Happy New Year! Investors were happy to see the tumultuous 2020 come to a close. The past year has been one with little precedent. A pandemic brought the global economy to a screeching halt. The stock market crashed, and it was followed by an unprecedented level of fiscal and monetary response from authorities around the world. As the year came to an end, a consensus is emerging that a cyclical recovery has begun and we are seeing the dawn of a new equity bull. Some have even compared it to the Roaring 20’s, when the world emerged from the devastation of the Spanish Flu and World War I.

New bull markets often start with powerful breadth thrusts. As LPL Financial documents, the second year of a new bull can also bring solid returns, albeit not as strong as the first year.

As I look ahead to 2021, I consider three key issues.

- The economy and its outlook;

- Market positioning and consensus; and

- What could go wrong?

A recovering economy

Let’s start with the economy. The policy response to the crisis was unprecedented during the post-war period. Even as the unemployment rate spiked to levels not seen since the Great Depression, the combination of fiscal and monetary response put a floor on household finances. Real personal income, which includes fiscal transfers from the government. spiked even as the economy shut down. While the policy response has exacerbated an inequality problem, that’s a future issue that doesn’t concern today’s markets.

Looking to 2021, there are numerous signs that the US and global economy are recovering. Cyclically sensitive indicators such as the copper/gold and base metals/gold ratios have risen strongly.

Heavy truck sales, another key cyclical indicator, has traced a V-shaped bottom.

New Deal democrat follows the economy using a framework of coincident, short-leading, and long-leading indicators. For several months, he concluded that both the short and long-leading indicators are pointing to an economy itching to recover (my words, not his), but short-term health and fiscal policy have weighed down the coincident indicators. The latest analysis is more of the same [emphasis added].

Among the short leading indicators, gas and oil prices, business formations, stock prices, the regional Fed new orders indexes, the US$ both broadly and against major currencies, industrial commodities, and the spread between corporate and Treasury bonds are positives. New jobless claims, gas usage, total commodities, and staffing are neutral. There are no negatives.

Among the long leading indicators, corporate bonds, Treasuries, mortgage rates, two out of three measures of the yield curve, real M1 and real M2, purchase mortgage applications and refinancing, corporate profits, and the Adjusted Chicago Financial Conditions Index are all positives. The 2-year Treasury minus Fed funds yield spread and real estate loans are neutral. The Chicago Financial Leverage subindex is the sole negative.

While there were no significant changes this week, the good news is that – contrary to expectations – several of the coincident indicators made new YoY highs this week.

He concluded, “The pandemic and public policy reactions thereto remain in control of the data”.

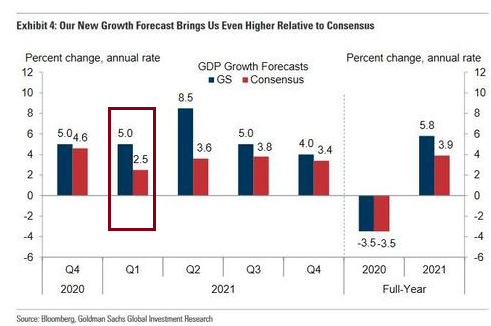

The $2.3 trillion spending bill signed by Trump last week, which includes $900 billion in renewed CARES Act 2.0 stimulus, should put a floor on Q1 growth even as the pandemic sweeps through the US and the economy shuts down. After Trump signed the bill into law, Goldman Sachs was the first major brokerage firm out of the gate with an upward revision to Q1 GDP growth to 5.0%.

Fed watcher Tim Duy wrote in a Bloomberg Opinion article that “Biden is Stepping Into a Dream Economic Scenario”.

The economy is instead poised for a rapid rebound for six main reasons:First, there is nothing fundamentally “broken” in the economy that needs to heal. And unlike the last two cycles, there was no obvious financial bubble driving excessive activity in any one economic sector when the pandemic hit. There is no excessive investment that needs to be unwound and the financial sector has escaped largely unharmed.

Second, the indiscriminate nature of the shutdowns this past spring provides the economy with a solid base from which to grow. The economy collapsed in the spring because in the effort to get ahead of the virus, we shut down about a third of the economy on an annualized basis. That created a lot of opportunity to rebound when the unnecessary causalities of the shutdown came back online and began to grow around the virus. That process will continue.

Third, household balance sheets were not crushed like they were in the last recession. Instead, the opposite occurred. Reduced spending, fiscal stimulus, rising home prices and a buoyant equity market have all helped push household net wealth past its pre-pandemic peak.

Fourth, the demographics are incredibly supportive of growth. During the last recovery, the economy was still adapting to the Baby Boomers aging out of the workforce with a much smaller cohort of Generation X’ers behind them. The larger Millennial generation was just entering college at the time. Now, the Millennials are entering their prime homebuyer years in force and will be moving into their peak earning years. The resulting strength in housing is fueling higher home prices and durable goods spending, and we are just at the beginning of the trend. Housing activity should hold strong for the next four years.

Fifth, household savings have grown by more than a $1 trillion, providing the fuel for a hot economy on the other side of the pandemic. Sooner or later, that money is going to come out of savings and into the economy and I expect it to flow into the sectors like leisure and hospitality where there is considerable pent up demand.

Sixth, and most importantly, vaccine is coming. Pfizer Inc. announced its Covid-19 vaccine is 90% effective. Many other vaccines are in development using the same strategy as Pfizer. To be sure, it will take some time for vaccines to be widely available but once they are the sectors of the economy most encumbered by the virus (the same as those for which consumers have pent-up demand) will be lit on fire. Moreover, schools and day cares can reopen allowing parents to return to the workforce.

The Roaring 20’s indeed.

Market positioning and consensus

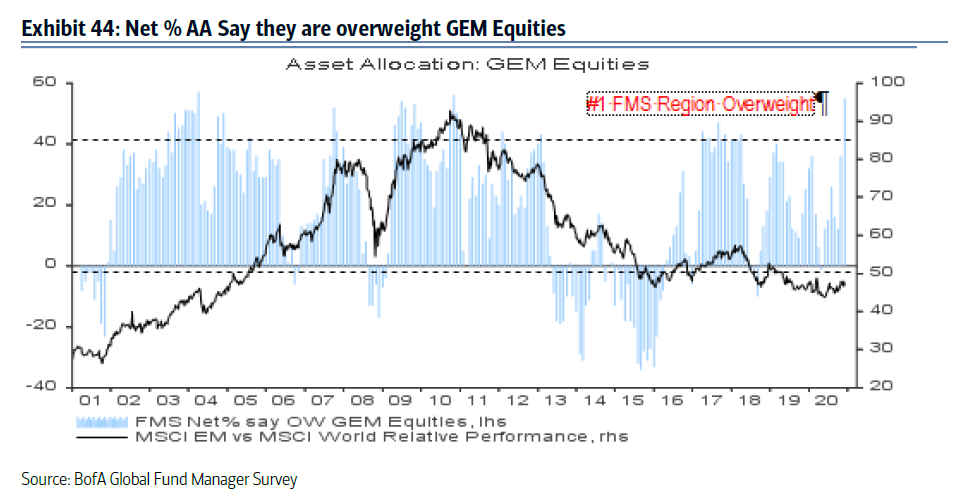

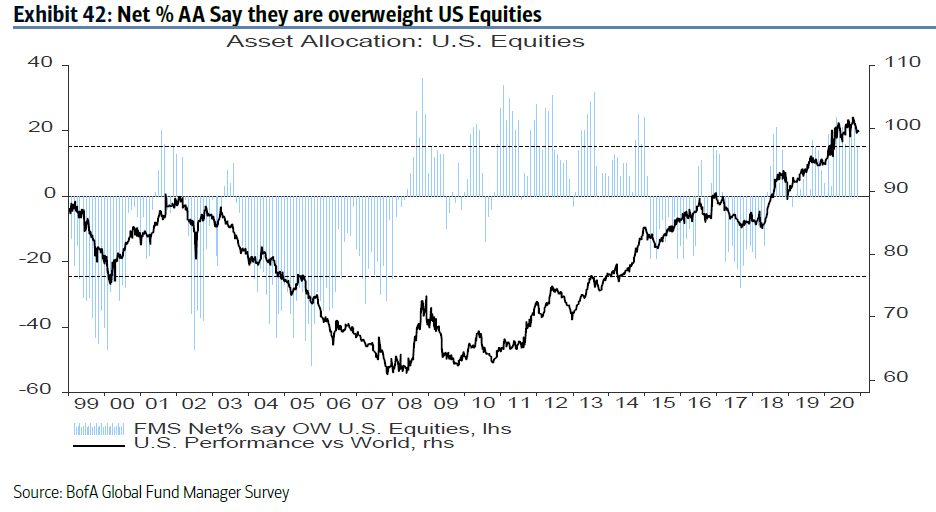

The global economic recovery is now the consensus opinion. The latest BoA Global Fund Manager Survey shows respondents expect a V-shaped recovery as vaccines become widely available by mid-2021.

As a consequence, they have piled into high beta emerging market equities for cyclical growth exposure.

What could go wrong?

In light of the emerging consensus of a cyclical economic recovery and new bull market, what could go wrong? I believe there are three key risks;

- Problems with a vaccine rollout;

- Rising inflation, which will force central banks to react and raise rates; and

- An unexpected slowdown in China.

Deutsche Bank recently conducted an investor survey of the biggest risks to the global financial markets in 2021. At the top were fears related to the rollout of vaccines, such as virus mutations, serious vaccine side effects that curtail their use, and the reluctance of people to become vaccinated, which would impede herd immunity.

Already, the failures of poor coordination are appearing. The FT FT reported about logistical bottlenecks are emerging in the EU, where the pace of immunization is too slow to keep up with the supply of vaccines. The NY Times lamented that a fumbled rollout has allowed vaccines to go bad in the freezer.

Of the 14 million vaccine doses that have been produced and delivered to hospitals and health departments across the country, just an estimated three million people have been vaccinated. The rest of the lifesaving doses, presumably, remain stored in deep freezers — where several million of them could well expire before they can be put to use.

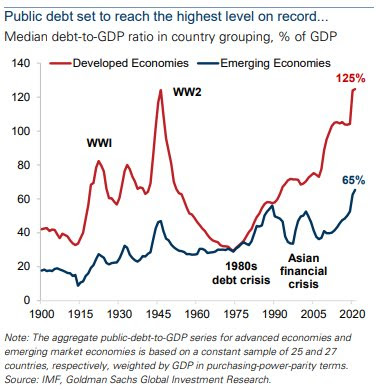

From a macro perspective, the unprecedented level of monetary and fiscal stimulus has created the risk of financial instability owing to rising debt levels. Debt-to-GDP has risen to levels last seen during World War II for the developed economies and exceeded those levels for emerging economies. While nominal rates are low to negative and real rates are mostly negative today, rising inflation could put upward pressure on rates and create instability.

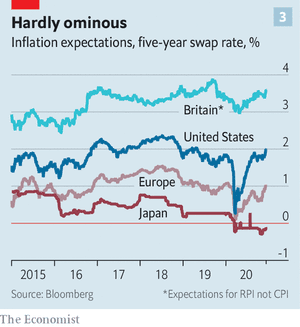

In the short-term, inflationary expectations are under control, and inflation surprises are occurring to the downside.

Moreover, developed economy inflation expectations are still tame. The problem of inflation, debt, and financial instability are problems in 2024 or 2025, not 2021.

China slowdown ahead?

I believe the key risk that could sideswipe markets is an unexpected slowdown in China. I recently observed that China is experiencing an uneven recovery (see Will Biden reset the Sino-American relationship?).

The rebound was led by fixed-asset investment and construction activity. Retail sales was the laggard. Beijing has returned to the same old formula of credit-fueled expansion. Moreover, Beijing has pivoted towards a state-owned led recovery.

A Bloomberg interview with Leland Miller of China Beige Book International (CBBI) confirmed the thesis of a hollow recovery in China. Miller warned investors to be wary of the bullish recovery signals from the commodity market. There is too much speculation in commodities. Chinese copper and steel firms reported Q3 collapsing sales, collapsing margins owing to higher input prices, e.g. iron ore, in the manner of early 2016.

In a normal recovery, China’s trade surplus should shrink as consumers spend more in response to improved conditions. Instead, the surplus rose, indicating an export and manufacturing-based recovery at the expense of the household sector. In addition, the Chinese authorities are tightening credit. Domestic credit rejection very high for retailers, indicating an unbalanced and hollow recovery.

Loan rejection rates for retail businesses increased to 38% in the final quarter of 2020 from 14% in the previous quarter, according to the latest quarterly report from CBBI. Rejection rates for small and medium-sized businesses rose to 24% in the final quarter, double the rate posted by large companies during the period.

“Large firms continue to gobble up whatever credit was available, enjoying much lower capital costs than their smaller counterparts, alongside higher loan applications and still falling rejections,” CBBI said. “This is the opposite of the quagmire small-and-medium enterprises find themselves in.”

Don’t be deceived by improvement in services in the PMI surveys. China Beige Book’s survey internals revealed an unbalanced recovery in services.

A recovery in services revenue was driven by businesses in telecommunications, shipping, and financial services, but those in consumer-facing industries, such as chain restaurants and travel, continued to lag behind, according to CBBI.

“Don’t confuse fourth quarter’s services recovery with the ‘Chinese consumer is back’ narrative,” said CBBI’s Managing Director Shehzad Qazi. “This is a business services — not consumer-side — recovery. Retail sector data bear this out even more clearly, with spending on non-durables sagging.”

China has led the global recovery, but these imbalances are an accident waiting to happen. I have no idea when this might unwind, but be prepared for a “China is slowing” narrative to sideswipe global risk appetite in the near future. This is a tail-risk that the market is not prepared for.

Investment implications

While a cyclical recovery and a new equity bull have become the new consensus, I remind readers that both the Dow Jones Industrials and Transports recently achieved new all-time highs, which constitutes a Dow Theory buy signal. This is a powerful indicator that the primary trend is up.

Should investors be worried about a case of too far, too fast? Variant Perception pointed out that notwithstanding investor sentiment, liquidity conditions are friendly to equity returns for the next six months.

That said, investors who want to position for a cyclical bull market should look beyond the S&P 500. The index has become very growth and tech-heavy. The weight of cyclical groups within the S&P 500 has dwindled to 24%.

US tech stocks are likely to face headwinds. Foreign institutions piled into US large-cap growth stocks during the pandemic as the last refuge in a growth-starved world. Now that the growth scare is over, investors are likely to rotate into cyclicals instead.

SentimenTrader also observed that tech stocks have gone too far, too fast. If history is any guide, don’t expect them to continue their winning streak. By implication, the S&P 500 is likely to face headwinds in advancing if tech and tech-like sectors comprise about half of the index’s weight.

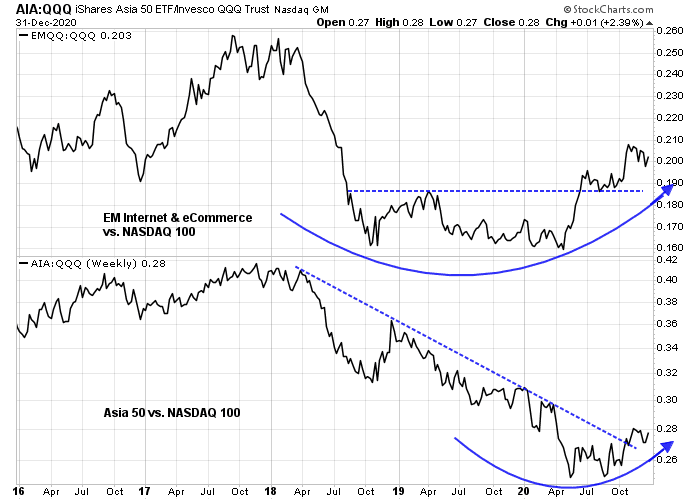

There are better opportunities for growth investors. A comparison of EM internet and eCommerce stocks (EMQQ) to the NASDAQ 100 (QQQ) and the Asia 50 (AIA), which is very tech and heavy, shows that the NASDAQ 100 has outperformed its EM and Asian counterparts. Both the relative performance of EMQQ and AIA to QQQ are showing signs of relative bottoms, which are constructive for these non-US tech-related issues. This is despite Beijing’s recent scrutiny of Ant Financial, which has depressed the Chinese fintech sector.

In conclusion, the global economy is undergoing a cyclical rebound. Equity markets have surged in response. In the short-term, sentiment has become stretched, risks are appearing, and the S&P 500 could correct by 5-10% at any time. While the fast retail and hedge fund money has mostly gone all-in, the glacial institutional money remains underweight beta. State Street Confidence, which measures the custodial holdings of institutional managers, is still below the neutral 100 level.

Investors should look to pullbacks to buy dips, but better investment opportunities can be found in non-US markets.

The pandemic will recede in our memories soon enough, along with its effects on the global economy.

As with all things in life, it’s up to all of us to focus on any silver linings and make the best of things. Here are a few that occur to me.

(a) The fastest bear market in history may well have been the pullback that launches what will be one of the greatest bull markets in history. The darkest hour before dawn and all that.

(b) Several high-profile companies will be relocating out of the Bay Area. In addition, many workers able to work permanently from home have already left. This has helped to stem the unaffordable housing situation. A combination of lower demand + low rates allowed our two oldest to buy their first homes in November – one in the Montclair district of the Oakland Hills – without any help from us. A year ago, I wouldn’t have believed it.

(c) I learned a few new tricks while trading my way out of hole last summer/fall. For one thing, by focusing on high-beta momentum names, it’s possible to repeatedly nail down a few hundred in gains (using small position sizes in the 4-5 figure range) in the premarket session and/or first thirty minutes of the regular session. I can’t recall exactly when it all started – over time it just became obvious that certain recurring patterns generated good profits for many traders in my Twitterfeed. The system works well for me, as I have neither the ability nor the patience to be watching screens all day.

(d) While Cam may wish to incorporate new ideas into his trading process, the fact remains that he has developed a process with a long track record. That’s why we’re all here. His 2020 report card represents a good self-assessment of the previous year, which tells me he’s already incorporated the necessary lessons moving forward.

There is no question that frustrated business owners/ consumers/ diners/ travelers are chomping at the bit for a return to normal life, and 2021 should reward investors willing to risk exposure ahead of the wave.

Best wishes to all this year.

Nothing about vaccines worries me. If one or two don’t work then one of the other fifty in development will. The Fed is committed to low rates for years and new board members just appointed are more dovish than the last ones. So inflation can rip without them touching the brake pedal. So inflation causing higher rates isn’t a problem for stock markets.

But America is heading for a big problem that the portfolio managers in the above survey are missing because of their privileged lives. That is civil unrest. They mention societal unrest because of the political divide. Bullshit. That is what they see at cocktail parties. I’m talking about the bottom half of the labour force who is getting screwed royally while the rest of us watch our stocks go up merrily. These folks are hurting and their day to day living conditions are precarious. They don’t care now about political parties. That was last year.

Occupy Wall Street after the GFC was a disjointed grab bag of grievances that sputtered out. I’m very concerned after the Covid Crash, anger will rise later this year when this last support runs out and jobs are slow to return or never return in some areas. Also general inflation indexes may not reflect the rise in food and other essentials to basic life that effect the bottom earners. The angst could boil over, big time. The black community will expect swift action from the Biden administration and may be disappointed. The Trump base feel cheated and left out.

With the trillions of dollars of government spending happening, we can expect a raft of corruption being discovered. The rich upper class will look like greedy sharks to the masses who are suffering.

How this effects markets is anyone’s guess. It may be a contributing factor on why American markets might underperform global.

My hope is that things unfold smoothly and fairly.

See https://www.theatlantic.com/magazine/archive/2020/12/can-history-predict-future/616993/

Yes, I read that article too. Very chilling and a reason for my message. The pandemic has speeded up so many trends in society that he worries about. I recommend everyone read it.

Well, maybe. But to paraphrase the Chinese social scientist also quoted in the article – then again, maybe not.

There’s something about the pessimistic outcome, the negative scenario, the eve of destruction – that fascinates. I prefer the optimistic scenario, wherein our so-called elite class will find solutions that benefit the masses as much if not more so.

After relocating to the Bay Area I first rented an apartment near El Cerrito and would try a different restaurant every night on Solano Avenue in Albany. After dinner one evening I decided to check out the Oaks Theatre down the block to watch some forgettable film. While waiting for the curtains to open someone played on old LP over the PA system, and it was Barry McGuire’s ‘Eve of Destruction.’ That’s when I knew for certain moving back was the right decision.

https://www.youtube.com/watch?v=MdWGp3HQVjU

Best new recent song discovery-

https://www.youtube.com/watch?v=8E8_utQlJbo

Can’t believe she’s been active since 1978 – talent ages well.

I think it is primal human nature. I say primal because of the “pecking order”, it affects how we think and act. It’s why there will always be elites, and counter elites and being higher up on the hierarchy feels good. Every day when I go for groceries at either Walmart or Trader Joes, I think of these people working there and how squeezed most are financially. The same can be said for the lower what 80%? But this has been true for 1000s of years and every now and then something really nasty comes along like the French or Russian revolutions. Hopefully with the next downturn there will be some help for those who would end up in terrible poverty, but the opportunists will see it as a chance for change. After all, in order to have a class struggle, you need 2 sides.

What struck me about Biden in his acceptance speech was that he did not point a finger, of course it is easy to be gracious when you win, compare Trump 2016 to Trump 2020…beware those politicians who point fingers and blame others.

People say a new bull market, but I think it is just more of the old bull market that started in 2009. The drop in 2020 was a correction because it was so brief, it was nothing like what happened in 2007 or 2000. A real bear market lasts longer. I know, this is just my opinion, but when they describe the phases of a market, bull or bear, there are words like euphoria, despair…it takes time for the mood to get really giddy or in a deep funk. That did not happen in 2020.

One of the things that all governments have in common is a desire for control, well any sizable country. So what happens when China comes out with it’s cryptocurrency and makes others including Bitcoin illegal? Or if the US and Eurozone do that? Then all this displacement of BTC from funds etc vanishes, as does the price of BTC..does this trigger something? India a while back did something about the denomination of notes..it was a control thing. We are not allowed to just bring more than 10,000 dollars when we travel, we have to be careful about our bank accounts when refinancing, is bitcoin immune to governments? It can always be used by criminal elements, but if it becomes illegal then there are problems for it. Gold had to be surrendered in 1933. I don’t think the Fed will say “sell us all your BTC at such and such a price” why would they when they can make their own crypto they control? In 1933 gold was something you could not just create, so they had to take it.

Control is human nature too.

Speaking of bears by the way, they say that bear market rallies can be very sharp, so maybe this is why in a secular (or at least bear of 1 to 2 years duration) you get twists that don’t do as well.

Here is the 5 year weekly chart of the dollar index:

https://www.stockcharts.com/h-sc/ui?s=%24USD&p=W&yr=5&mn=0&dy=0&id=p59736529957&a=865311509&listNum=1

My concern is that there tremendous support at these levels 88.50 to 89. If for some reason that we do not know the dollars rallies both emerging markets and precious metals will be adversely affected.

Then again Bitcoin just crossed $32,000! Maybe the dollar will continue to go down more.

Now a positive possibility. Everyone is expecting votes in the Senate will be strictly by McConnell dictated GOP lines that would block Biden spending plans like they blocked Obama. But what if many GOP Senators become moderate or simple Biden can negotiate a political truce. What if McConnell is replaced as GOP Senate leader? This would spur infrastructure spending especially green initiatives.

Expect four exciting years to come for media tabloids. Michael Avenatti (a one-time D favorite candidate to run against Trump) and Stormy Daniels are nothing compared to what to come. With D so deep in bed with CCP, expect tons of explosives. Just say “Gloves are off.”

Trump is still in office, but the opening salvo has been catapulted. Remember Eric Swalwell and Fang Fang? Other pics show she is also with Mike Honda and Ro Khana. One old scumbag replaced by a younger scumbag in the House of Representatives. Unfortunately Khana is representing a district I am currently living in.

At my place on the hill and behind thick trees I can see his house in Sunnyvale thru binoculars. My old (in real life) friend once visited me and stated that the weapon they developed at Lockheed can reach Khana from my place with accuracy of 1-2mm . I advised him not to dispense the good old-fashioned American justice at his personal liberty. It is not 60s and 70s anymore. Yakuzas don’t cut off their fingers or practice harakiri anymore.

Even Trump is spared in today’s world. The Globalist cabal can use media, riots, and election fraud to get him out office, and their goal is achieved. The previous three victims are not so lucky: JFK (foolishly trying to abolish the Federal Reserve), RFK (foolishly trying to follow JFK’s dream), and MLK Jr(foolishly trying to make the world a better place). Maybe a fourth one: JFK Jr (foolishly showing presidential ambition).

Maybe I can persuade the Indian guy ( his name sounds exactly like Bob Dylan) to run against Indian guy Khana in next election. This Indian guy almost won a local low-level office last time.

Jokes above for the new year. But seriously we need to pay attention to China from all angles. This is a year full of potential conflicts in every which way you can imagine. The ramifications on investing could be substantial.

What will happen to bonds ? The stock/ bond allocation has been golden for years. But with rates near zero, that cannot continue, right ?

Won’t there be a tsunami of money from the bond market looking for a decent return ?

I think the Nashville incident is just the beginning. Unrest is coming, how that will impact the market is uncertain.

If memory serves, market did alright in the 60s.