Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “

Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post,

Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The

Trend Asset Allocation Model is an asset allocation model that applies trend-following principles based on the inputs of global stock and commodity prices. This model has a shorter time horizon and tends to turn over about 4-6 times a year. The performance and full details of a model portfolio based on the out-of-sample signals of the Trend Model can be found

here.

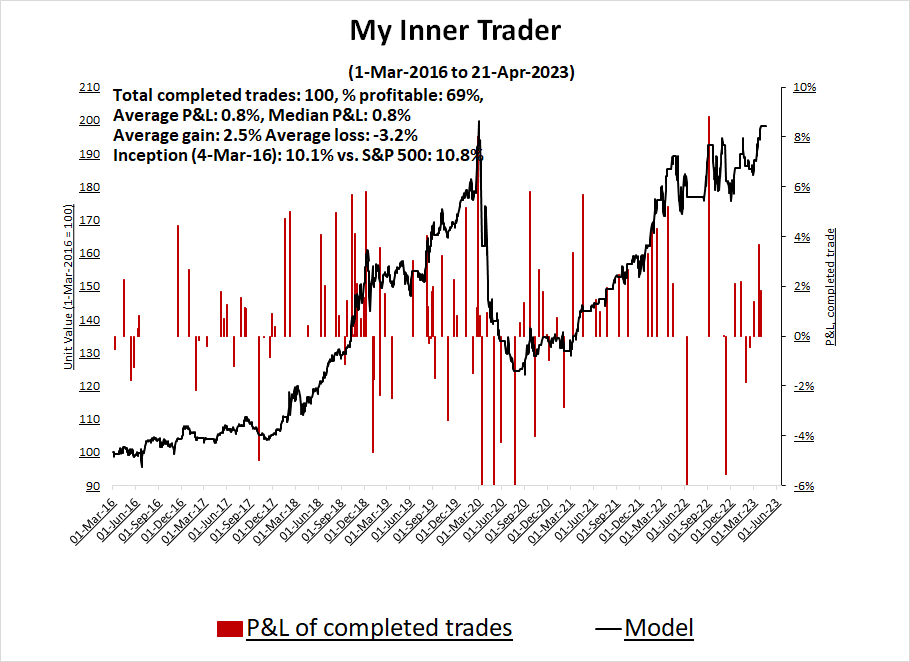

My inner trader uses a

trading model, which is a blend of price momentum (is the Trend Model becoming more bullish, or bearish?) and overbought/oversold extremes (don’t buy if the trend is overbought, and vice versa). Subscribers receive real-time alerts of model changes, and a hypothetical trading record of the email alerts is updated weekly

here. The hypothetical trading record of the trading model of the real-time alerts that began in March 2016 is shown below.

The latest signals of each model are as follows:

- Ultimate market timing model: Sell equities

- Trend Model signal: Neutral

- Trading model: Bullish

Update schedule: I generally update model readings on my site on weekends. I am also on Twitter at @humblestudent and on Mastodon at @humblestudent@toot.community. Subscribers receive real-time alerts of trading model changes, and a hypothetical trading record of those email alerts is shown here.

Subscribers can access the latest signal in real time here.

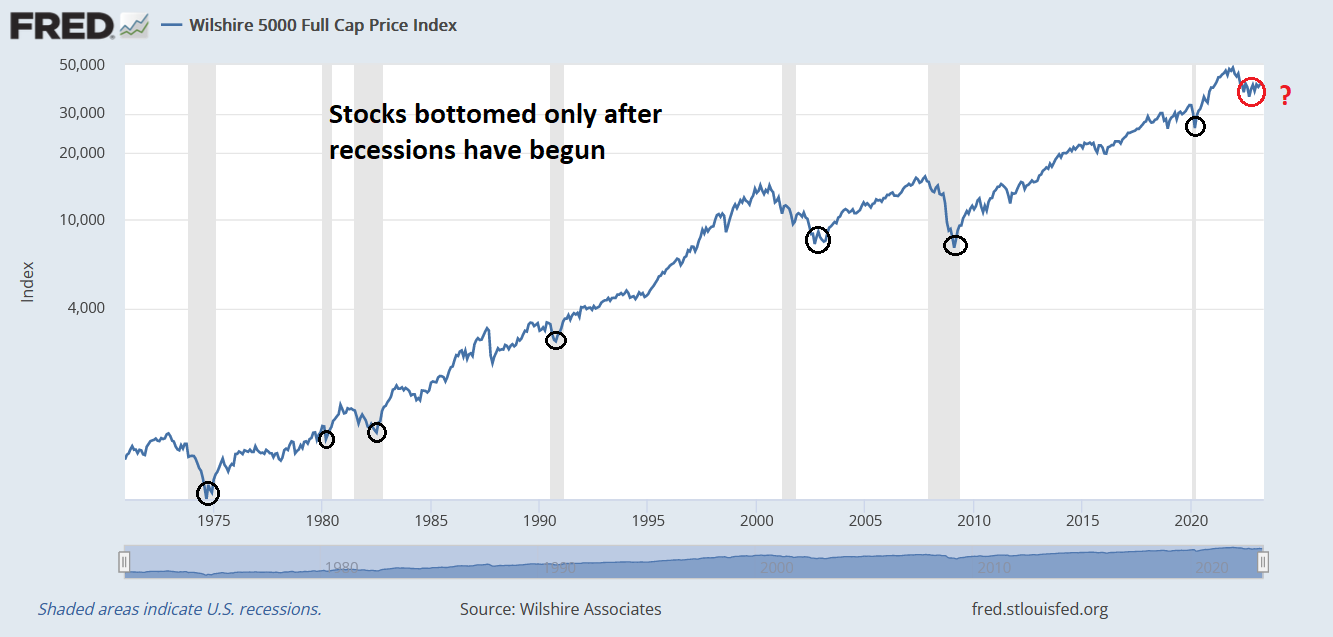

A tight trading range

The S&P 500 has been mired in two trading ranges for several weeks. The smaller range is defined by 4050–4180 (grey zone), and the larger one is defined by 3800–4180. Neither the bulls nor the bears have been able to break through.

I outlined the intermediate-term bearish market structure exhibited by the market last week and U stand by those remarks (see What market structure tells us about where we are in the cycle). While this is not my base case, I am starting to warm to the scenario of an upside breakout to a blow-off top, followed by a market collapse soon afterwards. As they say, don’t short a dull market.

Reasons to be bullish

The most compelling reason to be bullish is the behavior of corporate insiders. This group of “smart investors” has been timely at spotting tactical market bottoms in the past year, and net insider buying surprisingly appeared last week.

I interpret this to mean that, barring an unexpected negative surprise, downside risk in stocks is limited and risk/reward is skewed to the upside.

What’s more the Citi Panic/Euphoria Model is back in the panic zone. While this model is not useful for short-term trades, it nevertheless highlights the burden that the bears face.

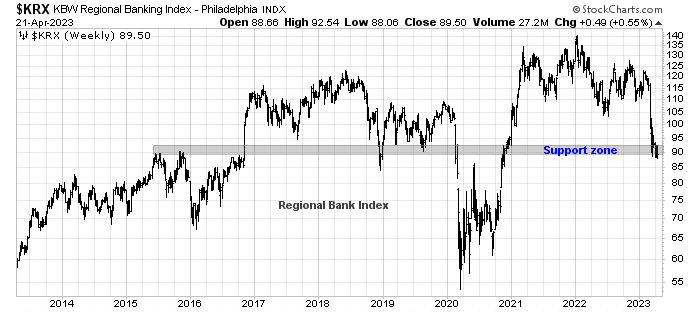

In addition, market fears of a regional banking meltdown is spiking. While there is no apparent fundamental resolution of those fears on the horizon, the tactical good news is the KRW Regional Banking Index is falling while exhibiting a positive RSI divergence, which is constructive.

Looking beneath the hood, seasonally adjusted deposits at small banks have stabilized after the Silicon Valley Bank debacle. The downward pressure on regional banking shares is fear based and not fundamentally driven.

The debt ceiling game of chicken

What could spark a buying stampede? How about a debt ceiling deal or a limited fallout from a Treasury default?

Washington politicians will undoubtedly posture for the cameras and reach a deal to raise the debt ceiling just before X-date, or the projected day that the U.S. government runs out of money. Nate Silver, writing in the

NY Times on January 30, 2023, revealed that Republican voters care more about cultural issues like Dr. Seuss than fiscal matters like the budget, which is an indirect indication of how much political capital Republican lawmakers are willing to expend in the debt ceiling fight:

In early March 2021, a Morning Consult/Politico poll found that nearly half of Republicans said they had heard “a lot” about the news that the Seuss estate had decided to stop selling six books it deemed had offensive imagery. That was a bigger share than had heard a lot about the $1.9 trillion dollar stimulus package enacted into law that very week.

The result was a vivid marker of how much the Republican Party had changed over the Trump era. Just a dozen years earlier, a much smaller stimulus package sparked the Tea Party movement that helped propel Republicans to a landslide victory in the 2010 midterm election. But in 2021 the right was so consumed by the purported cancellation of Dr. Seuss that it could barely muster any outrage about big government spending.

Both the Republicans and the White House are still talking and staff is working out the details of different proposals. In all likelihood, we will see a last-minute deal.

Unspeakable default?

What if there is no deal and the U.S. government defaults?

I am indebted to former New York Fed trader Joseph Wang who writes under the name, “the Fed Guy”.

Wang published the details of a contingency plan hatched in 2021 by the Fed and Treasury in case of a debt-ceiling default. The plan was pieced together from past

FOMC transcripts and

Congressional subpoenas. Despite statements that software systems are not set up to prioritize payments to different parties, Wang concluded that Treasury is prepared to prioritize:

Treasury will make noises to scare Congress into action, but it understands the importance of avoiding default and will prioritize debt payments once it runs out of headroom. Prioritization can support the Treasury market indefinitely, and even if that support is withdrawn the Fed stands ready to act as dealer of last resort.

Wang explained:

When Treasury reaches the ceiling limit and also runs out of accounting tricks, then it will not have enough money to meet all its obligations. But it will still have enough money to meet some of the obligations. Prior Administrations have claimed technical impossibility or illegality in prioritizing payments, but that was largely to exert political pressure on Congress. A 2016 Congressional report (h/t @AnalystDC) reveals the Obama Administration was working with the NY Fed to prioritize debt payments and social security payments during the 2013 debt ceiling episode. This is essentially a compromise that maintains pressure on Congress while limiting the potentially significant financial and humanitarian costs. The same policy choice will very likely be made this time around.

Payment prioritization would also raise the level of pressure on lawmakers without significantly denting the economy in the short term.

The biggest losers of prioritization are those who usually receive large government expenditures: the medical and defense industry. Both of which are well funded industries that can handle a liquidity squeeze (and send lobbyists to hasten Congressional action).

Some analysts have raised the risk that financial clearinghouses such as futures exchanges who ask for the deposit of T-Bills as margin collateral may struggle with holding defaulted Treasury securities. Consequently, they may raise margin requirements and spark a credit crunch cascade. Wang has an answer for that eventuality:

The Fed has the tools and motivation to backstop any Treasury market dislocation. When the Treasury market liquidity disappeared last March, the Fed cranked up the printers and bought $1 trillion of Treasuries over just 3 weeks. In the same way, FOMC transcripts show the Fed is prepared to 1) provide liquidity against defaulted Treasuries in its repo operations, 2) offer to swap out defaulted Treasuries for “clean” Treasuries with its securities lending program, and 3) and fire up the printers to purchase defaulted Treasuries outright. At the end of the day the Treasury market will be strongly supported as it was last March. The Fed will be the Treasury dealer of last resort.

Do you feel better now? The Fed and Treasury have the market’s back. A debt ceiling breach won’t be a catastrophe.

To be sure, these measures by Treasury and the Fed are the technical equivalent of going nuclear, which institutions would like to avoid. It may not come to that, even if there is no last-minute deal.

There are other steps the Administration could take. For example, President Joe Biden revealed that there has been some tentative consideration of invoking the 14th Amendment, even without a debt ceiling hike. Section 4 of the 14th Amendment states: “The validity of the public debt of the United States, authorized by law, including debts incurred for payment of pensions and bounties for services in suppressing insurrection or rebellion, shall not be questioned. But neither the United States nor any State shall assume or pay any debt or obligation incurred in aid of insurrection or rebellion against the United States, or any claim for the loss or emancipation of any slave; but all such debts, obligations and claims shall be held illegal and void.” In other words, any law, such as debt ceiling legislation, is unconstitutional because it can force a government default.

There are other gimmicky backstops, such as legislation that allows the Treasury to mint a$1-trillion platinum coin and deposit it at the Fed.

Reuters reported that “U.S. equity funds faced outflows worth $5.7 billion, which was their seventh consecutive week of outflows” and the sales were attributable to jitters over the debt ceiling. The stock market has been trading in a tight range for the last seven weeks. If that’s the worst that debt ceiling fears can do to stock prices, what happens if both sides come to an agreement?

Debt ceiling aftermath

After all the growing angst that’s in the market over the debt ceiling, any development that sidesteps all the worst effects of going over the debt ceiling cliff, such as a last-minute deal, constitutional workaround, or Fed and Treasury contingency plans to stabilize markets, would be welcome by the markets with a risk-on FOMO buying stampede. That’s how a blow-off top might happen.

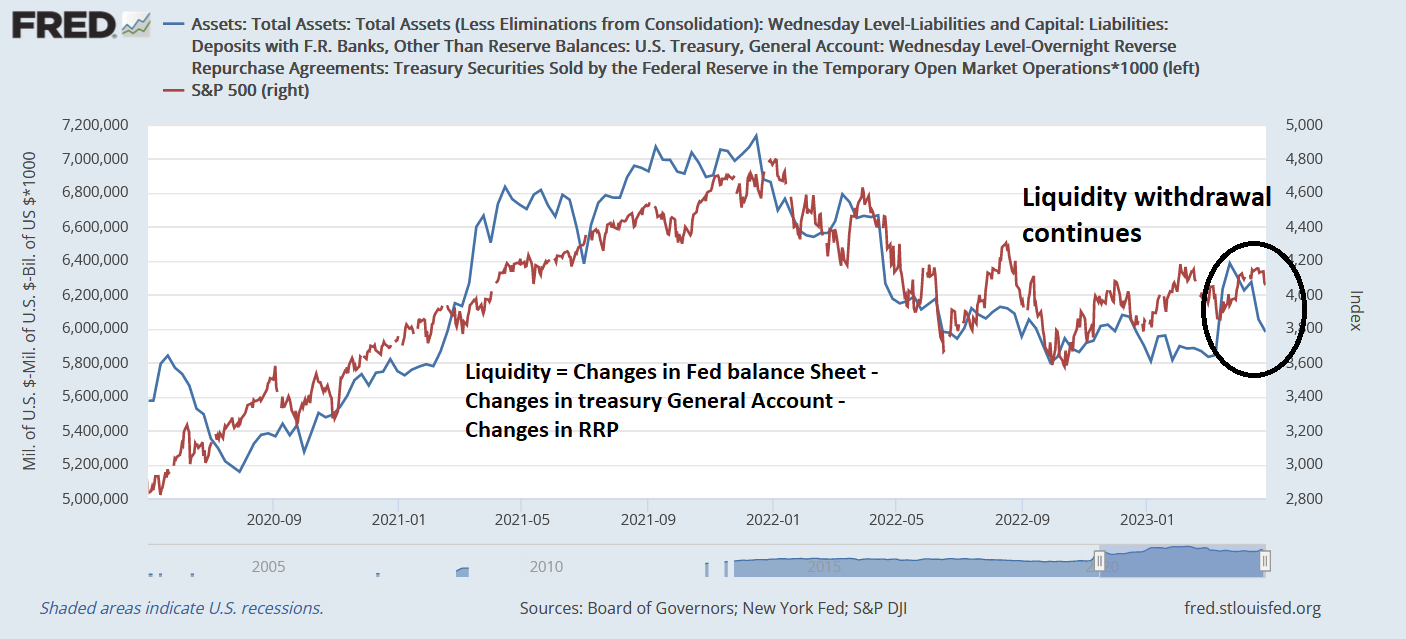

What would happen next? I already outlined the bearish nature of market structure last week. In addition, raising the debt ceiling would have a perverse effect of draining liquidity from the financial system, which would be bearish for risk assets. When it became evident that the ceiling was about to be breached, Treasury resorted to extraordinary measures and accounting tricks to pay the bills and keep government running. Accounting tricks include deferring the payment of funds into government employee pension plans and drawing down the Treasury General Account (TGA), which is the equivalent of the “bank account” that Treasury has at the Fed. When the government disburses funds from TGA, it has the effect of injecting funds into the financial system, which increases liquidity. When the debt ceiling is raised, TGA balances are raised and the process goes into reverse. Liquidity is drained, which creates headwinds for the price of risk assets.

If the stock market were to melt-up, the loss of liquidity could be the catalyst for a meltdown.

In conclusion, I continue to believe the path of least resistance for stock prices in the intermediate term is down. However, the odds of an upside breakout and a blow-off top are rising, followed by a collapse in the stock market. I would estimate the chances of the breakout and melt-up scenario at about one in three.

My inner trader remains tactically long the S&P 500. The usual disclaimers apply to my trading positions:

I would like to add a note about the disclosure of my trading account after discussions with some readers. I disclose the direction of my trading exposure to indicate any potential conflicts. I use leveraged ETFs because the account is a tax-deferred account that does not allow margin trading and my degree of exposure is a relatively small percentage of the account. It emphatically does not represent an endorsement that you should follow my use of these products to trade their own account. Leverage ETFs have a known decay problem that don’t make the suitable for anything other than short-term trading. You have to determine and be responsible for your own risk tolerance and pain thresholds. Your own mileage will and should vary.

Disclosure: Long SPXL