On Valentine’s Day, the European Central Bank tweeted a poem to underscore its commitment to fighting inflation.

The ECB tweet is also indicative of the tight monetary policy undertaken by most major central banks. Only two central banks, the BoJ and the PBoC, are meaningful suppliers of global liquidity. The rest are raising interest rates and engaged in quantitative tightening. While the Fed may be on the verge of a pause, last week’s hot PPI report and slightly stronger than expected CPI print has raised doubts about a dovish pivot.

Inflation is becoming a threat again.

Interpreting the US inflation reports

US inflation figures came in hotter than expected. The monthly changes in headline and core CPI were in line with expectations, but annual changes of headline and core CPI were both 0.1% above market consensus. By contrast, monthly core PPI came in at 0.5%, which was well ahead of the 0.3% forecast, and December was revised upward from 0.1% to 0.3%.

Notwithstanding the stronger than expected PPI report, the longer term trend shows that headline CPI retreated from over 8% to 5-6%. While the deceleration is constructive, both headline (red bars) and core (blue bars) are stabilizing at those levels. It’s less clear how inflation readings can fall to 2% without further significant monetary tightening.

The San Francisco Fed undertook a study of cyclical and acyclical components of PCE, the Fed’s preferred inflation metric. While it’s clear that acyclical inflation has fallen, largely because of the normalization of supply chain constraints, cyclical inflation is stubbornly high and rising.

The analysis of sticky price and flexible price CPI tells the same story. Core flexible price CPI, which reflects the rise and fall of pandemic shock goods like used cars, have fallen dramatically. On the other hand, sticky price CPI is stuck at about the 6% level.

This begs the question of what happens if China reopens successfully and global demand surges. What happens to the inflation picture then?

The monetary policy response

In the wake of the January CPI report, Fed Funds futures began discounting a higher terminal rate and two consecutive quarter-point rate hikes, followed by easing in late 2023.

Will that level of monetary tightening be enough? The February FOMC statement committed to “a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time”. What does “sufficiently restrictive” mean? The February FOMC statement made it clear that the Fed is laser focused on the labor market and central to the “sufficiently restrictive” definition.

Despite the slowdown in growth, the labor market remains extremely tight, with the unemployment rate at a 50-year low, job vacancies still very high, and wage growth elevated. Job gains have been robust, with employment rising by an average of 247,000 jobs per month over the last three months. Although the pace of job gains has slowed over the course of the past year and nominal wage growth has shown some signs of easing, the labor market continues to be out of balance. Labor demand substantially exceeds the supply of available workers, and the labor force participation rate has changed little from a year ago.

Both Cleveland Fed President Loretta Mester and St. Louis Fed President James Bullard made the case for half-point rate hikes in speeches last week. Former Fed economist John Roberts analyzed what stronger growth and higher inflation could mean for the Fed’s Summary of Economic Projections, otherwise known as the “dot plot”.

While the main focus of the analysis is the ongoing strength in the economy, I also modify my December SEP matching exercise to take account of the incoming data on inflation, which suggest a somewhat more optimistic outlook than the FOMC assumed in December. As I discuss in more detail below, I raise the path for the federal funds rate by enough to ensure that inflation is close to the FOMC’s objective by 2025.

He concluded that unemployment rises at the end of 2023 to 4.2% (vs. SEP median projection of 4.6%), core PCE at 3.5% (SEP median projection 3.1%), and the Fed Funds rate rises to 5.6% by Q3, which is higher than market terminal rate expectations.

Roberts’ study raises two key questions:

- In light of the Fed’s focus on the labor market, does an unemployment rate of 4.2%, which is 0.4% lower than the December SEP projection, satisfy the “sufficiently restrictive” criteria?

- How will the Fed respond to the global inflationary effects of higher China demand in the case of a successful reopening?

In short, it’s relatively easy to get inflation from 6% to 4%. Getting it down to the 2% target could be much tougher than anyone expects. The Congressional Budget Office is now projecting that inflation won’t reach 2% until 2027.

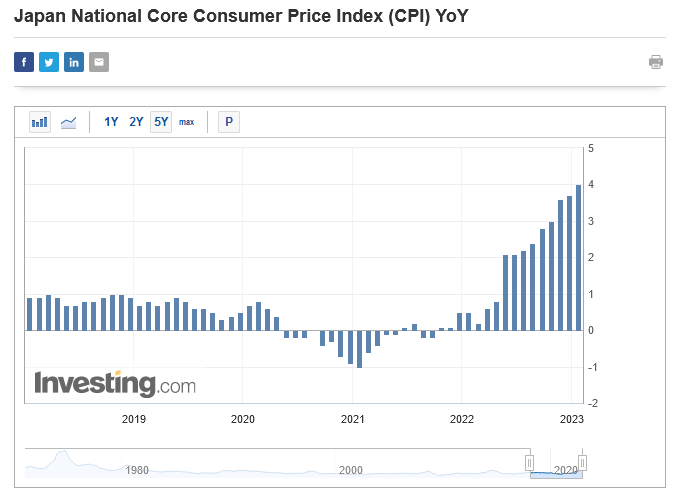

A seismic shift at the BoJ?

Across the Pacific in Japan, a seismic shift may be occurring at the BoJ. After decades of fiscal and monetary intervention, core CPI began rising in mid-2022 and has reached the 4% level.

The BoJ has been the lone holdout among G7 central banks by staying dovish while others have become hawkish. Rising inflation has begun to pressure the JPY exchange rate and the its bond market. The BoJ already gave in to market pressures and widened its yield curve control (YCC) level for the 10-year JGB from 0.25% to 0.50%.

Looking ahead, current BoJ head Kuroda is stepping down after two consecutive 5-year terms in which he authored an unprecedented easy credit and monetary policy to boost inflation. Kuroda is expected to be replaced by Kazuo Ueda, an academic whose views are largely not known to the public.

The current market consensus is the choice of Ueda by Prime Minister Kishida as a way to differentiate the government’s policies from the “Abenomics” strategy of near-zero interest rates and massive asset purchases by the central bank meant to combat stagnation. At best, Ueda will continue Kuroda’s easy monetary policy. The more likely path is a minor hawkish pivot in which the BoJ gradually pulls back from its YCC and eventually raises interest rates.

The BoJ and the People’s Bank of China (PBoC) are the two major central banks that are main suppliers of liquidity to the global financial system. For some perspective, the magnitude of the BoJ’s QE program is overwhelming the Fed’s QT program. The BoJ will likely reverse its ultra-loose credit policies in the next few years, creating headwinds for global risk appetite. In addition, the near-term path of US monetary policy is likely to be more hawkish than market expectations. The factors all serve to create headwinds for bond prices and risky assets in the medium term. Unless the growth outlook significantly improves, this will be a bearish environment for stock prices.

My base case scenario calls for a bullish recovery in H1 2023 for stocks, based on the cyclical effects of China reopening, followed by a dip in H2, triggered by a more hawkish monetary response to rising inflation (see The risk of transitory disinflation). The contrarian view is based on the Economist magazine cover indicator, which suggests that inflation will fall rapidly from here.

I can make loads of poems. “Roses are red, violets are blue, I don’t like the Fed, what about you?”

Barring some techno breakthroughs we have inflation in our future. Declining resources will cost more (barring free energy ), the USD will lose value compared to real things because there will be budgetary deficits until some seismic shift changes everything as we know it and trade balance will continue to be negative also until some sort of major change occurs.

In the shorter run, say less than 5 years, if we get a recession, a big fall in demand, china reopening etc etc, yeah we can easily have disinflation or deflation.

You know the Hemingway quote about bankruptcy? I have seen it many times, but never with an explanation, so I will give you mine. It’s a bit like a Minsky Moment. It’s when everyone who has been lending you money realizes you are broke.

So for the US, for decades we ran surpluses of trade, we were the greatest creditors, we manufactured stuff for the world. That shift in manufacturing really affected our trade balance, but we exported pollution to China.

Even if we onshore manufacturing via robotics, so will China and others, so it will boil down to a competition for resources.

Will we ever have politicians who will do the right thing and get kicked out of power? Will we elect politicians who promise us pain to do the right things? Will half the population receiving social security volunteer it back because they don’t really NEED it? Any yeses out there?

Is the plunge in TLT signaling us something? What would the effect of a commodities crisis be like for NIMBY USA? or NIMBY Europe.

You can’t print your way out of inflation.

So we might get to 2% transiently.

It is almost guaranteed that CPI and PPI numbers this year will be stochastic, owing to US structural problems and external factors beyond its control. So stay patient and wait for next data points. But the 2% target just looks random. The last 30 years is a macro anomaly and it finally is out of that quiescence. Economy adjusts to rates. There is no predetermined scenario.