Now that 2020 has come to an end, it’s time to deliver the Humble Student of the Markets report card. While some providers only highlight the good calls in their marketing material, readers will find both the good and bad news here. No investor has perfect foresight, and these report cards serve to dissect the positive and negative aspects of the previous year, so that we learn from our mistakes and don’t repeat them.

2020 was a wild year for equity investors. The S&P 500 experienced 109 days of high volatility days during the year, as measured by daily swings of 1% or more. Measured another way, the stock market had high volatility days 45% of the time in 2020, compared an average of 25% since 1990. This level of volatility was similar to a reading of 53% in 2009 and 41% in 2000.

Let’s begin with the good news. The Trend Asset Allocation Model’s model portfolio delivered a total return of 19.7% compared to 16.1% for a 60% SPY and 40% IEF benchmark (returns are calculated weekly, based on the Monday’s close). Total returns from inception of December 31, 2013 were equally impressive. The model portfolio returned 13.8% vs. 10.6% for the benchmark with equal or better risk characteristics.

An unprecedented policy response

Now for the bad news, and there was plenty of it. While the Trend Model was disciplined enough to spot the crash in March and recovery thereafter, it was very late to turn bullish. I attribute this to two critical errors in thinking.

The unemployment rate had spiked to levels not seen since the Great Depression. I found it difficult to believe that the economy would not tank into a deep recession. I did not understand the magnitude of the fiscal and monetary response that put a floor under the downturn. The chart below tells the story. Even as unemployment rose to unprecedented levels, personal income rose as well. This was an unusual pattern not seen in past downturns and can be explained by a flood of fiscal support to the household sector.

We can see a similar effect with the savings rate, which also spiked to absurdly high levels even as unemployment soared. As government money flooded into households, some of the funds were not needed immediately, and the savings rate rose as a consequence. To be sure, the fiscal support was uneven and exacerbated inequality problems, but that’s an issue for another day. The actions can be partially excused by characterizing the legislation as battlefield surgery, which is imperfect but designed to save as many as possible under crisis conditions.

As well, the Federal Reserve and global central banks acted quickly to flood the global financial system with liquidity and financial stress was contained.

A valuation error

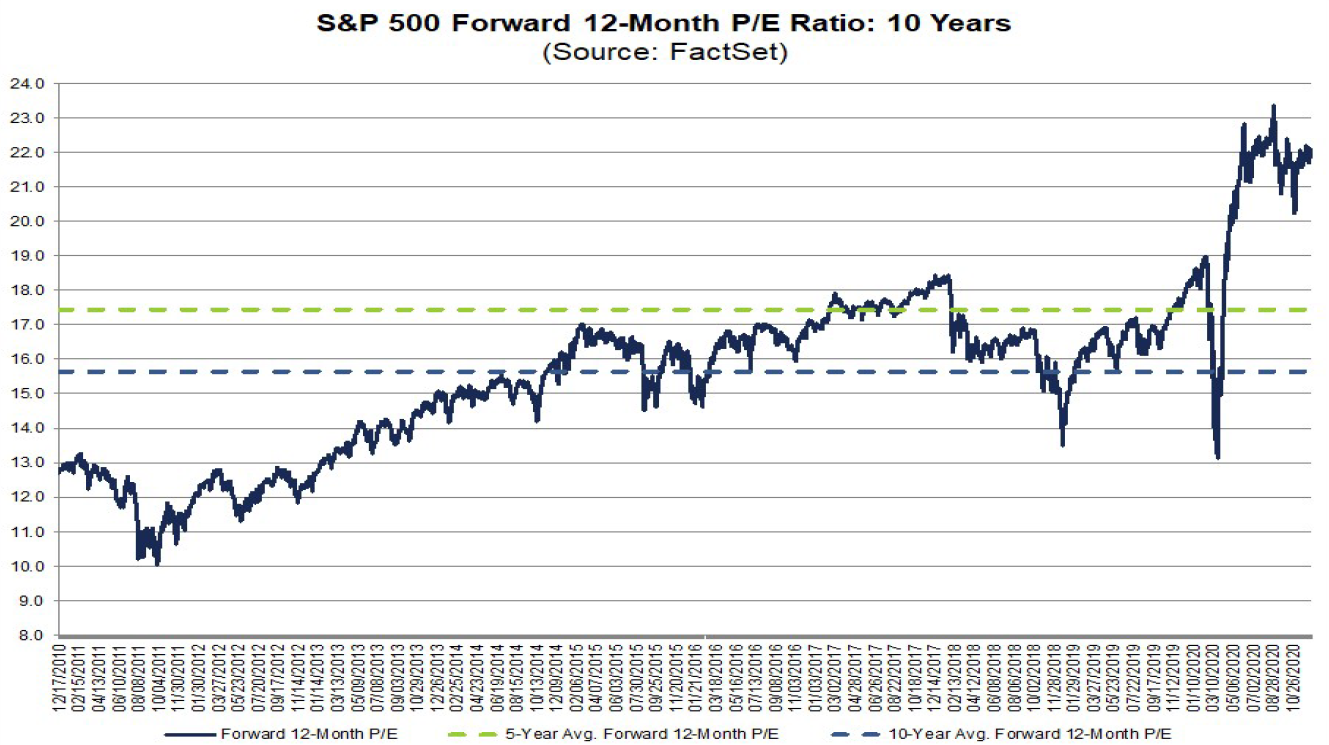

My second error was my assessment of valuation, which was based mainly on the forward P/E ratio, which had risen to historically high levels. I could not initially fathom why that constituted good value for equities.

Other traditional metrics, such as the Rule of 20, which specifies that the stock market is overvalued if the sum of the forward P/E and inflation rate exceeded 20, were screaming for caution.

An excessive focus on forward P/E based valuation turned out to be a conceptual error. I addressed those concerns in early October in a post (see A valuation puzzle: Why are stocks so strong?).

One of the investment puzzles of 2020 is the stock market’s behavior. In the face of the worst global economic downturn since the Great Depression, why haven’t stock prices fallen further? Investors saw a brief panic in February and March, and the S&P 500 has recovered and even made an all-time high in early September. As a consequence, valuations have become more elevated.

One common explanation is the unprecedented level of support from central banks around the world. Interest rates have fallen, and all major central banks have engaged in some form of quantitative easing. Let’s revisit the equity valuation question, and determine the future outlook for equity prices.

Soon after, I followed up with a cautious bullish call to Buy the cyclical and reflation trade?. The month of October was still gripped by election uncertainty. I turned unequivocally bullish in November with Everything you need to know about the Great Rotation, but were afraid to ask.

Better late than never.

My inner trader

The trading model had been performing well until 2020. The most charitable characterization was my inner trader caught the coronavirus. The drawdowns were nothing short of ugly. This was attributable to the conceptual error in thinking that I outlined, and a belief that the market would return to test the March bottom.

When the prospect of one or more vaccines and an economic recovery came into view at the end of Q3, I recognized that markets look ahead 6-12 months, and the odds of a retest had become highly unlikely.

Looking ahead to 2021, tactical trading models used by my inner trader are likely to be less relevant. The point of market timing models is to avoid ugly downturns in stock prices. This is a new cyclical bull market. The costs of trying to avoid corrections, which is a risk that all equity investors assume, are less worthwhile if the primary trend is bullish.

Happy New Year, and I look forward to a better 2021.

Most striking to me is the maximum drawdown in the model portfolio. Pretty amazing.

That’s because the range of asset allocation on the model portfolio is a maximum of 80% SPY and 20% IEF, and a minimum of 40% SPY and 60% IEF.

There is a considerable fixed income component to that portfolio.

This is a year when a lot of pros bite the dust. Market behaviors finally confirmed the trend of relentless bid. Going forward I am wondering what the Markets will look like?

Investors in general are less and less trigger-happy and less inclined to sell. And there is a new trend in investing biz: custom indexing. This will put even more pressure on pros.

They learned in 2020 that there can be no biz as usual, or else your career is soon over. I don’t know how they will adapt. New added element in relentless bid comes from future corporate buy-back programs. This is going to be big now that just about every company is flush with cash. Junk or investment grade, it doesn’t matter.

Civilian sectors are filled with money too. Housing prices are soaring. Is equity market going to explode much higher too? What are we going to do with all this liquidity sloshing around?

A wise man learns from his mistakes and an even wiser man learns from others’ mistakes.

Cam, let me be the first to congratulate you on an excellent newsletter and wish you and all your subscribers a happy and prosperous New Year.

As Ken very aptly has said on many occasions, we are all in this together. Any suggestion I make is in this vein and should not be misconstrued as an affront. I have too much respect for you as an analyst, so to think otherwise would be incorrect.

Since I live in the world of short term trading and have crossed the border from a being a net loser to making hundreds of thousand dollars this year I would like to share with the readers an objective critique of what needs to be done to improve the performance of the “inner trader”. My success is not a one year fluke as I make money consistently every year.

1. The first question one should ask is why do you trade. The answer could be to make money or to show your friends and spouse how smart you are or for that matter to increase your number of subscribers.

2. If the objective is to make money, then there has to be a firm set of rules. Unfortunately, they cannot be subjective but have to be based on a risk reward basis.

That is, how much am I willing to loose to make x amount on a trade. In your case even though 65% of your trades are profitable, the losses on the ones not profitable overwhelm the ones that are profitable. The size of your loss is in disproportion to your gain. The criteria has to be, not how often you are right but how much you make when you are right. The solution is simple – use stops; hard paper stops not mental stops. The stop should be placed at the initiation of the trade.

3. As a trader it is important not to fight the trend. There is glory in being able to call the top or the bottom BUT if one is wrong take your loss quickly. Re-asses the trend by an objective manner i.e. moving average. Your choice at that point is to trade with the trend or step aside. For the last three weeks I have been looking for signs of a top and taking small losses (3 trades back to back). So now I wait patiently to see if anything changes in the New Year. It could be the dollar finding a floor.

4. Finally, in my trading I tend to pyramid into trades. I buy a position in three intervals. If the first one shows a loss I stop till it either does what I was hoping it would do or I take a loss and move on.

As an aside I tend to be more right than wrong on my trades. If I have one MAJOR weakness which I am working on is to let my profits run. Unlike you I tend to take my profits prematurely. Hopefully that will change.

Again all the best to everybody for the New Year!

It’s important to reflect on what has happened to improve. But 2020 with its pandemic and never before seen government and Central Bankers’ responses were truly unprecedented. This link reports how the previously successful, most sophisticated quants did extremely bad because they base their black boxes on historical data that was not only irrelevant but misleading.

https://www.bloomberg.com/news/articles/2020-12-30/human-run-hedge-funds-trounce-quants-in-year-defined-by-pandemic

Being a student of the markets like Cam, I too expected a normal bear market second plunge after the March rally when in fact a tsunami of Fed liquidity was floating everything higher. So be it, I forgive myself and anyone who was fooled. My saving grace with clients is that I went to almost all cash two days after the February peak and stayed that way to the bottom. Any mistakes were missing opportunities and not pissing away capital by bailing in a panic near lows.

But what have I learned that I can use in future? Here is where I have seen so many investors make mistakes in the past. They make changes to fight the last battle after a bear market. I don’t want to embrace new pandemic investment rules that will be counterproductive in a non-Covid world. Those hedge funds that fold into their algorithms the Covid market data may be screwed up forever.

I have learned that by far the key to the direction of stocks are Central Bankers and politicians. Gong into 2020 we had the US government deficit at record highs and the Fed pumping hard when the employment rate was at multi-decade lows. That was clearly politically motivated. Powell bent a knee to Trump. Then the response to the pandemic was way too much. Instead of sending checks to just the people that needed it, they sent the $1,200 to those with jobs or retired folks like Bill Gates. Even this last $600 is not targeted to those in need or about the be evicted.

This is all very socially conscious and necessary when the government forced people into a pandemic economic shutdown but continuing these huge Fed and government programs will distort the economy and the value of money. Just look at the home price boom occurring during an economic depression. Bottom line is that the Fed is distorting valuation norms to the benefit of stock and home owners. They equate the level of the S&P 500 with Main Street economic success. I don’t see the Fed changing their policies. They are hypersensitive to and avoid any economic pain. This will lead us to Crazy Good or Crazy Bad markets. History will not be a guide.

Now on to investing. I learned that my Factor research works incredibly well and should have simply been trusted. It shows when investors turn risk-on confidently even if I think I know better and fail to join the party.

I learned that my momentum research should be trusted even when the outperforming growth ETFs including FAANGs seem insanely priced (and then went up a hell of a lot more.) Trends persist. Go with the flow and prosper. Don’t judge when one is in a new world. Now the flow has flipped to economically sensitive Value when their profits don’t (as yet) justify their stock prices. I won’t judge the masses. Go with the flow.

On a behavioral basis, I’ve learned that at turning points at a low, this is the time to buy the riskiest investments. That is when they feel most dangerous but in fact are safest. One has to fight the urge at that time to buy less volatile things. For example, Small Cap or the hated Energy. In today’s markets, by the time you are confident a new intermediate uptrend is happening, these riskier sectors are up huge in price and at truly riskier prices. When a correction is happening, I will be searching for high beta sectors that are experiencing growing investor pessimism to get ready for one of my Tactical Factor Twists to mark a low and then pounce. Anticipation is the key to quick, successful action.

Behaviorally, I know it will be difficult but necessary to buy non-American (or non-Canadian for me as well) stocks. My momentum work is showing World ex-America is outperforming after years of doing poorly. “Home Country Bias’ is tough to escape.

Marty Zweig said a long time ago. “Don’t fight the Fed and don’t fight the tape Ken”. It is amazing that we have to keep learning the SAME LESSON again and again.