It is said that while bottoms are events, but tops are processes. Translated, markets bottom out when panic sets in, and therefore they can be more easily identifiable. By contrast, market tops form when a series of conditions come together, but not necessarily all at the same time.

I have stated that while I don’t believe that the stock market has made its final cyclical top, we are in the late stages of a bull market (see Risks are rising, but THE TOP is still ahead and Nearing the terminal phase of this equity bull). Nevertheless, psychology is getting a little frothy, which represent the pre-condition for a major top. This is just another post in a series of “thing you don’t see at market bottoms”. Past editions of this series include:

- Things you don’t see at market bottoms, 23-Jun-2017

- Things you don’t see at market bottoms, 29-Jun-2017

- Things you don’t see at market bottoms, bullish bandwagon edition

- Things you don’t see at market bottoms, Retailphoria edition

- Things you don’t see at market bottoms, Wild claims edition

Numerous readings indicate that any semblance of investor fear has gone out the window. An update of the Euphoriameter.from Callum Thomas shows that it has reached a new recovery high for this market cycle.

There are plenty of other examples of fearlessness.

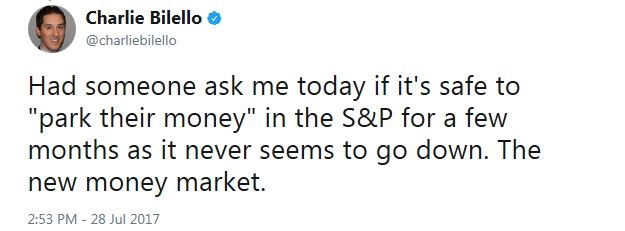

The new money market

Let’s begin with a self-explanatory tweet from Charlie Bilello.

[Shudder]

There is also this *ahem* enticing ad that came across my desk.

[Double shudder]

A kid’s market

Mark Hulbert recently wrote that we are now in a “kid’s market”, where the “kids” with no fear are making all the money:

The concept of a “kids market” was introduced by Adam Smith, the pseudonymous author, in his classic book from the late 1960s entitled “The Money Game.” He used that phrase to refer to an investment environment in which the advisers and traders making the most money are those too young to remember the last bear market.

That would certainly appear to be the case today. The 2007-2009 financial crisis and bear market is now more than eight years in the past. Anyone younger than in their mid-30s probably wasn’t even out of college or graduate school during that bear market, and therefore has little or no direct investment experience of a severe bear market. Their attitudes toward downside risk are entirely different from those of us who lived through that crisis, the bursting of the internet bubble, or other bloodbaths of investment history…

Consider the investment newsletters I monitor with the best risk-adjusted returns over the trailing 30 years (Investment Quality Trends, edited by Kelley Wright) and trailing 20 years (The Buyback Letter, edited by David Fried). Both of these ranking periods are long enough to encompass not just one but at least two severe bear markets. And neither of these top performers is currently recommending Amazon, Facebook or Netflix.

To be sure, kids markets can remain that way for some time. Eventually, however, the kids will encounter a bear market and, in the process, become older and wiser like the rest of us.

As another example of the “kids’ market”, Marketwatch reported on a survey indicating that millennials are far more bullish on equities than their elders:

According to a quarterly investment survey from E*Trade Financial, nearly a third of millennial investors—defined as ones between the ages of 25 and 34—are planning to move out of cash and into new positions over the coming six months. By comparison, only 19% of Generation X investors (aged 35-54) are planning such a change to their portfolio, while 9% of investors above the age of 55 are planning to buy in.

In addition, AAII’s asset allocation survey, which reports on what AAII members are actually doing in their portfolio rather than the volatile weekly sentiment survey, shows that cash allocations have reached a 17 1/2 year low, or the NASDAQ top (chart via Dana Lyons). To be sure, the survey also reported that equity allocations edged down from a 12-year high, but readings are still ahead of levels seen at the start of the Great Financial Crisis.

Booming retail “client engagement”

The rise in retail investor appetite is exemplified by the comments that accompanied the financial results from Schwab, indicating that account openings is the strongest in 17 years, or since the NASDAQ market top:

Strong client engagement and demand for our contemporary approach to wealth management have led to business momentum that ranks among the most powerful in Schwab’s history. Equity markets touched all-time highs during the second quarter, volatility remained largely contained, short-term interest rates rose further, and clients benefited from the full extent of the strategic pricing moves we announced in February. Against this backdrop, clients opened more than 350,000 new brokerage accounts during the second quarter, bringing year-to-date new accounts to 719,000—up 34% from a year ago and our strongest first half total in seventeen years.

These comments are consistent with my previous report about the comments from T-D Ameritrade CEO Tim Hockey about “investor engagement” and “asset gathering”:

Investor engagement has been resilient. High trading volumes despite ongoing volatility. We’re seeing very, very healthy trends and new funded account growth, and asset inflows from both new and existing accounts. Asset gathering itself is a quarterly record, and we’ve already met our previous fiscal year record for net new assets with nearly a quarter yet to go.

The T-D Ameritrade Investor Movement Index is at an all-time high since its inception in 2010.

Surging Street employment

As a result of the retail boom, securities industry employment has risen to a new high (via Sentiment Trader), despite the puzzlement voiced by Josh Brown about downsizing on Wall Street.

No fear in credit markets

Bloomberg recently pointed out that yield spreads in credit markets have become so tight that the rule of thumb of a bond coupon falling below a company`s leverage is being violated:

Bond buyers have a rule of thumb that says be wary when the coupon on a new debt sale slips below the issuer’s leverage. It’s an indicator that investors aren’t being paid enough for the risk they’re taking on.

This adage is being tested anew amid a bubble-like market, as issuers wear down buyers with deals that they’d spurn in almost any other era. One recent example is July’s $500 million sale from HD Supply Waterworks. The water and wastewater company priced the debt beneath its 6.3 level of leverage, which measures debt as a multiple of earnings.

Not only did the sale go through, but demand allowed HD Supply to boost it from $475 million and pay even less interest than initially asked, finishing at 6.125 percent.

In a recent interview, Howard Marks cited the Argentina 100-year bond issue (see my previous comment, Things you don’t see at market bottoms, 23-Jun-2017), as well as the Netflix 10-year bond with a 3.625% coupon as signs of market froth (click this link if the video is not visible). Marks expressed concern about the maximum upside of 3.625% for a growthy company like Netflix,

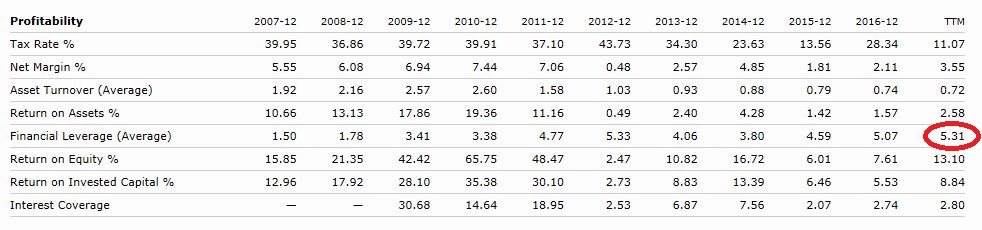

As a frame of reference, the latest statistics from Morningstar shows the NFLX interest coverage to be 2.8, and a debt to equity ratio of 5.3 – well above the 3.625% coupon.

That’s enough. I am exhausted and don’t have time to talk to you anymore, I am heading back into the party and to trade the new 5x leverage ETPs.

“That’s enough. I am exhausted and don’t have time to talk to you anymore, I am heading back into the party and to trade the new 5x leverage ETPs.”

Genius

That’s exactly the way I see it.i have been looking at SPY Oct straddles…option prices are very cheap…the complacency is astounding. By the way I am 71 years old and have been investing/ trading since 1977.