Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Model is an asset allocation model which applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. In essence, it seeks to answer the question, “Is the trend in the global economy expansion (bullish) or contraction (bearish)?”

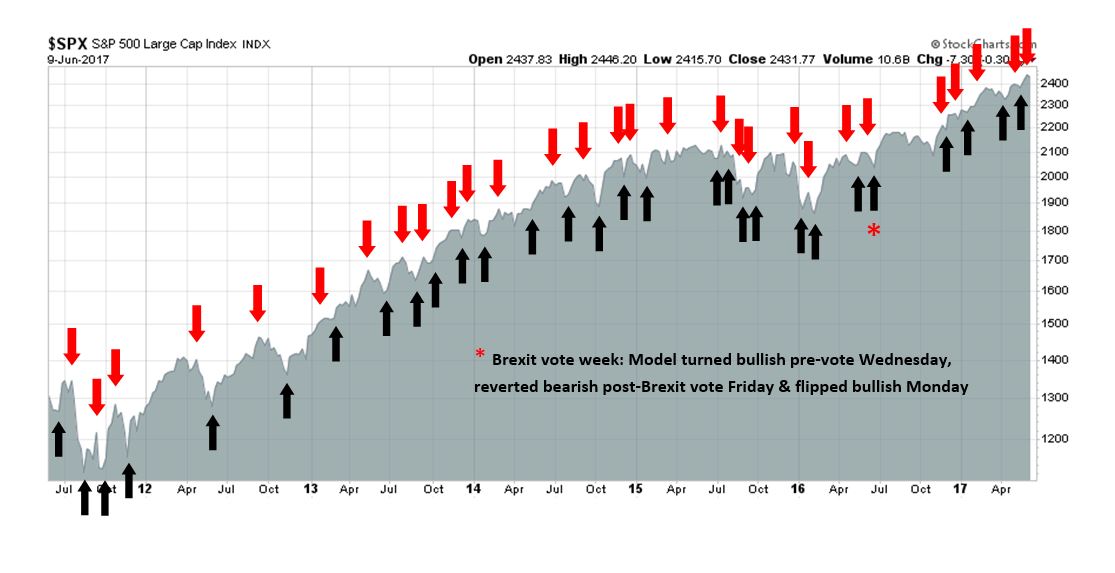

My inner trader uses the trading component of the Trend Model to look for changes in the direction of the main Trend Model signal. A bullish Trend Model signal that gets less bullish is a trading “sell” signal. Conversely, a bearish Trend Model signal that gets less bearish is a trading “buy” signal. The history of actual out-of-sample (not backtested) signals of the trading model are shown by the arrows in the chart below. Past trading of the trading model has shown turnover rates of about 200% per month.

The latest signals of each model are as follows:

- Ultimate market timing model: Buy equities

- Trend Model signal: Risk-on

- Trading model: Bearish

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers will also receive email notices of any changes in my trading portfolio.

Marvin Goodfriend for Fed chair?

Over at Calculated Risk, Bill McBride asked the following questions after featuring analysis from Goldman Sachs which expected a June rate hike:

Almost all analysts expect a rate hike this week, even though inflation has fallen further below the Fed’s target. A few key questions are: Does the FOMC see the dip in inflation as transitory? Will the Fed keep tightening if inflation stays below target? Will the next tightening step be another rate hike or balance sheet normalization?

Those are all good questions, but as the market looks ahead to the FOMC meeting next week, it’s time to look beyond what the Fed might do at its June meeting, or even the remainder of the year. The bigger question is how the Fed reaction function might change in 2018 as the new Trump nominees to the Board of Governors assume their posts.

Another key question to consider is whether the Trump administration plans to keep Janet Yellen as Fed chair. As there are three open positions on the board, and there are three rumored nominees, any potential new Fed chair would come from the current list of new appointees. Of the three, the most likely candidate is Marvin Goodfriend.

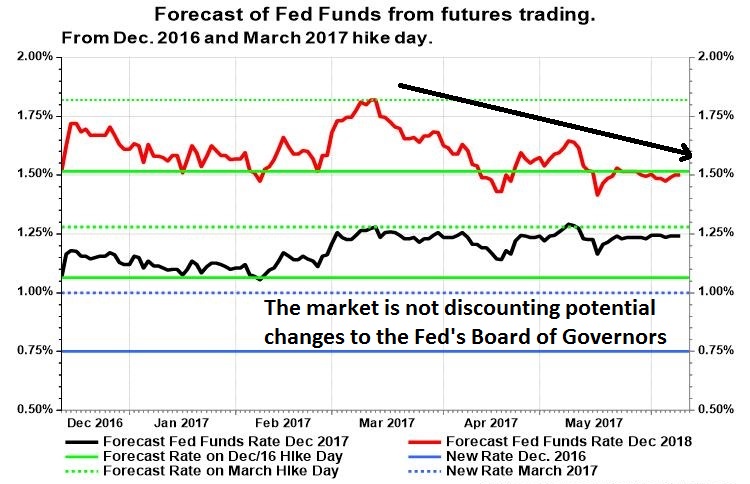

Current market expectations show that December 2017 Fed Funds (black line) to be relatively steady, but December 2018 Fed Funds (red line) have been declining.

Regardless of whether Goodfriend becomes the new Fed chair, I examine this week how the influence of the three likely appointees may change the path of monetary policy in 2018 and beyond.

The Fed’s current analytical framework

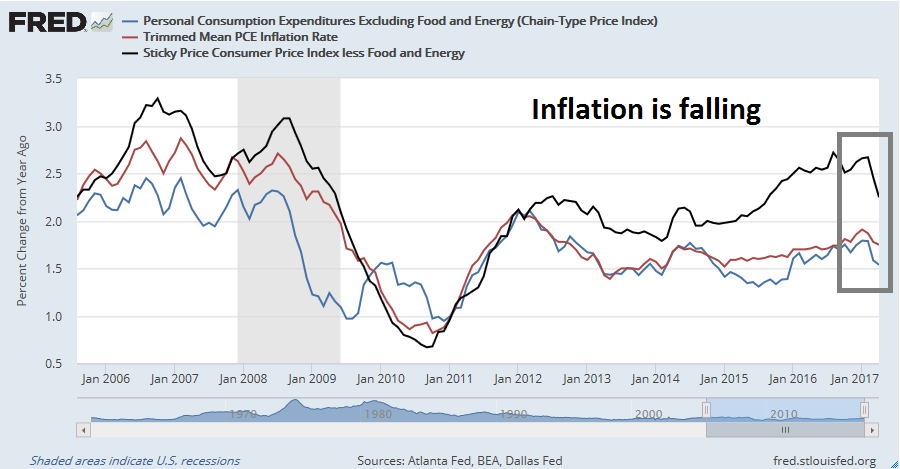

Let’s start with the analytical framework of the current Fed. There has been much hand wringing about the decline in inflation. However it’s measured, whether using the Fed’s preferred metric of core PCE inflation, trimmed-mean PCE, or sticky-price inflation, inflation is falling.

For now, evidence of falling inflation is likely to be ignored. As Fed watcher Tim Duy pointed out, “The Fed’s focus remains on the labor market. Hence, they remain focused on two rate hikes and balance sheet action still to come this year.”

Here is how the employment picture looks like right now. Unemployment (black line) has fallen to the historically low level of 4.3%, while median nominal real earnings (blue line, quarterly data) has been accelerating, and the more timely average hourly earnings (red line, monthly data) has softened.

As the Fed has traditionally been cautious, and believed that monetary policy operates with a lag, the natural tendency would be to hike in June and wait for more data.

Transitory weakness?

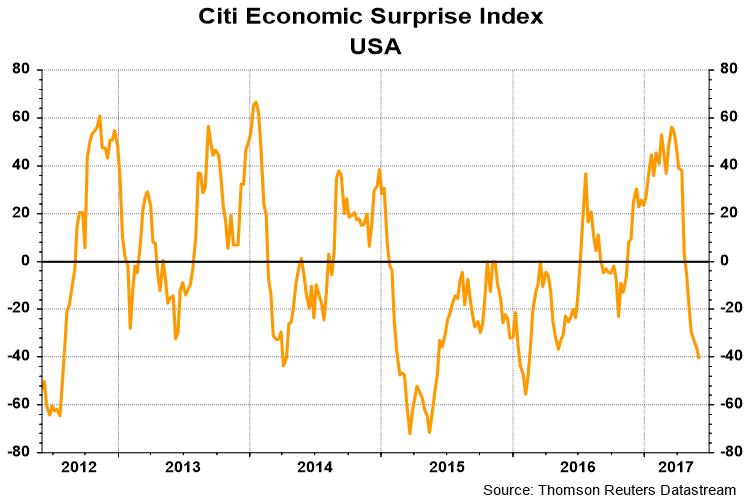

The FOMC’s June statement is likely to feature an interpretation of the current patch of soft economic conditions as being “transitory”. Sure, the Citigroup Economic Surprise Index has been falling, indicating that macro releases have mostly missed market expectations.

Looking around the world, however, the global economy remains robust. At the margin, buoyant non-US economies are likely to provide a boost to the US economic growth. As the chart below shows, a comparison of the SPX and non-US markets show that while the SPX led the rally in weeks after the November election, non-US markets have caught up and have been outperforming since early March. Even if a case could be made that the US equities were rallying because of the anticipation of Trump tax cuts and deregulation, the same argument would not hold for non-US stocks. The Trump trade is dead, but the global reflation trade lives on.

Callum Thomas of Topdown Charts observed that indicators of global trade are rising, which is bullish for growth.

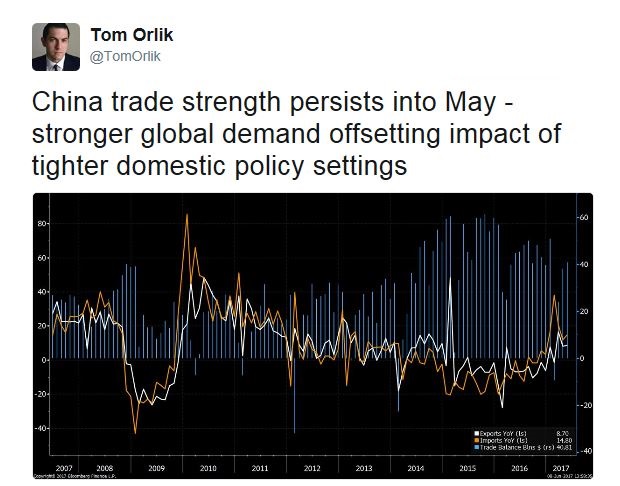

The latest Chinese trade statistics also point to a similar conclusion (via Tom Orlik).

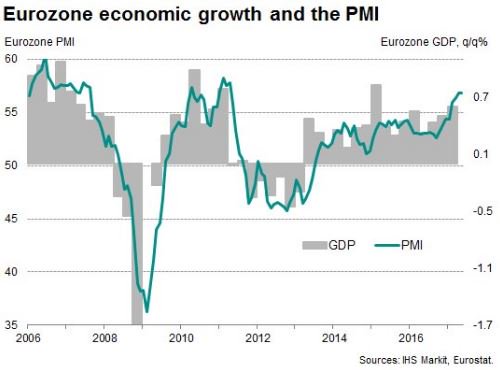

Across the Atlantic, Reuters reported that eurozone growth was revised to the highest rate in two years.

In short, while US economic conditions may appear to be a bit soft, but the global outlook is strong. In the absence of strong evidence to the contrary, the Fed should continue on its path of monetary policy normalization, which translates to three rate hikes this year and the initiation of balance sheet reduction in either late 2017 or early 2018.

Here comes the new Fed governors

So far, what I have described is the most likely outlook of the current Fed, which is likely to change soon. The New York Times reported that Trump is about to nominate Randy Quarles, a former Treasury official in the George W. Bush administration, and Marvin Goodfriend, former Richmond Fed economist and academic, to the Federal Reserve Board of Governors. Bloomberg also reported that Robert Jones, the chairman of a community bank in Indiana, is being considered for a seat on the Fed board (Indiana Jones at the Fed?).

If these nominations do go forward, then it begs the question of who the next Fed chair might be. Any new Fed chair would have to be on the Board of Governors, and there are three vacancies with three potential nominees. We can either interpret the identification of these potential candidates as Trump’s intention to keep Janet Yellen as Fed chair, or her replacement will come from one of the three new governors.

Consider the background and likely jobs of the three candidates for clues to Yellen’s possible replacement. Jones would fill the seat reserved for small bank representation. Quarles’ mandate is likely to be deregulation. By process of elimination, the most likely candidate to replace Janet Yellen is Marvin Goodfriend.

Who is Marvin Goodfriend?

The next question for investors is, “Who is Marvin Goodfriend?” Gavyn Davies recently wrote an endorsement of Goodfriend in the FT, “Marvin Goodfriend would be good for the Fed”, Here is a brief summary:

- Goodfriend’s conservative pedigree goes all the back to Reagan’s Council of Economic Advisors. He is a typical member of his generation…in having a very profound distaste for inflationary monetary policies.

- Goodfriend believes in a formal inflation target, which he thinks should be approved by Congress, rather than being set entirely within the Fed…On the Taylor Rule, Prof Goodfriend has recently argued that the FOMC should explicitly compare its policy actions with the recommendations from such a rule, because this would reduce the tendency to wait too long before tightening policy.

- Goodfriend believes that interest rates are a much more effective instrument for stabilising the economy than quantitative easing.

- Goodfriend has frequently argued forcibly against allowing an “independent” central bank to buy private sector securities such as mortgage-backed bonds, which he deems to be “credit policy”.

- Goodfriend has always been worried that “independent” central banks will develop a chronic tendency to tighten monetary policy too late in the expansion phase of the cycle.

In other words, Goodfriend has the academic credentials and ticks off all the boxes to be a good Republican Fed chair.

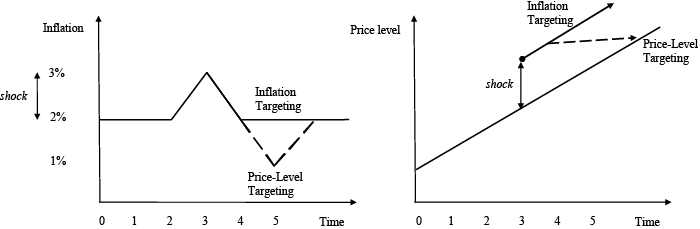

I believe that the most important difference between Goodfriend and the current Fed is Goodfriend seems to favor price level targeting, instead of inflation targeting. Here is one explanation of the difference of the two approaches:

The main difference between inflation targeting and price-level targeting is the consequence of missing the target.

- Unanticipated shocks to inflation lead to corrective action when the price is the target.

- Under inflation targeting, past mistakes and shocks are treated as ‘bygones’.

If, for example, inflation is unexpectedly high today, this would be followed in the future by below average inflation under a price-level targeting regime. By contrast, inflation targeting aims for average (i.e. on-target) inflation in future years regardless of the level of current inflation.

Once you adopt a price level target, you try to play catch-up if you undershoot or overshoot inflation. Even with rates so low, Goodfriend doesn’t believe that the zero bound is a problem for central bankers. He presented a paper at the Fed’s 2016 Jackson Hole symposium with an unusual proposal to drive interest rates to highly negative levels:

The zero bound encumbrance on interest rate policy could be eliminated completely and expeditiously by discontinuing the central bank defense of the par deposit price of paper currency. The central bank would still stand ready to exchange bank reserves and commercial bank deposits at par; and it could stand ready to convert different denominations of paper currency at par. However, the central bank would no longer let the outstanding stock of paper currency vary elastically to accommodate the deposit demand for paper currency at par.

Instead the central bank could grow the aggregate stock of paper currency according to a rule designed to make the deposit price of paper currency fluctuate around par over time. The paper currency growth rule would utilize: i) historical evidence relating currency demand to GDP, ii) the estimated interest opportunity cost sensitivity of the demand for currency relative to GDP, and iii) the GDP growth rate.

In other words, a dollar doesn’t have to be worth a dollar anymore under a Goodfriend Fed. FT Alphaville also reported that Goodfriend thinks that the Fed’s reaction function should be more decisive as a way of demonstrating the central bank’s credibility:

We recently had the chance to chat with a former student who was in Goodfriend’s spring 2015 business school class on monetary policy. (We attempted to contact Goodfriend to confirm the recollection of the former student but have yet to get a response.)

Goodfriend repeatedly spoke about the importance of a public and legally-binding inflation target. In his view, the current “longer-run goal” for inflation is too mealy-mouthed.

Moreover, it lacks legislative authority. Current law instructs the Fed to promote “stable prices” and “maximum employment” without defining either term. Unelected policymakers get to interpret their mandate as they see fit. They also have considerable leeway to change their interpretations on a whim. (This includes ignoring the third part of the Fed’s legal mandate, which is to promote “moderate long-term interest rates.)

In Goodfriend’s view, all this weakens the Fed’s credibility and partly explains the slow rate of inflation since the downturn.

The 2015 episode is a good example of a Fed policy error, according to Goodfriend [emphasis added]:

Goodfriend was also sceptical of the Fed’s decision to begin raising interest rates in 2015, when inflation was weak — even excluding commodities — and nothing indicated it would quickly return to 2 per cent. According to this former student, Goodfriend believed the Fed should make its moves over relatively short periods of time. Thus the 1994-5 tightening was close to ideal because it quickly recalibrated the level of short-term interest rates from 3 per cent to 5.25 per cent. (With an overshoot to 6 per cent in the middle, but still…)

The former student recalls Goodfriend saying that if the Fed were to raise interest rates in 2015 it would probably have to wait a long time before any additional rate increases, which would damage the Fed’s credibility and potentially worsen the downtrend in inflation expectations. That’s more or less exactly what happened. According to this student’s account, Goodfriend would have preferred the Fed waited until it could commit to a relatively short and uninterrupted campaign of “normalisation”.

The view that the Fed should move quickly and decisively and “commit to a relatively short and uninterrupted campaign” clashes with the general accepted wisdom of a gradual approach to changes in monetary policy. Consider this recent “docking the boat” metaphor voiced by San Francisco Fed president John Williams, who has been one of the more hawkish voices on the FOMC board:

When you’re docking a boat, you don’t run it in fast towards shore and hope you can reverse the engine hard later on. That looks cool in a James Bond movie, but in the real world it relies on everything going perfectly and can easily run afoul. Instead, the cardinal rule of docking is: Never approach a dock any faster than you’re willing to hit it. Similarly, in achieving sustainable growth, it is better to close in on the target carefully and avoid substantial overshooting.

Great! We will get both Indiana Jones and James Bond at the Fed.

A more hawkish and activist Fed: What dual mandate?

In short, should the all three rumored candidates be nominated and appointed to the Fed’s Board of Governors, the direction of monetary policy will change quite dramatically, possibly as soon as Q4 2017. At a minimum, the Fed is likely to get more hawkish. Quarles has stated that he favors a rules-based approach to monetary policy, and any rules based model is sure to set a Fed Funds target that is significantly higher than what rates are today. Marvin Goodfriend said in a March 2017 interview that he believes that the Fed is behind the curve.

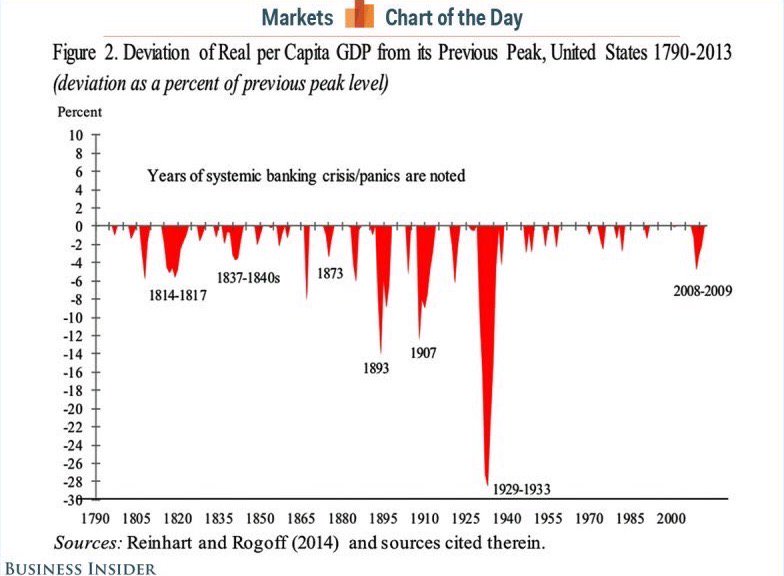

The approach advocated by both Quarles and Goodfriend of a singular devotion to a explicit rules-based monetary policy also implies a downgrade of the Fed’s attention to the other half of its dual mandate of full employment. Moreover, should the Fed adopt Goodfriend’s “relatively short and uninterrupted campaign” tactic to monetary policy normalization, then the likely outcome is a more volatile growth path for the economy. The bigger risk is the economy will experience more frequent and deeper recessions and panics, much like the way it did during the 19th Century.

The current market environment features a high level of stock-bond correlation, which is an indication of complacency. In the past, such environments have been resolved with market disruptions, though not all of which were equity unfriendly.

Add in Marvin Goodfriend’s decisive and activist approach to monetary policy to the mix, the risk of a volatility spike over the next few years rises significantly. And none of that has discounted by the markets.

Market potholes in late 2017?

Despite these possible bearish outcomes for the market, the possibility of changes in Fed policy is really a H2 2017 investment story. The Trump administration has not officially nominated any of these candidates yet. Relax!

For now, US economic policy uncertainty is low by historical standards.

The latest update from Barron’s of insider activity shows that these “smart investors” remain buyers of their companies equities.

Wall Street continues to revise earnings estimates upwards, according to Factset.

The current positive fundamental backdrop is a sign that the intermediate term trend for stocks is still up, and any pullbacks should be relatively shallow.

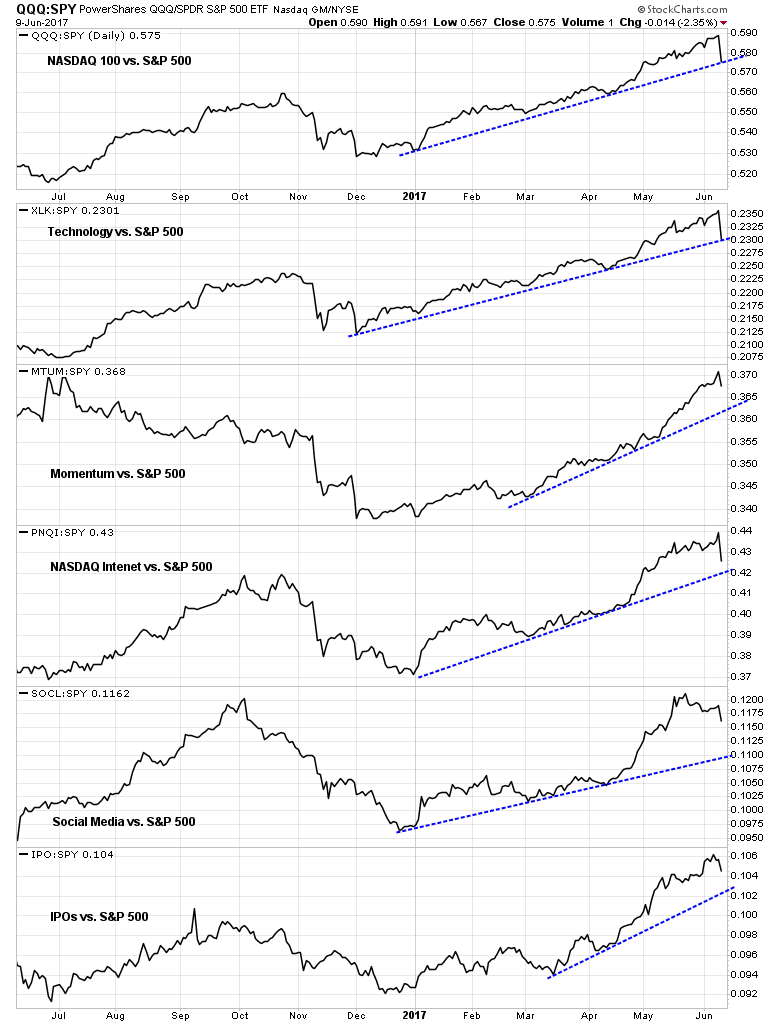

Interpreting the NASDAQ break

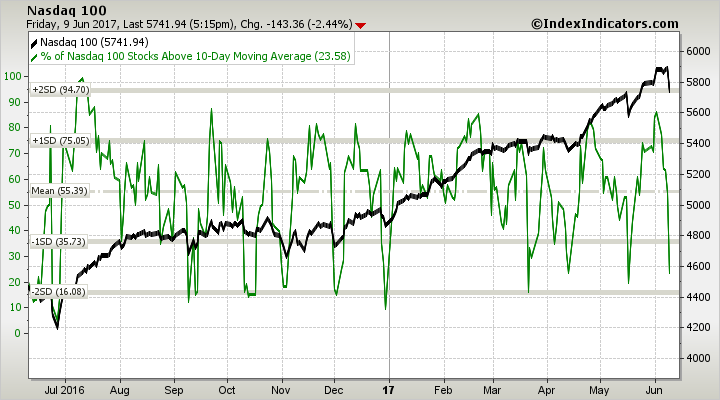

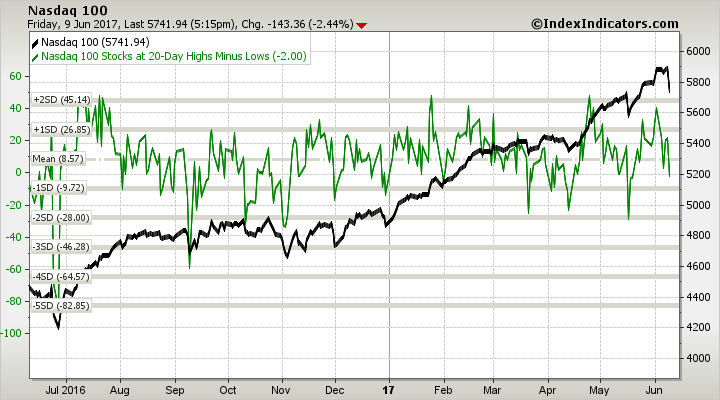

In the short-term, however, the downside break in Technology and NASDAQ stocks on Friday caught almost everyone by surprise. The decline had occurred on high volume, though NASDAQ TRIN did not reach 2, which would be indicative of downside capitulation. The break was not a big surprise from a technical perspective as the NASDAQ Advance-Decline Line had been moving sideways even as the index advanced.

It is unclear whether the downside break is a correction in an uptrend, the start of a correction, or just a sector rotation featuring a sideways consolidation of the other major averages. The weakness was evident in all Technology and high-beta momentum stocks. However, the relative uptrends of these groups all remain intact, though the NASDAQ 100 and Technology groups retreated to test their trend lines.

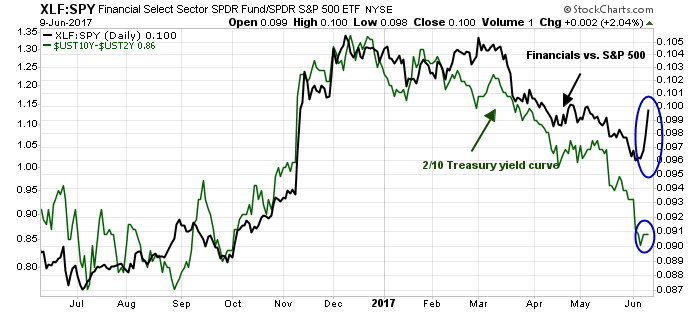

Some of the funds that left the high flyers went into other sectors, such as Financials. This sector also benefited from the early signs of a steepening yield curve.

Some of the logical leaders a sector rotation scenario would be capital goods intensive Industrials and other cyclicals. However, the jury is still out on these groups. Industrial stocks (top panel) remain range bound relative to the market, though they did stage a rally on Friday. By contrast, European industrial stocks have been in a relative uptrend for most of this year. On the other hand, the DJ Transports did not rally on Friday, though they appear to be tracing out a bottoming formation relative to the DJIA. While Friday`s action in the Industrials are supportive of leadership rotation into cyclical stocks, the behavior of the DJ Transports do not.

Short-term breadth charts from Index Indicators show that NASDAQ stocks to be oversold (though oversold markets can get more oversold).

On the other hand, longer term (1-2 week) indicators have only retreated to neutral.

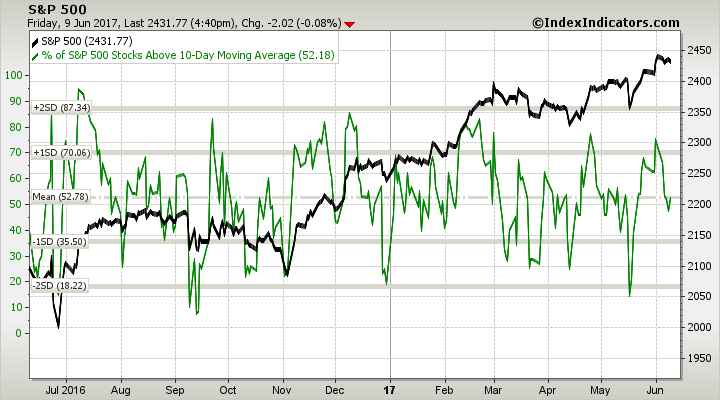

Similar indicators for the SPX are only showing mixed readings. The % of stocks above their 10 dma are neutral.

Net 20 day highs-lows for SPX stocks is neither overbought or oversold.

Bottom line, we need further evidence before declaring Friday`s Tech break to be either the start of a general market correction, a pause in an uptrend for high beta stocks, or the start of an internal rotation into other sectors.

The week ahead

Looking to the week ahead, the most obvious potential market moving event is the FOMC meeting on Wednesday. Urban Carmel observed (N=3) that the past three FOMC meetings where the Fed has raised interest rates has seen flat to down stock markets, and falling 10-year yields, which imply a flatter yield curve that is a signal of slower economic growth.

Next week is also June option expiry. As Rob Hanna at Quantifiable Edges showed, The seasonal bias for June OpEx has been weak compared to other OpEx weeks.

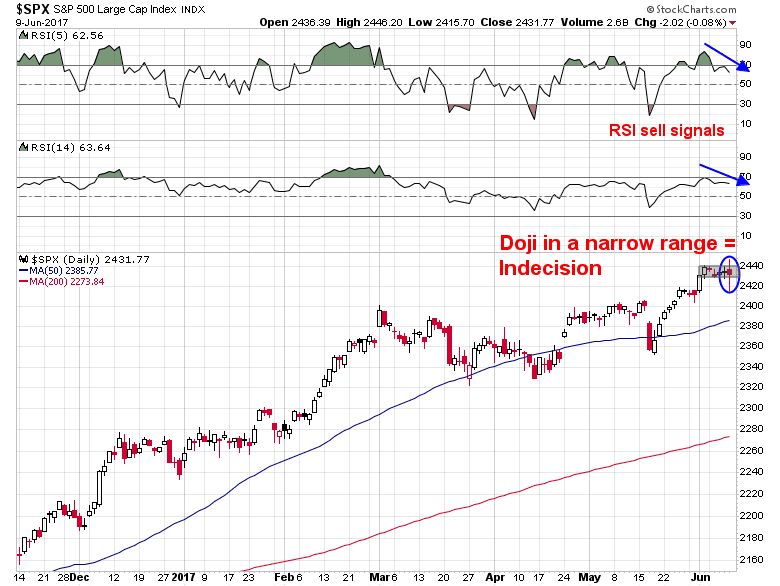

The SPX remains range bound, and Friday`s doji like candle is indicative of market indecision. Both the 5 and 14 day RSI flashed sell signals last week, and I indicated that the market may be setting up for a volatility spike (see A possible volatility spike ahead). While I still have an open mind to all possibilities, the short-term bias is to the downside, with likely support at about the 50 dma level at about the 2380-2390 level.

My inner investor remains constructive on equities. My inner trader still has a small short position in small cap stocks.

Disclosure: Long TZA

Do we really have confidence in the “rules” that would determine Fed policy? Given the changing economic and political realities aren’t the findings of economic research at best “guidelines”.

So, as the “rules based policies” take hold and fed fund rates approach “normality” what happens to the rest of the yield curve? One could make a case for significant and deep corrections in assets like stocks, causing longer term bonds to rally and inversion of yield curve. I am reading a book that references the 1973-74 bear market. The stock market correction of 1973-74 is well known, little did I know that long term bonds also lost a lot (about 28%; yes, inflation was 11% then). I am not entirely sure if long term bonds would also not see a sell off this time, if the “rules based fed” rapidly normalizes interest rate policy. I suppose, bonds at current levels are absurdly priced and there may be a greater probability of big sell off (rather than a further rally) in longer dated bonds as well, under the scenario, much like the 1973-74 bear market.

What is different here as compared to 1973-74 is that we are in a much more globalized markets and as the fed funds “normalize” difference between German bunds and Yen based scrips may tilt the balance towards money flowing into $ bonds, causing rallies in long dated US bonds. Any ideas?

History doesn’t repeat, it rhymes. It’s hard to tell what might happen this cycle, but given the stress points in the three major economic blocs (US, Europe, China), USD assets are likely to be the safe haven in the next crisis.

A significant thing is happening with global trade. With America turning inward away from free trade there was a fear that other countries would build barriers too just like the 1930’s that deepened the Depression. But no, instead we are seeing them quickly renew their commitment. The new free trade leaders are China and Germany. This is an excellent thing for long term global economic growth and global stock markets. How it works for US based companies and their economy is a question mark. They could lag instead of lead.

Lacy Hunt the genius fixed income guru believes society is so overly indebted that even small rate increases will send the economy into a tailspin with long term bond rates plunging afterwards. Truth is that he has been amazingly right at every turn in the bond make for years.

If he’s right then a rules based rapid jacking up of rates would be a disaster.

This is an absolute no brainer. Morphine of free money has buoyed all asset classes (Farmland, US stocks, art work, FAANG stocks, bank stocks, global bonds, gold, etc.). Unemployment rate has also come down since 2008. A contracting fed balance sheet and rise of fed fund rates would likely have a negative effect, depending on the rate of rise of fed funds rates. What Lacy Hunt has indicated is pretty obvious. We are all staring at that abyss.

Note on gold: Yes, gold is down from a peak of 2011 by 40%, but it is up 425% since bottom of 1999, when it was around 266 $ an oz, give or take (today around 1260$ give or take).

Cam: It is very bad form to mock someone’s name – e.g., “Indiana Jones at the Fed”. You are – or should be – better than that.

Suggesting that a rules-based monetary policy (a) ignores the Fed’s full employment mandate and (b) will result in a more volatile growth path for the economy with more frequent and deeper recessions has a fatal flaw in the premise. That is, it assumes the Fed alone has responsibility for the economy. It does not. That various administrations and legislatures have largely abdicated their responsibility and through the “full employment” mandate foisted such responsibilities on the Fed does not excuse any of them.

As a fully engaged bureaucracy the Fed eagerly – too eagerly – accepted the full employment mandate as a means to enhance its powers and broaden the scope of its control over the economy. By eagerly accepting this mandate the Fed effectively absolves the elected government from any responsibility to do its job in the fiscal, tax and regulatory areas. Our system of government depends on the Administration and Legislature to do their job else the voters should do theirs.

I welcome a rules-based monetary policy and hope that it marks the high water event of Fed power and control. There may have been numerous recessions in the 19th century but note that the worst one occurred AFTER the Fed was established. Further, if the Fed is NOT reined in there is a strong probability that such economic volatility will increase as it has so far in the 21st century economy as a more political Fed ebbs and flows its policy tides.

If “a rules based rapid jacking up of rates would be a disaster” then what alternative is there? Ignore the imbalances ZIRP has created? Accept negative interest rates? At what point do we make the effort to normalize our economy and interest rates? Never? When interest rates are held at artificially low levels how do we realistically value assets?

Is there any reasonable economic basis to assume ZIRP and quantitative easing are a positive long term economic policy?