Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Asset Allocation Model is an asset allocation model that applies trend-following principles based on the inputs of global stock and commodity prices. This model has a shorter time horizon and tends to turn over about 4-6 times a year. The performance and full details of a model portfolio based on the out-of-sample signals of the Trend Model can be found here.

My inner trader uses a trading model, which is a blend of price momentum (is the Trend Model becoming more bullish, or bearish?) and overbought/oversold extremes (don’t buy if the trend is overbought, and vice versa). Subscribers receive real-time alerts of model changes, and a hypothetical trading record of the email alerts is updated weekly here. The hypothetical trading record of the trading model of the real-time alerts that began in March 2016 is shown below.

The latest signals of each model are as follows:

- Ultimate market timing model: Sell equities

- Trend Model signal: Neutral

- Trading model: Bullish

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers receive real-time alerts of trading model changes, and a hypothetical trading record of those email alerts is shown here.

Subscribers can access the latest signal in real time here.

Still a single macro trade

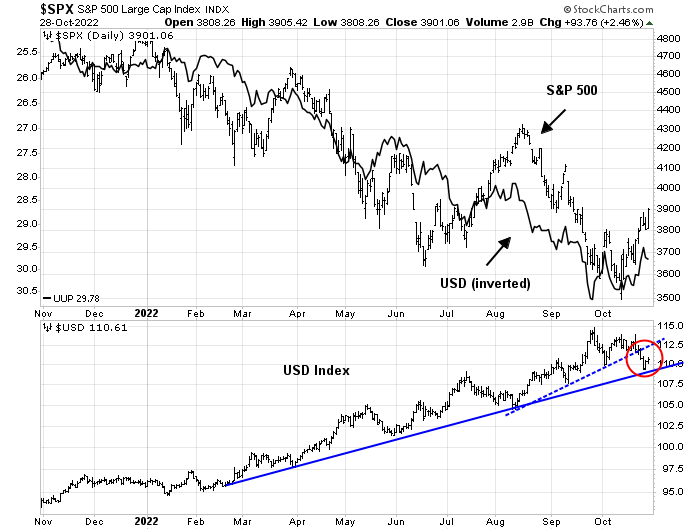

How should investors interpret the recent risk-on episode? It’s all still one big macro trade. The S&P 500 continues to be inversely correlated to the USD Index, which is mainly driven by the expectations of a less hawkish Fed. The USD Index helpfully broke down through a minor rising trend line, which is a positive sign for risk appetite.

I call it the Fed Whisperer rally (h/t Walter Deemer).

Earnings, earnings!

There is no question that earnings matter and the stock market faced headwinds from disappointing earnings results from large-cap technology giants. While the Street has questioned the long-term viability of META’s business model, the challenges faced by the other FANG+ names are cyclical in nature. The primary driver of large-cap growth stock relative performance continues to be the 10-year Treasury yield.

That said, the NASDAQ TRIN spiked above 2 on Thursday, which was before the Apple and Amazon earnings reports. This is an indication of blind panic selling in large-cap growth stocks.

Setting aside the problems of Big Tech, earnings results weren’t all bad. Investors saw strong positive results from the cyclical generals, such as General Motors and General Electric, as well as other cyclically sensitive industrial stocks, all of which reported results last week.

Mid and small-cap leadership

Here are some possible positives that are likely not fully discounted by investors. Even as the S&P 500 rally began to stall under the weight of tech earnings, small and mid-cap stocks were undergoing a stealth advance. The midcap S&P 400 is already in a choppy relative uptrend against the S&P 500. The small-cap S&P 600 achieved a relative breakout, while the Russell 2000 is testing a key relative resistance zone.

In other words, market breadth is stronger than it appears on the surface.

Fading geopolitical risk

Here are some other things that could go right. I have written before about the signs of fading geopolitical risk, as measured by the relative breakout achieved by MSCI Poland.

While this is not my base case, unrest in Iran sparked by a backlash against restrictions against women could topple the government in Tehran, which would be energy bearish but risk appetite bullish. The Economist summarized the protests in Iran this way:

Dictatorships tend to fall the way Ernest Hemingway said people go bankrupt: gradually, then suddenly. The omens can be obvious with hindsight. In 1978 Iran’s corrupt, brutal, unpopular regime was besieged by protesters and led by a sick old shah. The next year it was swept away. Today Iranian protesters are again calling for the overthrow of a corrupt, brutal regime; this time led by a sick old ayatollah, Ali Khamenei. As Ray Takeyh, a veteran Iran-watcher, put it, “History…is surely rhyming on the streets of Tehran.”

Pessimists caution that mass protests have rocked Iran’s theocracy before, notably in 2009 and 2019, and the regime has always snuffed them out by shooting, torturing and censoring. Yet there are reasons to think that this time may be different; that the foundations of the Islamic Republic really are wobbling.

The challenge for the regime is whether the security forces would obey orders to use deadly force on women, or whether entrenched interests would acquiece to such harsh levels of oppression.

Yet however much the mullahs may want to crush these unruly women, they cannot be sure that the security forces would obey an order to shoot them in the street, or that the fury that would follow mass femicide could be contained.

Previously, when faced with protests, the regime has called on its supporters to stage counter-demonstrations. This time, hardly any have shown up. And several grandees who might in the past have condemned the protests or voiced support for the regime have conspicuously failed to do so. For now, Iran’s generals say they back Mr Khamenei. But it is unclear how far they will go to support an out-of-touch 83-year-old who wants to install his second-rate son as his successor. When protests in Egypt got out of hand in 2011, the top brass elbowed aside the unpopular president (who was also grooming his son as his heir) and allowed a brief flowering of democracy before eventually seizing power. In Iran, as in Egypt, the top brass have vast, grubby business interests to protect. If they sense the supreme leader is sinking, they have no incentive to go down with him.

Moreover, the collapse of the Iranian government would deprive Russia of an ally and arms supplier, which would pressure the Kremlin to end the Russo-Ukraine war, which would be another bullish development.

The week ahead

In the wake of a slowing core PCE print of 0.5%, which was in line with expectations, compared to a downward revision of 0.5% from 0.6% in August, I reiterate Jim Paulson’s analysis of S&P 500 returns when inflation is decelerating (see How inflation is a game changer for portfolios).

Tactically, the current rally may have further upside potential. The market is anticipating a 75 bps hike at the November FOMC meeting, followed by two consecutive 50 bps hikes at the next two meetings, and a terminal rate of 475-500 bps, which is already the base case scenario.

San Francisco Fed President Mary Daly has said she could support slowing rate hikes to 50 and 25 bps hikes at subsequent FOMC meetings. If the Fed were to signal such a dovish path, it would spark a further risk-on rally. The probabilities are asymmetric. At worst, the Fed will behave in line with expectations and at best it will spark a risk-on episode.

Credit Suisse pointed out that the dovish central bank surprises have recently outnumbered hawkish ones. Will the Fed continue that trend next week?

Here’s where Fed watching gets a little tricky. What ultimately matters to the market isn’t whether the Fed slows to a 50 bps hike at the December FOMC meeting, but the level of the terminal rate. Investors are seeing some very different messages from the rates market. The 2-year Treasury yield (black line), which can be a proxy for market expectations of the terminal rate, has been trending up but recently pulled back to 4.4%. The 5-year breakeven rate (red line) has trended downwards and recently steadied. Arguably, this rate signal is overly noisy because it’s based on the TIPS market, which has been dominated by the Fed and may produce a false market signal. The 5×5 year rate (blue line) has traded sideways for all of this year. Which market signal should investors believe?

In the meantime, the equity bull party is in full swing. The S&P 500 regained its 50 dma on Friday, which gives it a shot at its inverse head and shoulders measured objective of about 4120, which is also the site of its 200 dma.

Bullish traders should enjoy the party, but be aware that event risk is rising.

Disclosure: Long SPXL

From Yahoo Finance. Harnett has been very accurate in his calls throughout this bear market. Supports Cam’s Q4 tactical rally call.

Bank of America strategist Michael Hartnett is waiting for a blowout in credit spreads before going all-in on stocks, according to a Friday note.

That’s because he still expects a recession shock to materialize in the coming months, which would drive stocks to new lows in the first quarter of 2023.

Higher interest rates in particular could have an outsized, but delayed, impact on the economy as central banks around the world seek to tame inflation. According to Hartnett, global central banks have implemented 243 rate hikes so far in 2022. “That’s 1 rate hike [for] every trading day.”

Rate hikes take time to work their way through the economy, and the end result is a recession, according to the note. “Bond market now pivoting from inflation to recession,” he said, adding that a fourth-quarter rally in risk assets could materialize as some central banks “blink” on their current tightening policy.

“But we say ‘recession shock’ equals new highs [in] credit spreads [and] new lows [in] stocks in Q1,” Hartnett said, adding that the “recession trade is always long bonds, short stocks.”

Credit spreads will often surge to higher levels when uncertainty in the stock market and economy reaches a crescendo. The spreads measure risk appetite in credit markets, as investors demand higher yields when buying at a time of heightened risk.

But so far, credit spreads have remained relatively subdued. The ICE BofA US High Yield Index Option-Adjusted Spread was at just 4.76% as of Thursday, still below the July peak of about 6% and the March 2020 peak of nearly 11%. During the Great Financial Crisis, the spread hit a high of nearly 20%.

While a bear market rally could send the S&P 500 to 4,000, it will still be too early for the Federal Reserve to pivot away from its current rate hike policy, according to the note.

“Norm is Fed starts cutting only once US unemployment rate [gets above] 5.5%; and rising unemployment rate normally means higher defaults and wider credit spreads,” Hartnett said. The US unemployment rate

“If like us you believe job losses mean new highs in spreads it’s a bear market rally, lows yet to be seen, and rules of road remain,” he said.

And one of those rules means investors should wait on buying stocks: “Once credit spreads show recession priced-in, we are all-in.” So far, that’s no where near close to happening.

Cam,

Republicans are expected to take control of both Houses after the mid-term. How does that impact the direction of the stock market? What sectors may benefit?

We can expect more stalemate and hopefully some constraints on fiscal policy.

Also what are your views on the USD going forward? The US interest rates and the USD are driving the markets everywhere.

Thank you.

Momentum is finally outperforming.

Momentum ETFs do well when leading market sectors lead for a long time. The last few years have seen sectors flip, flop from leading to lagging badly too quickly. You can see on a chart of the three big momentum ETFs (iShares MTUM, Invesco SPMO, Fidelity FDMO) have underperformed (relative 6-month performance under zero) for most of the last two years. That has now changed. I believe momentum is in for a good long run.

Invesco SPMO has performed better. Recently, last week, the Fidelity FDMO sagged when the FAANG stocks, which it owns, fell. SPMO and MTUM have migrated to owning quality, Value and Low Volatility oriented stocks and kept rising when FDMO fell.

Thanks. SPMO – oil plus BRK plus KO. Looks like a double dose of oil, soda and staples.

top 10 components:

Exxon Mobil Corporation 9.62%

UnitedHealth Group Incorporated 7.79%

Chevron Corporation 6.87%

Berkshire Hathaway Inc. Class B 4.43%

Eli Lilly and Company 4.21%

AbbVie, Inc. 4.03%

ConocoPhillips 3.17%

Merck & Co., Inc. 2.86%

PepsiCo, Inc. 2.77%

Coca-Cola Company 2.68%

China is crashing (down 36% in two months), sucking Asian neighbors down with it. America and the Developed World next?

Everything is falling in China together. This is just not the China Internet stocks falling.

There have been huge drops in just the last few weeks. Also, Emerging Markets especially Asia, have been caught up in the problem with Emerging Ex-China EMXC is very weak.

The Asian junk bond ETF KHYB continues to fall. The crash in Asia will signal an end when this Asian junk index turns up and stays rising, not before. Junk of any country is the health gauge of their business conditions,

Commodities ex-energy are falling hard with China problems the likely cause.

Mustn’t this have an American and global negative stock market impact? The American GFC spread weakness to the world.

I step back and look at the S&P 500 down 17% from its tulip bulb crazed, zero interest rate, Fed pumping, FAANG loving, high point. This seems minor damage when we consider Fed rates have gone in a year from free money to hurtful levels along with massive inflation and a war.

So, buying this market for a, let’s say, a 7% gain, would then have the S&P down just 10% heading into a recession of unknowable depths and damage to earnings. This doesn’t jive.

I understand the technical and sentiment indicators are set up like bear market lows of the past twenty years, But the macro background both in America and abroad, screams “This time it’s different”.