Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Model is an asset allocation model which applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. In essence, it seeks to answer the question, “Is the trend in the global economy expansion (bullish) or contraction (bearish)?”

My inner trader uses the trading component of the Trend Model to look for changes in the direction of the main Trend Model signal. A bullish Trend Model signal that gets less bullish is a trading “sell” signal. Conversely, a bearish Trend Model signal that gets less bearish is a trading “buy” signal. The history of actual out-of-sample (not backtested) signals of the trading model are shown by the arrows in the chart below. Past trading of the trading model has shown turnover rates of about 200% per month.

The latest signals of each model are as follows:

- Ultimate market timing model: Buy equities

- Trend Model signal: Bullish

- Trading model: Bearish

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers will also receive email notices of any changes in my trading portfolio.

Volatility ahead

Equity market volatility, as measured by the VIX Index, has been extraordinarily low by historical standards.

Last week’s events is setting the stage for greater market volatility in 2018, which stems from the following three sources:

- Political uncertainty

- Fiscal policy

- Monetary policy

Let’s examine each, one at a time.

The tale of l’affaire Russe

Last Friday, the stock market was hit by the report that former Trump administration National Security Adviser Mike Flynn had pleaded guilty to a minor charge, and he was fully cooperating with the Mueller investigation by testifying against the Trump campaign in return for leniency. It was further reported that Flynn claimed that Trump had directed him to contact the Russians during the election (later corrected to the transition period). The SPX nosedived over 1% on the news, though it recovered later in the day to close -0.2%. The difference between the timing of any Russian contact is legally important. If candidate Trump had contacted the Russians during the campaign, it could be interpreted as a violation of the Logan Act which prohibits ordinary citizens from negotiating with unfriendly governments. Contacting foreign governments during the transition period to conduct foreign policy could be viewed as it constitutes the normal business of a new team.

Nevertheless, it is hard to see how Flynn got off so lightly if the only revelation was the Trump transition team had contacted the Russian government. There was no mention of the planned Gulen rendition to Turkey in return for a $15 million fee in the indictment, and Mueller declined to indict his son. The Lawfare blog’s quick and dirty analysis concluded that we should expected further bombshells in the near future:

The narrowness [of the charge against Michael Flynn] gives a superficial plausibility to the White House’s reaction to the plea. Ty Cobb, the president’s ever-confident attorney, said in a statement: “The false statements involved mirror the false statements [by Flynn] to White House officials which resulted in his resignation in February of this year. Nothing about the guilty plea or the charge implicates anyone other than Mr. Flynn.” Cobb reads Friday’s events as an indication that Mueller is “moving with all deliberate speed and clears the way for a prompt and reasonable conclusion” of the investigation.

This is very likely not an accurate assessment of the situation. If Mueller were prepared to settle the Flynn matter on the basis of single-count plea to a violation of 18 U.S.C. § 1001, he was almost certainly prepared to charge a great deal more. Moreover, we can infer from the fact that Flynn accepted the plea deal that he and his counsel were concerned about the degree of jeopardy, both for Flynn and for his son, related to other charges. The deal, in other words, reflects the strength of Mueller’s hand against Flynn.

It reflects something else too: that Flynn is prepared to give Mueller substantial assistance in his investigation and that Mueller wants the assistance Flynn can provide. We are not going to speculate about what that assistance might be. But prosecutors do not give generous deals in major public integrity cases to big-fish defendants without good reason—and in normal circumstances, the national security adviser to the president is a very big fish for a prosecutor. The good reason in this case necessarily involves the testimony Flynn has proffered to the special counsel’s staff. The information in that proffer is not in any of the documents released Friday, and it may not even be related to the information in those documents. Prosecutors tend to trade up. That is, for Mueller to give Flynn a deal of this sort, the prosecutor must believe he is building a case against a bigger fish still.

Notwithstanding any dispute over whether anyone violated the Logan Act, the Trump team`s troubles with the Mueller probe are not over. Trump’s weekend tweet was problematical, as he admitted that he knew Flynn had lied to the FBI, and then asked Comey to back off on the Flynn investigation. Many legal analysts have interpreted these actions as obstruction of justice, which was the charge that forced Nixon`s resignation.

The latest Gallup presidential job approval, which was taken before the Flynn news, shows that Trump’s approval at 34%. Historically, the stock market has not performed well when the approval rate falls to 35% or lower.

That’s bearish, right? Well…should sufficient evidence surface to force either the resignation or impeachment of Donald Trump, the knee-jerk market reaction would be bearish. However, Wall Street would undoubtedly sleep better at night if President Pence were to be in the White House, which would be a bullish outcome.

Hence the potential volatility. How this plays out, or how the market is likely to react to any single piece of news, I have no idea. But watch for rising political uncertainty in the year ahead.

Upside volatility from a cyclical surge

Notwithstanding any possible noise from l’affaire Russe, the market will continue to focus on the combination of the earnings and interest rate outlook. Even without any tax cut effects, the earnings outlook looks bright, which will likely be a source of upside equity price volatility.

As experienced investors are aware, Street analysts tend to publish earnings estimates that are too high and then gradually revise them downward. The latest update from FactSet indicates that Q4 EPS estimates are seeing the least amount of downward revisions since Q2 2011.

In addition, the latest FactSet summary of EPS estimates show that normalized forward 12-month EPS continues to rise steadily. This is another sign of bullish fundamental momentum that is supportive of higher stock prices.

In addition, Callum Thomas pointed out that the market is enjoying a period of macro tailwinds, as economic surprises and investor sentiment, otherwise known as FOMO, tend to surge into January.

Tax cuts: Upside or downside volatility?

What about the effects of the corporate tax cuts? The aggregate benefits of a corporate tax cut may be marginal. The next step for the tax bill is the reconciliation between the Senate and House versions of the bill before it can become law. One of the key differences is the Senate version of the bill cuts the corporate tax rate to 20% in 2019, while the House version immediately lowers the corporate tax rate to 20% in 2018.

Assuming the optimistic case that the corporate rate is 20% in 2018, a Reuters report indicated that the consensus 2018 EPS estimate would be about $150. Based on the current FactSet FY2018 estimate of $146.05, that amounts to a 2.7% increase in EPS. To be sure, other strategists put the increase higher, in the 5-8% range,

A mid single digit percentage increase in earnings, which translates to a similar level of stock market price appreciation, assuming no further multiple expansion? Is that all?

Ed Yardeni came to a similar conclusion using top down data. Yardeni, who declared that he was “all for tax cuts”, but he was “having a problem with the data”. He analyzed the effective corporate tax rate using two separate and distinct sources, the GDP data, and IRS data. The effective corporate tax rate was somewhere between 13.0% and 20.7%. If the effective rate is already that low, what’s the benefit of cutting the statutory rate to 20%?

Yardeni concluded:

Congress may be about to cut a tax that doesn’t need cutting. Or else, the congressional plan is actually reform aiming to stop US companies from using overseas tax dodges by giving them a lower statutory rate at home.

It is unclear how much of the stock price rally in the last few months is attributable to the cyclical effects of better earnings growth, and how much is discounting the effects of a tax bill. Given the relatively meager tax cut estimated boost to 2018 EPS growth. The tax bill may already been discounted by the market. In that case, we may be setting up for the downside volatility effect of “buy the rumor, sell the news” scenario when the bill is actually passed.

And we haven’t even discussed the possibility of a government shutdown in early December…

How will the Fed react?

Assuming that the GOP tax cut package does pass, another downside wildcard is the Fed’s reaction. Will the Fed be more inclined to tighten monetary policy faster in the face of fiscal stimulus?

Consider where we are today. The market is fully discounting a December quarter-point rate hike, and about two quarter-point rate hikes in 2018. By contrast, the Fed’s dot plot calls for a December hike, followed by three more raises next year.

While there has been some discussion from Fed officials about the uncertainty surrounding possible rate hikes in light of the absence of inflation, the inflation internal indicators are edging up. In all likelihood, we will start to see rising inflationary pressures in the very near future. As an example, the New York Fed’s Underlying Inflation Gauge (UIG) has been gradually rising. The latest readings in October shows the full data set measure at 3.0%, while the price-only measure at 2.3%. Both of these metrics are above the targeted inflation rate of 2.0%.

In the past, real YoY money supply growth has gone negative ahead of recessions. Real M2 growth is falling and could go negative by Q1 or Q2 at the current pace of deceleration.

In addition, the nomination of Marvin Goodfriend as Federal Reserve Governor will tilt the FOMC in a more hawkish direction. I wrote about Goodfriend last June (see A Fed preview: What happens in 2018?). At that time, I had highlighted the Gavyn Davies endorsement of Goodfriend for the Fed by characterizing him as an orthodox rules-based monetarist:

- Goodfriend’s conservative pedigree goes all the back to Reagan’s Council of Economic Advisors. He is a typical member of his generation…in having a very profound distaste for inflationary monetary policies.

- Goodfriend believes in a formal inflation target, which he thinks should be approved by Congress, rather than being set entirely within the Fed…On the Taylor Rule, Prof Goodfriend has recently argued that the FOMC should explicitly compare its policy actions with the recommendations from such a rule, because this would reduce the tendency to wait too long before tightening policy.

- Goodfriend believes that interest rates are a much more effective instrument for stabilising the economy than quantitative easing.

- Goodfriend has frequently argued forcibly against allowing an “independent” central bank to buy private sector securities such as mortgage-backed bonds, which he deems to be “credit policy”.

- Goodfriend has always been worried that “independent” central banks will develop a chronic tendency to tighten monetary policy too late in the expansion phase of the cycle.

Goodfriend has also shown himself to be a highly dogmatic advocate of demonstrating central bank credibility in its price stability mandate. As an example, he wanted to raise rates in 2011, even as the eurozone underwent its crisis and Washington underwent a debt ceiling crisis. As a way of demonstrating its credibility, Goodfriend believed that the Fed should abandon a gradualist monetary policy and adopt a rapid-fire decisive approach to interest rate changes (via FT Alphaville):

Goodfriend was also sceptical of the Fed’s decision to begin raising interest rates in 2015, when inflation was weak — even excluding commodities — and nothing indicated it would quickly return to 2 per cent. According to this former student, Goodfriend believed the Fed should make its moves over relatively short periods of time. Thus the 1994-5 tightening was close to ideal because it quickly recalibrated the level of short-term interest rates from 3 per cent to 5.25 per cent. (With an overshoot to 6 per cent in the middle, but still…)

The former student recalls Goodfriend saying that if the Fed were to raise interest rates in 2015 it would probably have to wait a long time before any additional rate increases, which would damage the Fed’s credibility and potentially worsen the downtrend in inflation expectations. That’s more or less exactly what happened. According to this student’s account, Goodfriend would have preferred the Fed waited until it could commit to a relatively short and uninterrupted campaign of “normalisation”.

You want policy volatility? You’ll get it with Marvin Goodfriend. Despite his monetarist beliefs, Marvin Goodfriend may be more tolerant of rising inflationary pressures, at least initially, and then respond with a series of staccato rate hikes to cool off the economy.

Left unsaid during the news of the Goodfriend nomination is the identity of the Fed vice chair. The latest speculation of the two top contenders are John Taylor, who is just as dogmatic as Goodfriend and equally hawkish, and the more moderate Mohamed El-Erian.

Even though El-Erian may be viewed as the moderate and pragmatic choice by Wall Street, he may turn out to have far more hawkish views should he assume the position as vice chair. In early 2016, El-Erian had penned a Project Syndicate essay, entitled “The End of the New Normal?”. In that essay, he worried that the Fed would run out of bullets in the next downturn, and it was time for fiscal policy to engage in some of the heavy lifting currently performed by monetary policy. More recently, he wrote a Bloomberg article that was supportive of the tax bill and infrastructure plan, which is likely to endear him to Trump:

That brings us back to the importance of policy implementation in sustaining and buttressing the historic rally in stocks.

To maintain the uptick in growth, Europe and the U.S. need to implement measures that reverse persistent downward pressures on potential — that is, the ability of advanced economies to grow not just today but also in the future, and to do so in a more inclusive manner.

In the U.S., this requires progress on Capitol Hill on the tax plan, as well as congressional support for the administration’s infrastructure initiative and steps to enhance labor productivity and improve the benefit-to-cost ratio of technological innovation.

That said, the passage of a tax cut would take some of the pressure off the Fed to be overly accommodative and embark on a faster pace of monetary policy normalization. While Mohamed El-Erian as vice chair would largely be supportive of the Republican tax bill, he would also push for faster pace of rate hikes.

The market is only expecting about two quarter-point rate hikes next year. Would four or five hikes increase market volatility?

The week ahead

Looking to the week ahead, the market may be ready for a brief pause in its advance. I sent out an alert to subscribers on Thursday that my trading account was taking a short position in the market. A number of signs of bullish exhaustion were starting to appear.

First, risk appetite was starting to roll over. Momentum stocks, which had been performing well, had begun to weaken relative to the market. As well, small cap stocks, which tend to be more domestically exposed and more sensitive to tax cuts, underperformed even as the tax bill made its way through the Senate.

Sentiment is getting a little frothy. The 10 day moving average of the CBOE put/call ratio (CPC) has reached a crowded long reading. In the past, the market has tended to stall out at these levels of complacency.

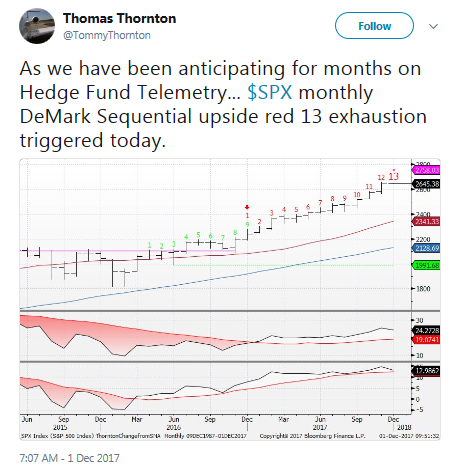

In addition, Tommy Thornton identified a monthly $SPX DeMark upside exhaustion signal on Friday.

The track record of these signals have been remarkable, though the sample size is small (N=7).

My inner trader is short the market, and he is waiting for either signs of oversold conditions on short-term indicators to cover, or a renewed upside surge to fresh highs as a way of defining his downside risk. The market ended Friday with a hanging man candle, which is a potential sign of a bearish reversal.

History has shown that if we get any downside follow-through on Monday, the short-term outlook is bearish for stock prices over a 3-4 day time horizon.

My inner investor remains constructive on stocks, and his asset allocation is at roughly the level specified by his investment policy statement. If history is any guide, the market is likely to pause briefly before resuming its seasonal rally into year-end (via Topdown Charts).

Disclosure: Long SPXU

I think the volatility peaked on Friday when that false report of Trump being involved with violating the Logan Act appeared. I closed out my short.

Your short calls have not worked out very well this year, I think you are not giving enough weight to political developments and how they drive this market, I would like to know how your trading account did this year.

Some individual names in sectors like semiconductors sold off pretty sharply on Monday already, so the NASADQ might temporarily stabilize here. A bottom on Thursday would be in agreement with the haning man study and also the old trading rule that markets tend to see weakness on the Thursday before option expiration weeks. On the other hand, the market has recently developed a tendency to resolve bearish or bullish setups in shorter timeframes, so I am curiously waiting to see if it will take 3-4 days to play out this selloff.

Here is another read on trading in December: http://jeffhirsch.tumblr.com/post/168198047653/typical-december-pattern-any-retreat-usually-a

Sanjay

Thanks for the link to Almanac trader. I note the bottom is circled around the tenth trading day of December, which this year would be around 14th December, if the pattern holds. That said, Nasdaq is weak here, last few trading sessions. A weak Nasdaq is not a good development for larger indices like S&P as large cap Nasdaq stocks like FAANG are likely to contribute significantly to S&P 500. Such divergences can be made up for by sector rotation like value stocks, Telecom, staples, old line industrials, defense and aerospace etc. (some of these were the primary beneficiaries of the Trump election). That said, such sector rotation may not be able to stave off losses from Nasdaq spreading to broader indices. Here is a link I found useful.

https://www.cnbc.com/2017/12/04/stock-markets-crazy-monday-could-be-a-warning.html

Cam’s warning may be prescient.