Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “

Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post,

Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The

Trend Asset Allocation Model is an asset allocation model that applies trend-following principles based on the inputs of global stock and commodity prices. This model has a shorter time horizon and tends to turn over about 4-6 times a year. The performance and full details of a model portfolio based on the out-of-sample signals of the Trend Model can be found

here.

My inner trader uses a

trading model, which is a blend of price momentum (is the Trend Model becoming more bullish, or bearish?) and overbought/oversold extremes (don’t buy if the trend is overbought, and vice versa). Subscribers receive real-time alerts of model changes, and a hypothetical trading record of the email alerts is updated weekly

here. The hypothetical trading record of the trading model of the real-time alerts that began in March 2016 is shown below.

The latest signals of each model are as follows:

- Ultimate market timing model: Buy equities (Last changed from “sell” on 28-Jul-2023)

- Trend Model signal: Bullish (Last changed from “neutral” on 28-Jul-2023)

- Trading model: Bullish (Last changed from “neutral” on 27-Oct-2023)

Update schedule: I generally update model readings on my site on weekends. I am also on X/Twitter at @humblestudent. Subscribers receive real-time alerts of trading model changes, and a hypothetical trading record of those email alerts is shown here.

Subscribers can access the latest signal in real time here.

Oversold markets can become more oversold

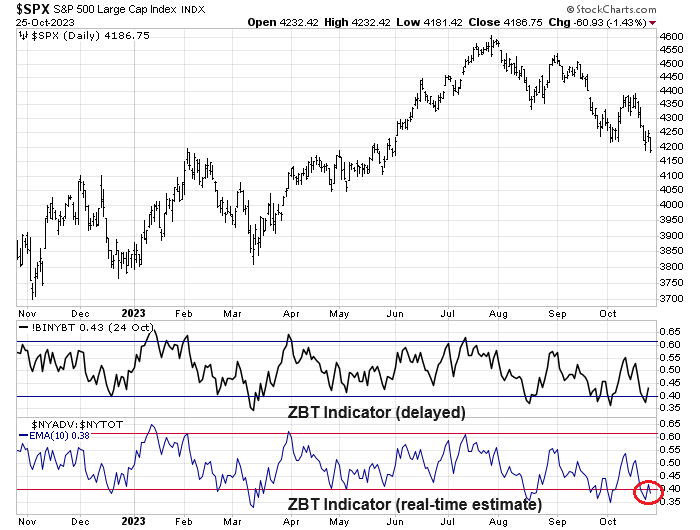

This stock market is oversold on a whole host of indicators. Consider, for example, the Zweig Breadth Thrust Indicator. A Zweig Breadth Thrust buy signal occurs when the ZBT Indicator surges from an oversold to overbought condition within 10 trading days. In the last 10 years, there have been four such buy signals (red dotted lines) and numerous oversold conditions (grey lines).

Here’s what we know. In all cases, the market has been higher 12 months later after a buy signal, though they didn’t always rise in a straight line. In all cases, the market has staged a relief rally when the ZBT Indicator has become oversold, but oversold markets can become more oversold.

A case can be that this is one of those occasions the market could become more oversold and experience a deeper drawdown.

The bear case

The most disturbing pattern is the lack of breadth support exhibited by this market. The accompanying chart shows the percentage of S&P 500 above their 200 dma. Whenever this indicator reached 30%, it has almost invariably fallen further. I interpret this as a sign of bearish momentum caused by poor breadth.

Evidence of poor breadth can be graphically illustrated by the following chart of different U.S. equity indices by market cap. The strongest is the Dow at the top. Market weakness becomes more and more evident as we go down by market cap bands, until the small-cap Russell 2000 at the very bottom. Even if the market were to stage a relief rally, one pre-condition for a durable rally would be a broadening of market leadership.

As well, none of the components in my Bottom Spotting Model are flashing a buy signal right now, though the VIX Index did surge above its upper Bollinger Band and the NYSE McClellan Oscillator did become oversold earlier last week. These conditions as the components of this model have come off levels of extreme stress even as stock prices retreated.

I interpret these readings as the market hasn’t fully discounted several key risks.

- The geopolitical risk of an enlargement of the Israel-Gaza conflict.

- Renewed upward pressure on Treasury yields, which would pressure equity valuation.

- The risk of a disorderly unwind in the credit markets owing to the stress caused by monetary tightening.

An equally disturbing pattern can be seen in some sentiment indicators. The Fear & Greed Index improved even as stock prices declined, indicating growing bullishness, which is contrarian bearish. This argues for a final drop and wash-out before the market can form a durable bottom.

The bull case

While readings from the Fear & Greed Index are worrisome, two sentiment indicators with strong track records have flashed buy signals.

The first is the NAAIM Exposure Index, which measures the sentiment of RIAs who manage individual investors’ funds. The NAAIM Exposure Index fell below its 26-week lower Bollinger Band last week. Such conditions have marked either short- or intermediate-term bottoms in the entire history of this indicator.

Another reliable sentiment indicator is the action of corporate insiders, though this is not a contrarian signal. The market has bottomed whenever insider purchases (blue line) exceeded insider sales (red line), which just occurred late last week.

While I believe seasonality factors are only of secondary importance in technical analysis, the combination of an oversold market and bullish sentiment signals are more important and constructive signs for the stock market.

Technical analyst Wayne Whaley found that the case for an end-of-year rally remains intact, especially when the August–October period has been negative.

However, any upward march in stock prices in November and December may not occur in a straight line. The S&P 500 cycle composite from NDR is projecting a November advance, followed by a low in late November/early December, and higher highs in late December and January

Q3 earnings season has been a qualified success. Forward 12-month EPS estimates are rising, the EPS beat rate is slightly above average, and the S&P 500 forward P/E ratio is below its 5- and 10-year averages. The only blemish is the subpar sales beat rate

In conclusion, the S&P 500 is at a key technical crossroad as it tests support at 4100. While the market is oversold, it isn’t as oversold as it was during the sell-offs in 2022, which opens the door to further potential weakness. However, sentiment readings are turning and pointing to a near-term bottom. To be sure, oversold markets can become more oversold as the market faces several key risks, I judge the odds of a year-end rally at 70% and further weakness at 30%. If a relief rally fails to materialize and the index fails to regain the trend line, or if market breadth does not broaden out, stock prices could see a panic sell-off into much lower levels.

Subscribers received an email alert Friday that my inner trader had initiated a long position in the S&P 500. While sentiment indicators are signaling a strong buy signal, technical indicators are signaling caution. Should Wednesday’s combination of the Quarterly Refunding Announcement and FOMC decision fail to provide a bullish catalyst. I expect to exit my tactical trading position and the Trend Model will be downgraded from bullish to neutral. The usual disclaimers apply to my trading positions.

I would like to add a note about the disclosure of my trading account after discussions with some readers. I disclose the direction of my trading exposure to indicate any potential conflicts. I use leveraged ETFs because the account is a tax-deferred account that does not allow margin trading and my degree of exposure is a relatively small percentage of the account. It emphatically does not represent an endorsement that you should follow my use of these products to trade their own account. Leverage ETFs have a known decay problem that don’t make the suitable for anything other than short-term trading. You have to determine and be responsible for your own risk tolerance and pain thresholds. Your own mileage will and should vary.

Disclosure: Long SPXL