It is said that while bottoms are events, but tops are processes. Translated, markets bottom out when panic sets in, and therefore they can be more easily identifiable. By contrast, market tops form when a series of conditions come together, but not necessarily all at the same time.

I have stated that while I don’t believe that the stock market has made its final cyclical top, we are in the late stages of a bull market (see Risks are rising, but THE TOP is still ahead). Nevertheless, psychology is getting a little frothy, which represent the pre-condition for a major top.

As a result, I am starting a one in an occasional series of lists of “things you don’t see at market bottoms”:

- Argentina’s 100-year bond offering

- Irrational Exuberance Indicator at fresh highs

- The E*Trade Indicator flashes a warning

- More signs of excesses from the Chinese debt time bomb

Argentina’s 100-year bond

Earlier in the week, Argentina announced that it had received USD 9.75 billion in its financing for a 100-year USD denominated bond offering (via Reuters). Demand was strong, and the deal was priced at a yield of 7.9%.

Excuse me? Didn’t Argentina just emerge from default? Who in his right mind would lend Argentina money at 7.9% for 100 years? This financing is evidence of how starved the market is for yield.

If you don’t think that financing is unreasonable, then I have the following question for anyone who voted for Donald Trump. The latest small business confidence figures from NFIB shows confidence surged in after the November election. Undoubtedly, much of the rise was attributable to the renewed optimism of Trump supporters in the small business sector.

How much would you lend money to a Donald Trump led government? The yield on a 7-8 year Treasury, assuming a two-term Trump presidency, is about 2%.

Is 2% enough for 7-8 years? If not, then how much more would you want?

Irrational exuberance

Jeroen Blokland recently pointed out that the Irrational Exuberance Indicator, which is calculated from Yale’s survey of confidence that the “market will be higher one year from now” compared to confidence in “valuation of the market”, has risen to levels that were higher than past market peaks.

This is definitely another thing that you don’t see at market bottoms.

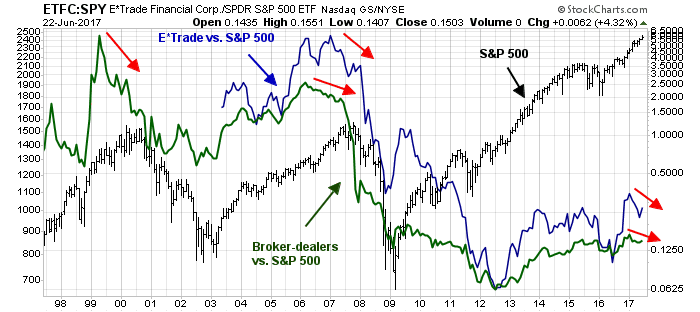

The E*Trade Indicator

Joe Wiesenthal recently made an off-beat observation about E*Trade (ETFC):

Rather than just focus a single stock, the chart below shows the relative performance of ETFC against the market and the Broker-Dealer ETF (IAI) against the market. Both relative performance ratios topped out before the last two major market peaks.

Both ETFC and IAI are struggling to achieve new highs even as the SPX rises to new highs. Is this another warning of a market top?

The China debt time bomb

Economic recessions serve to unwind the excesses that occurred in the previous expansion. In the US, there are no significant excesses, if unwound, are likely to totally tank the economy. While some valuation excesses can be found in unicorns, the implosion of Snapchat, Uber, or other Silicon Valley darlings are unlikely to cause significant economic damage.

From a global perspective, however, much of the excesses can be found in China. The New York Times recently reported that the market was getting spooked because Beijing was cracking down on the foreign takeover financing of a number of large Chinese conglomerates:

Some of China’s largest companies may pose a systemic risk to the country’s banks, a senior banking official said on Thursday, in the latest signal that Beijing is ratcheting up scrutiny of a financial system plagued with hidden debt that poses a hazard to the health of the economy.

The official, Liu Zhiqing of the China Banking Regulatory Commission, did not name any companies. But shares of some of China’s biggest global deal makers plunged on Thursday.

They included the publicly traded arms of Fosun International, which in recent years bought the Club Med chain of resorts and other properties; Dalian Wanda, which owns the AMC Theaters chain in the United States and has long sought deals in Hollywood; and the HNA Group, an acquisitive conglomerate with murky ownership.

At a briefing on Thursday in Beijing, Mr. Liu, deputy head of the commission’s prudential regulation bureau, said that his agency was looking into “systemic risk of some large enterprises,” according to numerous media accounts, and that the risk could spread to other institutions.

Bloomberg columnist David Fickling revealed that much of the concerns stemmed from the fact that many of the large Chinese acquirors have been free cash flow negative. In other words, these companies are relying on the kindness of the financial system to maintain both solvency and their acquisition sprees.

By contrast, FCF of recent major American acquirors have been consistently positive.

These two charts dramatically illustrate the point of the differences in the levels of financial excesses between China and the US. While I am not predicting an imminent collapse of the Chinese economy, this is another thing that you don’t see at market bottoms.

Despite these negatives, I reiterate my contention that this is not the top of the equity market. In a future post, I will explain why the global reflation trade still has some life left.

” In the US, there are no significant excesses, if unwound, are likely to totally tank the economy. While some valuation excesses can be found in unicorns, the implosion of Snapchat, Uber, or other Silicon Valley darlings are unlikely to cause significant economic damage.”

There are excesses all over the US economy. An implosion of “Silicon Valley darlings,” which I presume would include the FANG stocks, would cause significant economic damage, through a chain of consequences.

As it stands now, most state and municipal pension funds are vastly underfunded, even assuming they could achieve their ~8% wishful thinking assumptions of growth. IL for one seems heading for bankruptcy as is, or a downward spiral of tax increases and emigration.

A severe bear market would require massive tax increases to keep those funds solvent. Either that, or the alternative of multiple bankruptcies and pensioners losing their incomes, would cause an unwinding of the “everything bubble” and create a recession at least as bad as when housing collapsed ten years ago.

I wouldn’t be too complacent about our relatively less indebted situation compared to China. If one added to our debt totals the commitments that have been made for pensions and retiree health care, we aren’t in much better shape financially. We have the edge of having a smaller role for the government in the economy than China does, and thus we misallocate less capital, but that won’t save us.

Rick –

You raised two points that I would like to address:

1) First, the valuation of FANG and its variants are not the same as unicorn valuation. FANG valuation is relatively reasonable compared to its own history. Private market unicorns valuations are far more elevated compared to public market Tech stocks.

2) I recognize that defined benefit plans, whether public sector or private sector, have unrealistic assumptions that represent a ticking time bomb. A recession is unlikely to be the trigger that blows up the bomb, however. As long as cash flows remain solvent, the funding authority can play an extend and pretend actuarial game.

The kind of pain that you postulate that is involved is unlikely to occur, as there will be benefit cuts. Just as airline employees in the past few cycles when the funding authority (airline) got into financial trouble.

1) The valuations of some of the broader FANG universe (e.g. Tesla) are every bit as extended as Uber. And keep in mind that the investors in the private companies have been investing money they know they are highly unlikely to need to redeem for many, many years, if ever. So Uber’s valuation is likely to fall dramatically at its next fund raise, but that won’t induce its existing holders to try to peddle their shares in competition with the company itself.

The FANG, etc. public companies are mostly held by ETFs that are held by the public, which always gives lip service to “investing for the long run” but in bear markets are more likely to sell the more stocks go down, usually clearing out completely at the bottom. That will especially be the case in the next bear market. All those years of ZIRP forced plenty of people into stocks and ETFs who really don’t belong there. I’m thinking of baby boomer retirees, who should really be mostly in safe fixed income, but those things still pay nothing much, so they have excessive levels of equities for the amount of loss they can handle. As they see their net worth dropping in a bear market, they will feel they have to sell. Losses in 50% or more range can’t be ruled out for the market in general and overowned FANGs in particular. (BTW, I agree with you we probably aren’t at the top just yet.)

2) The cause and effect is not that a recession will cause a pension problem directly. Rather, a bear market will shrink pension funds, and the resulting increase in taxes will exacerbate the recession and the bear market.

The authorities can pretend as much as they want, but they can’t extend. They have to be able to write checks to the retirees, and pay their health care premiums. Besides the baby boomers already older than 65, many government workers can retire starting at 55, so there is a huge increase in pension obligations in process. When those not yet retired see a fund rapidly depleting, they will retire too to grab what they can while there is still something there, as happened with the Dallas police and firefighters late in 2016.

Given that government employees unions have outsize political influence, the solution nearly everywhere will be much higher taxes. I don’t think your airline example applies. If airlines had the ability to tax the general public, then they would have done so instead of cutting benefits; politicians can and will raise taxes.

In general, it is easy to underestimate the effect on profit margins of a recession. Profit margins as a percentage of sales are close to record highs going back many decades. One reason for that has been companies laying off non-essential workers and moving to a relatively fixed cost structure to capture operating leverage as revenues rose.

Should their revenues drop, how are they going to cut costs enough to maintain profit margins–lay off some computers and robots? So stocks that seem not overvalued on today’s earnings won’t look so cheap should, as is likely, a recession causes a big drop in profits on even small drops in revenues.

The valuation of Tech stocks, outside of TSLA, isn’t that unreasonable. See Yardeni: http://blog.yardeni.com/2017/06/relative-exuberance-for-tech.html

As long as the pension funds have enough money to pay retirees, they can still play the extend and pretend game. It’s not just the state and municipal authorities, but the corporates do the same thing. Arguably, GM is one big hedge fund with a pension pool and pension liabilities.

Rick

If the kind of asset deflation that you have described, sets in, government printing presses will work overtime to print money. The minions who make these decisions, cannot risk their jobs, through societal anarchy and loss of confidence in the fiat currency system.

As debt to GDP ratios go, the US, is at the low end of the spectrum by comparison to Japan and Europe (yes, as an aside, Professor Shiller has questioned the whole idea of debt to GDP, and I agree with Professor Shiller). As FAANG valuations go, it is better than such stocks circa 2000. The FAANG valuations are only justifiable if their growth rates continue for the foreseeable future.

Your point about asset bubbles is well taken. The bail out of the US banking system is perhaps the most egregious bubble that was floated. Bill Gross from PIMCO was right when he referred to uncle Sam as “debt man walking”. Governments will tax, will print money and try to inflate their way out of insolvent situations (like Illinois tax system).

As things stand today, Joe six pack is still not buying stocks with both hands, but it is coming. Time and Newsweek magazine covers will tell us when that happens (for now, Bitcoin mania is at its peak).

Without getting too verbose about this, one could divest oneself of fiat currency and buy “real assets” with such currency before it becomes confetti. Here is a book I read painstakingly but was still worthwhile: When money dies by Adam Ferguson. Here is another painful read that is worthwhile also: This time is different: Eight centuries of financial folly by Professors Reinhart and Rogoff. My thoughts above are elaborated in detail in these two books.

We live in a “relative” world. US ten year treasuries currently yield 2.14% are much cheaper than German bunds of similar maturity.

FAANG valuations are rich today, but by comparison to year 2000, are extremely attractive (PE to Growth ratio would be a better metric to use for comparison here).

Yes, in an “absolute” world, there are bubbles everywhere, based on Bill Gross’s missive, I referred to earlier, but we live in a “relative” world.

So, if GE, MSFT, INTC, ORCL could float 200 year bonds, they may be able to buy large quantities of their own shares, and valuations of these companies would become ridiculously cheap (Warren Buffet is on record, and he is right about it, that if today’s interest rates are to be held for another ten years, stocks are an absolute steal). Another example of “relative world”.

Here is one more bubble being inflated. Yesterday’s Wall Street journal has a full section on real estate. The first article is on how ‘confident’ buyers are able to buy real estate sight unseen. The journal talks about real estate boom in Victoria Canada and also has an advertisement with the title ‘Why today’s real estate brokers have become educators’. Due apologies to realtors, I have nothing against them.

Front page article in the same journal also talks about ‘Fed tests buoy case for easing banking rules’. Cheap money will eventually spawn bubbles (like Argentine 100 year old bonds or real estate circa 2008 or oil drilling circa last decade). As US banks open the spigot of capital, more bubbles may form. We do live in interesting times. Are we there yet, is the question, ‘there’ means a market peak. I would like to see Joe six pack mortgaging houses and buying stocks with both hands at some point in this cycle. It is unfortunate and sad to say something like this, but that is the history of market tops.

D.V. this is exactly why I watch margin loan levels.

Here is what I watch. It’s a page with three charts. Top is S&P middle is loans. Bottom is my calculation of YOY % growth in margin loans versus YOY in S&P. Note the burst higher in loans versus market at previous peaks in 2000 and 2007.

http://product.datastream.com/dscharting/gateway.aspx?guid=0d4bdbe2-691d-48d2-8964-8362f5c8d135&action=REFRESH

Note that when the ratio is negative as in 2015 the market is vulnerable to correction. It’s showing a lack of speculation energy.

Keep this link. It updates but note that margin loans are announced monthly with a long delay. May’s number is not out yet for example.

Ken, thanks for posting this. It is very useful to have these charts at one place.