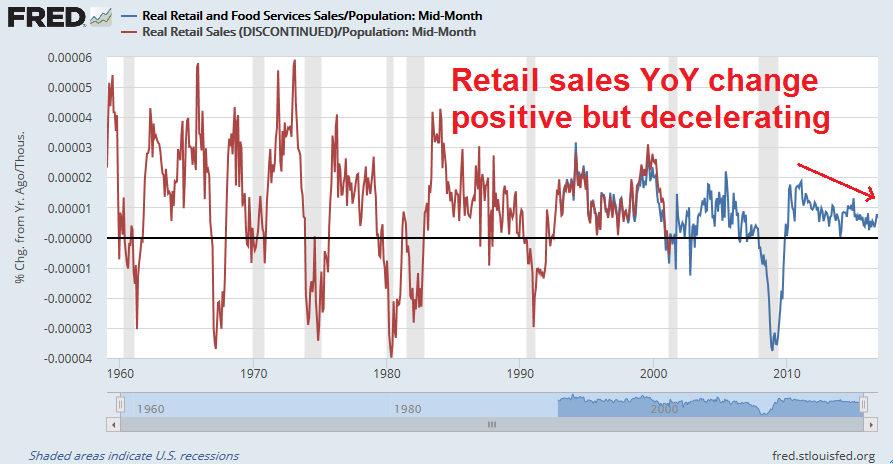

Despite Trump’s rhetoric about a revival of an America that’s on its knees, he inherits an economy that is growing and in the late stages of an expansion. This chart of initial jobless claims, normalized by population, shows that initial claims are at or near all-time lows.

Unemployment has been falling in the wake of the crisis of 2008, and it is at levels consistent with rising wages and rising inflationary pressures. These are further signs of a late cycle expansion, which is usually followed by the start of a Fed tightening cycle that ends in recession.

In addition, retail sales are robust, but decelerating, which is another indication of a late cycle expansion.

A second wind?

The counterfactual to these rosy economic statistics is the discontent that elected Donald Trump. True, the job picture has improved considerably since 2008, but the quality of jobs haven’t returned. For much of Main Street America, the “animal spirits” in the form of business dynamism has been missing. Economic Innovation Group found that most of the counties that swung from Obama to Trump in the election experienced a decline in business dynamism:

It appears that business closures helped the president-elect poach counties that had voted for President Obama twice before. Of these 209 counties, roughly 75% saw more businesses close than open from 2010 to 2014. It’s important to note that these counties ran the gamut from affluent to distressed; highly educated to below average; overwhelmingly white to majority-minority. In spite of their many differences, a decline in business dynamism is where the vast majority found common ground.

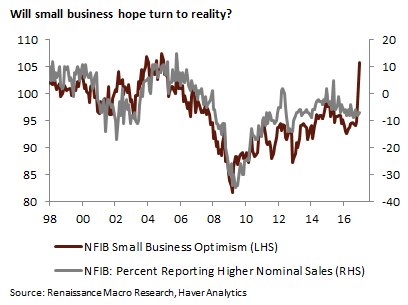

In the wake of Trump’s electoral win, Small business confidence has soared, though we have yet to see the revival in actual sales (see last week’s post Main Street bulls vs. Washington bears).

View through Main Street’s prism, Trump`s triumph has woken the economy’s dormant “animal spirits” out of hibernation.

Economic “animal spirits”

There are other ways of defining “animal spirits”. If we were to think about the idea of “animal spirits” like an economist, we might think of it in the monetary framework of:

MV = PQ

Where M = money supply, V = velocity, P = price, and Q = quantity

In other words, GDP (= Price x Quantity of goods and services) is a function of money supply growth and monetary velocity. While monetary theory held that V is constant over time, that hasn’t been true in practice. As the chart below shows, M1 money supply growth has been positive, which indicates that Fed policy remains acccommodative. However, monetary velocity has been falling dramatically, which has offset the Fed’s stimulus efforts through lower interest rates and several rounds of quantitative easing.

If the economy’s “animal spirits” were to revive, then one sign would be a rise in monetary policy. That hasn’t happened yet, though monetary velocity is a quarterly data series that is slow to update and therefore that data set is reported with a lag.

Investment’ “animal spirits”

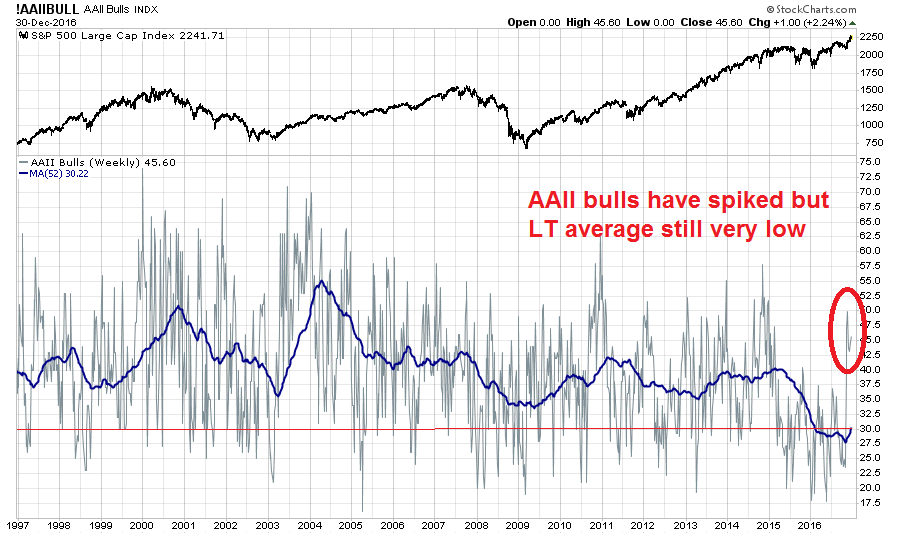

If we were to think about “animal spirits” from an investor’s viewpoint, it would be in the form of investor sentiment. As the chart of AAII sentiment shows, weekly readings are volatile and noisy. The 52-week moving average of the bull-bear spread (blue line) shows that long-term investor sentiment remains at depressed levels.

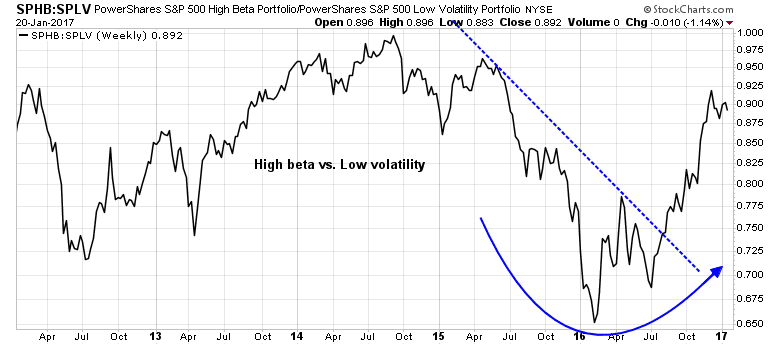

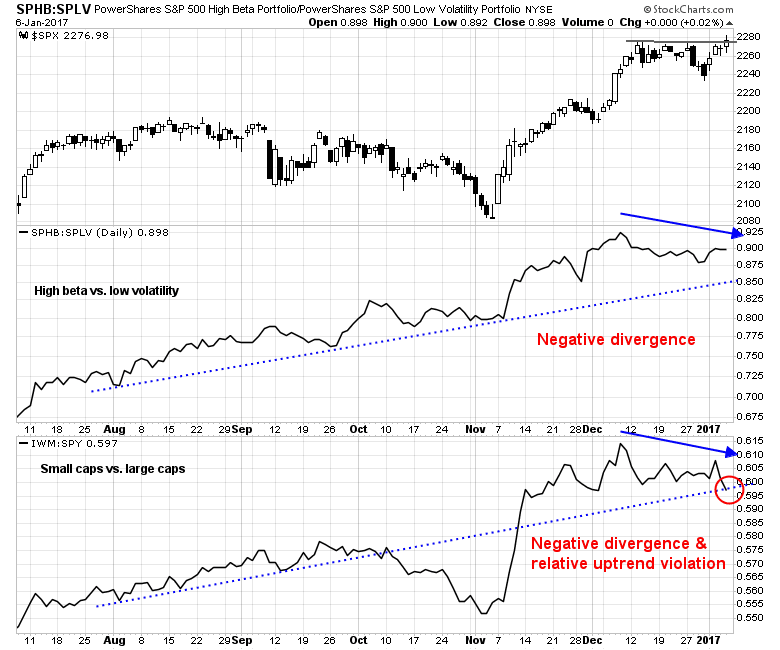

Indeed, this chart of the relative performance of high beta stocks against low-volatility stocks, which were the investment darlings of last year, shows that risk appetite is starting to revive. However, sentiment is nowhere near levels that could be described as frothy or a crowded long.

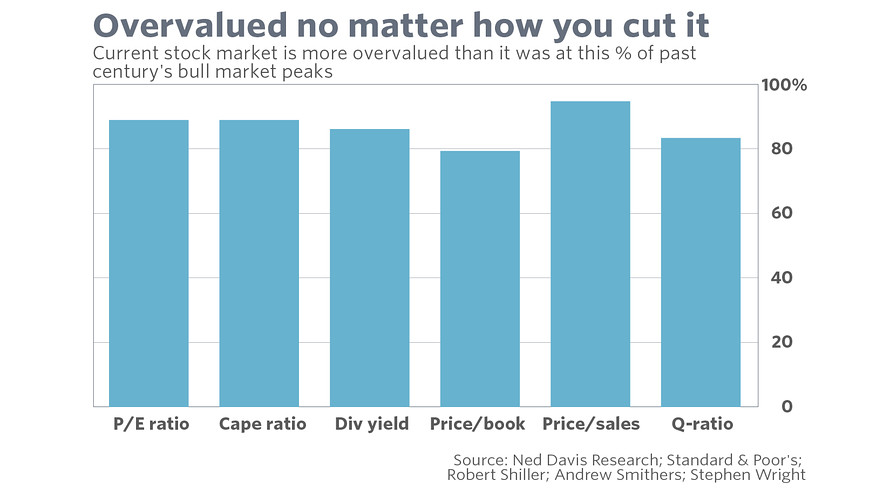

Recently, Mark Hulbert warned about valuation headwinds for stock prices and argued that stock prices were overvalued on a variety of metrics.

While I don’t necessarily agree with Hulbert’s assessment (see Top-down meets bottom-up: How expensive are stocks?), the one element that has been missing in this market cycle is the presence of excessive bullishness as one of the prerequisites of a market top. If investor “animal spirits” were to revive and we see a blow-off top, then that requirement would be complete.

Animal spirits: The bull case

So where does that leave us? The bull case is based on preliminary evidence of the revival of “animal spirits”. Ed Yardeni is optimistic:

A week after his election victory, I concluded that incoming President Donald Trump could succeed in stimulating economic growth, so I raised my real GDP forecast for 2017 from 2.5% to 3.0%. Since then, I’ve been keeping track of all the signs showing a revival of “animal spirits” in surveys of consumer and business confidence.

His YRI Weekly Leading Index, as well as the ECRI Weekly Index, have been surging.

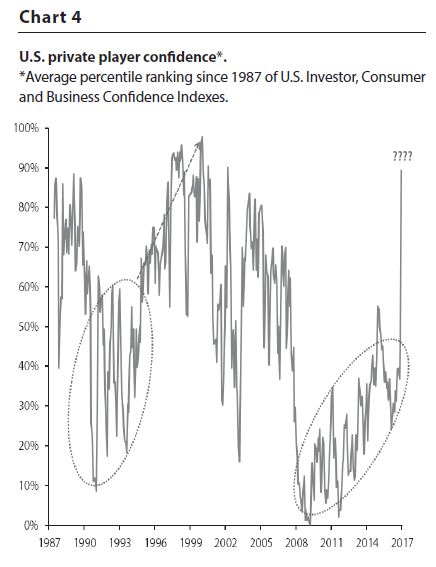

Jim Paulsen of Wells Capital Management is showing a similar level of cautious optimism. The chart below depicts a composite of investor, small business, and consumer confidence, all of which have surged to new cycle highs.

Paulsen went on to ask if investors are positioned for the next possible upleg:

Indeed, both investor and business confidence have probably spurted to unsustainable levels recently. Although both may decline somewhat again, given the impressive confluence of factors (shown above) which have recently formed to provide a foundation for this renewed optimism, it seems possible that overall private player confidence might remain much stronger during the balance of this recovery.

Investors may want to ruminate a bit on whether they are prepared and positioned for a potential second “confidence driven leg” to this economic and financial market recovery?

Animal spirits: The bear case

The bear case is based on the assertion that much of the factors behind the “animal spirits” consist of mostly smoke and mirrors.

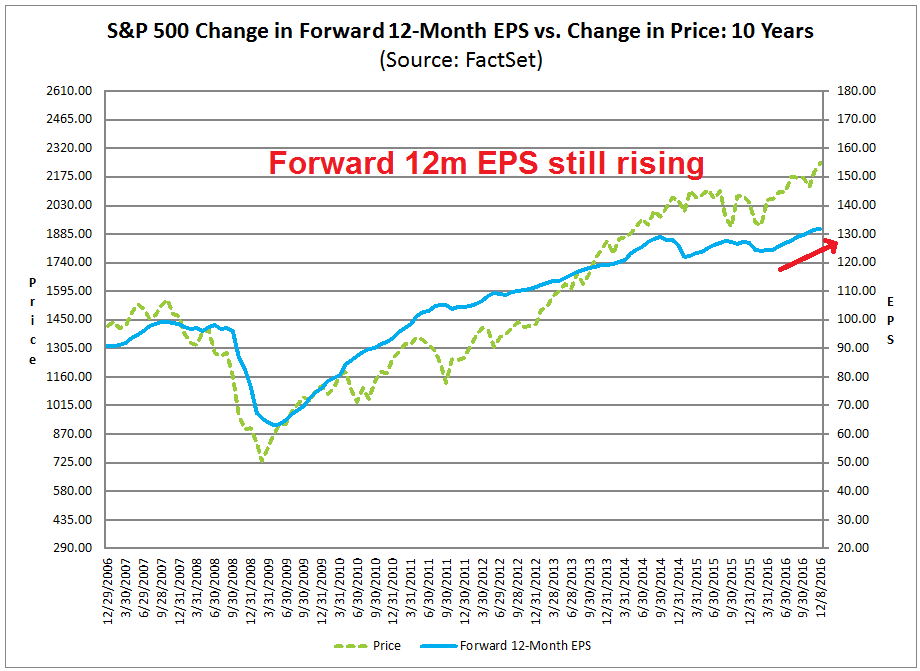

Consider, for example, Ed Yardeni’s observation of a rise in growth expectations. As the chart below of forward 12-month EPS from Factset shows, investors need to distinguish between the cyclical effect of a growth revival, and the “animal spirits” effect. Forward EPS had already been rising well before the election, so what we are observing might be a cyclical effect, rather than a second wind of growth based on improving business dynamism.

As for Trump’s claims of bringing jobs back to America, Josh Brown observed that corporate executives have learned to play the game:

Either before or after the tweet is sent about your company, you make a trip to Trump Tower on Fifth Avenue or to Mar-a-Lago (which will be the new combination White House / Camp David, by the way) and you parade ostentatiously before the bank of TV cameras. “Look at me! I’m down with the President’s agenda!”

Then a half hour later, you come down the golden elevator with the man himself, who holds an impromptu Q&A with you, as part of his end of the deal. Announcements of new jobs are made. New factories. New initiatives that will be undertaken, ASAP. Then he goes back up in his golden elevator for the next meeting and you get another 10 minutes of face time with the news crews. You grin optimistically, knowing that you and your company are off the Twitter shit list for awhile.

Mission accomplished.

It’s an old playbook, imported from the east. More on that in a moment.

One of the obvious things going on here, at least to the business world, is that much of this is just another reality show. There’s truth to these corporate pronouncements, but there’s plenty of artifice as well. It’s a pageant of sorts, designed for the consumption of the masses. To which I’d say, so what? If it gets the job done, let the man put on his show. Just don’t get overly excited about any sort of national transformation.

Business goes on as before. It really is all smoke and mirrors.

Resolving the bull and bear cases

So what’s the answer? Can Donald Trump spark the “animal spirits” in the economy? The jury is still out. Here are some observations from Avondale’s company notes:

The optimism is palpable

“The optimism for positive change here at Bank of America and among our customers is palpable and has driven bank stock prices higher. We will have to see how these topics play out, but we are optimistic.” —Bank of America CEO Brian Moynihan (Bank)

There’s a lot of optimism but not a lot of action

“there’s more optimism and positive commentary for a lot of our business customers. But we haven’t seen a significant change in utilization or actually take down of credit yet. So while the talk is there, the actual action is not yet shown itself.” —US Bank COO Andy Cecere (Bank)

“What I’m cautious about is nothing has actually happened yet, other than there has been a move in rates, right, and it changes sentiment. And I think we need to start seeing some of confirmations get through. We need to see real progress on tax reform. We need to see real progress on infrastructure, spending bills of state and local, and then all of a sudden, this thing takes flight, but right now, it’s just people talking about it.” —PNC CFO Rob Reilly (Bank)

For the last word, I conclude with a CNBC interview with Ray Dalio. Notwithstanding his tremendous optimism about the “can-do” attitude of Americans, Dalio believes that the market had largely discounted the obvious changes, such as the Trump tax cuts. Now there are more questions than answers with regards to policy implementation, such as how Trump’s fiscal plan gets turned into legislation, as well as geopolitical questions like as Sino-American relations.

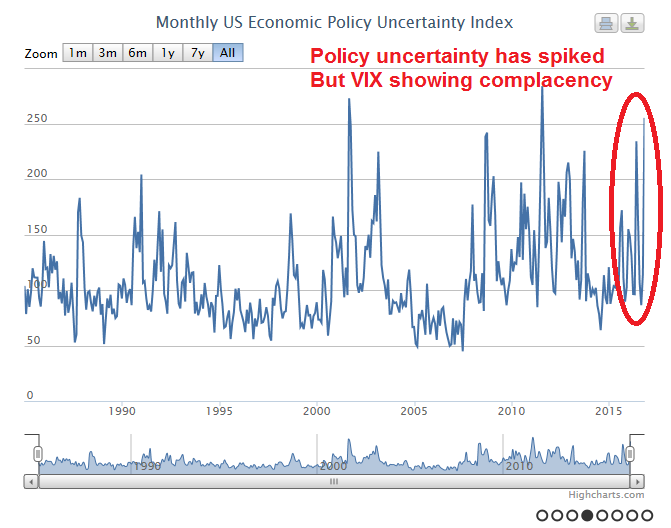

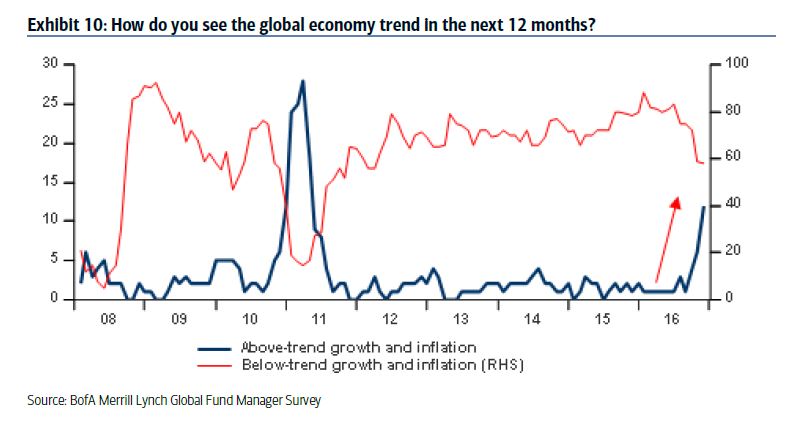

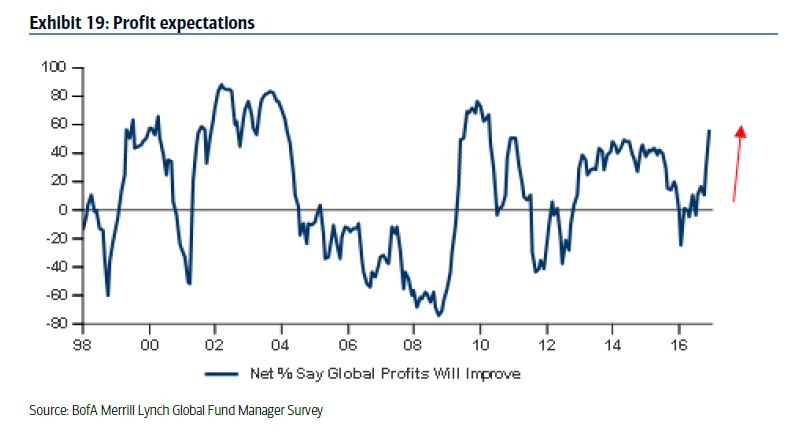

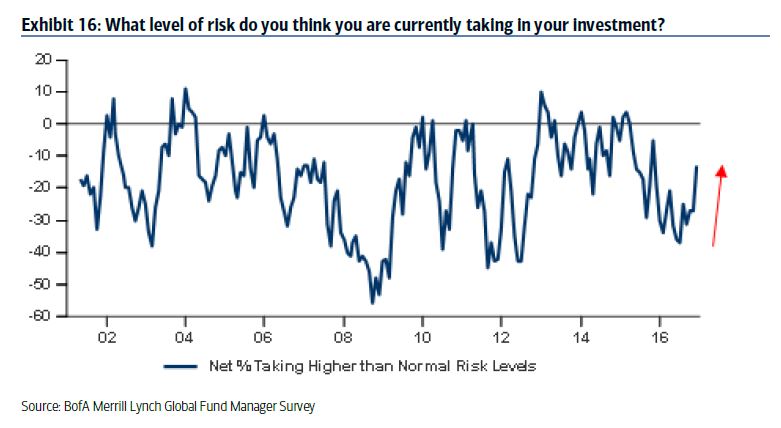

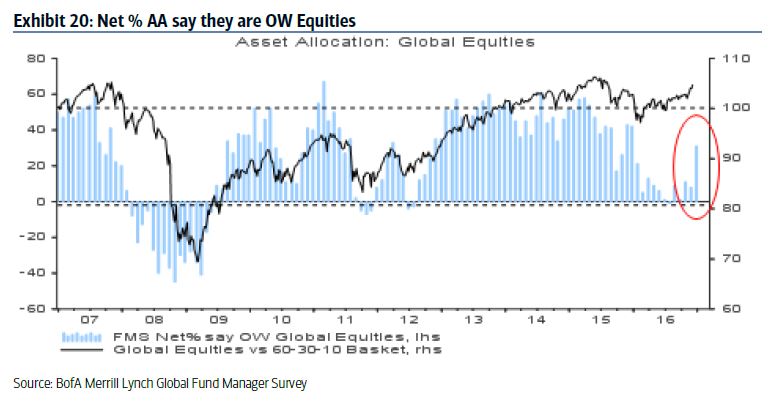

In the coming weeks, we will undoubtedly see some of the bumps in the road that will create uncertainty, raise the risk premium, and spook the markets. The latest BAML Fund Managers Survey shows that fund managers are deathly afraid of a protectionist backlash, or US policy error (annotations in red are mine).

Indeed, assertive language like this on trade on the White House website will undoubtedly unnerve investors:

President Trump is committed to renegotiating NAFTA. If our partners refuse a renegotiation that gives American workers a fair deal, then the President will give notice of the United States’ intent to withdraw from NAFTA.

In addition to rejecting and reworking failed trade deals, the United States will crack down on those nations that violate trade agreements and harm American workers in the process. The President will direct the Commerce Secretary to identify all trade violations and to use every tool at the federal government’s disposal to end these abuses.

We will see next week how much of these fears have been discounted by the market.

The week ahead

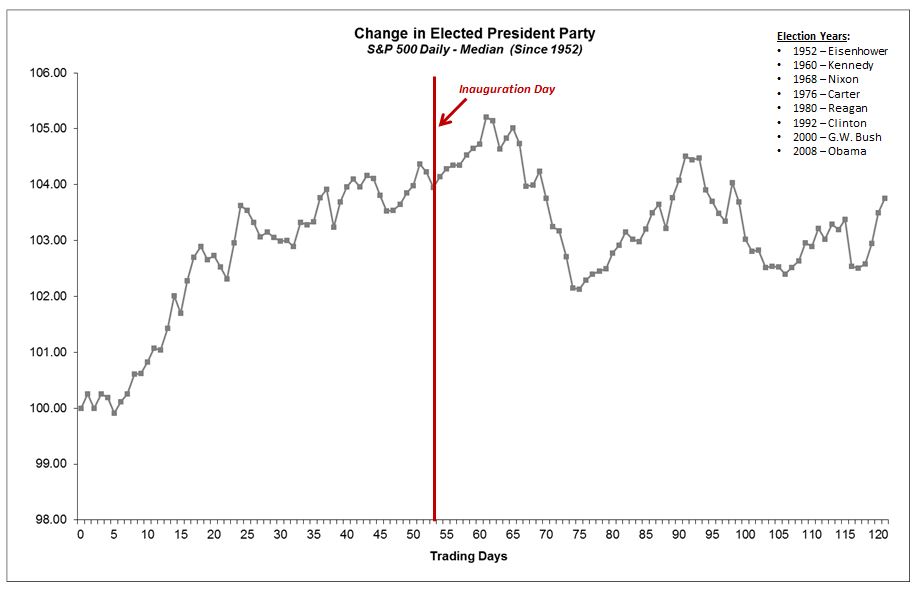

Looking to the week ahead, the stock market will face its first test under a Trump administration. At a minimum, can it at least conform to the inauguration pattern as outlined by Alpha Hat (via Business Insider)? Historically, the market typically rallies for about two weeks after inauguration, followed by a February correction. Longer term, however, Republicans president markets have tended to underperform.

The market action on Friday did not give any strong clues. The hourly chart of the SPY shows that the market broke down through and uptrend on Thursday, but rallied to (barely) regain the trend line. At this point, it’s unclear whether the breakdown below the trend line was a false break.

My inner investor remains long the market. His base case scenario calls for a shallow correction in Q1, followed by a rally later in the year. Market internals appear to be setting up for a period of sideways consolidation or pullback (see The contrarian message from rotation analysis).

My inner trader still has a small short position in the market, but he will close that short should the market break out to new highs.

About a month ago (see The bear case: How Trumponomics keeps me awake at night), I highlighted a Bloomberg interview with BAML currency strategist David Woo. Woo pointed that there is an inherent contradiction in a couple of Trump’s policies. His fiscal policy of tax cuts is pro-growth and therefore USD bullish, but his “America first” trade policy needs a weaker dollar. So what does he really want, a strong dollar, or a weak dollar?

We may have an answer. In a recent WSJ interview, Trump said that the dollar is “too strong”, especially considering the China’s yuan is “dropping like a rock.” While those remarks were made in the context of Sino-American trade relations, Trump signaled that, if he had to choose, he would prioritize a weaker currency over fiscal stimulus.

Trump`s priorities of trade policy over fiscal policy is consistent with his criticism of the House Republican border tax adjustment plan as “too complicated“ (via WSJ). Already, the spectacle of passing a fiscal budget, even with Republican control of the White House, the Senate, and the House, is turning into a public “sausage making“ exercise.

A strategy of USD weakness makes more sense for Trump if he wants to achieve his trade policy objectives. As Larry Summers pointed out, Trump’s populist message of attacking trading partners like Mexico has the unintended effect of depressing the Mexican Peso. A lower MXNUSD exchange rate paradoxically incentivizes companies to move production south of the Rio Grande (via AP and Business Insider):

Summers told a panel at the World Economic Forum on Wednesday that the president-elect’s “rhetoric and announced policies” over Mexico have led to a big fall in the value of the Mexican peso against the dollar.

That, he said, is a “dagger at Ohio,” as it will make it even more attractive for firms to move to Mexico.

How to weaken the USD

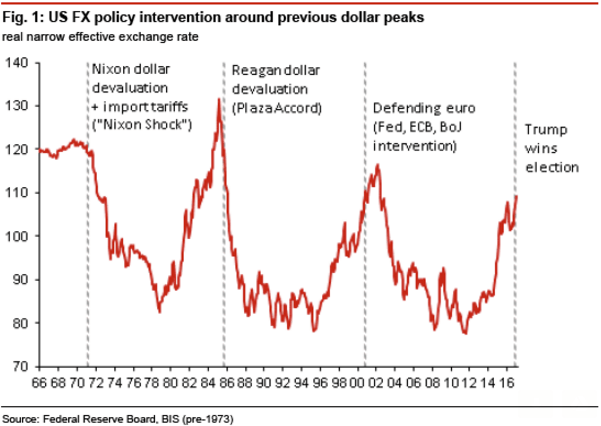

Bloomberg featured an article that outlined several options that the US government could employ to weaken its currency, along with the pros and cons of each approach.

A couple of previous notable Republican Presidents have been responsible for currency intervention, as seen in this handy chart.

Should the Trump administration want to go down this path, I believe that the Plaza Accord may be the best template for crafting an agreement to weaken the USD. Trump`s threats of protectionist measures may be enough for other major trade blocs to agree to weaken the USD in the manner of the Plaza Accord of 1985.

USD bear = Gold bull

That brings me to another point. Should the Trump administration succeed in crafting another Plaza Accord, a weak greenback would be gold bullish. The chart below depicts the price of gold (blue line) and the trade weighted USD (red line, inverted scale), along with the major interventions shown in the previous chart. Should an agreement be reached to weaken the dollar, then historically that has marked the beginning of a major gold bull.

At this point, such a scenario is highly speculative. However, investors should be prepared for such an eventuality and its investment consequences, should it ever occur.

Mid-week market update: Occasionally, it is useful to step back and view the market through a different prism. I was reviewing the RRG charts of sector, region, and factor, and I found that they are all telling a similar story.

First, let’s start with a primer. Relative Rotation Graphs, or RRG charts, are a way of depicting the changes in leadership in different groups, such as sectors, countries or regions, or market factors. The charts are organized into four quadrants. The typical group rotation pattern occurs in a clockwise fashion. Leading groups (top right) deteriorate to weakening groups (bottom right), which then rotates to lagging groups (bottom left), which changes to improving groups (top left), and finally completes the cycle by improving to leading groups (top right) again.

The latest sector rotation chart shows that financial stocks and cyclical stocks (energy, industrials, materials) are the leading groups, but they are weakening. By contrast, defensive sectors are starting to improve from the lagging quadrant to improving. In particular, the upgrade of interest sensitive utilities from lagging to improving quadrant is consistent with the nascent counter-trend rally seen in the bond market.

In short, high beta is faltering and defensive sectors are starting to turn up.

Confirmation from Europe

The trend of waning risk appetite appears to be global in nature. We can see a similar pattern in the RRG chart of European sectors. The main difference between the US and European RRG charts is the behavior of the materials sector. The European basic materials sector has already deteriorated into the weakening quadrant, whereas US materials remain in the top right leading category.

Style rotation: Too far too fast?

The message from style rotation of US equities also tells a similar story. High beta groups are ascendant, but starting to weaken. The value style, which had been on a tear, is also starting to roll over in relative strength. By contrast, out of favor styles such as dividend payers, as well as growth and momentum (think FANG), are starting to turn up.

Global regions: Buy Europe and Asia

A glance at regional and country rotation tells a story of cyclical factors starting to roll over. The leadership countries are Russia and Canada (oil), and the US. Europe appears to be a source of emerging strength, while Asian markets are lagging, but starting to improve. Tactically, traders may wish to consider selling their cyclical exposure and start to add exposure to Europe and Asia.

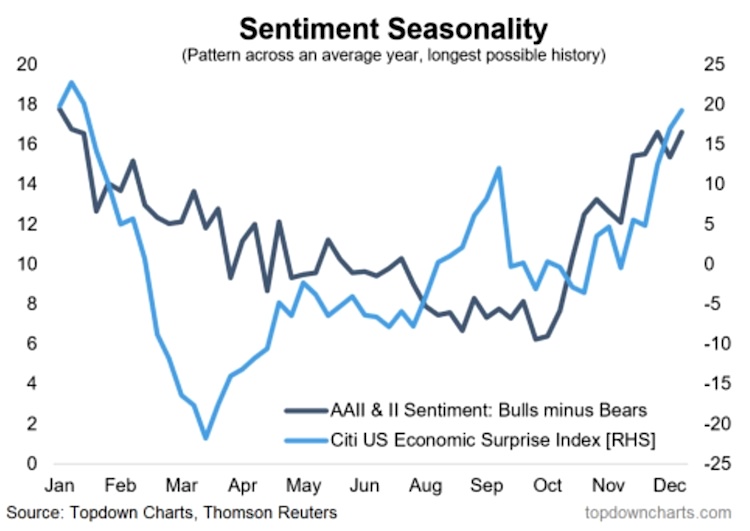

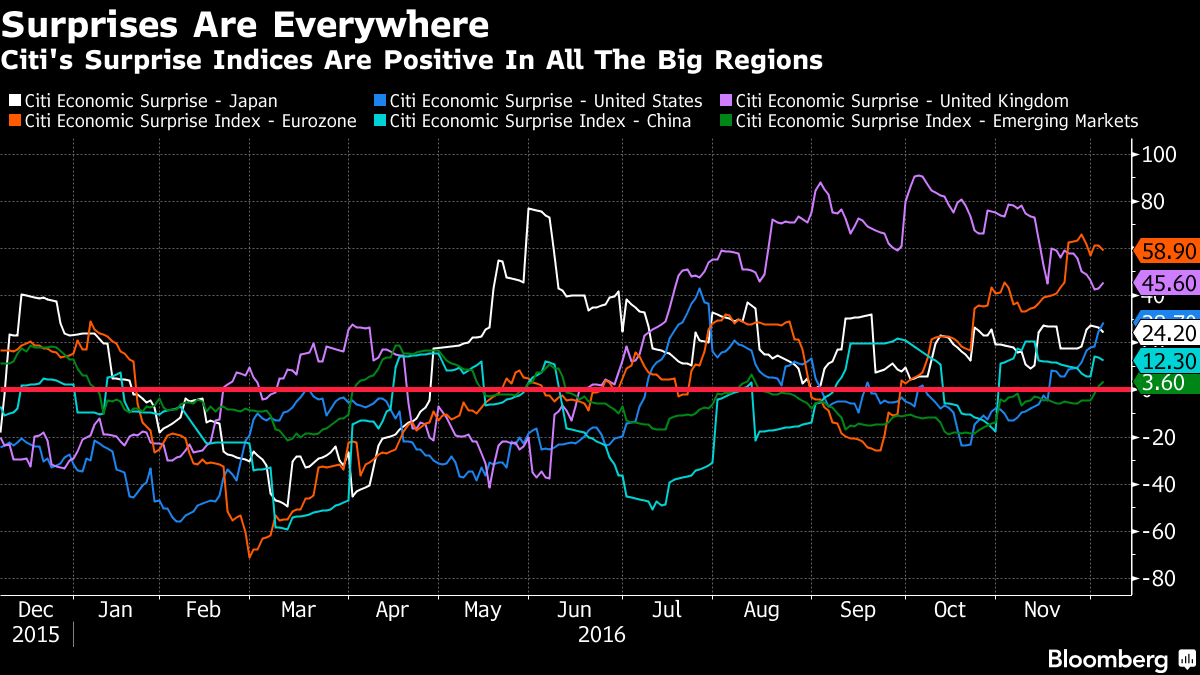

From a top-down macro perspective, even though Citigroup’s Economic Surprise Index have been surging, the market believes that the pace of improvement is probably unsustainable (h/t Topdown Charts).

Be contrarian

From an absolute return viewpoint, the de-risking pattern from the RRG charts suggests that US equities are likely to undergo a period of sideways action, or mild pullback for the remainder of Q1.

In addition, the message from group rotation analysis is a cyclical rally that is starting to stall. Better performance may be found in some of the laggards, such as emerging leadership groups like interest sensitives (utilities, bond market), or European equities (in the face of anxieties over Brexit and upcoming elections in France and Germany). As well, traders may also want to consider beaten up and out of favor groups, such as growth and momentum stocks, as well as Asian equities.

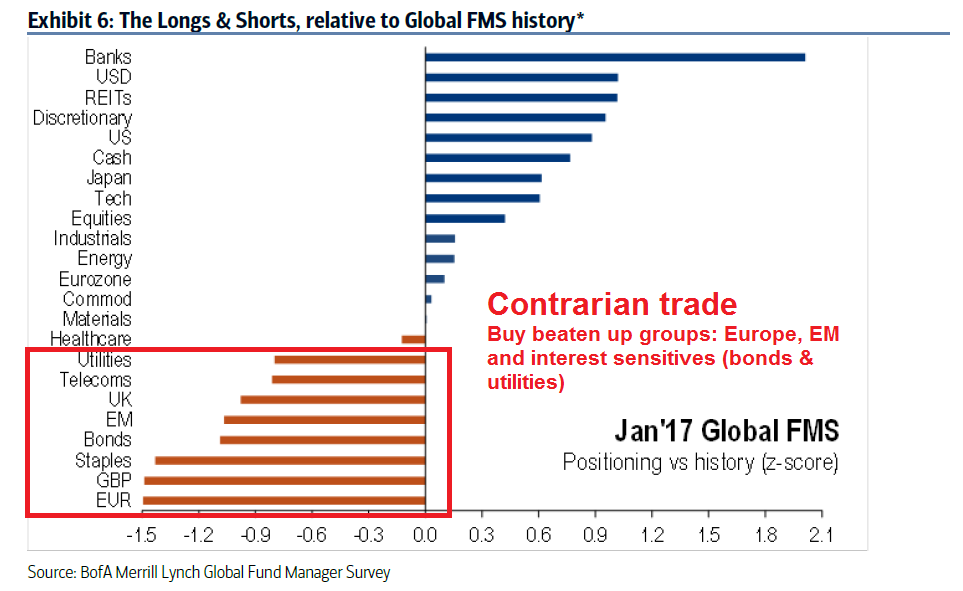

In other words, be contrarian. This view is confirmed by the latest results in the BAML Fund Manager Survey (annotations in red are mine).

Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Model is an asset allocation model which applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. In essence, it seeks to answer the question, “Is the trend in the global economy expansion (bullish) or contraction (bearish)?”

My inner trader uses the trading component of the Trend Model to look for changes in direction of the main Trend Model signal. A bullish Trend Model signal that gets less bullish is a trading “sell” signal. Conversely, a bearish Trend Model signal that gets less bearish is a trading “buy” signal. The history of actual out-of-sample (not backtested) signals of the trading model are shown by the arrows in the chart below. Past trading of the trading model has shown turnover rates of about 200% per month.

The latest signals of each model are as follows:

Ultimate market timing model: Buy equities

Trend Model signal: Risk-on

Trading model: Bearish

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers will also receive email notices of any changes in my trading portfolio.

Bifurcated opinions

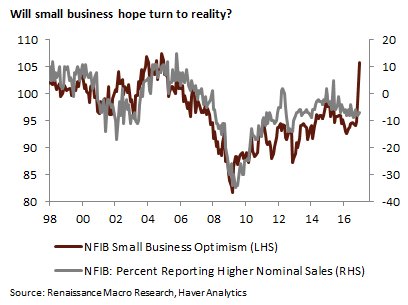

Opinions are starting to split badly on the market and the economy. Main Street has become more upbeat on the economic outlook. The NFIB small business survey showed that optimism surged in December, though Renaissance Macro pointed out that optimism has not translated yet into a significant upswing in sales growth.

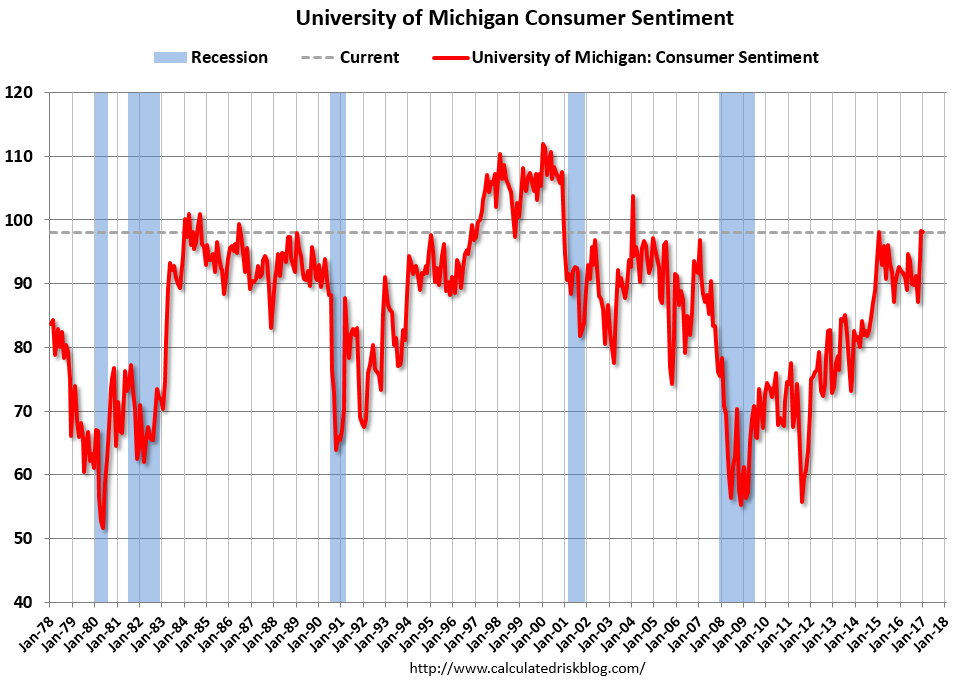

The preliminary January report of UMich consumer confidence shows that it is elevated, though opinions are reportedly split along political lines:

The post-election surge in optimism was accompanied by an unprecedented degree of both positive and negative concerns about the incoming administration spontaneously mentioned when asked about economic news. The importance of government policies and partisanship has sharply risen over the past half century. From 1960 to 2000, the combined average of positive and negative references to government policies was just 6%; during the past six years, this proportion averaged 20%, and rose to new peaks in early January, with positive and negative references totaling 44%.

By contrast, I am seeing signs of doubt from political circles that Trump will be successful with his pro-growth agenda, even among Republicans. Traditional approaches to sentiment analysis states that the public tends to be slow. When the public finally latches onto an economic theme, it is indicative of a contrarian top (or bottom). On the other hand, the improvement in business and consumer confidence can be signals of broad based economic strength.

So who is right? Main Street, or Washington?

The stakes are high

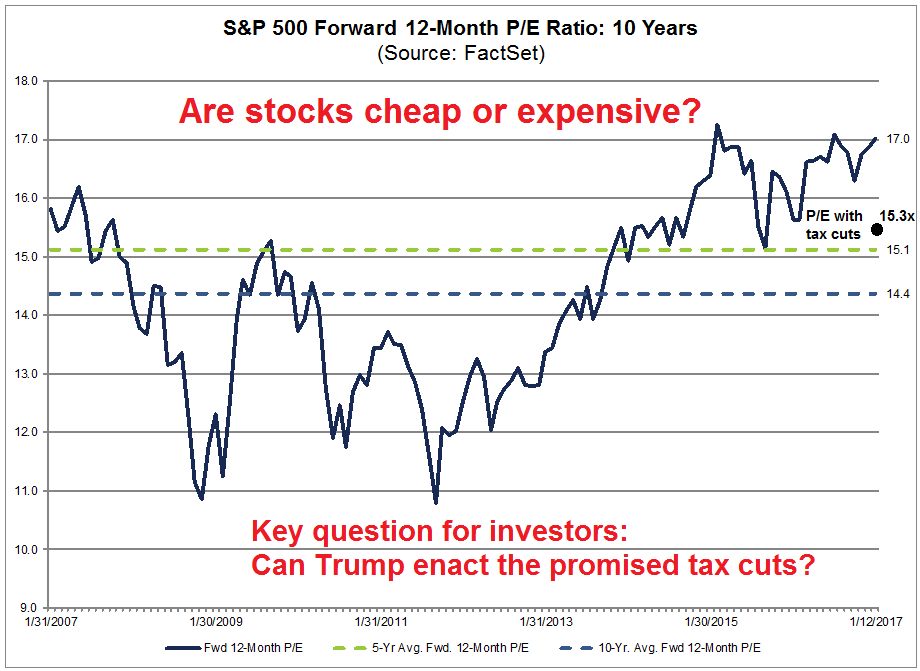

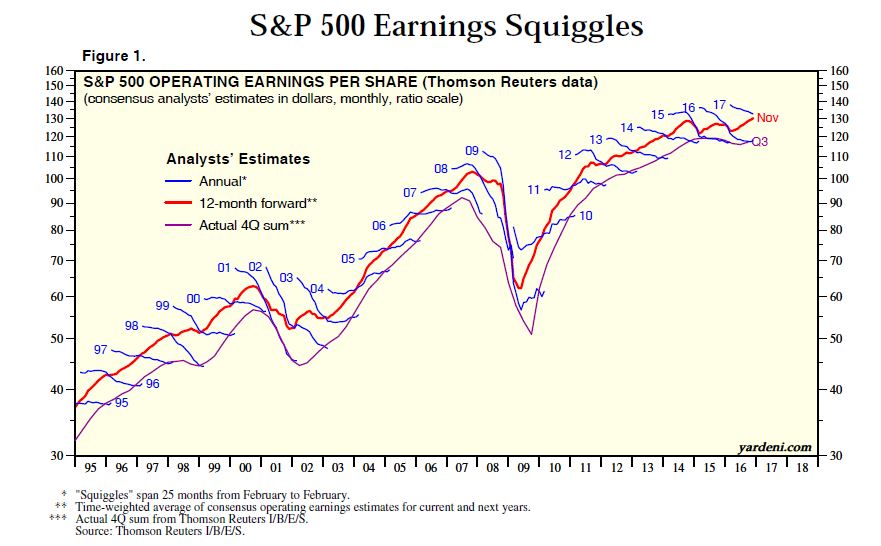

Here is what’s at stake for equity investors. As we enter earnings season, Factset shows that forward EPS continues to rise, which is indicative of Street expectations of broad based cyclical strength.

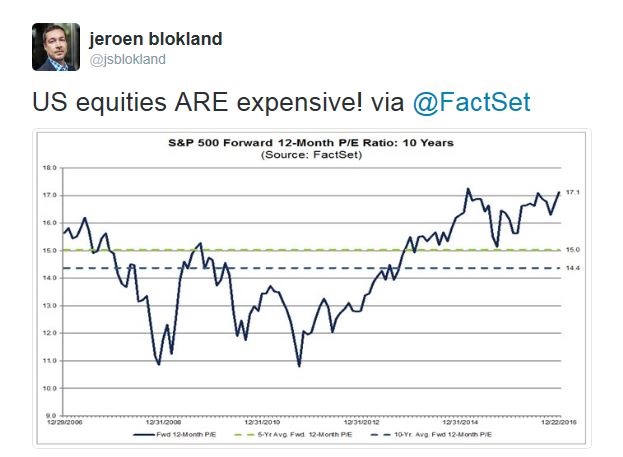

However, broad based cyclical upturn can only get you so far. This Factset chart also shows that forward P/E ratio is elevated and expensive compared to its own history. Current forward P/E is based on bottom-up derived earnings based only analyst expectations of economic conditions without the Trump fiscal plan. That’s because you can’t make estimates when you don’t have the details of the proposals. A top-down analysis suggests that the Trump tax cuts could add roughly 10% to forward earnings, which would bring down the forward P/E ratio to more reasonable levels (annotations are mine).

To rephrase my previous question: Who is right about the expectations for the Trump tax cuts? Main Street or Washington?

Republican skepticism

When Donald Trump takes his oath of office, he will be entering the White House with an unusually high unfavorability rating for an incoming president. It is therefore no surprise that consumer confidence is bifurcated and there is skepticism from Democrats that he will be able to implement all of the policies that he promised on the campaign trail.

I was surprised that skepticism is also coming from die hard Republicans. Bloomberg report that Republican governor of Kansas, Sam Brownback, had words of caution for the incoming president:

The governor of Kansas has some wisdom for Donald Trump, from one Republican tax-cutter to another: The reductions may take longer than expected to give the economy a sustained lift.

Like President-elect Trump, who said on the campaign trail that slashing taxes would jump-start growth, Sam Brownback in 2012 said steep cuts to personal income and small-business taxes in the Midwest state would provide the economy a“shot of adrenaline.” What followed wasn’t the promised jolt. The shortfall in revenue has instead forced the government to curtail spending on everything from health care to higher education.

John Mauldin, market analyst and staunch Republican from Texas, described himself as “skeptically optimistic” about the new regime. Passing legislation is never easy. Seemingly straightforward proposals can get delayed, watered down, or simply fall apart:

I’m told the Republicans have a long list of relatively uncontroversial (at least on their side of the aisle) bills that they can pass very quickly. They want to show progress, and they think quick passage of some popular measures will buy them credibility to use later. I expect an initial burst of activity after January 20, probably followed by a lull as the Congress moves into more contentious issues like Social Security and healthcare reform. Things will keep happening, but we may not see as many votes.

The hard part is getting agreement on the big items like taxes and healthcare reform. I love seeing Trump and Pence and Ryan and McConnell and all the guys holding hands and acting as if they’re all ready to walk into the bright new future together, but the reality is that there are some quite different ideas in Washington about what serious reforms should look like, and a lot of congressmen want to put their personal stamp on the final bills.

The reform effort could fall apart for various reasons. The Senate majority is narrow enough that just a handful of GOP defectors will be able to stop any given bill, assuming Democrats stay united in opposition. I think Republicans should be on guard against hubris, as well. The decision last week to kick off the year by softening ethics rules was a terrible idea. They accomplished nothing and energized an opposition that was otherwise on its heels.

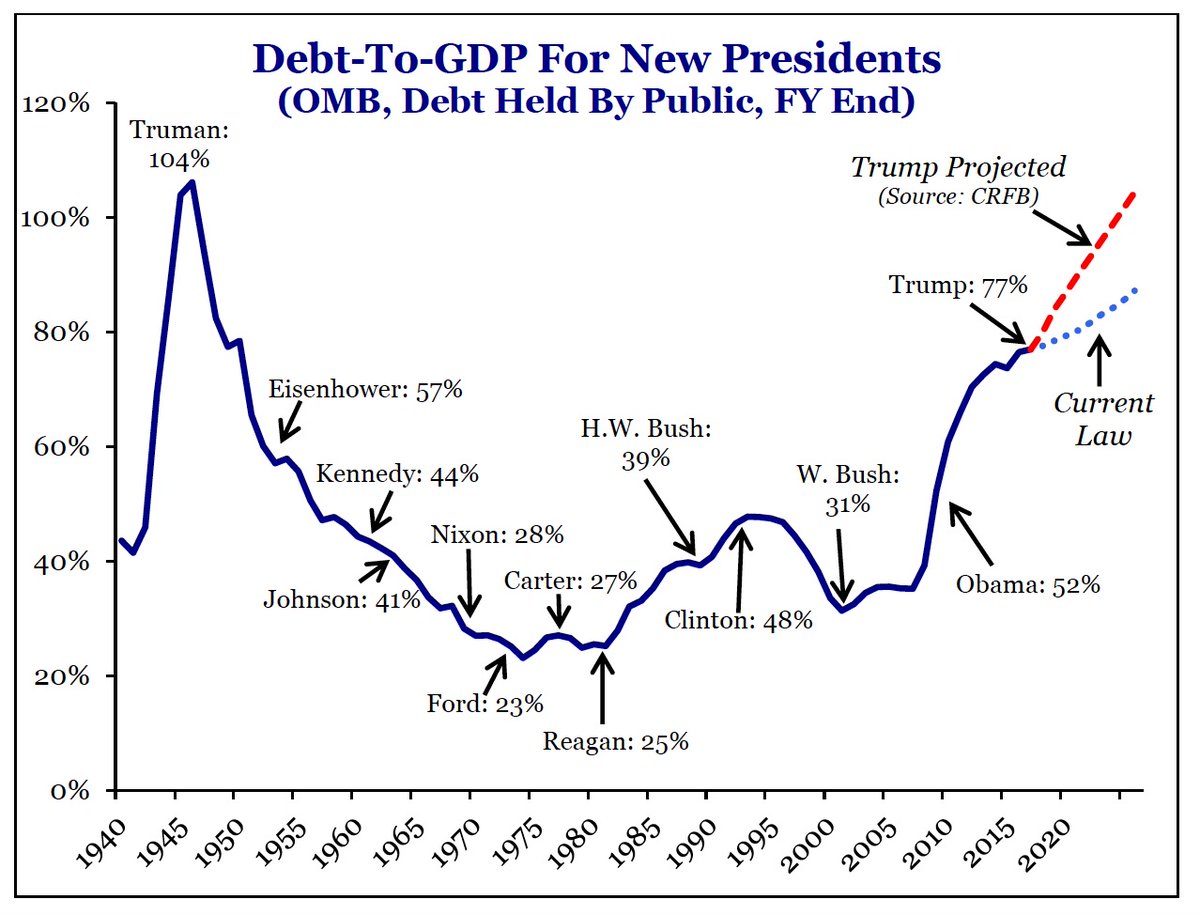

As an example, this pattern of debt to GDP could give GOP deficit hawks some pause as they consider Trump’s fiscal plan, which is expected to balloon the deficit.

Maudlin added that the new administration could get distracted by an unexpected crisis that weakens its ability to pass legislation.

Finally, as I cautioned last week, there is always the chance that some “bolt from the blue” could change everything. An international crisis, a large bank failure, terror attacks – any one of a long list of unforeseeable events could conceivably derail this train. Not to mention the endemic problems of Europe and China, which we will deal with below and which are entirely foreseeable. But if we can get through the first 100 days with this administration, then I think its agenda will have enough momentum to keep rolling.

The latest story that Russian intelligence had compromised Trump is just one of many tests that will face the new administration. The Lawfare blog had a the most balanced perspective that I had seen on this episode.

First, we have no idea if any of these allegations are true. Yes, they are explosive; they are also entirely unsubstantiated, at least to our knowledge, at this stage. For this reason, even now, we are not going to discuss the specific allegations within the document.

Second, while unproven, the allegations are being taken quite seriously. The President and President-elect do not get briefed on material that the intelligence community does not believe to be at least of some credibility. The individual who generated them is apparently a person whose work intelligence professionals take seriously. And at a personal level, we can attest that we have had a lot of conversations with a lot of different people about the material in this document. While nobody has confirmed any of the allegations, both inside government and in the press, it is clear to us that they are the subject of serious attention.

Third, precisely because it is being taken seriously, it is—despite being unproven and, in public anyway, undiscussed—pervasively affecting the broader discussion of Russian hacking of the election. CNN reported that Senator John McCain personally delivered a copy of the document to FBI Director James Comey on December 9th. Consider McCain’s comments about the gravity of the Russian hacking episode at last week’s Armed Services Committee hearing in light of that fact. Likewise, consider Senator Ron Wyden’s questioning of Comey at today’s Senate Intelligence Committee hearing, in which Wyden pushed the FBI Director to release a declassified assessment before January 20th regarding contact between the Trump campaign and the Russian government. (Comey refused to comment on an ongoing investigation.)

Politico reported that, on late Friday after the market close, the Senate Intelligence Committee has opened an investigation into this affair, Even before the Inauguration, this inquiry already has the potential to either distract the Trump team or weaken its apparent authority to pass legislation.

A Trumpian “animal spirits” revival?

Independent of what happens inside the Beltway, the latest NFIB survey represents a boost to economic confidence. Even though small business owners tend be conservative and therefore not reflective of views the general population, Ed Yardeni made some good points on why small business confidence matters:

(1) Small business is big employer. ADP, the payroll processing company, compiles data series on employment in the private sector of the U.S. labor market by company size. At the end of 2016, the shares of employment attributable to small, medium-sized, and large firms were 40.5%, 37.7%, and 21.8%.

(2) Small business drives jobless rate. There has been a very high correlation between “poor sales” reported by small business owners and the national unemployment rate. If Trump succeeds in boosting their sales by cutting personal income tax rates, the jobless rate should remain low.

There is also a high correlation between the earnings of small businesses and the inverse of the poor sales. Trump’s proposed tax cuts would boost their earnings, which are inversely correlated with the national unemployment rate.

Yardeni believes that rising small business confidence is a sign that the economy’s “animal spirits” are stirring, which will serve to drive further growth. Another manifestation of these “animal spirits” can also be found in the recovery in consumer confidence, despite the political bifurcation of opinions.

Investment implications

How should investors resolve this apparent contradiction? Should they be cautious, or bullish?

I interpret these conflicting signals in terms of differing time frames. It turns out that consumer confidence are coincidental indicators (via Bill McBride of Calculated Risk):

Consumer sentiment is a concurrent indicator (not a leading indicator). The survey shows some people are now much more positive than prior to the U.S. election – and others are much more negative.

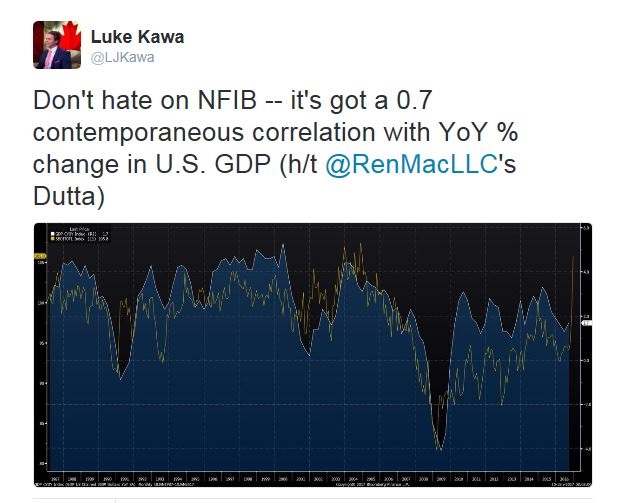

Luke Kawa also observed that small business confidence is highly correlated with GDP growth, which makes it another coincidental indicator.

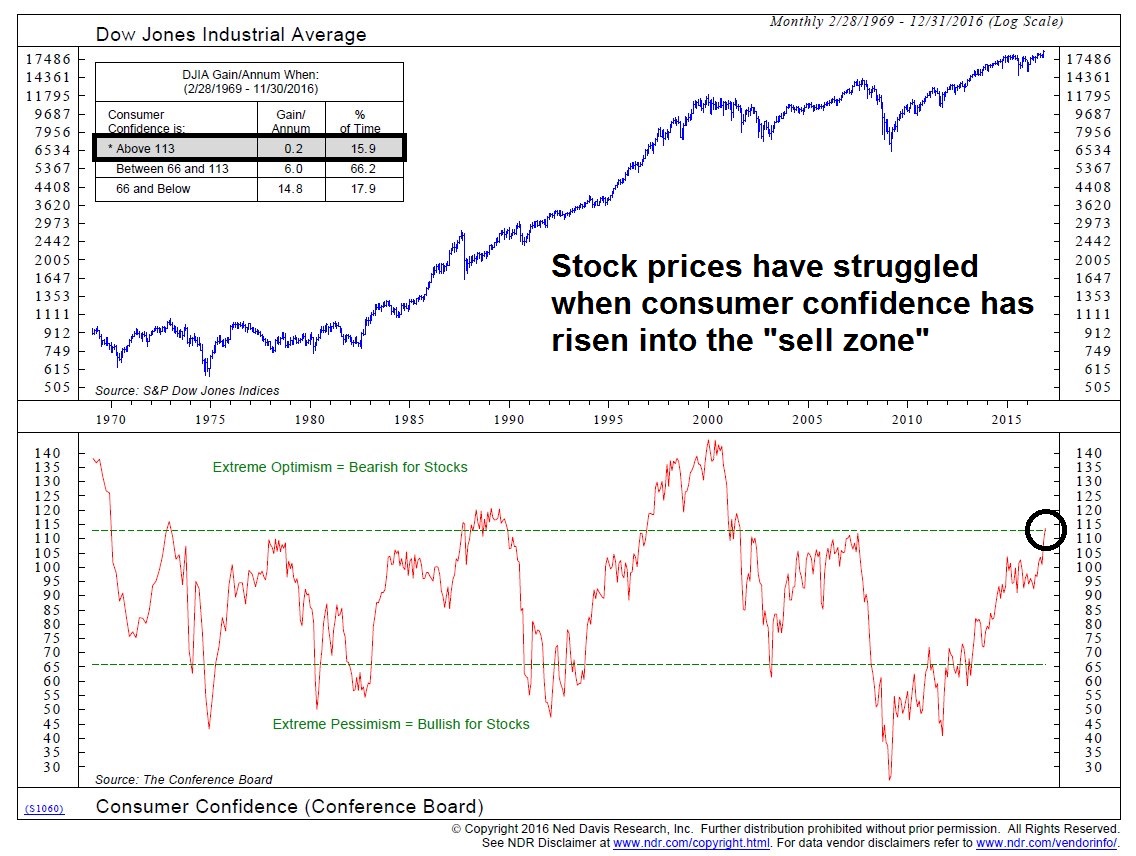

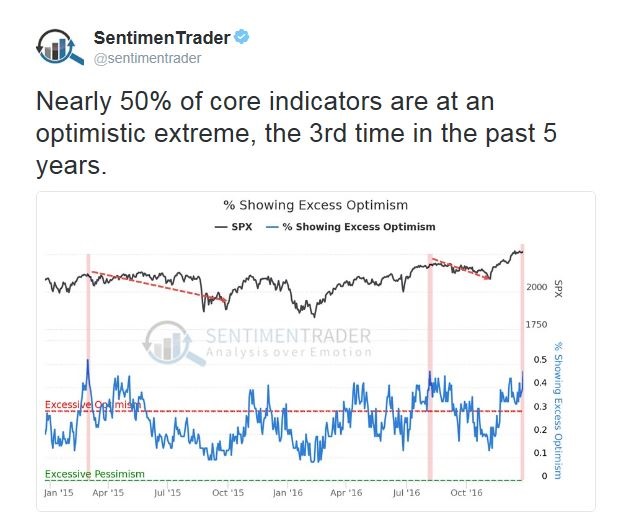

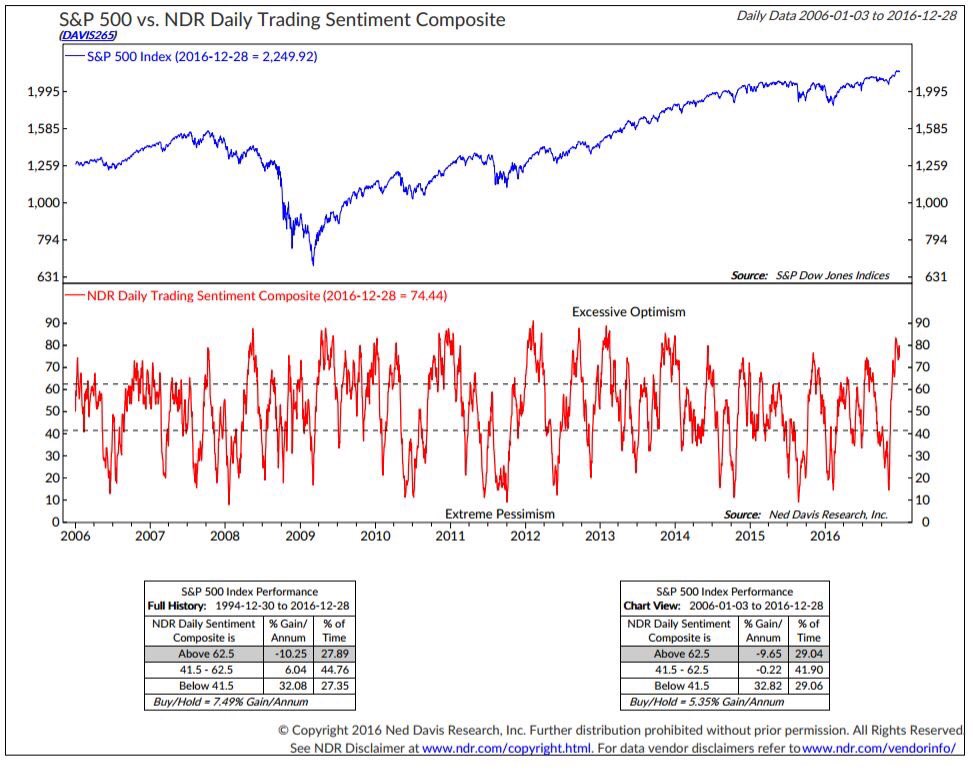

If you try to forecast a leading indicator, like stock prices, with coincidental indicators, it doesn’t work very well. In fact, Ned Davis Research found that extreme readings in consumer confidence can be used as contrarian indicators – and it’s flashing a sell signal right now (annotations are mine).

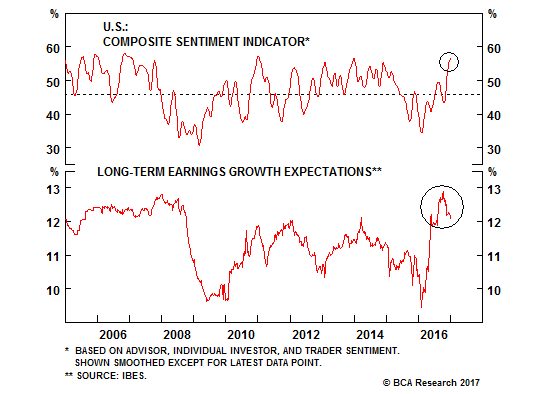

In the short term, the Trump rally looks overdone. Mark Hulbert reported that his sample of NASDAQ market timers is at a crowded long level, which is contrarian bearish.

The inverse of contrarian sentiment is insider activity. The latest update from Barron’s of insider trading is flashing a sell signal as this group of “smart investors” have stepped up their selling for a second consecutive week.

From a cross-asset viewpoint, the disappointing tone of Trump’s tone in his Wednesday press conference served to deflate the US Dollar and therefore also has bearish implications for equities. Instead of talking up tax cuts and deregulation, the president-elect chose to focus on protectionism (via CNBC):

The U.S. dollar index hit a one-month low Thursday after President-elect Donald Trump disappointed investors in a Wednesday press conference. Rather than discussing infrastructure spending, deregulation or tax cuts, Trump emphasized a tough position on trade and a border tax.

“The market had priced in a very positive scenario of Trump: fiscal policy without trade protectionism,” said Athanasios Vamvakidis, a European currency strategist in Europe for Bank of America Merrill Lynch.

“That’s why the press conference is a scare,” he said, noting that traders are now focused on the dollar and what the new administration does after next Friday’s inauguration.

This chart from Hedgopia shows that the USD Index is pulling back, but large speculators are still in crowded long position. That’s a recipe for further weakness.

Short term cautious, medium term bullish

My own views are well summarized by BCA Research‘s expectations for equity markets. In the short term, bullish sentiment is overdone and a period of consolidation or pullback can be expected. Longer term, growth expectations are still high and stock prices should rise after a corrective episode.

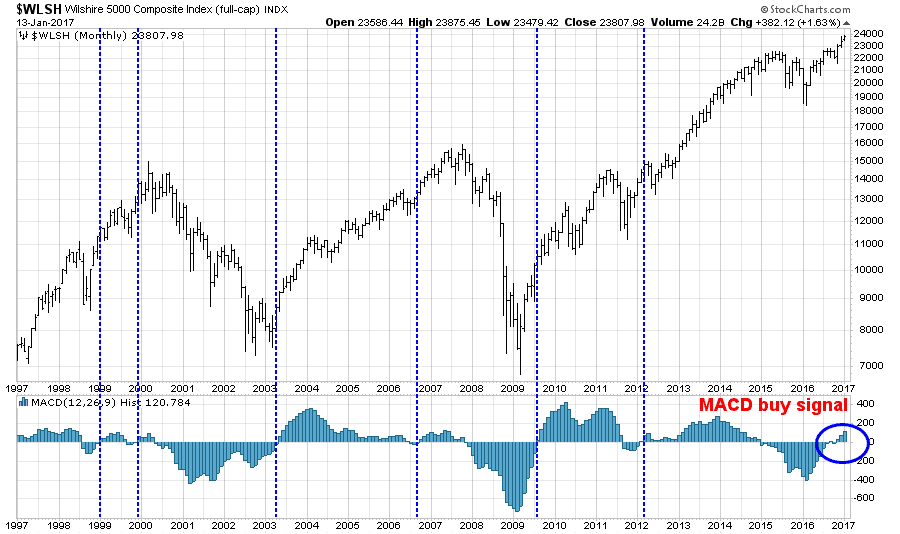

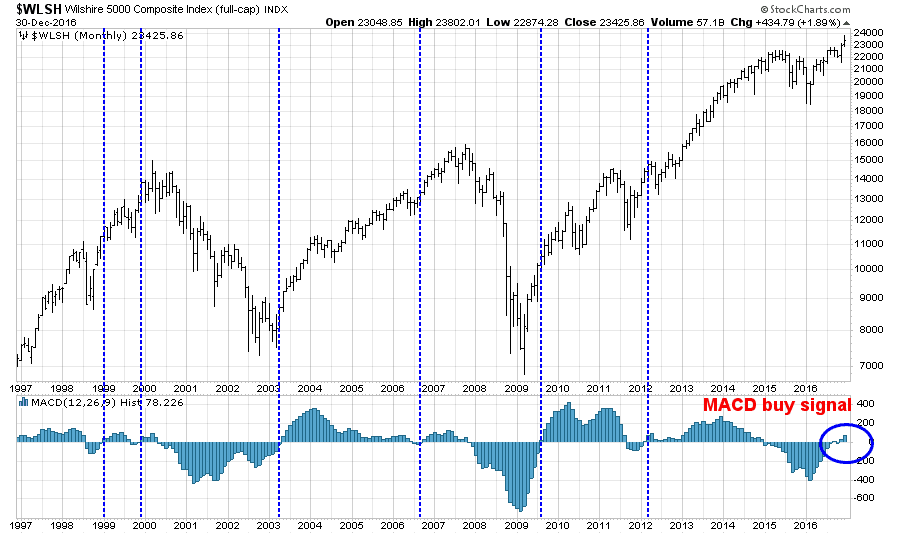

From a technical perspective, the MACD buy signal for the Wilshire 5000 based on monthly price data remains in force.

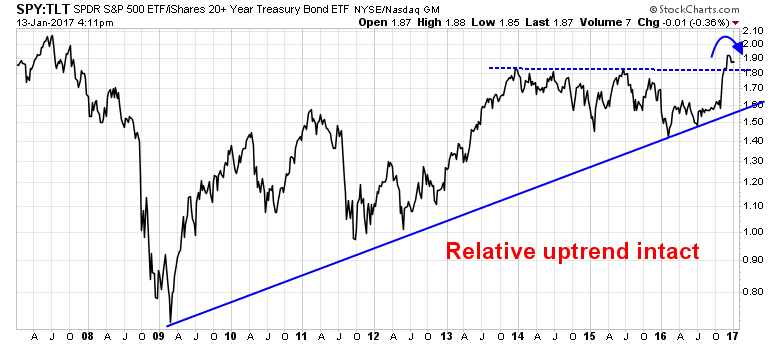

We can see a similar pattern from the relative performance of stocks (SPY) vs. Treasuries (TLT). The longer term trend remains bullish, but stocks have started to pull back against bonds. Further short-term weakness would be no surprise. As long as the long term trend remains intact, my inner investor is inclined to remain equity bullish.

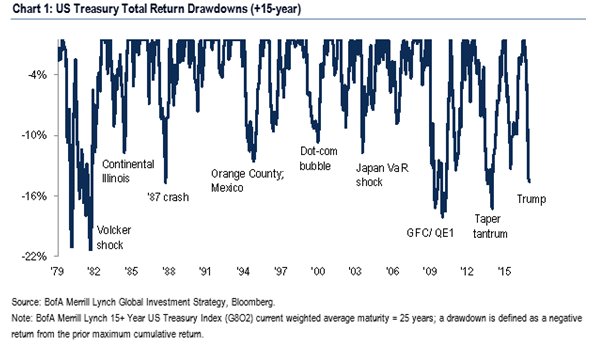

Indeed, the sell-off in bonds appear to be overdone. Michael Hartnett at BAML demonstrated that the drawdown in UST prices are at levels where past major bottoms have occurred.

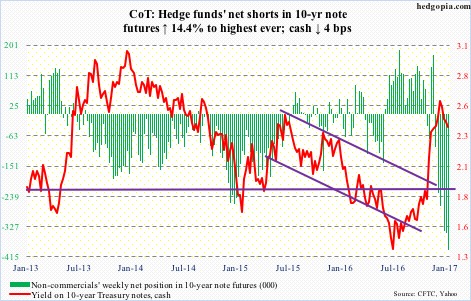

This chart from Hedgopia shows that even as 10-year yields have started to retreat, large speculator short positions continue to rise.

These conditions all suggest bond prices are poised for a powerful counter-trend rally for the next couple of months. From a cross-asset perspective, it also points to softer stock prices ahead.

There is an important caveat to this forecast. This scenario of near-term equity weakness and longer term strength falls apart if unexpected events, such as a trade war or even a shooting war, were to occur.

The week ahead

Looking to the week ahead, I expect volatility to rise as the market becomes subject to the event risk from Q4 earnings season. As well, Inauguration Day is Friday and who knows what kinds of fireworks and new initiatives will be announced.

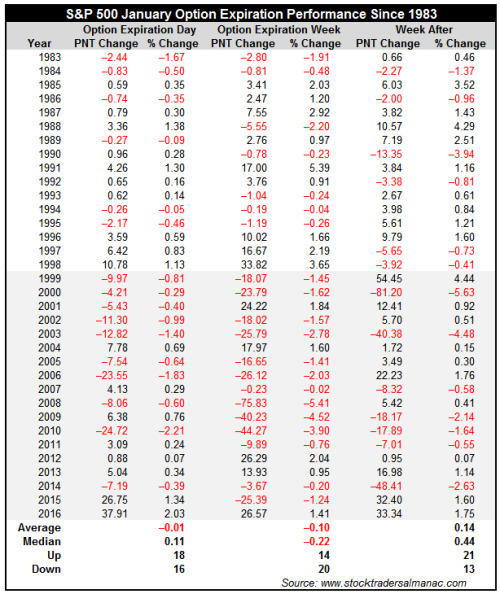

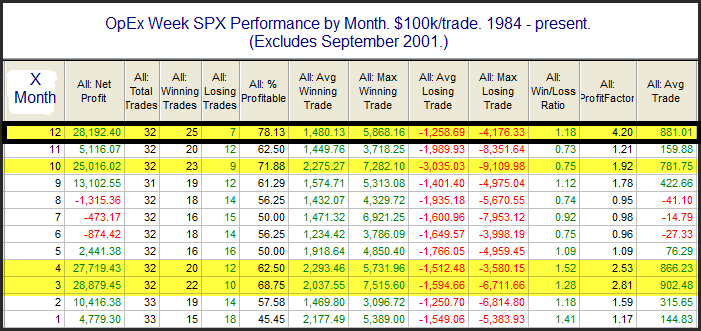

Next week is also option expiry week. Jeff Hirsch at Almanac Trader observed that returns during January OpEx week tends to be a mixed bag and does not show the usual bullish seasonal bias of OpEx weeks.

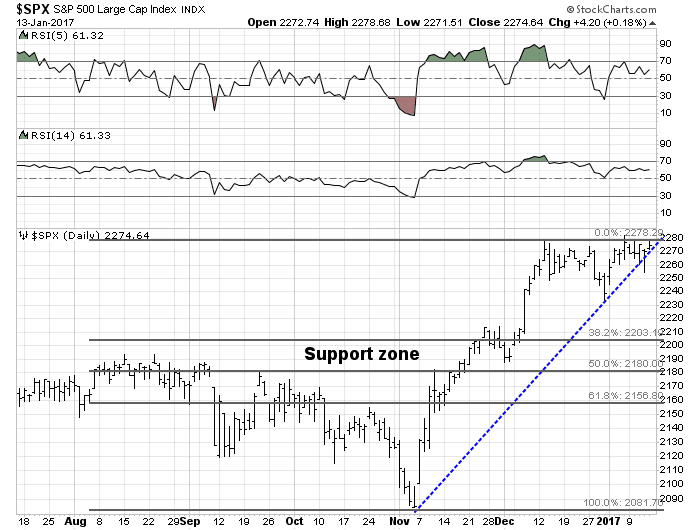

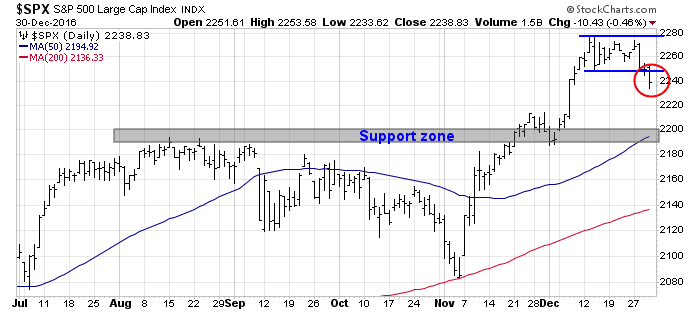

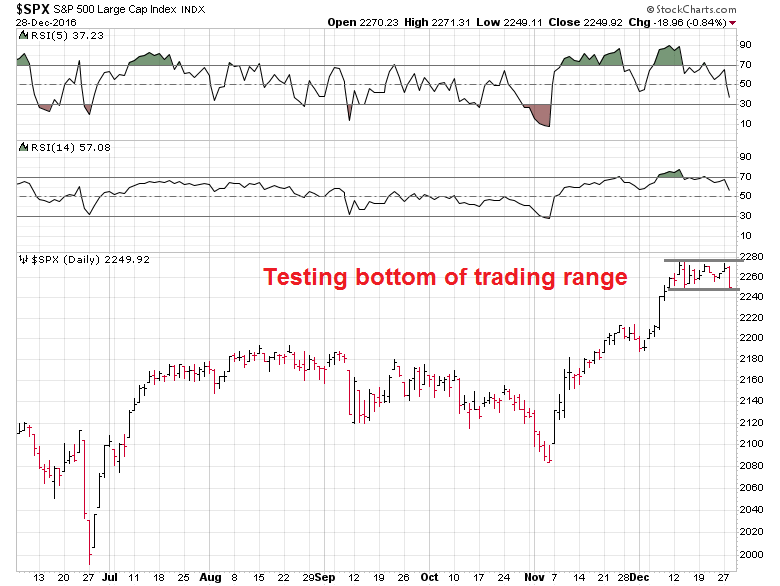

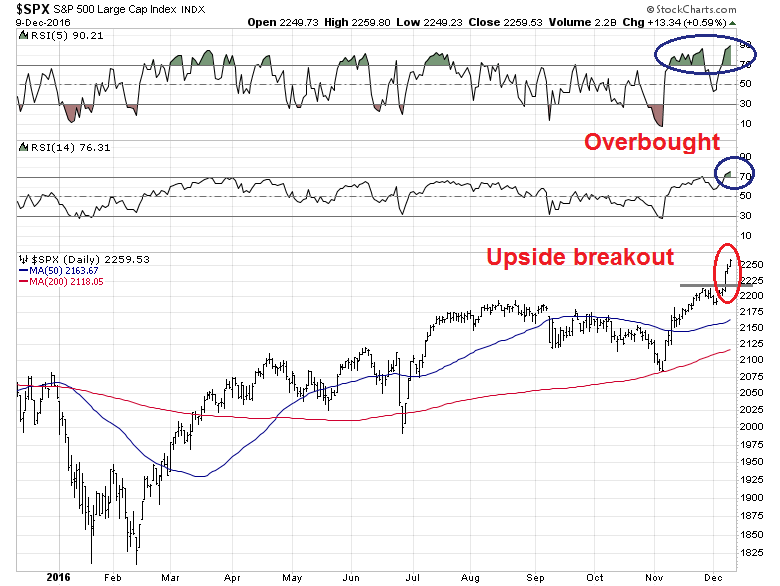

The SPX has spent several weeks in a narrow range and it is testing a key uptrend line. For the reasons I outlined, I expect that the upside potential to be limited. Should the uptrend get violated, support exists at the 2180-2200 zone, which is roughly the level where the index staged its upside breakout to all-time highs.

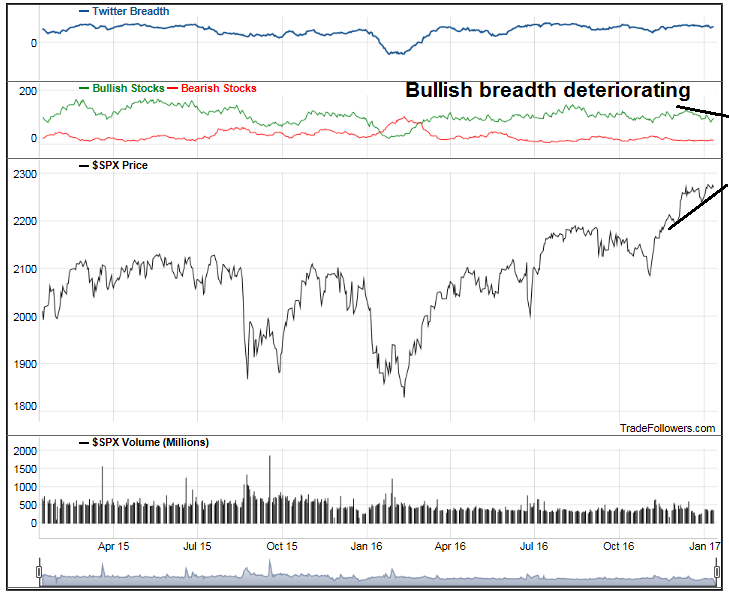

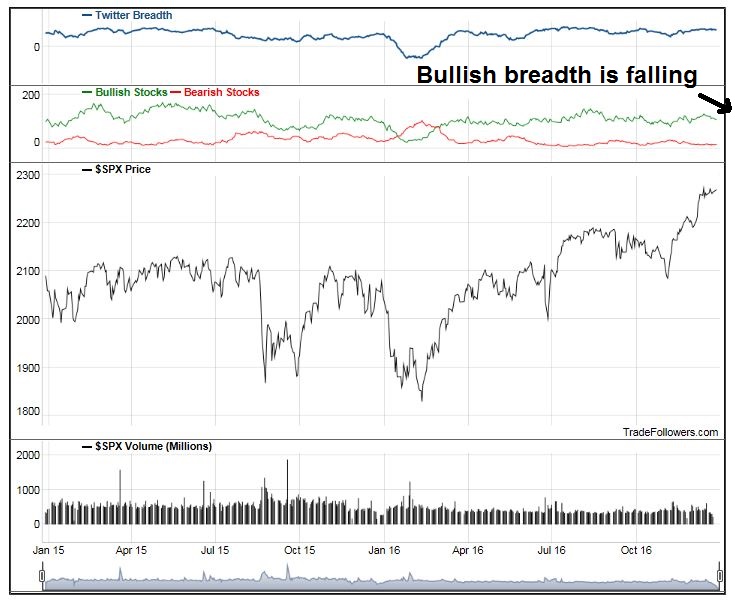

Market internals also point to a bearish resolution of the sideways consolidation. Analysis from Trade Followers shows a negative divergence as bullish Twitter breadth has been deteriorating even as the market has rallied.

My inner investor remains constructive on stocks. My inner trade has taken a small short position in the SPX.

Mid-week market comment: Arthur Hill at stockcharts recently observed that the Russell 2000 was in a tight consolidation range, which is characterized by a narrowing Bollinger Band. Such conditions tend to resolve themselves with volatility expansions which represent breakouts from the trading range.

His remarks about the Russell 2000 could also be applicable to the current conditions of the SPX as well. The key question is which direction will the breakout occur?

Clues from inter-market analysis

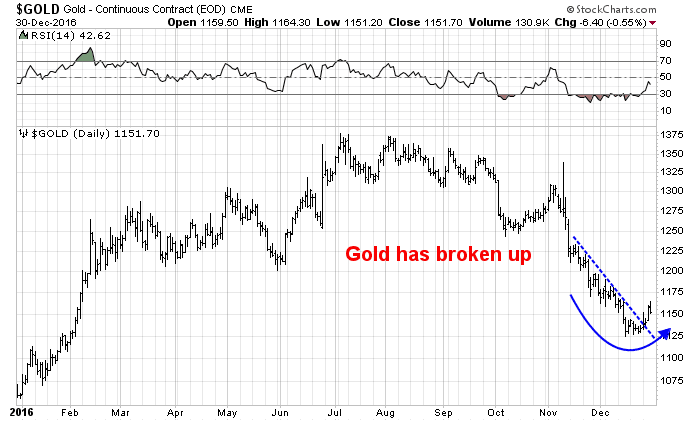

We can get some clues from market internals and the performance of other asset classes. Kevin Muir, writing at The Macro Tourist, pointed out that the “Trump trade” of long Russell 2000 and US Dollar, short gold and bonds has started to roll over after a huge rally since the election. These conditions suggest an environment of falling risk appetite.

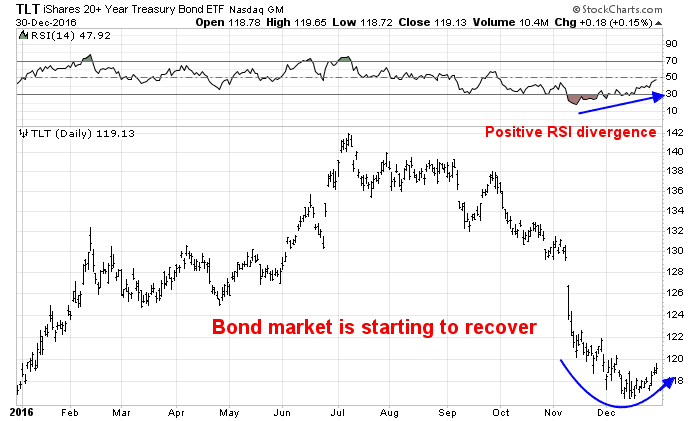

Indeed, the chart below of long Treasury prices shows that the 20+ year Treasury ETF (TLT) has started to turn up after experiencing a positive RSI divergence.

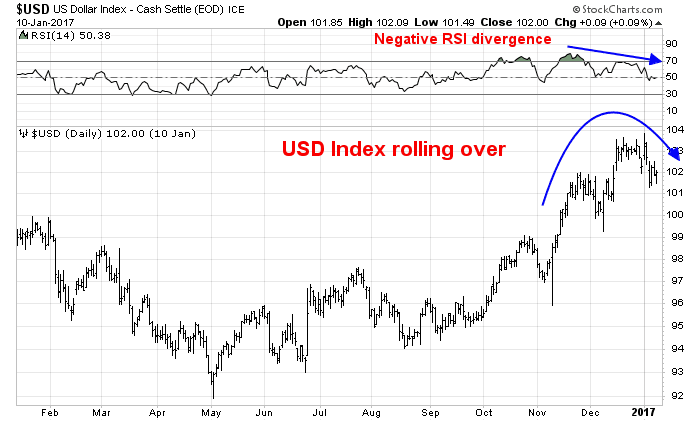

The chart of the USD Index is also telling a similar story. In this case, the USD Index is starting to roll over.

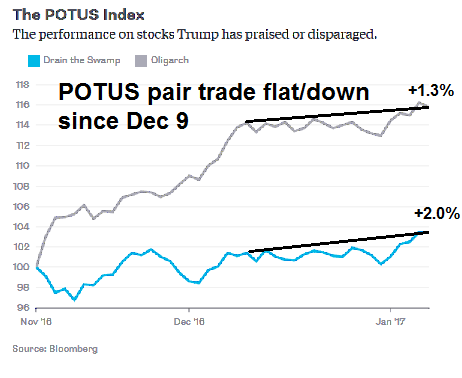

Independent of Muir’s analysis, Barry Ritholz constructed a POTUS Index, which consists of a basket of shares of companies that Trump has praised (grey line) and a basket of shares of companies that Trump has disparaged (blue line). As the chart below shows, this pair trade has been flat to down for the past month, which is indicative that the euphoria over the Trump election is fading (annotations are mine).

Despite these headwinds, stock prices have been surprising resilient. How will the Trump transition team deal with the challenges in the weeks ahead?

A test for the market and the Trump team

Early in the week, CNBC reported that the Trump team’s strategy ahead of the confirmation hearings scheduled this week was to “flood the headlines so that no bad news gets through”. The “bad news” was presumably any negative confirmation hearings headlines for the numerous nominees, such as Jeff Sessions, for Attorney General, John Kelly, for Homeland Security, Rex Tillerson, for Secretary of State, Betsy DeVos, for Education, and so on.

But the Trump team has a different strategy this week: They’re going to make a lot of news. So much, in fact, that the bet is no one piece of bad news will break through the media clutter. It’s all about safety in numbers.

That’s why you’ll see a wave of confirmation hearings all scheduled for the same day on Wednesday — even as Donald Trump himself provides cover with a long-awaited news conference in midtown Manhattan on the same day. The newser is bound to generate a wave of tweets, blog posts, cable TV hits and newspaper headlines that Republicans hope will wash over any poor performances by Trump’s nominees on Capitol Hill. The idea is to flood the zone.

Unfortunately, the Trump transition team did not count on the news about how Russian intelligence’s possession compromising material on Donald Trump caused the Trump advisers worked with Russian agents (see WSJ article and report from the Guardian). I’ll spare you the salacious details of the story, which have were seen by by various news organizations but not published because the details could not be confirmed.

The lurid details of how Trump may have been compromised should be of only minor concern to the markets. What really matters to investors is whether this story has the potential to distract and hamper the incoming administration’s ability to pass its package of fiscal programs.

In other words, will the tax cuts get delayed because the Trump team has to face Congressional investigations about Russian influence? That’s the first test for the Trump team, and for market psychology in the days and weeks ahead.

I had been meaning to write about the December Jobs Report, which was released last Friday, but I hadn’t gotten around to it. The report had elements of both good news and bad news.

The good news is the December report showed a solid market. True, the headline Non-Farm Payroll figure missed market expectations, but November was revised upwards, and the positive revision in November was bigger than the December miss.

In conjunction with the December Jobs Report, the Council of Economic Advisers released a report indicating that the American economy had added more jobs than other advanced economies in the last eight years (via Business Insider).

Notwithstanding the political victory lap nature of the CEA`s report, the December Jobs Report should keep the Fed on track with its expectations of three rate hikes in 2017.

Here is the bad news. There are worrisome signs that the economy is starting to overheat. The combination of Fed actions on interest rates and wage pressures on operating margins are likely to be unfriendly to the stock market. Unless the Trump administration comes through on their promised tax cuts in the near future, upside for equity prices will be limited in 2017.

The return of inflation

It was a solid jobs report. One of the more concerning features of the report was the return of wage pressures. YoY growth in average hourly earnings (AHE) rose to a new high for this economic cycle at 2.9%, which is well above the Fed’s 2% inflation target.

The surge in wage pressures is no surprise to the markets. The bond market’s inflationary expectations have been steadily rising for the last couple of months.

The reflationary trend has not just been isolated to American shores. Frederik Ducrozet constructed a global PMI price pressure index – and it has been surging.

These conditions give the Fed cover to stay on their path of interest rate normalization. Fed watcher Tim Duy analyzed the report and he believes that the risks to the growth outlook are weighted to the upside:

A solid report largely consistent with expectations among monetary policymakers. Hence it should have little impact on interest rate forecasts for the coming year. But watch out for upside risks to the outlook; the economy gained some traction in the final months of 2016. It is reasonable to believe that traction will hold in 2017.

Here comes margin pressure!

It’s not just the Fed that equity investors have to worry about. As the economy moves towards full employment, the upward pressure on wages from the labor shortage is likely to start to compress corporate operating margins. Variant Perception observed that rising real unit labor costs (note inverted right scale) tend to lead corporate profits by about two quarters.

In the absence of other factors, such as the Trump tax cuts, earnings growth is likely to come under pressure. For now, Factset reports that the Street has jumped on the global reflation theme and forward EPS is rising. In fact, the pace of downward earnings guidance has been lower than usual.

The risk of a negative surprise from falling operating margins should rise should labor market conditions stay tight.

The risk of a policy error

Even as the Fed prepares to raise rates, there is a risk that the Fed may mis-read the economy over-tighten a maturing expansion into recession. An area of concern is the loss of momentum in NFP growth. In the past, the deceleration of YoY NFP growth to 1.5% has been an ominous sign for both the economy and the stock market.

The evolution of temporary employment is telling a similar story. Temporary employment edged down in December. While the decline may be a data blip, temp jobs has led labor market growth in the last two cycles.

Indeed, New Deal democrat, who monitors high frequency economic releases, is starting to worry about weakness in his long leading indicators, though the short leading indicators and coincidental indicators remain healthy.

The interest rate components of the long leading indicators improved enough in the last two weeks to score neutral. The yield curve and money supply as well as real estate loans remain positive. The big news, however, is that both purchase and refinance mortgage applications have now turned negative.

Short leading indicators, including stock prices, jobless claims, industrial commodities, the regional Fed new orders indexes, spreads, and temp staffing are all positive. Oil and gas prices, and the US$ are neutral. Gas usage turned neutral.

The coincident indicators remain mixed. Steel, consumer spending, and tax withholding are positive, and rail mildly so. The BDI is neutral. The Harpex shipping index, the TED spread and LIBOR remain negative.

Seasonality will continue for one more week to be a huge factor in the volatility of the data. This week I am particularly discounting the strong staffing number. That being said, the shorter term 6 month forecast remains strongly positive (barring a trade war). The 12+ forecast is murkier now with mortgage applications finally turning negative. How long the post-Brexit strength in the monthly housing numbers continues will be important to watch.

If the Fed were to raise rates three, or maybe even four times, this year, it risks committing a policy error by looking in the rear view mirror of inflationary pressures and tightening just as the economy rolls over.

All eyes on the Trump administration

In short, market expectations for the Trump administration’s policies are high, even though Trump hasn’t even taken office. The bull case for equities rests on a combination of global reflation, Trump tax cuts, and deregulation. The bear case is based on the risks of a trade war (see How Trump/Navarro could spark a market crash), a hawkish Federal Reserve, and wage pressures on corporate margins.

David Kostin of Goldman Sachs (via Josh Brown) quantified the effects of these factors on earnings in the chart below, though he did not take into account the effects of high wage rates. As well, rising interest rates have a relatively minimal effect on earnings, but affect stock prices through changes in the P/E ratio. As the chart shows, the effects of tax policy is significantly higher than most of the other factors (annotations in red are mine).

In other words, Trump better come through on those tax cuts, or the stock market will see a very rough 2017.

Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Model is an asset allocation model which applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. In essence, it seeks to answer the question, “Is the trend in the global economy expansion (bullish) or contraction (bearish)?”

My inner trader uses the trading component of the Trend Model to look for changes in direction of the main Trend Model signal. A bullish Trend Model signal that gets less bullish is a trading “sell” signal. Conversely, a bearish Trend Model signal that gets less bearish is a trading “buy” signal. The history of actual out-of-sample (not backtested) signals of the trading model are shown by the arrows in the chart below. Past trading of the trading model has shown turnover rates of about 200% per month.

The latest signals of each model are as follows:

Ultimate market timing model: Buy equities

Trend Model signal: Risk-on

Trading model: Bearish

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers will also receive email notices of any changes in my trading portfolio.

How the market could crash

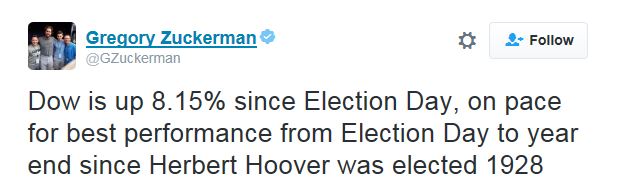

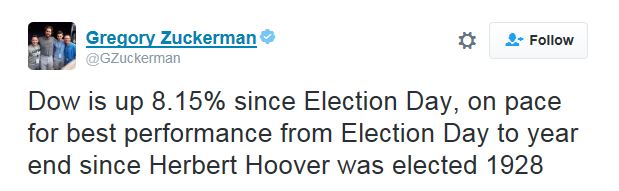

At the end of 2016, WSJ reporter Greg Zuckerman made a tweet with ominous implications. Hmm…what happened in 1929?

Here is how a market crash can happen. Donald Trump’s appointment of Peter Navarro, the author of Death by China, represents the biggest source of policy tail-risk for the capital markets. Bashing China may be satisfying for Trump supporters, but the Chinese economy is increasingly fragile (see How much ‘runway’ does China have left?). Impose tariffs on Chinese goods, and you risk a Chinese economic slowdown that drags the world into a synchronized global recession.

While a crash is most definitely not my base case, the scenario of collapsing trade flows from a Chinese hard landing would first tank the Asian economies, followed by Europe, whose banking system are still over-levered and have not fully recovered from the Great Financial Crisis. Under such circumstances, an equity bear market would be a 100% certainty, and a market crash would be within the realm of possibility.

It’s hard to estimate the actual probability of a US induced China hard landing scenario. However, we should get better clarity as the Trump team moves into the West Wing of the White House in the coming weeks. In addition, President-Elect Trump may give us some clues on trade when he holds his press conference on Wednesday.

Fragile China

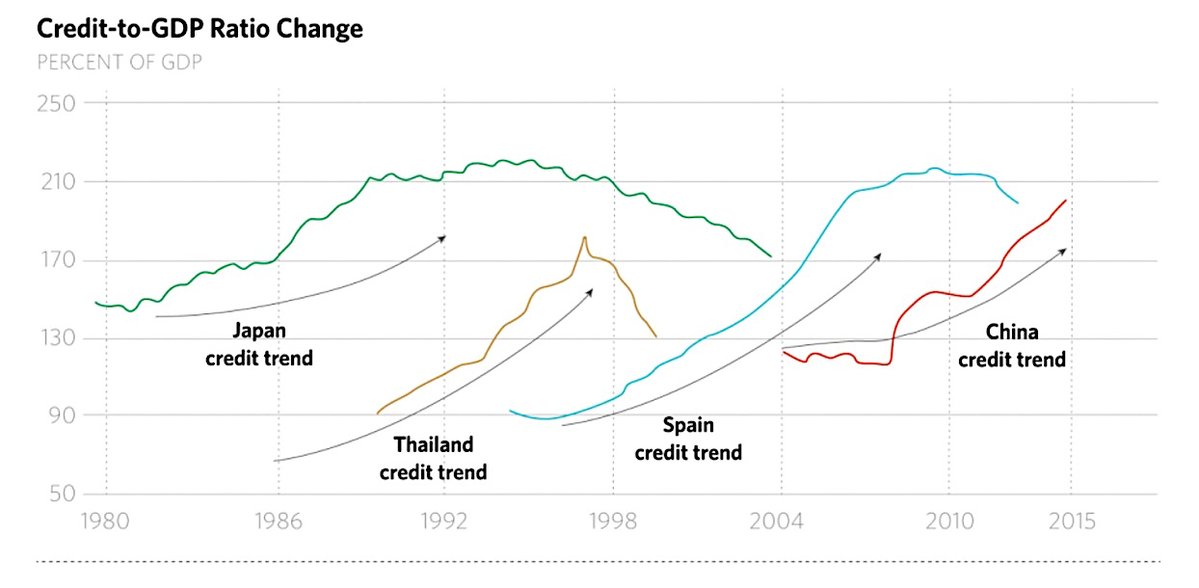

The chart below (via Stratfor) shows the trajectory of credit to GDP of countries that have experienced a strong rise in debt. It is only a matter of time that China’s debt capacity hits the wall, just like every country that has experienced a period of hyper-growth in the 20th and 21st Century.

I wrote a post last summer that highlighted analysis from China watcher Michael Pettis. Pettis made the case that China had a maximum of 2-3 years to resolve its growing debt problem (see How much ‘runway’ does China have left?). Fast forward to today, the time horizon is only 1-2 years.

Christopher Balding, writing in Bloomberg Views, explained the fragility of China’s financial system this way: