Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Asset Allocation Model is an asset allocation model that applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. The performance and full details of a model portfolio based on the out-of-sample signals of the Trend Model can bsoe found here.

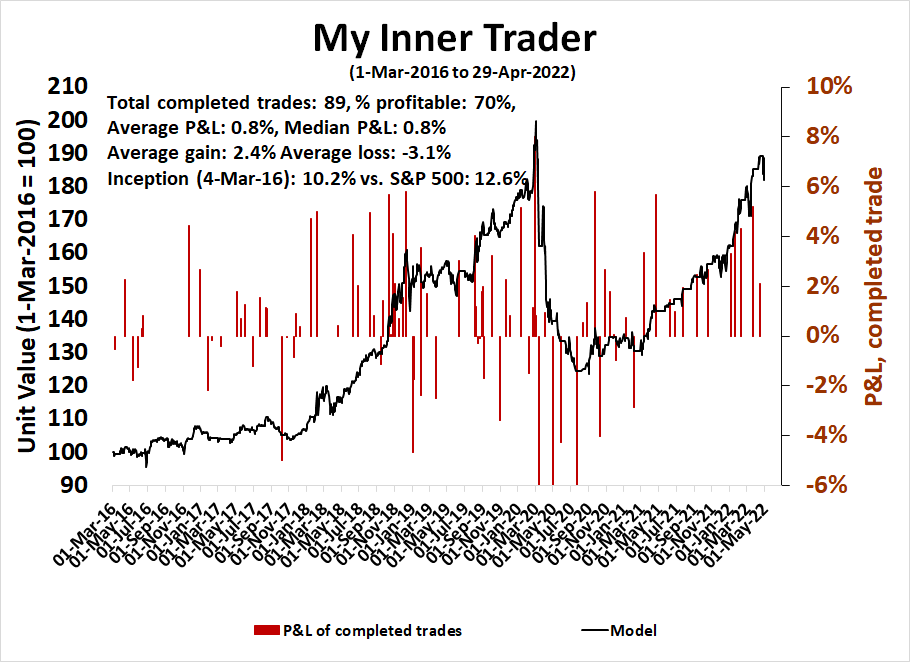

My inner trader uses a trading model, which is a blend of price momentum (is the Trend Model becoming more bullish, or bearish?) and overbought/oversold extremes (don’t buy if the trend is overbought, and vice versa). Subscribers receive real-time alerts of model changes, and a hypothetical trading record of the email alerts is updated weekly here. The hypothetical trading record of the trading model of the real-time alerts that began in March 2016 is shown below.

The latest signals of each model are as follows:

- Ultimate market timing model: Buy equities

- Trend Model signal: Bearish

- Trading model: Bullish

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers receive real-time alerts of trading model changes, and a hypothetical trading record of those email alerts is shown here.

Subscribers can access the latest signal in real-time here.

Another test of the 2022 lows

Here we go again. The S&P 500 tested its 2022 lows on Friday while exhibiting a positive 5-day RSI divergence. Selected sentiment readings are at off-the-charts levels. Both the bond and stock markets are poised for a relief rally, and the FOMC meeting Wednesday could be the catalyst.

A historic sentiment extreme

I recently expressed doubts over the weekly AAII sentiment survey readings, but the latest survey results now finally confirmed a contrarian bullish conclusion. For the third consecutive week, the bull-bear spread remains below -20. Not only has bullish sentiment collapsed in the latest week, but also bearish sentiment spiked to a nearly off-the-charts reading, indicating unbridled panic. Both the bull-bear spread and bearish sentiment have not been this bearish other than the bear market low in 1990 and the generational equity market low in February 2009.

In addition, equity fund flows have tanked to levels last seen during the 2020 COVID Crash, the 2011 Greek Crisis, the 2008 Lehman Crisis, and other major market panic lows.

At a minimum, this is a setup for a tactical stock market rally, though I remain unconvinced that investors have seen the actual low for this market cycle. As we look ahead to the FOMC meeting in the coming week, the market is also setting up for a bond market rally with important implications for stock market leadership.

Stocks vs. bonds

Stock and bond prices have undergone the unusual condition of falling together in 2022. Both stock and bond sentiment are exhibiting excessively bearish readings. A review of the technical and sentiment backdrop leads me to believe that bond prices have greater intermediate upside potential than stocks.

Let’s begin with the equity market outlook. While the AAII sentiment readings appear contrarian bullish, other sentiment models are not confirming similar extremes. The CNN Business Fear & Greed Index is fearful, but conditions are not at panic-driven lows seen in the recent past.

Similarly, the NAAIM Exposure Index, which measures the sentiment of RIAs managing individual investor funds, retreated last week. While readings are below average, indicating minor levels of bearishness, they are nowhere near conditions seen in past washout lows.

To be sure, all four components of my bottom spotting model flashed buy signals within a few days of each other last week.

From an intermediate-term perspective, the S&P 500 has definitively violated neckline of a head and shoulders pattern. This suggests that any relief rally will encounter overhead resistance at about 4310.

From a long-term technical perspective, the percentage of S&P 500 stocks above their 200 dma reached a “good overbought” condition of over 90% in 2020 and recycled below in mid-2021 (top panel). Historically, such declines don’t end until the percentage of S&P 500 above their 50 dma fall to 20% or less (bottom panel). Investors have yet to see that capitulation low.

From a valuation perspective, the S&P 500 is trading at a forward P/E of 18.1, which is constructive. I pointed out recent (see US equity investors are playing with fire) that the last two times the 10-year Treasury yield traded at current levels, the forward P/E ranged from 13.5 to 16, which represents further downside potential from current levels.

In addition, we have not seen the clusters of insider buying that exceed sales that usually mark major market bottoms.

As a reminder, this is the pattern of insider activity during the COVID Crash bottom.

What about bonds?

Turning to the bond market, Ed Clissold of Ned Davis Research observed that bond market sentiment is excessively bearish.

The blogger Macro Charts also confirmed that the 10-year Treasury Note’s Daily Sentiment Index is at a bearish extreme, though DSI can be an inexact timing indicator.

As the market looks ahead to the May FOMC meeting, investors are faced with the unusual condition where the Fed Funds rate has barely budged but the 2-year Treasury yield has skyrocketed in anticipation of a fast tightening cycle.

The market is anticipating a half-point hike in May, followed by a three-quarter point hike in June, and a half-point hike in July, which represent extremely hawkish expectations. In all likelihood, a three-quarter point hike in July may be overly aggressive and any hint of a steady course of half-point moves would be enough to spark a bond market rally.

Watching for confirmation

From a technical perspective, the 7-10 Year Treasury ETF (IEF) appears to be trying to form a bottom, but we have seen similar false starts in the recent past.

Here is what I am watching. If the bond market were to stage a rally from bearish sentiment extremes, watch for confirmation from changes in equity market leadership from inflation hedge groups to interest-sensitive issues.

In addition, falling bond yields would translate into better relative performance for high duration quality large-cap growth stocks such as the NASDAQ 100.

In conclusion, extremes in bearish sentiment in both stocks and bonds are setting up for tactical rallies in both asset classes. Short-term stock market readings are extremely oversold and major downdrafts simply don’t begin under such conditions. My base case scenario calls for better intermediate upside potential from the bond market. The upcoming FOMC meeting is a potential catalyst for the rally.

Strap in and brace yourself.

Disclosure: Long SPXL

I think you have it exactly right for both stocks and bonds Cam. A rally to around 4,300 and down from there. The Fed meeting is a logical catalyst for a tactical rally. The Fed cannot be any more hawkish and even consistent messaging may be met with relief.

This is learned research supporting a tradeable rally coming up. The key here is to look inward and see whether you are keen to buy to take advantage. IMO that would put you on the wrong side of this global scorched earth Central Bank shit-show coming at us with unimaginable unintended consequences. Being on the right side of this would be glee in timing the peak of any sucker’s rally to place downside bets or lighten up long-term positions that you mistakenly left on. Check your perspective.

We are in Investment Winter with no signs of Spring. Unpredictable coming epic negative events are very predictably on the horizon. The global economy is unwinding massive Central Bank overreach and a loss of credibility. Where the cracks will appear is anyone’s guess.

Here is my guess on where the crack will appear: cryptocurrencies.

In early 2000, and elderly couple who were clients of mine wanted to put all of their life savings into a Dot.com mutual fund. Their son worked in Silicon Valley and he said to buy. I refused and said that bubbles were organic things that keep growing until the last buyer is found. In this case, they were the last buyers. They took their account away and that turned out to be the peak.

Last week and elderly wealth client spending the winter in Arizona, was anxious to buy a new crypto-coin that some con artist had created. Same story as the year 2000. He was the last buyer of these chain-letter, Ponzi schemes. There are thousands of fraudulent cryptos made out of thin air that come and go with promoters pocketing the publics money for every Dogecoin that succeeds.

My research assistant has done deep analysis of stablecoins and expects a massive, Lehman-type scandal to expose the fact they aren’t fully backed or even much less backed by dollar assets. As young investors keep losing money they will be cashing in their crypto holdings and the amount of stablecoins will fall. If as I suspect, the pool of dollar assets is low, the day will come when they can’t send out cash when someone wants to redeem. Then the crypto world will have a very bad day that could spill into the real world.

This is an example of what surprises can happen when a bubble pops.

You know when movie and sports stars are pimping easy to use apps to buy crypto that requires “no knowledge” the peak has been reached.

I think the only smart money was made in the pst by folks that harnessed some creative way to mine crypto. I have a friend with a house in Tahoe who bought a bunch of servers to do just that and would only mine in the winter when he could leave his windows open to take advantage of the cold to cool his hot running tech. He made out quite nicely.

Fidelity Investments manages roughly one third of the 401(k) assets in the country. They are now allowing bitcoins in those accounts(if the employer so chooses) of up to 20% – A recent news item and not a fake news.

Is this a step towards Bitcoin becoming a legitimate asset class? Chase, Fidelity and others offer it to their institutional clients as well.

I think it’s more volatile than equities with questionable diversification benefits.

Going to zero? That’s what Charlie Munger said yesterday. You have a wise person in your corner.

The interesting part is always getting the timing right. I think it is well known by now that claims of a stablecoin like Tether being backed by something of real value are very questionable at least. Just think about the Wirecard scandal, the first FT report about fraud emerged January 30th, 2019, but it took almost 15 months until the stock really collapsed and short bets on it would really pay off. Fast forward to today, no one in the crypto world is really paying attention to Buffett and Munger, people do not take these warning serious anymore, just like few people took Dr. Michael Burry’s warnings serious at the beginning of last week.

I do not understand the foundations of the crypto world and just try to follow it from time to time. More than anything, what concerns me is the aftershock of a crypto collapse if there is one. That could be ugly.

Nonetheless, why are giant institutions involved? Is there a systemic risk building up? Would a 3% 10 year Treasury upset the apple cart or just reset the value at which apples are sold?

There are many esteemed people forecasting doom and gloom. Jeremy Grantham for one. Ken on our pages is another. But Rick Rieder of BlackRock thinks we are 90% done.

One has to choose carefully depending on their circumstances and disposition.

Things may look dire right now, but two consecutive weeks of large losses can be liberating for the bulls – in many cases it had been short term bottoms. However in more than a few cases it will keep falling another week or part of the week (eg 2008-10-10 and 3 other weeks that followed).

https://ibi.sandisk.com/action/share/1e2fc78d-6d6c-4499-9b70-8bfec95655da

Simple strategy based on two consecutive weeks of large losses in the $SPX is now posted, same linked folder as above. Do the count properly and you can get similar results. 2007 to 2011 all positive returns. 2009 return was 13.15%. Time in the market 12%, so in a bear market don’t stick around in the long position – not for the faint of heart but not difficult either.

Cam, Which portion of the bond duration yield curve are you expecting to stage a relief rally? Model portfolio has 7-10 year duration treasuries. Stick with that or go longer term like 20+ years?

Thanks

Cam or anyone else,

Everyone is talking about the Fed being very hawkish now. 50bps hikes in the upcoming 3 meetings and then a continuous rise of 25bps, and some QT along the way.

If they are really serious, why wait for the FOMC meeting to raise rates? Why can’t they do one in-between? That will send the markets a very clear, unambiguous message.

May be it is just some jawboning and hoping that some of the supply-chain issues will soften and that inflation will come down somewhat on its own.

If the Fed raises the FFR as the market expects, there will be a recession and possibly more.

The Fed is stuck between a rock and a hard place. What do they focus on? Avoid a recession or tolerate high inflation?

But inflation affects every American while loss of jobs only affects a few unfortunate ones. Which one will you pick if you were a politician in an election year?

There are clearly more votes if you bring inflation control.

Boy, busy page huh?

There are all kinds of reasons for doing things slowly, just like removing bandaids slowly, or sloths getting divorced, but they are rationalizations hiding some other narrative.

What strikes me is the dramatic response of mortgage rates to the .25% bump. One can only imagine what a .5% or .75% bump would do.

Wasn’t the last GDP (real #s) negative?

My take is the Fed will opt for .25% in May, so they talked about .5% but mortgage rates are at 5.375 on a 30year and the UST2Y is at 2.7 when at New Years it was 0.7.

So there are plenty of reasons for the Fed to hem and haw.

I still think it’s a bear trap, this is why sentiment is so bearish in spite of a modest decline, but it could be the last one before the cliff.

We’ll see what happens

Yes, sentiment is clearly in dumps as Cam has said it so well. I think we should see a modest rally in coming weeks as well.

GDP was negative because of weak exports. The US consumer spending is still quite strong. That likely won’t stop the Fed from raising rates.

Cam mentioned yesterday that Dudley wants to kill both the stock and bond markets which will make the Americans feel poor via the wealth effect.

Check out Erza Klein’s podcast interview with Larry Summers.

No place to hide.

Bonds? New ytd lows.

Cash? At 8% inflation? Not exactly a hiding place either.

Gold? Not today.

That leaves stocks. Which may be the contrarian play for now.

Diversification is the best way to survive a bear market.

Apart from the above asset classes, there’s owning a home. Even having a job. Two of the best hedges against price inflation.

Re the ongoing discussion about cryptocurrencies, here’s a true story.

There’s a guy at work who reconnected with a guy he grew up with – someone who married a woman who eventually became a successful banker in LA. Unlike his wife, this guy was stuck in a low-level job and eventually became unemployed. So he started playing with digital coins – and discovered he was pretty good at it. He returned one day from LA to the Bay Area to visit his friends – a low-key guy not inclined to say much about himself. Over the course of several days he revealed that he and wife had recently purchased a large home in LA. A few days later he flew to some place in the southeast to pick up a new McLaren, which he drove back across the country with his son. So I guess he was one of the fortunate early investors. One can only infer how well he did, but as is always the case with these things it’s the early bird that walks away with the loot.

The best advice on a day like this may be to simply remember that it’s not all about the market.

Life goes on.

80% of the folks in the world pay scant attention to the numbers we watch every day.

Too many traders expecting an oversold rally today, which just makes it unlikely.

Here’s my thinking right now.

Every time I’ve been ahead of the SPX by x% and I try to get cute – I end the year behind the SPX.

I’m going to try locking in ~+10% lead over the SPX (and probably a +10% aggregate lead over bonds as well) by avoiding the temptation to

micromanage…