Stock prices raced upwards last week on the news that the COVID-19 outbreak is improving in New York and other parts of the US, and on the news that the Fed unveiled another $2.3 trillion bazooka of liquidity. Despite these positives, I am not convinced that this bear market has seen its lows yet.

This week, I analyzed the market using a variety of techniques. All of them lead to the conclusion that a major market bottom has not been reached yet.

- Long-term market psychology

- Technical cycle analysis

- Valuation

- Smart investor behavior

Let’s start with long-term investor psychology. In the past few weeks, I have received numerous questions from readers to the effect of, “I am a long-term investor, should I be putting some money to work in the stock market here?”

If we were to change our viewpoint from an anecdotal to a more formal data perspective, the New York Fed conducts a regular survey of consumer expectations. One of the survey questions asks if respondents expect higher stock prices in the next 12 months. Instead of fear, investors are exhibiting signs of greed. Investor psychology just doesn’t behave that way at major market lows.

Mark Hulbert made a similar point about his sample of market timing newsletter writers in a WSJ article. While market timers were fearful at the end of the March quarter, their fear level was nowhere near the levels seen at past market bottoms.

This is not time to relax. The bear market is not over.

No technical signs of a long-term bottom

If I was to put on my technical analysis hat, I see no signs of a long-term bottom. Markets are inherently forward looking, and if stock prices are starting to discount a recovery, we should see hints in cyclical indicators, as well as commodity prices. None of those signals are present.

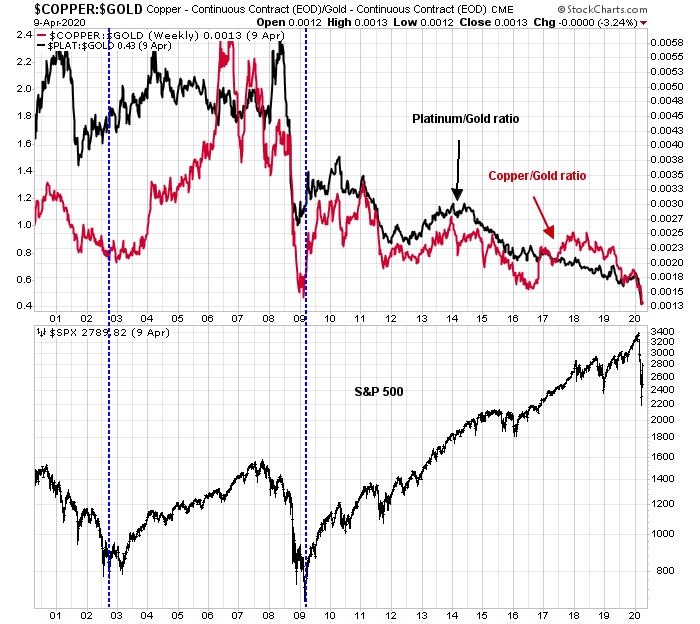

Consider, for example, the copper/gold and platinum/gold ratios. Copper, platinum, and gold are all commodities and have inflation hedge characteristics. However, copper and platinum have industrial uses, and the copper/gold and platinum/gold ratios should signal upturns in the global cycle. In the last two market bottoms, which are marked by the vertical lines, the platinum/gold ratio bottomed out ahead of the stock market bottom, while the copper/gold ratio was roughly coincident with stock prices. Currently, both of these ratios are plunging, and there is no early signal of a cyclical bottom.

Commodity prices also led or were coincident with stock prices at the last two major market bottoms. The CRB Index bottom well ahead of stocks in the aftermath of the NASDAQ Bubble bear market, and they slightly led stocks in 2009. The CRB Index is still weak, and shows no signs of a durable bottom.

Here is a close-up of the pattern in 2009. The CRB Index bottomed out a few days ahead of the stock market’s bottom in March 2009.

Metal prices also show a similar lead-lag pattern with stock prices. While gold has its unique characteristics and bullion marches to the beat of its own drummer, silver, copper, and platinum all turned up ahead of stock prices at the last two bear market bottoms. There is no evidence of any similar buy signals today from any of these commodities.

Market bottoms are also characterized by changes in leadership. Bear markets are forms of creative destruction. The old leaders from the last cycle, whose dominance become overdone, falter, and new market leaders emerge. Instead, the old leadership of US over global stocks, growth over value, and large cap over small caps are all still in place.

I am doubtful that a new bull market can begin with technical conditions like this.

Valuation headwinds

Another challenge for the long-term bull case is valuation. The S&P 500 is currently trading at a forward P/E ratio of 17.3, which is above its 5-year average of 16.7 and 10-year average of 15.0. Moreover, we are entering Q1 earnings season, and the E in the forward P/E ratio is going to be revised substantially downwards.

How far down? Consider that FactSet reported consensus bottom-up estimate is 152.81 for 2020, and 178.03 for 2021. By contrast, most of the top-down estimates I have seen for 2020 is in the 115-120 range, and the 2021 estimate is about 150. Those are very wide spreads between top-down and bottom-up estimates. The gap will be closed mainly with falling bottom-up estimates, rather than rising top-down upward revisions.

During my tenure as a quantitative equity portfolio manager, I have learned that whenever a country experiences an unexpected shock, all quantitative factors stop working. They then begin to work again in the following order. First the price technical factors start to convey information about the market. Next comes the top-down strategist estimates, followed by the bottom-up estimates. That’s because everyone knows the shock is bad, but no one can quite quantify the effects. The top-down strategists first run their macro models and come up with some ballpark estimates, but the company analysts cannot revise their estimates until they have fully analyzed the companies and industries to be able to revise their earnings. That’s where we are in the market cycle.

The final stage of the adjustment occurs when most of the damage is known, and fundamental factors like value and growth start to work again. We are far from that phase.

With that preface, let’s then consider the market’s valuation. I went back to 1982 and analyzed the market’s forward P/E ratio at major market bottoms. The 1982 bottom was an anomaly, as the market bottomed out at a forward P/E of about 6 because of the nosebleed interest rates of the Volcker era. The 2002-2003 bottom saw a forward P/E ratio of about 14. Those are the two outliers. The 1987, 1990, 2009, and 2011 bottoms all saw forward P/E ratios of about 10. All of these episodes occurred during backdrops of very different interest rate regimes. Can a new bull market begin today at a forward P/E of 15, with an uncertain E that is dropping quickly?

Here is how we arrive at the downside potential for the S&P 500, assuming the top-down estimates of 120 for 2020, and 150 for 2021. Supposing that the market bottoms out today, or at the end of March, forward 12-month EPS would be 75% of 120 + 25% of 150 = 127.50. Applying a P/E multiple range of 10-12, we arrive at a range of 1275-1530. Using the same methodology, a June bottom yields a 12-month forward EPS of 135, and a price range of 1350-1620. A September bottom results in a forward EPS of 142.50, and price range of 1425-1710.

For investors who believe that P/E ratios should be adjusted for interest rates, Callum Thomas of Topdown Charts calculated the equity risk premium of the US equity market based on CAPE. While current levels are starting to look cheap, they are nowhere near the compelling readings that are usually found at past major market bottoms.

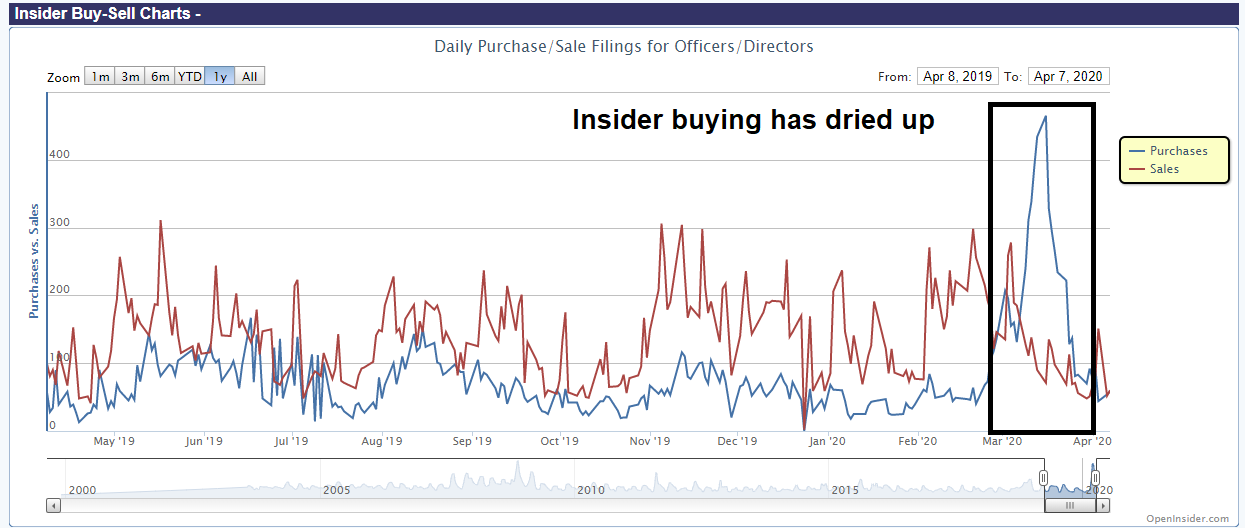

What are smart investors doing?

Here is another way of thinking about valuation. Insiders stepped up an bought heavily during the most recent downdraft, but this group of “smart investors” backed away as the market rose.

To be sure, insider buying is an inexact market timing signal. Insiders were too early and too eager to buy during the initial decline in 2008.

They were also early in 2018.

For the last word on this topic, here is all you need to know about “smart investors”. At the bottom of the market during the Great Financial Crisis, Warren Buffett stepped in to rescue Goldman Sachs when the Goldman sold an expensive convertible preferred to Berkshire Hathaway, with share purchase warrants attached to the deal. When the market recovered, Buffett made out like a bandit.

What has Berkshire done today? It is raising cash. It sold its airline stocks, and Bloomberg reported that it is borrowing $1.8 billion in a Yen bond offering. In the current economic environment, there are many companies who need to borrow to shore up their liquidity, cash rich Berkshire Hathaway does not fit into that category.

Does this just make you want to rush out to buy stocks to get ahead of the FOMO stampede?

Instant bear, instant bull?

This bear market was the result of an exogenous shock that led to a recession. Ryan Detrick of LPL Financial found that recessionary bear markets last an average of 18 months, mainly because recessions take time to snap back and cannot normalize instantly.

While we have experienced an instant market, for stock prices to turn around back into an instant bull requires at least a light at the end of the tunnel. Namely, the circumstances that sparked the recessionary conditions are on their way to be resolved.

The markets began to take on a risk-on tone last week when the trajectory of COVID-19 cases and deaths began to improve, both in the US and Europe. While such improvements are to be welcome, they are the necessary, but not sufficient conditions for a re-launch of a new bull. In the absence of a miracle medical breakthrough, it is difficult to envisage how the current recessionary conditions can be resolved quickly. Even if the virus were to be under control, no one can just flip a switch and restart businesses in an instant.

Based on the first-in-first-out principle, we can observe that Asia is beginning to see a second wave of infection as governments ease lockdown restrictions. As an example, Singapore, which was extremely successful at controlling its outbreak, saw new cases spike as soon as restrictions were eased.

Unless a population were to acquire herd immunity, either allowing COVID-19 to run rampant through its people, or through some medical treatment that controls the outbreak, governments are going to be playing the game of whack-a-mole with this virus for some time. Under such circumstances, even the top-down S&P 500 earnings estimates of 115-120 for 2020 and 150 for 2021 are only educated guesses, and subject to revision based on changes in public health policy.

Despite the gloomy outlook, I have some good news. This recession is not to become a depression. Fed watcher Tim Duy wrote a Bloomberg article explaining the prerequisites for a depression depends on three Ds, depth (of downturn), duration sufficient for a recession or depression, and deflation. Duy observed that we certainly have the depth to qualify as a downturn, though the duration of the weakness is unknown. However, global central banks have sufficiently taken notice that they are doing everything in their power to combat deflation. While this global recession is going to be ugly, it is unlikely to metastasize into a depression.

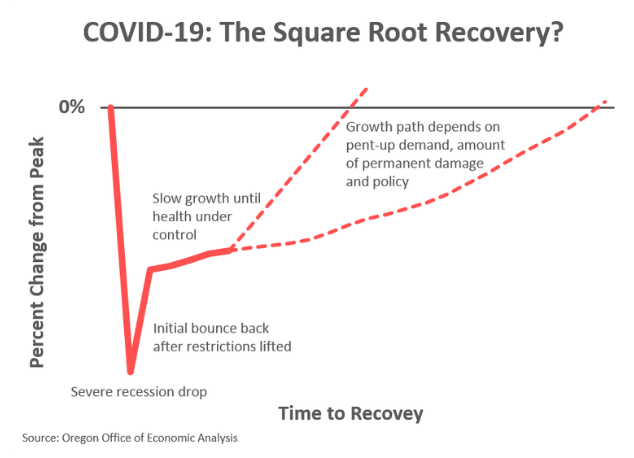

I would also like to clarify my reference that the shape of this recovery is likely to be a “square-root” shaped (see From V to L: What will the recovery look like?). The Oregon Office of Economic Analysis provided a stylized answer. Expect an initial partial V-shaped bounce back, followed by a slower pace of growth, whose shape will be a function of policy, demand, and the amount of permanent economic damage.

In conclusion, I have analyzed the market using a variety of techniques. All of them lead to the conclusion that a major market bottom has not been reached yet.

- Long-term market psychology

- Technical cycle analysis

- Valuation

- Smart investor behavior

While this is an excellent analysis, the lingering question is whether the Fed will continue to do everything to prop up the market. I’m sure Powell is under tremendous pressure to avoid further down draft. There is never been this type of intervention before from the Fed. Thoughts?

It takes a combination of fiscal, monetary, and public health policy to get the global economy out of this crisis. The first two can only buy time, they cannot find a treatment or vaccine.

Put it another way, if we got a Zombie Apocalypse, will tax cuts, rate cuts, and QE solve the problem?

Cam appreciate the insight – and the answer is not easy as many camps out there expecting we will go back and test March lows. A couple of observations – Berkshire raised that cash at what rate of interest ? (with cash so cheap – would consider that bullish) also they issued a 1B EUR bond with 0% interest – I would also consider that bullish for them? Listening to Tommy Lee – he is seeing more beaten up stuff bounce which happened in 09 – why would restaurants such as DRI be making a higher low. BTW did we get a Zweig thurst signal last week as not sure with the stock charts data. Thanks

The ZBT signal missed. We did not get the buy signal.

Cam, I am seeing a lot of parallels between current market and what we saw in 2011 at the time of European debt crisis. Then as now, market saw a quick 50% retracement of decline and then went sideways in a choppy fashion for many months before rising again in 2012. This time could be similar as we await a treatment/vaccine to become available over next few months. Thoughts?

Great analysis, clear and concise.

It has been an amazing retracement rally. If we define faith as confidence in outcomes that have yet to materialize, then it may be appropriate to call it a rally based on faith in the Fed/ public health policies/ modern medicine.

When I talk to family/ friends/ colleagues, in general their faith is evident – we all want to be optimistic. But we all harbor nagging doubts as well – the response to this global pandemic feels outsized to the point where no one is able to predict/ price in the economic fallout.

I did this blog post this week. Just my 2c. I keep running into variations on the “quick in and out” economic scenario. Most disturbingly among professional investors and other people who should know better. I think this reflects a consensus that hasn’t moved past the “Denial” phase of the stages of grief (followed by Anger, Bargaining, Depression, and Acceptance).

I see a long, sluggish recession as the most likely scenario after so much economic disruption.

Consensus seems to expect a quick in-and-out. I think that is insane. The economic equivalent of WW1’s “The war will be over by Christmas… 1914, 1915, 1916, 1917, 1918?!?” Here’s a reality check.

When Do You Think Disney World Will Re-Open?

Keep in mind the park only works with a certain (very large, continuous) volume of people flowing through it. My answer is either:

After we have a widely available vaccine – so 2021 at earliest given production ramp-up times etc…

Shortly before we go through another massive resurgence of the virus (sparking and another economic tailspin). Maybe after a “Economic Grand Re-Opening” in late summer keyed to a desperate effort to re-elect Trump.

Neither scenario above solves for getting back to normalcy in the next 6-12 months. Which also doesn’t solve for a return to prior valuation levels – the Fed’s dollars be damned.

If it works better for you, ask whether March Madness 2021 1). happens at all? 2). happens in empty arenas?

US government was supposedly going to bail out in 1965, from Vietnam (see documentary by Ken Burns). It did not, for a good part of next decade.

More to your point, no one knows how this epidemic will end and for how long will it lasts. Greg Ip (WSJ; referenced by Cam) is on record that it is not the depth but the length of recession that is the key here.

Regarding ZBT, am I correct that it missed according to the “within 10 days” rule but would have triggered had the rule been “within 13 days”?

It would have triggered on either day 12 or 13 had the window been longer, but the last time the signal came late the market topped and traded sideways.

Very interesting — thank you!

Re the Fed. There is a certain “wizard of oz” faith in all the noise and smoke coming out of the Fed, but we know precious little of that easing is reaching main street business or consumers. The various lending plans are bogged down in private bank’s red tape and the Fed is too arms length to go direct. One could argue that the Fed’s $$ can prop up the big (public) companies, but this ignores those companies foundations in that real world economy. I think the underlying problem is that a lot of investors living in affluent enclaves have lost any personal or emotional connection to that “real world economy.” Average people are seen more as chess pieces on a board than as human actors with capacity for independent action (ie to stay at home as much as possible until there’s a vaccine). Not meant polemically, just that I don’t think the chess pieces are going to obediently go back to consuming when they know as well as we do there’s a deadly virus rampaging out there. ANd if they don’t go back, the economy doesn’t re-start.

Having gone through the 2008 crisis as a research analyst at a (very large) fund complex and 2000 as a sell-sider, Cam is 100% right about bottoms up estimates being worthless. No analyst out there would even try to defend their current estimates, which should all carry *(placeholder) notations. Pointless to try and update them with earnings season coming up so soon. Too much guesswork. My guess (and current bet) is the last two weeks rally, which has happened during quiet period, dies a death of a thousand cuts when earnings start next week. Company after company will kitchen sink every piece of bad news they’ve been storing up, confirm how awful March has been, lack of visibility, and hammer home the difficulties in re-starting.

So, in your opinion, raising cash now, is a good idea?

Hi Cam,

I think by now everyone understands that downward EPS revisions will be massive, and the key question here is can FEDs “Buy Everything” stimulus offset that kind of EPS drop, and could QE of this size distort your analysis comparing this Bear market with historical Bear markets moves which DID NOT have such large safety net from the Fed?

I don’t recall if we covered this before, but Mark Hulbert wrote an article where he used previous bear markets to judge when we might actually find the bottom. His analysis arrived at two average dates to consider for an actual bottom. June 14th and August 7th. Given that this bear was unusually swift to reach an initial bottom and the rally was breathtaking, I think we may also see the subsequent retest run equally ahead of schedule. Therefore, the eventual bottom could conceivably be reached in May or June but, of course, anything is possible.

https://www.marketwatch.com/story/stocks-will-revisit-their-coronavirus-crash-low-and-heres-when-to-expect-it-2020-04-09?mod=mark-hulbert

Thanks for the insights Cam. Beffet also sold 30 million USD worth of Bank of New York Mellon stocks this past week, amid the rally: https://www.barrons.com/articles/warren-buffett-berkshire-hathaway-sells-bank-of-new-york-stock-51586467957

By the way, I would be very interested if you can share more stories/experience of your career at Myrill Lynch. Quite a few very good technical analysts I follow worked for Myrill Lynch, including John Murpy.

You mean Walter Murphy? Walter is on Twitter at @waltergmurphy

No, I meant John Murphy, who currently writes for Stockcharts. He worked for Merrill Lynch I believe back in the 1970s. My own analytical framework has been heavily impacted by his books and articles, especially on intermarket analysis.

Your and Fred Meissner’s reports are also among my favouriate.

Consumer psychology, sentiment, and behavior will be key going forward. Sixteen million have already lost their jobs. Millions more will in coming months in-spite of all the stimulus. They will get unemployment and cash payments. But how are they going to think about it? They will hunker down and spend as little as possible. People who still have jobs are worried about what’s in the future. They are going to hunker down and build their savings. From a health perspective, even if there is a therapeutic that is 95% plus effective, who would want to take a chance of getting sick with a virus that is still evolving and not well understood. So, till there is a vaccine, consumers will be defensive in their outlook. A vaccine is not expected till sometime in 2021. That itself puts the recession lasting at least that long.

The stock market will start anticipating these events by late summer and start to recover. Will the earnings get back to 2019 level with a multiple of 18-20 in 2021? I think so.

Short term, lot of pain and uncertainty. How bad? I think Cam has outlined some decent goalposts.

All good points. I might add that the drugs currently being used and those under investigation aren’t without risks of their own. With regard to the ‘cure being worse than the disease,’ it’s not just the economic disruptions that will exact a price – sometimes adverse reactions and/or permanent damage (to vital organs and/or nerves) make prevention many times preferable to treatment.

An interesting article on the World Economic Forum website

https://www.weforum.org/agenda/2020/04/mapping-covid19-recession

by a serious economist, Kenneth Rogoff:

https://en.wikipedia.org/wiki/Kenneth_Rogoff

He is not too sanguine about this recession.

One more interesting article about how we come out of the virus mess:

https://www.vox.com/2020/4/10/21215494/coronavirus-plans-social-distancing-economy-recession-depression-unemployment

This article references 4 plans across a wide political spectrum: “There’s one from the right-leaning American Enterprise Institute, the left-leaning Center for American Progress, Harvard University’s Safra Center for Ethics, and Nobel Prize-winning economist Paul Romer.”

Like you had anything else to do on Easter!!

Good analysis. We are seeing real life app of Stephanie Kelton’s MMT. The key point is that so called fiscal balance or responsibility is basically a facade of one Potemkin village. The system is just left hand paying right hand. Jay Powell has admitted as such: we don’t run out of ammo and that doesn’t happen, just a few weeks ago. Let us see how this distorts market.

Last week German CB started directly funding its government. I would think what is happening might have a tremendous effect on large investors, especially those with firm belief of classical money concept.

Ray Dalio just doubled down on “Cash is Trash.” He perhaps is talking his book. But we have to observe how asset classes respond to these dramatic rethinking. Perhaps this is a turning point in investing.

Scientific progress is made at the pace of one funeral at a time. But market rethinking happens at rapid-fire speeds. Profit incentive is the ultimate driving force of all.

Cam, curious as to your “unlikely depression” call. Investopedia/Wikipedia define a depression as a really long recession (ie 3 years) OR > 10% GDP drop. Are you using a different definition or don’t think a 10% GDP drop is likely?