In the past few months, I have received a lot of feedback and criticism over my use of forward 12-month EPS estimates, such as the chart below that appeared in last weekend`s post (see Brexit panic: A gift from the market gods?). I would like to clarify why this form of analysis matters and this is a valuable technique to beat Wall Street analysts at their own Earnings Game.

Here is we know about Street estimates.

Earnings estimates do matter

Earnings do matter to markets. Expectations matter. If you don’t think that they don’t, just remember all the speculation, jockeying and positioning before and after the earnings reports of traders’ favorite stocks such as FANG and tell me otherwise.

Analysts are wrong

As shown by this chart from Yardeni Research, Street EPS estimates are notoriously inaccurate and overly optimistic. EPS estimates for any single fiscal year or quarter tend start high and they decline over time. In fact, you will find a huge gulf between aggregated bottom-up estimates and top-down estimates from Street strategists. It’s not unusual at all to find bottom-up estimates amounting to GDP growth + 10%, which is wildly optimistic.

So the next time someone (like Zero Hedge) tells you that earnings for any single fiscal quarter or year for stocks are falling, remember this chart. Earnings estimates have a natural tendency to fall over time because of excess optimism and declining estimates are not necessarily a bearish sign for the stock market.

As analysts’ projections become more realistic over time and they lower their earnings estimates, another force comes into play to raise the error rate. Corporate management plays games with the Street to lower expectations and so that companies can beat consensus estimates at announcement time. The latest Factset report shows that the average 5-year EPS beat rate for EPS is 67% and the average 5-year sales beat rate is 56%.

That’s why the sales beat rate is more important than the EPS beat rate these days.

Estimate revision = Fundamental momentum

The way to correct for Street estimation error is to monitor the direction of change in analyst estimates and this technique is known as estimate revision modeling. Technical analysts are familiar with the concept of price momentum. Estimate revision is a form of fundamental momentum.

There are several ways of calculating EPS estimate revision. One is to use a diffusion model by observing the number of upward revisions against downward revisions without regard to the magnitude of the change. Another wrinkle for the quantitative analyst is whether to focus on FY1 estimates or FY2 estimates. For example, if the fiscal year ends in December and we are analyzing estimates in October, FY1 estimates really amount to only Q4 estimates as the first three quarters are already known. In that case, what’s more important to the stock’s outlook, FY1 or FY2?

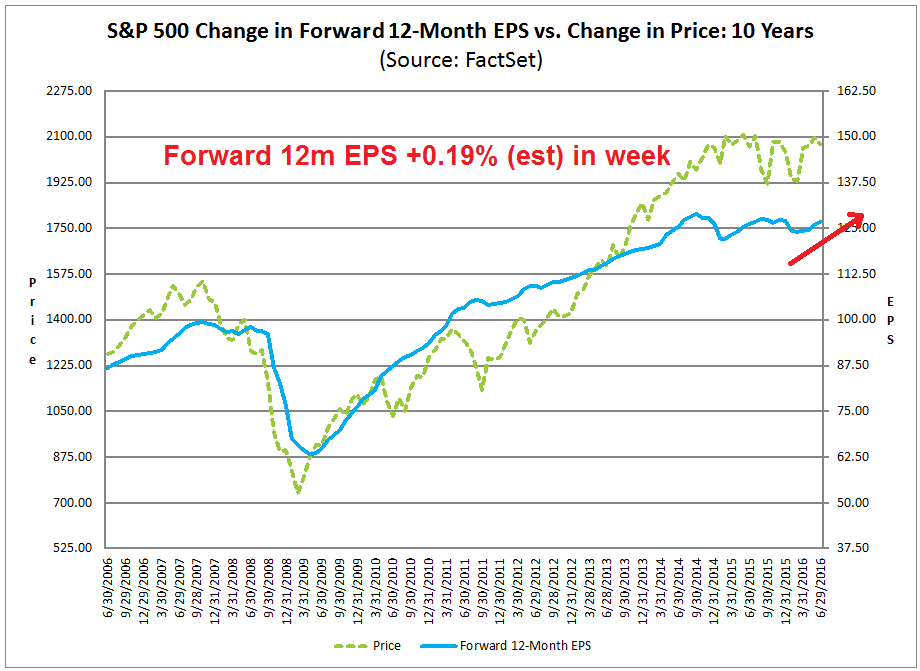

I have tested a number of different approaches to measure EPS expectations. The most stable method is to calculate a rolling forward 12-month EPS by blending FY1 and FY2 estimates together. This constant forward EPS technique corrects for the problem of overly optimistic estimation problem because the forward bias is constant.

By monitoring how forward EPS changes, we can observe changes in fundamental sales and earnings momentum. That’s because not all analysts change their estimates at the same time and not all investors, institutional in particular, respond to estimate changes at the same time. Different Street analysts publish reports on the same company at different times. If there is a shift in the underlying fundamentals of the business, EPS and sales estimates will see a similar shift as analysts jump on the bandwagon – and that bandwagon effect is a form of fundamental momentum in expectations.

Now compare and contrast the Yardeni chart above with my original Factset chart of forward EPS and price. The relationship between forward EPS and price is far more stable and less prone to estimation error. The chart shows that forward EPS is roughly coincidental or slightly lags price. In fact, price is the far more noisy data series and, if you believe in fundamentals haven’t changed, earnings can be a better guide to the long-term equity return outlook.

Modeling drawbacks

No model is perfect and there are a number of disadvantages to this approach.

First, estimate revisions are inherently noisy. If you monitor them on a daily or weekly basis, the changes appear to be microscopic – but that’s not a bug, it’s a feature. At an individual stock level, I have had some success with generating buy and sell signals stocks with extremes in estimate revisions as a way of spotting the rolling bandwagon that I mentioned before. This fundamental momentum effect has diminished somewhat since the advent of Rule FD as corporate management has become increasingly reluctant to speak to analysts between earnings announcements, but it can nevertheless be an effective stock picking technique. (Don’t ask me to generate lists of buys and sells based on this model as that level of company level data detail is not available to me.)

At an aggregate level, we can smooth out some of the noise by looking at trends. By observing how Street sentiment is changing towards the market and at sector levels, we can see whether sentiment is improving or deteriorating. As trends tend to be persistent, we can also profit from the trend, or bandwagon effect, from a top-down viewpoint.

Another drawback of using estimate revision is the Street is notoriously bad at turning points in the market. For that, I have tended to rely on other models based on macro-economic, technical and sentiment analysis to spot turning points.

Nothing is perfect, but applying an estimate revision analytical framework to forward 12-month EPS estimates remains a valuable tool for both bottom-up and top-down market analysis.

A fine post this one is.

How much do you think one should weigh the fact that GAAP earnings and revenues have been flat to slowly dropping for quite a few quarters, and that any increase in EPS is a function of stock buybacks reducing shares? Add in that much of the money to buy the shares is debt financed, and that to the extent it isn’t, the money used is consuming a significant percentage of corporate cash flows, suggesting that the next major change in stock buybacks will be towards down, not up.

Not that the market can’t go up for other reasons, but getting excited about EPS in a time period that looks like it will be seen in retrospect as a “peak buyback” era, seems not much different than paying a high multiple of a company’s earnings at a cyclical peak. Am I missing something? Thanks.

If you are looking at past reported sales and earnings, you are looking in the rearview mirror. The market is a forward discounting mechanism and what happened before is less relevant. Next 12-month EPS is a forward looking metric and the direction of the change is probably more useful for determining equity returns.

The buyback issue doesn’t seem to pose that much of a problem. See http://uk.businessinsider.com/how-companies-fund-share-buybacks-2015-11