The stock market began 2023 with a rally based on the “green shoots” narrative of a Fed pivot and optimism about the effects of China reopening its economy. Since then, the S&P 500 rose to test resistance as defined by its falling trend line and pulled back. Similarly, the equal-weighted S&P 500, the mid-cap S&P 400, and the small-cap Russell 2000 all tested and failed at overhead resistance.

Are the “soft landing” green shoots being trampled? Here are the bull and bear cases.

The bull case

Let’s start with the good news. The bull case rests on the following narratives:

- Inflation is falling, which is expected to allow the Fed to pivot to a less hawkish policy.

- China is reopening its economy, which will boost global demand.

- The market’s technical internals point to a cyclical recovery.

The Fed pivot

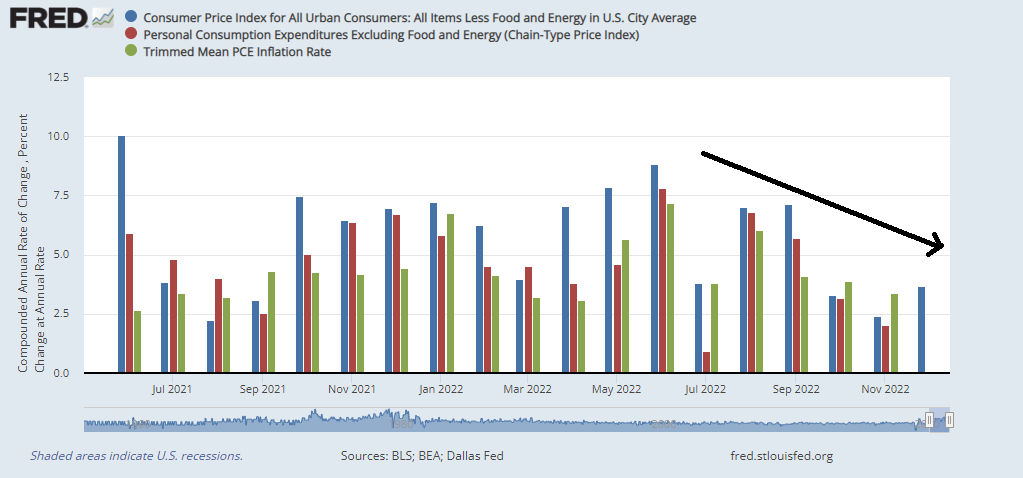

Expectations of a dovish Fed pivot are rising. Core inflation, however it’s measured, is decelerating.

Services inflation is also showing signs of softness. To be sure, shelter inflation is still rising, but the Fed recognizes that rent, as measured by BLS for the purposes of CPI calculation, is a lagging indicator. Consequently, researchers at the Cleveland Fed and BLS published a

paper outlining a New Tenant Repeat Rent Index.

Prominent rent growth indices often give strikingly different measurements of rent inflation. We create new indices from Bureau of Labor Statistics (BLS) rent microdata using a repeat-rent index methodology and show that this discrepancy is almost entirely explained by differences in rent growth for new tenants relative to the average rent growth for all tenants. Rent inflation for new tenants leads the official BLS rent inflation by four quarters. As rent is the largest component of the consumer price index, this has implications for our understanding of aggregate inflation dynamics and guiding monetary policy.

The New Tenant Repeat Rent Index shows a marked deceleration in rents, which is a signal that BLS shelter inflation will be softening in the coming months.

In addition, the Fed has pivoted to focusing on the labor market and wage growth as a source of inflation. The Employment Cost Index, which measures total compensation and is reported quarterly, has begun to decelerate. A similar pattern of softness can also be seen in average hourly earnings.

China reopening

In recent weeks, the market has become excited over the prospect of China reopening its economy. From a top-down perspective, Chinese equities have rebounded strongly and the USD has weakened. Even though the MSCI China and the USD is inversely correlated, it’s difficult to explain the chicken-and-egg problem of correlation and causation.

The USD has been an indicator of risk appetite. A weak greenback has provided a boost to the S&P 500 and the USD Index is now testing a key support level. A definitive violation of support could open the door to more tailwinds for equity prices.

Michael Howell of

Crossborder Capital has highlighted the flood of liquidity and monetary stimulus from the PBOC, which should provide a boost to Chinese GDP growth. As well,

China Beige Book unveiled its China Fiscal Stimulus Index, which is also signaling a fiscal boost to the Chinese economy.

Signs of a cyclical recovery

The combination of the expectations of these bullish factors has led to a recovery in cyclical market leadership. Here are my main takeaways from a review of the relative performance of cyclical sectors:

- Infrastructure stocks have become the new leadership and they have staged a relative breakout to new recovery highs.

- Metals & mining, homebuilders, and semiconductor stocks are all forming saucer-shaped relative bottoms, which are constructive signs of a cyclical rebound.

- Oil and gas stocks are undergoing of consolidation relative to the market, which is not surprising in light of the positive price shocks in the aftermath of the start of the Russo-Ukraine war.

- The only laggard among cyclical industries is transportation, which is still consolidating sideways relative to the S&P 500.

In short, the message from industry leadership to investors is to get ready for a cyclical rebound.

The bear case

The bears will argue that the bull case for equities depends on a difficult trinity. The economy has to navigate a series of challenges, all of which have to happen, namely a short or shallow recession, a rapid decline in inflation, and an aggressive Fed pivot.

Let’s begin with the prospect of a shallow recession or a soft landing involving no recession. Investors need to realize that monetary policy operates with lags. Callum Thomas of

Topdown Charts pointed out that the nature of the global credit crunch. Rates are rising and lending standards are becoming more restrictive. If history is any guide, such conditions usually resolve with a disorderly unwind and credit crisis. The chances of the global economy skirting a recession under such conditions are low.

If the bulls are right and the economy does see a renewed upward impulse in activity, what does that mean for the current decleration in inflation rates? Will prices for goods and services recover as demand rise? How will the Fed react?

Inflation hasn’t been defeated

Moreover, the inflation battle hasn’t been won. Goldman Sachs economist pointed out that the odds of an echo inflation spike in January are high, as year-end price increases reflect the rising costs from 2022.

Inflation fight a marathon

Current expectations call for the Fed Funds rate to rise by two quarter-point increments by the March FOMC meeting, plateau and begin to decline in late 2023. Are those expectations realistic?

The

WSJ surveyed 71 business economists and found a majority expected the Fed will not cut rates in 2023:

- Six expect the Fed to keep raising rates in the second half of the year

- 39 expect the Fed to hold rates steady in the second half of 2023

- 31 expect one rate cut between July and December

The December FOMC minutes continued this key quote: “No participants anticipated that it would be appropriate to begin reducing the federal funds rate target in 2023.” The Fed considers the inflation fight to be a marathon, not a sprint. While goods inflation is moderating as supply chain bottlenecks ease, wages and prices can get sticky, especially in a tight supply-constrained labor market. Arguably, labor shortages are becoming structural and not cyclical, which will put a floor in the pace of wage increases.

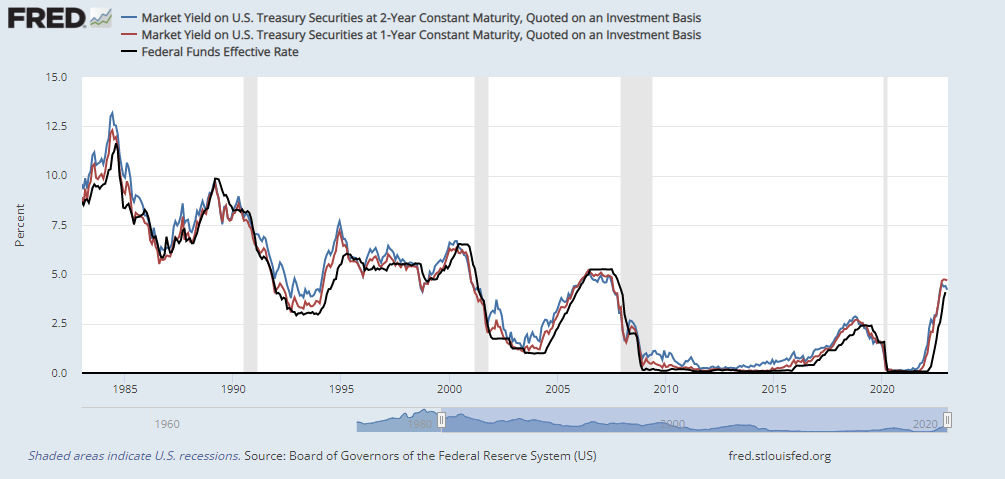

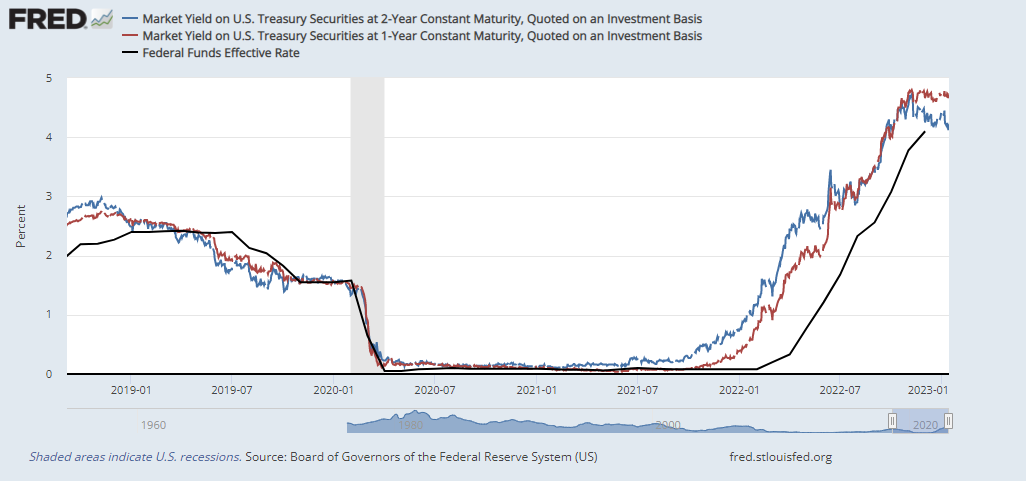

The evidence from the fixed-income market tells the story of differing expectations. The 2-year Treasury yield is a good proxy for the market’s expectations of the ultimate Fed Funds terminal rate and it has been a reasonable forecaster of the terminal rate. By contrast, the 1-year yield represents a short-term expectation.

Here is the close-up of the same chart. While the 2-year yield has declined, the 1-year yield has been flat. By this metric, the market isn’t discounting cuts in the Fed Funds rate in late 2023 and any expectations of Q4 rate cuts are overblown.

By anticipating a Fed pivot, the stock market have loosened financial conditions to near pre-rate hike levels. In other words, the market thinks the inflation fight is a sprint instead of a marathon. Who wins this disagreement?

Risk and reward assessment

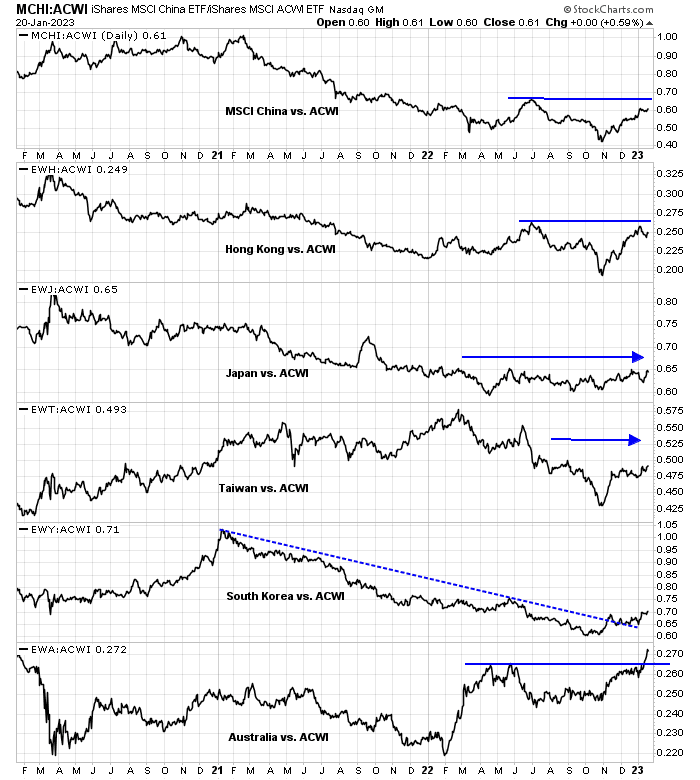

Here is where we stand on upside potential and downside risk. After an initial flurry of excitement over China reopening its economy, the relative performance of China and Chinese sensitive equity markets have begun to pull back and consolidate on a relative basis, other than Australia.

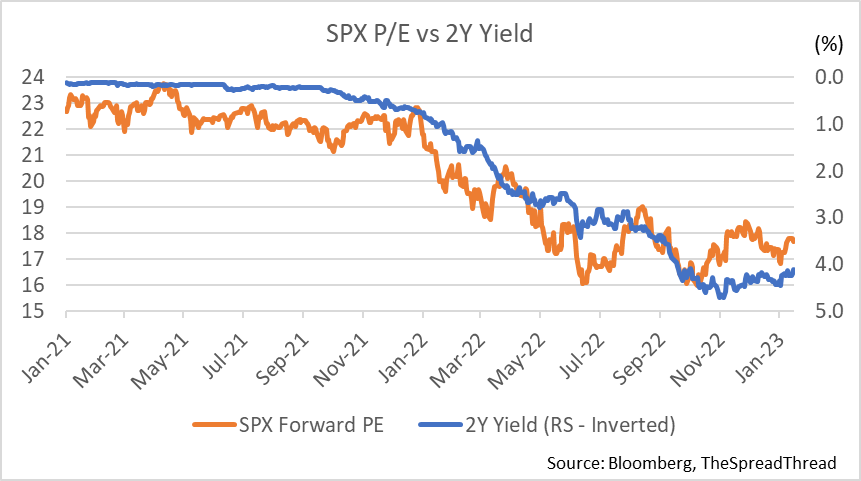

The S&P 500 is trading at a forward P/E of 17 times soft landing earnings. which is a challenging valuation in light of the competition from default-free Treasury yields. What’s the upside if the economy recovers and what’s the downside if the economy were to falter or if rates stay high?

Lastly, don’t forget the debt ceiling fight brewing in Congress. Forecasting how the disagreement will be resolved is beyond my pay grade, but market anxiety is growing as the price of insuring against a US default has skyrocketed. As the Freedom Caucus of the Republican Party is punching above its weight in political influence, a tighter fiscal policy will be a virtual certainty. The combination of a tight fiscal policy and a neutral or tight monetary policy is not conducive to the economy’s growth outlook.

Will the soft landing shoots be trampled? I am inclined to keep an open mind. The coming weeks will be an acid test for both bulls and bears. Earnings season is in full swing and the macro narrative of a soft landing could shift suddenly to an earnings recession. The February 1st FOMC meeting could set the stage for monetary policy. As well, China is celebrating its Spring Festival as workers return to their homes for the Lunar New Year. Spring Festival travel has the potential to develop into a COVID catastrophe as rural China’s healthcare facilities are not as well developed as they are in the major cities, and any possible second wave of infection could reset the tone for the reopening narrative. Risk levels are elevated and everything has to go right for the bulls to prevail.

I believe inflation also depends on liquidity. FED’s assets are twice pre pandemic levels. Let’s see how assets prices react when liquidity tightens. If inflation goes down, earnings will go down too. I believe there will be a lot of volatility in the next 6 months. Just my opinion

A panel discussion at WEF:

https://www.weforum.org/events/world-economic-forum-annual-meeting-2023/sessions/what-next-for-monetary-policy

1. The panel expects rates to be higher a year from now. Implication-don’t expect rate cuts in 2023.

2. Fed is likely wary of the strong labor market and it’s impact on wage inflation. Likely to keep rates higher for longer.

3. The history of seventies inflation is likely to influence their deliberations.

Who’s right? Market or the Fed?

Items 2. And 3. Are not from the panel. Rather, my thoughts.