Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Model is an asset allocation model which applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. In essence, it seeks to answer the question, “Is the trend in the global economy expansion (bullish) or contraction (bearish)?”

My inner trader uses the trading component of the Trend Model to look for changes in the direction of the main Trend Model signal. A bullish Trend Model signal that gets less bullish is a trading “sell” signal. Conversely, a bearish Trend Model signal that gets less bearish is a trading “buy” signal. The history of actual out-of-sample (not backtested) signals of the trading model are shown by the arrows in the chart below. Past trading of the trading model has shown turnover rates of about 200% per month.

The latest signals of each model are as follows:

- Ultimate market timing model: Buy equities

- Trend Model signal: Risk-on

- Trading model: Bullish

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers will also receive email notices of any changes in my trading portfolio.

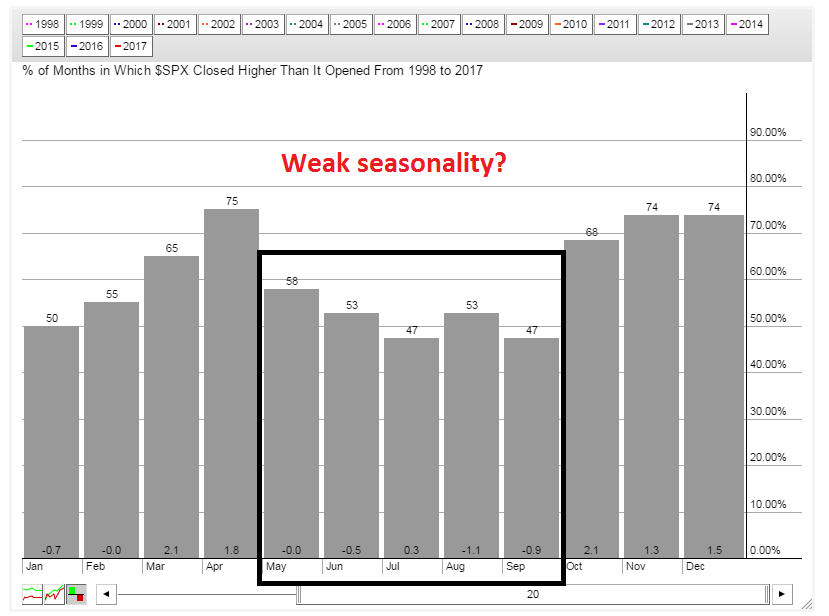

Sell in May?

The adage “sell in May and go away” has been well known to traders for many years. Indeed, the chart below shows that the stock market is entering a period of weak seasonality.

Should investors heed the cautious seasonal signal and avoid stocks? Let’s consider the bull and bear cases before making a decision.

A solid earnings growth outlook

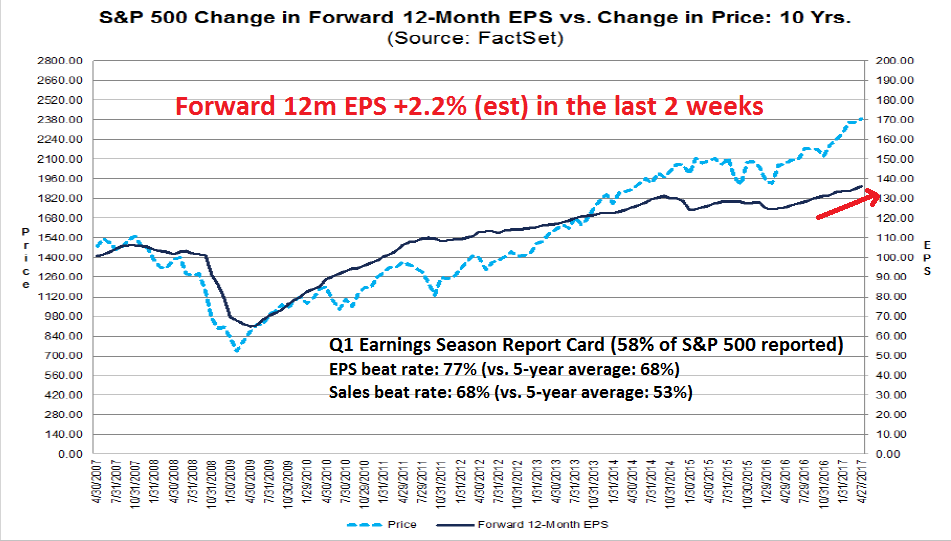

Earnings and earnings growth is one of the key drivers of stock prices. Q1 Earnings Season has shown solid results so far. The latest update from Factset shows that both the EPS and sales beat rates are well above average. As well, forward 12-month EPS estimates continue to rise, which reflect continued Wall Street optimism about the earnings outlook (chart annotations are mine).

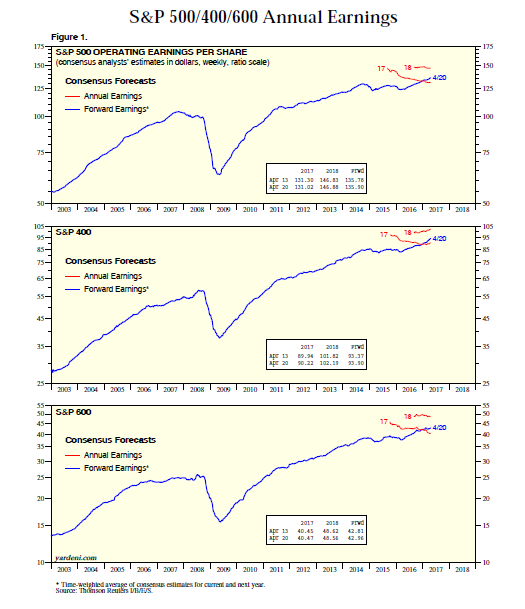

Additional analysis from Ed Yardeni shows that forward EPS is rising across the board for large, medium, and small cap companies in a broad-based advance in fundamental outlook.

What about the Q1 GDP miss last Friday? How can we resolve a picture of upbeat Wall Street earnings expectations with the disappointment in Q1 GDP growth?

Don’t be so sure about economic weakness. 1Q real GDP rose 1.9% YoY. 1Q final sales, which is GDP growth after stripping out inventory adjustments, grew 2.1%, indicating few signs of growth deceleration and little deviation from trend.

Q1 GDP has shown a history of missing expectations. The problem is “residual seasonality”, which is an issue that the BEA is aware of and addressing.

Possible fiscal tailwinds

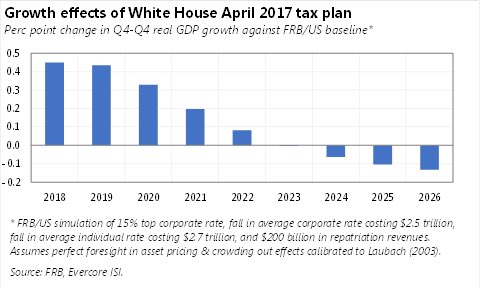

Another possible tailwind for equity prices come from the long awaited tax cuts promised by Candidate Trump during his election campaign. The Trump White House presented an outline of its plan for tax reform last week. While Wall Street largely scoffed at the likelihood of its enactment, I regard the equity risk/reward from the tax plan as one-sided. At worse, it won’t get enacted and the effects will be neutral. At best, its implementation will show some upside for equity prices.

Evercore/ISI ran the plan through the Fed’s macro model and found that the plan would boost economic growth by about 0.5% in the early years but the effects gradually decline and go negative as time goes on.

To be sure, the Trump administration’s record of enacting legislation has been less than stellar. The latest “tax reform” proposal should therefore be regarded as nothing more than the opening offer in multiple rounds of bargaining with the GOP caucus. Should a tax reform be enacted, the most likely case would be some form of standard Republican tax cut package with little or minimal levels of tax increases.

With that scenario in mind, this analysis from Citi Research of the GOP House and Trump proposals puts the negotiations into some context. Notwithstanding the inevitable horse trading that will occur, the easiest and most likely proposal to be enacted will be an offshore cash repatriation tax holiday (annotations in red are mine).

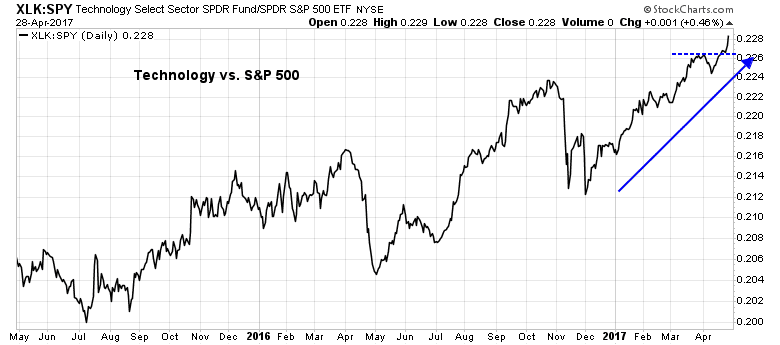

The most obvious beneficiary of such a proposal are Technology stocks. The two biggest stocks in the NASDAQ 100 account for 20% of index weight are APPL and MSFT, both of which are cash rich and would benefit from an offshore cash repatriation tax holiday. As another example of the possible benefit from this tax provision, CNBC reported that Credit Suisse double upgraded CSCO from underperform to outperform and raised the price target from $27 to $40 based on the offshore cash repatriation proposal.

As the chart below shows, the technology sector has been outperforming the market. While the relative advance appears to be a little extended in the short run, the sector should continue to be market leaders as the Trump tax reform proposals evolve.

The bear case

While the bull case consists mainly of an upbeat growth outlook and possible fiscal tailwinds, investors should not ignore possible bearish catalysts:

- A China deleveraging slowdown

- Hawkish monetary policy

Chinese curbs on financial risk

Regular readers know that my analytical approach has been global in nature. I use a framework of analyzing the health of the three major trade blocs, namely the US, Europe, and China. As I have already outlined, the US growth outlook remains upbeat. The results of the first round of the French election has taken much of the political tail-risk off the table in Europe. The one possible growth blemish comes from China.

The Chinese stock market has been weakening as a result of Beijing’s curbs on financial risk. Bloomberg reported that Beijing is employing a multi-dimension approach of regulatory oversight and heightened corruption scrutiny:

Maintaining financial safety is “strategically important” to the country’s economic and social development, Xi said at a meeting of the Communist Party Politburo Tuesday, according to the official Xinhua News Agency. It was a rare occasion for the top policy making body to discuss a specific topic. Officials who attended the group study included the central bank governor and chiefs of the nation’s market watchdogs.

The statement came just as the country’s top leaders said at a separate meeting on Tuesday that they will improve financial support for the real economy, while also stressing preventing financial risks. Chinese banks are pulling back $1.7 trillion source of inflows in response to a series of regulatory guidelines over the past three weeks that put a spotlight on the risks, helping erasing stock market value and sending bond yields to the highest level in near two years.

The government is seeking to reduce financial-system risk by tightening the screws on leverage. The banking regulator said late last week it will intensify steps against irregularities in the financial sector, echoing comments by the securities watchdog just days earlier, while the top insurance official is being investigated on suspicion of “severe” disciplinary violations.

So far, the fallout from the regulatory crackdown appears to be contained within China itself. The chart below of the Chinese stock market and the stock markets of China’s major Asian trading partners tell the story. While the Shanghai Composite (top panel) has been falling and it is now testing its 200 day moving average (dma), the stock indices of the other Asian market look healthy. All are trading above their 50 dma. Hong Kong’s Hang Seng Index has rallied to test new highs. Of particular note is the South Korean KOSPI, which has been strengthening and reflects minimal anxiety over geopolitical tensions with North Korea.

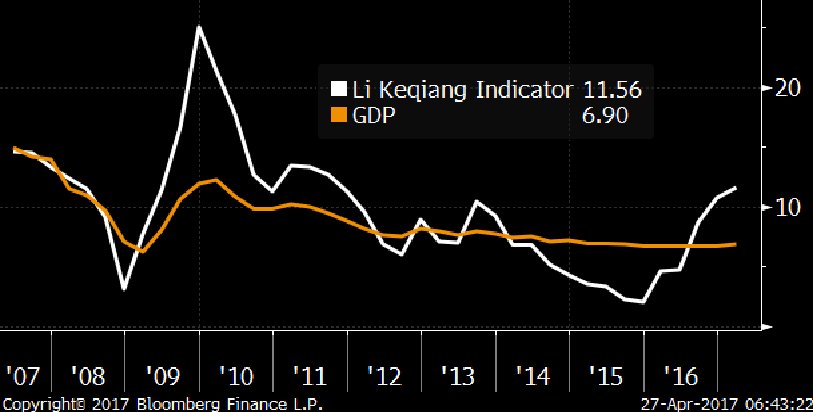

In addition, Chinese economic growth is going like gangbusters. The Li Keqiang Index is 11.6%, which is the greatest level of strength since Li became the Premier of China. For readers unfamiliar with the index, Wikipedia explained it this way: “According to a State Department memo (released by WikiLeaks), Li Keqiang (then the Party Committee Secretary of Liaoning) told a US ambassador in 2007 that the GDP figures in Liaoning were unreliable and that he himself used three other indicators: the railway cargo volume, electricity consumption and loans disbursed by banks.”

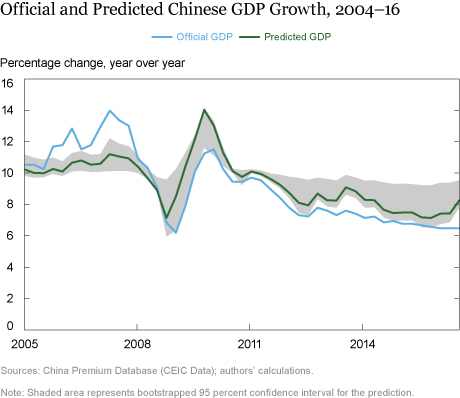

Staff economists at the New York Fed confirmed the story of Chinese economic strength in an unusual way. It conducted a study of Chinese economic growth based on the brightness of night lights using satellite data. They concluded that Chinese growth has not been overstated, but understated.

Bottom line: Investors should relax, China is not crashing. The authorities will take every step to minimize tail-risk ahead of the Party Congress this fall.

What about the Fed?

Recently, the perennially cautious John Mauldin featured analysis from the equally cautious Lacy Hunt and Van Hoisington about the risks posed by the Fed’s tightening cycle. Hunt and Hoisington warned that the “last ten cycles of tightening all triggered financial crises”:

Four important considerations exist today that were not present in past cycles and that may magnify the current restraining actions of the Federal Reserve:

1. The Fed has initiated a tightening cycle at a time when significant differences exist in the initial conditions compared to the initial conditions in prior cycles. Additionally, the Fed is tightening into a deteriorating economy with last year’s growth in nominal GDP worse than in any of the prior fourteen cases.

2. Business and government balance sheets are burdened with record amounts of debt. This means that small changes in interest rates may have an outsized impact on investment and spending decisions.

3. Previous Federal Reserve experiments, primarily the periods of quantitative easings, have led to an unprecedented balance sheet (an action of “grand design”) to which the economy has grown accustomed. The resulting reduction in that balance sheet (reduction in the monetary base) may have a more profound impact on growth than anticipated.

4. The monetary base reduction and the impact of the changing regulatory landscape, both in the U.S. and globally, has meant a significant increase in the amount of liquid reserves that banks are required to hold. Liquidity may have already been sharply restrained by the lowering of the monetary base, despite its massive $3.8 trillion size. This is evident as the monetary and credit aggregates are following the expected deteriorating pattern resulting from monetary restraint, suggesting recessionary conditions may lie ahead.

The Fed seems dead set on tightening monetary policy. In a past post, I had pointed out that Fed watcher Tim Duy and award winning economic forecaster Jim O’Sullivan believe that the Fed is likely to look through any Q1 weakness and continue on its tightening path (see Will the real Q1 GDP please stand up?).

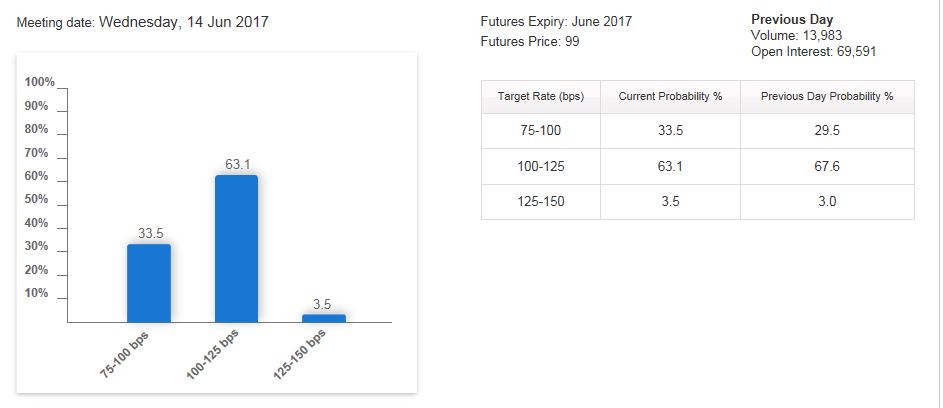

Indeed, as the FOMC prepares meets next week, the market expects the Fed to stand pat. The latest markets expectations from the CME shows only a 5% of a May rate hike and an about two-thirds chance of a June hike.

More revealing will be the tone of the language in the FOMC statement. Despite the soft Q1 GDP figure, one of the key indicators to watch will be core PCE inflation which is due for release on Monday. Core PCE is the Fed’s preferred inflation metric and its progress will be an important input into monetary policy. Last Friday’s GDP release also saw the Employment Cost Index rise 0.8% in the quarter, which was ahead of expectations and shows growing wage pressure. As well, the Employment Report due Friday, which is after the FOMC meeting, will also play a key role in the determination of interest rate policy.

For the time being, I agree with Tim Duy when he wrote in Bloomberg that both the stock and bond markets can be right:

Equities have renewed their rally — and so have bonds, and that is creating much alarm among some investors. Whereas the former suggests the stage is set for solid growth, the latter and the accompanying narrowing of the yield curve raises red flags about the health of the economy. I am not sure there is much of a puzzle here. This dichotomy is fairly typical of a monetary tightening cycle and can exist for a long time. How long? Until the Federal Reserve finally snuffs out the expansion with excessively tight monetary policy.

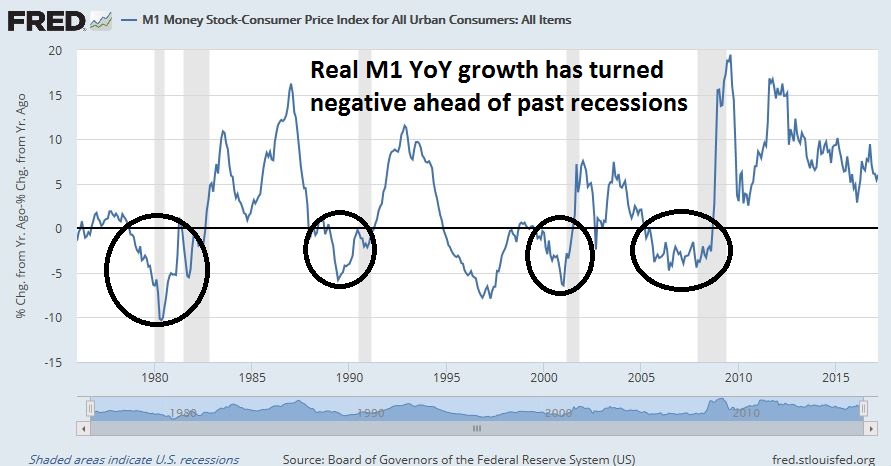

For investors, the trick is to spot the inflection point when the Fed “snuffs out the expansion with excessively tight monetary policy”. One indicator that can be used to proxy the degree of accommodation in monetary policy is real M1 growth, which has tended to turn down before recessions. As the chart below shows, real M1 growth is decelerating, but it is far from the overly restrictive danger zone (for now).

If the Fed were to stay on its current course of two more rate hikes this year, recession risk is unlikely to rise significantly until late 2017. Since the markets are forward looking, that implies a cyclical market top at about the same time, with the caveat that this forecast is “data dependent”.

Until then, the equity party is still going. Enjoy!

A breadth thrust failure?

Turning to the technical outlook, I identified a possible bullish setup in my last post in the form of a breadth thrust that had until a deadline of last Friday’s close to flash a buy signal (see Just overbought, or a “good overbought”?). Unfortunately for the bulls, the buy signal did not materialize, but that failure does not necessarily instantly translate into a sell signal.

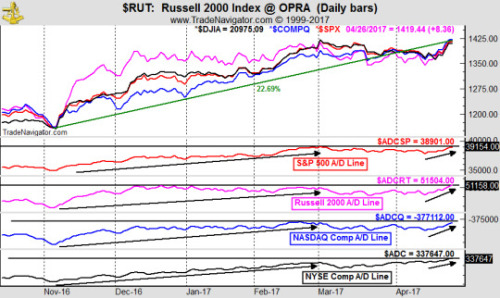

Market internals remain supportive of higher prices. Jeff Hirsch of the Stock Trader’s Almanac has gone against this year’s “sell in May” seasonal bias by issuing a buy signal based on improving breadth:

Well, patience with our Best Six Months Seasonal MACD Sell Signal has sure proved to be a virtue thus far. Both MACD indicators for both the S&P 500 and DJIA went negative in early March and did not all turn positive until the past Monday’s big gains. Now we are getting some bullish confirmation from market breadth. The cumulative Advance/Declines in several major market indices are trending higher and on the brink of more new highs.

This weekly chart of the NYSE McClellan Summation Index (NYSI) shows that it bottomed five weeks ago after flashing an oversold reading. The NYSI is rising again and it is far from overbought, which indicates further room for an intermediate term advance.

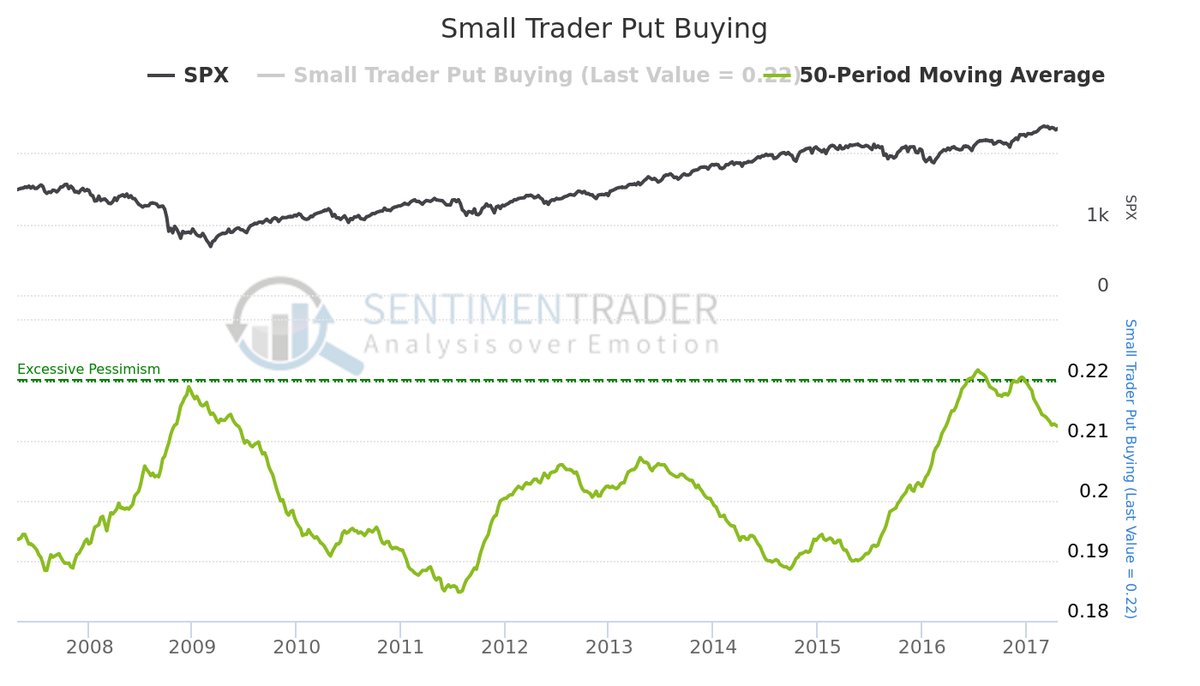

As well, Sentiment Trader pointed out that small option traders (the “dumb money”) has been buying put options at levels consistent with past market bottoms.

Lastly, analysis from Eric Parnell shows that a “sell in May” strategy would have given the trader little or no edge in the post-crisis era.

Instead of wondering whether to sell in May and go away, I would prefer to stay long in May and play.

The week ahead

Looking to the week ahead, there is plenty of potential from event driven volatility. In addition to the key macro releases like PCE inflation and ISM on Monday, the FOMC meeting announcement on Wednesday, and the Jobs Report on Friday, a number of index heavyweights will be reporting earnings results. These include trading favorites like AAPL (Tuesday) and FB (Wednesday). As well, the second round of the French election is scheduled for May 7.

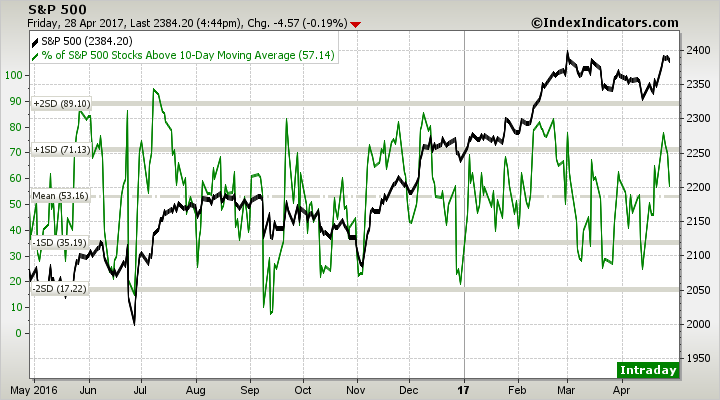

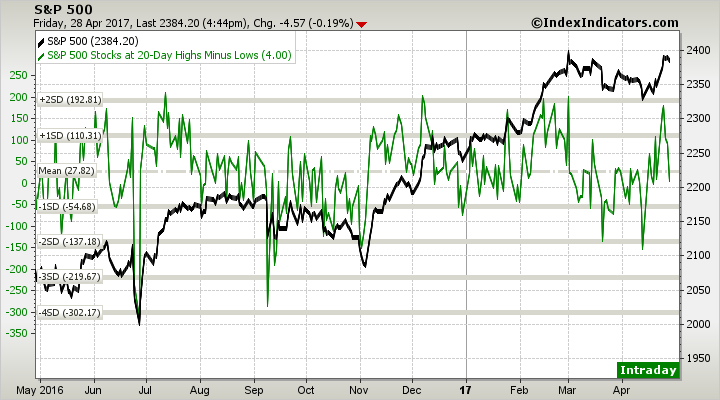

From a technical perspective, the failure of the SPX to punch through technical resistance was a setback for the bulls. However, breadth charts from Index Indicators show that the market has already retreated from overbought levels to neutral, which suggests that either the pullback has already occurred, or further corrections are likely to be shallow.

This chart of net 20 day highs-lows, which tends to have a 1-2 week trading time horizon, tells a similar story of a pullback from overbought conditions to a neutral reading.

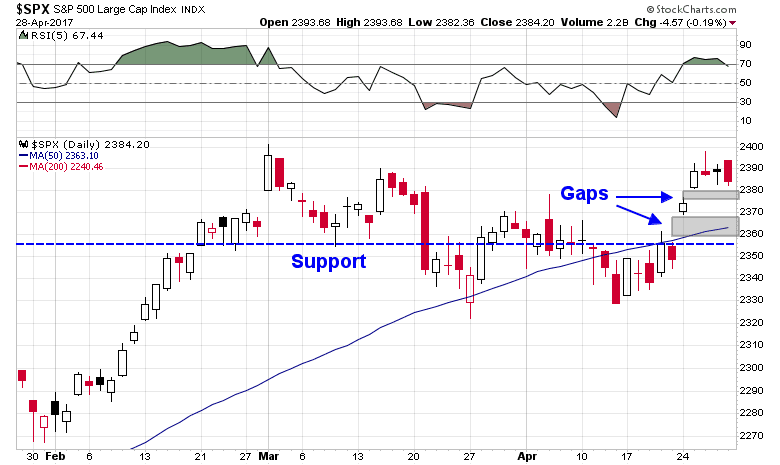

If the SPX were to weaken, look for the gaps to be filled. Initial support can be found at the 50 dma at about the 2360 level, which represents downside risk of less than 2%.

My inner investor remains bullishly positioned. The intermediate term outlook remains positive and he is not worried about minor downside blips of 2% or less.

My inner trader remains long the market, with a tilt towards the technology heavy NASDAQ stocks.

Disclosure: Long SPXL, TQQQ

Money managers have recorded the worst relative performance in history versus the market averages in the last five years. In my opinion, it is because they had a previous history of success and are using that experience in a business, monetary and economic that no longer returns to previous means. Retailers are not just down because of temporary factors and soon to recover like the old cycles. No, the internet is killing them and those that don’t adapt will fail. Oil prices aren’t just down due to temporary supply/demand problems. No technology has forever changed the finding of oil and electric vehicles are compounding the problems. Money managers have a history of success with Walmart and Exxon, both great, well managed companies but will they or their industries return to previous norms, no.

The same with analyzing monetary policy. Richard Fisher, Dallas Fed President said in 2012 (I have it taped to my computer), “… we are sailing into uncharted waters. And nobody – in fact no central bank anywhere in the planet – has the experience of successfully navigating a return home from a place we now find ourselves.” These previous great strategists that use old economic relationships to forecast monetary policy are likely going to be humbled just like previously great portfolio managers.

I agree totally with Cam’s assessment of where we are economically at the start of this tightening cycle. Central Bankers will tip-toe around the mountain of global debt not wanting to start an avalanche they can’t stop. This is the Moonless world I talk about. The Central Bank is the Moon that used to cause big economic tides where the whole economy would have synchronized booms and recessions. Now they are and will stay basically absent. We are Moonless. This allows industries individually to go through their own business and stock market cycles, like energy in 2014-2016.

We have a test of the Moonless economy theory happening now. The two big interest sensitive sectors, housing and autos, I believe are on separate paths, unlike any other cycle. Autos are peaking since easy money (sub-prime in a big way) has led to above trend sales. The prices of used cars is falling and auto debt delinquencies are rising fast. This will lead to a recession in that industry regardless if and how high interest rates go up or not. On the other hand, home building will likely rise due to rising wages, rising household formation, low mortgage rates and lack of inventory. Let’s see if these two formerly coincident industries go their own ways in a Moonless world.

How does one invest in a Moonless world? Momentum, pure and simple. If you crash landed in the mountains and did not know your way, you would best follow a valley and a river to guide you. In the same way, following those sectors that are outperforming (flowing easily) will lead you through uncharted economic and business conditions.

I agree with Cam about technology. It is outperforming and for good reason. We are in a digital revolution. Plus the border tax which would have been a tech industry disaster (supply chain fiasco) is fading away. Earning estimates are rising. It is a key momentum play.

Rob Hanna of Quantifiable Edges points out that in years when the market does not during the first 4 months of the year experience a 5% drawdown from its January 1 high, then 80% of the time the market is higher on October 31st than it was on April 30.

Tom

Really useful analysis from Cam, Ken and Thomas. Most appreciated.

Cam, any concern that the set up is very similar to what we saw in mid-Sept 2016? Structure of the following four are of concern to me: 1) Zweig Breadth Thrust failure, 2) breadth charts from Index Indicators, 3) SPX MO (akin to $NYMO) and 4) existing negative divergences of MACD & RSI. I think this could easily materialize and the pull back in that case would be > 2% — most likley to $SPX 2300.

Anything is possible, but I can only play the odds. Right now, the weight of the evidence leans bullish.

Here are momentum charts from my book;

NASDAQ ETF (QQQ)

https://product.datastream.com/dscharting/gateway.aspx?guid=9db5b651-0a18-4b88-85ea-0702fba73ba6&action=REFRESH

Technology ETF (XLK)

https://product.datastream.com/dscharting/gateway.aspx?guid=b81df5f0-ef47-466b-8bf5-e967e42e7403&action=REFRESH

There are two charts on each of these. The top one shows the nine month rate of change of the ETF and the S&P 500 and the bottom one shows the difference. The QQQ and XLK are both outperforming the S&P.

Buy my book and get connected to all the best daily updatng industry and country ETF charts plus an explanation of my improved momentum investing strategy.

http://www.thepathway.ca