An unusual divergence has appeared between the VIX Index and MOVE, which measures the implied volatility of the bond market. While MOVE has spiked, VIX has fallen.

The difference in the two indicators can be explained by two forces that affect markets today, namely geopolitical risk and macro risk as defined by the Fed cycle. The decline in the VIX and equity rally reflects a compression in geopolitical risk premium in light of constructive Russia-Ukraine discussions, while the elevated nature of the MOVE Index reflects the market’s concerns about the Fed’s tightening cycle.

Here is a framework to consider. In the short-term, geopolitical risk will continue to dominate market volatility. Longer-term, it is the Fed cycle that matters to stock prices.

Longer-term, the key question for equity investors is the evolution of the Fed cycle. There are two schools of thought. The recession school believes that the Fed will keep raising rates until something breaks and the economy goes into recession. The stagflation school believes the Fed is so far behind the curve that Fed actions will only slow the economy without any meaningful effect on inflation.

The recession vs. stagflation call will be the key macro call for equity investors for the coming year. Under a recessionary scenario, investors should be cautious with overweight positions in defensive sectors and market weight high-quality growth stocks in anticipation that the market bids up growth in a growth-scarce environment. Under a stagflation regime, investors should overweight hard asset plays such as energy, mining, agriculture, and real estate as inflation hedges.

A inverted 2s10s yield curve

There seems to be a disagreement between the Fed’s perception of its policy effects and the market’s perception. The 2s10s yield curve has inverted and heightened investor anxiety about a recession in 2023.

In response to the heightened level anxiety, the Fed published a

paper, “(Don’t Fear) The Yield Curve, Reprise”, in order to push aback against the concerns. The paper concluded that the 2s10s yield curve is not a good predictor of recessions. Instead, the near-term forward spread, which is the spread between the 18-month and 3-month Treasury rate, is a much better forecasting tool.

It is not valid to interpret inverted term spreads as independent measures of impending recession. They largely reflect the expectations of market participants. Among various terms spreads to consider, the 2-10 spread offers a particularly muddled view. Especially in the present circumstances when the 2-10 spread is very much out of step with the near-term forward spread, which offers a much more precise view of market expectations over the next year and a half, it is difficult to concoct a reason to be concerned about the flattening of the 2-10 spread. In contrast, if and when the near-term spread does contract, we know that investors will then be expecting a cessation in monetary policy tightening. While such a shift in expectations could well be precipitated by future concerns about a recession, that need not be the case. A more benign cause would be a marked easing in inflation and inflation expectations that allow for a cessation of policy firming.

The following chart shows the different techniques of measuring the yield curve. The blue line depicts the 2s10s yield curve. As FRED does not have an 18-month Treasury rate, I approximated the 18-month rate by interpolating the 1-year and 2-year rates. While the approach isn’t perfect, it serves as a reasonable approximation of the 18-month to 3-month spread (red line). In addition, the green line shows the 10-year to 3-month Treasury spread.

While the 2s10s yield curve is inverted, the other yield curves are still strongly upward sloping. The difference can be explained by the shape of the short end of the yield curve, which is still quite steep.

Callum Thomas also pointed out that the 2s10s yield curve has been highly correlated to the expectations – current situation components of the Conference Board Consumer Confidence Index. This observation is consistent with the view that the 2-year Treasury yield contains an expectational component that’s signaling an economic slowdown. As well, the flattening yield curve prompted

New Deal democrat to concede that, as far as recession conditions go, “The Camel’s Nose is in the Tent”.

For a contrary perspective, Kansas City Fed President

Esther George, who is regarded as a monetary policy hawk, recently voiced her concerns about the flattening yield curve from a financial stability perspective:

My concern about an inverted yield curve does not reflect its intensely debated value as a predictor of recession. Rather, my view is that an inverted curve has implications for financial stability with incentives for reach-for-yield behavior. An inverted yield curve also pressures traditional bank lending models that rely on net interest margins, or the spread between borrowing short and lending long. Community banks in particular rely on net interest margins to maintain their profitability, with rural areas especially dependent on community banks.

She went on to concede that “a soft landing is possible but not guaranteed” and “less favorable outcomes are certainly possible”.

Tightening into a slowdown?

Another disagreement between the Fed and the market is whether the Fed is engineering a recession by tightening into a slowdown. Jerome Powell’s comments at the March 2022

FOMC press conference made it clear that Fed officials believe the economy is strong and it is able to withstand a withdrawal of monetary accommodation.

Powell characterized the job market as “extremely tight”. He voiced concerns about inflation and the disruptive effects of the Russia-Ukraine war on commodity prices.

Inflation remains well above our longer-run goal of 2 percent. Aggregate demand is strong, and bottlenecks and supply constraints are limiting how quickly production can respond. These supply disruptions have been larger and longer lasting than anticipated, exacerbated by waves of the virus here and abroad, and price pressures have spread to a broader range of goods and services. Additionally, higher energy prices are driving up overall inflation. The surge in prices of crude oil and other commodities that resulted from Russia’s invasion of Ukraine will put additional upward pressure on near-term inflation here at home.

Indeed, the latest Markit PMI report is pointing to growth acceleration, not a slowdown, as well as strong inflation pressures.

Price pressures remained a significant theme in March, as costs increased at one of the fastest rates on record. Firms stated that further hikes in raw material, fuel and energy costs drove inflation, but also highlighted that the war in Ukraine and China’s lockcdowns were exacerbating supply chain strain.

The Citigroup Economic Surprise Index, which measures whether economic reports are beating or missing expectations, is similarly strong.

Regardless of which side of the debate you are on, a recessionary slowdown will see employment tank. While there has been some anecdotal evidence of softness in the jobs market, the employment situation remains strong.

TINA no more?

For equity investors, rising rates are pressuring valuation. When the Fed pushed rates to ultra-low levels in response to the COVID Crisis, equity investors could point to the TINA (There Is No Alternative to stocks) narrative. Now that rates are rising, is this a case of TINA no more?

The S&P 500 trades at a forward P/E of 19.5, which is above its 5 and 10-year averages. The forward P/E ratio peaked in 2020 and fell dramatically in 2022, which is consistent with a rising yield environment. However, recent market strength boosted the P/E ratio, which is pressuring valuation.

In such an environment, stock prices have to rely on earnings growth for all of the heavy lifting in the face of competition from higher rates. For now, forward EPS estimates are continuing to rise.

Here are valuation bull and bear cases.

George Pearkes at Bespoke pointed out that profit margins are soaring despite all the hand wringing about wage pressures.

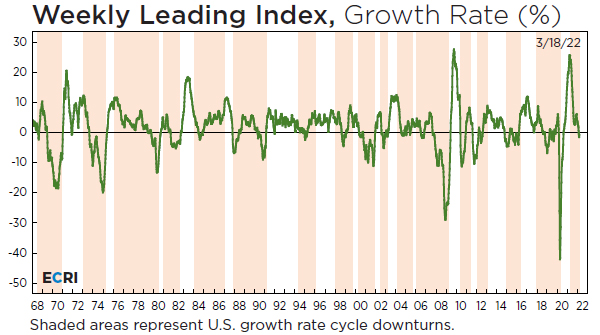

The bears will argue that while the current snapshot shows a strong economy, forward looking indicators such as the ECRI Weekly Leading Indicator are tanking. While readings aren’t at recessionary levels, they do point to a slowdown. Earnings growth expectations should decelerate accordingly.

As well, the combination of rising stock prices and rising 10-year Treasury yields has severely compressed the implied equity risk premium, defined as the forward earnings to price ratio minus the 10-year rate.

The market’s message

It’s time to settle the argument. Which school of thought will win in the end, recession or stagflation?

I conclude that current conditions indicate a late-cycle expansion consistent with a stagflation thesis. Forward looking indicators, however, point to a slowdown and possible recession ahead.

Timing the turn will be a tricky task for investors, but I have a simpler heuristic. The recent 2s10s flattening episode has been a bear flattener, where yields have risen, which is bearish for bond prices, while the 2s10s spread has turned negative. Instead, I prefer to focus on the longer end of the yield curve. Independent of the pace of Fed tightening and the anticipated pace of monetary policy, a falling 10-year yield is the bond market’s signal of economic weakness. If the 10-year yield begins to decline significantly, such as the violation of the 10-week moving average, that will be a signal for investors to embrace the recession scenario.

As well, an analysis of the relative performance of global resource groups shows that energy, mining, and agribusiness, which are sensitive to war-related supply chain disruptions, are undergoing high-level consolidations after upside relative breakouts. I interpret this to mean that stagflation pressures are steadying, but they haven’t completely faded.

In conclusion, the markets are being battered by geopolitical risk in the short term, which is stagflationary, and a Fed tightening cycle in the long term. The key risk for investors is whether the Fed will tighten into a recession, or if inflation expectations have taken hold and the economy has shifted into a stagflation era. The question is important because each scenario calls for different ways of positioning equity portfolios.

Current conditions call for a commitment to the stagflation trade, with an overweight position in late-cycle hard assets plays such as energy, materials, agriculture, and real estate. But investors shouldn’t overstay the party. The Fed tightening cycle should begin to squeeze inflation and growth expectations in the near future.

The key indicator of the regime shift will be bond yields. If bond yields were to decisively decline, it would be a market signal of slower growth and recessionary conditions on the horizon.

Well done Cam. An excellent treatise of the recession vs stagflation dilemma. Really appreciate the time and effort you put into these articles.

I echo Gary’s comment above.

Cam, under what circumstances would the yield curve revert and steepen? Would that mean ten year yield going up from current levels? How much risk is there in longer duration bonds? What about equities?

Thanks

The yield curve could steepen in a couple of ways:

1) Bear steepener: Yields go up, but long yields rise faster than short yields

2) Bull steepener: Yields fall, but short yields fall faster than long yields, or long yields actually rise.

(1) probably attributable to hawkish Fed

(2) probably because Fed reverses course and starts to ease.

Thanks!

1. The rise in long yields would be likely due to inflation expectations rising in spite of Fed’s tightening efforts? In that scenario, Fed is likely to get more hawkish causing an eventual recession?

2. The drop in long yields is a sign of impending recession too.

It seems a recession is almost necessary to tame the inflation genie, if that is what the Fed wants.

Ravindra,

I think Fed wants to cause a recession, and I believe it is needed for a couple of reasons:

1) Too much free $$$s floating around which needs to be reined in. People need to lose that money via bad investments etc. This is not necessarily readers of this website but Robinhood et. al. bunch.

2) Too many people not feeling the pinch and not taking jobs which are going unfilled and as a result causing slower growth.

All business are feeling the pain right not of not having enough workers. I think raised prices (Inflation) and destruction/loss of some of the extra moneys will cause a reversion to normal, with Post-pandemic and post war World, people needing to go back to Work.

At least that’s what I am imagining as a scenario.

I agree that Fed will push rates much higher believing that the economy can handle the rates. How the economy responds is the critical question. We may get a clue from the earnings and the guidance. Jamie Dimon is circumspect too.

I am gradually getting more defensive but not there with Cam.

Ukraine Russo war will have a much bigger impact on the long term outlook and has been discounted to some extent. If the conflict drags on into the end of the year, hostilities will expand to other countries.

It may too early to decide whether the war of the Fed matters more. It may be years before we fully understand the repercussions of the Ukraine invasion – or the impact of wrong moves by the Fed. For instance, one Twitter thread debates whether a protracted increase in the CPI will hasten the demise of Social Security (or at least force Congress to act sooner to save the program).

Sorry – meant to say whether the war OR the Fed matters more.

As I micro watch and read of micro dynamics, I occasionally see a long-term of the S&P 500 and think, “How the hell can we be this close to the peak with a hot war, the highest inflation in forty years, a huge number of Fed hikes coming, anti-globalization reversing prior efficiencies, political gridlock in America with epic food and gasoline inflation hitting lower income folks hard.

Then, I think that none of my micro positive indicators are can overcome the fact that the index is simply too high with the multiple risks coming at us. This can’t be explained away.

Imagine a world a year down the road where inflation has abated to around 3%, COVID is endemic, supply chains have adjusted and functional, Russia has new leadership, peace trumpets have sounded. Yes, reconstruction in Ukraine will take some time but that is a capital intensive effort and stimulative. Agriculture would return relatively soon.

I do imagine a world where things are much better. But, that is me.

Thanks for the optimism. Very needed.

The road to that world is likely to be difficult and rocky.

Over-thinking is not good. Market is telling us it is in N gear at indices level, until new data coming to change it. But under the surface it is a very orderly trading environment. Some of those trashed tech stocks are quietly making a comeback. A lot of money are shifting from Europe to US so that helps too. European markets are at historically cheapest vs US markets. But you don’t put money there for years to come.

It all depends where the money goes. Money must be going into the market to support it, because it does not make sense that with everything going on that the market is not down much more. If you look at a long term chart of the S&P, it’s just a blip. Maybe things go higher, which would not surprise me, or maybe it will be one of those grinding out a top processes, although the parabolic rise from 2020 makes me think more like 1929, or Nikkei 1989, nasdaq 2000 that the top will be sharp and sudden.

Maybe US markets are being played like bonds. Nobody buys bonds at 1/2% for the yield, but to trade if yields go lower and the price of the bond rises. Could be the same for US stocks, a gain on Forex, some safety in the face of all that is going on for emerging markets with rising rates and energy prices going up. Think of a sinking ship, the stern may rise, and sharply, but not forever.

I still think a bear trap is in the works, it is laying the groundwork for the boy who cries wolf, so that when the real top arrives the warnings will be ignored. Right now, who has been saying BTFD? Nobody, no there was tremendous pessimism in early March.

I don’t know about bear traps and how long they take to declare themselves, but looking at past moves in the S&P, including LTCM in 98, they have been sharp, so if it’s a trap the rally should continue over then next month or 2 to new highs. That would be my expectation.

But I am very fearful of what lies down the road, and if we break to new highs, I will be looking for the euphoria, and the “nothing can stop this bull”…geez I’m nervous already

Maybe monetary expansion can partially explain the S&P level

True Alex but the Fed is still buying mortgages every month but mortgage rates are up from 2.5,% to 4.5% and the Home Construction ETF is down 30%.

So a fall in anticipation of mortgage QT when very little in anticipation of QT everywhere else.