Ahead, of the upcoming FOMC, meeting, what is the market discounting? I conduct a factor and sector review for some answers. Starting with a multi-cap review of value and growth, value stocks have been outperforming growth stocks within large caps since early August, but this has not been confirmed by mid and small caps. The value and growth relationship has been mostly trendless since June.

Sector review

Here is a deeper dive into the value and growth framework. The relative performances of the growth sectors relative to the S&P 500 are weak. Communication services has been in a relative downtrend for about a year (thank you, META). Technology topped out on a relative basis in August, and consumer discretionary, which is dominated by the heavyweights AMZN and TSLA, has been weakening since mid-September.

The value sectors are showing some signs of life. Financial, industrial, and energy stocks have been in relative uptrends since August, while materials and the equal-weighted consumer discretionary sector, which reduces the effects of AMZN and TSLA, have moved sideways.

For completeness, most of the defensive sectors, with the exception of healthcare, are trading flat to down relative to the S&P 500.

Signs of a cyclical rebound

A deeper dive into some of the sectors reveals signs of a cyclical revival. The top panel of the following chart shows the relative performance of large and small cap industrials relative to their respective benchmarks (black=large cap industrials to S&P 500, green=small cap industrials to Russell 2000). The bottom panel shows the relative performance of small and large caps (black) and small cap industrials to large cap industrials (green). Both panels show that small cap industrials are showing better relative strength, which confirms the signs of cyclical strength.

While large cap material stocks have mostly been trading sideways relative to the S&P 500, small cap materials have been beating their small cap benchmarks. This is another sign of a cyclical rebound.

From a global perspective, the cyclical rebound theme is confirmed by the BASF/Dow Chemical pair. Both are large cap commodity chemical companies, with BASF headquartered in Europe and Dow in the US. Both stocks tracked each other closely until the start of the Russo-Ukraine war, when BASF tanked on a relative basis because of higher European energy costs. The BASF/Dow pair achieved a relative breakout, indicating a cyclical revival in Europe despite a

Reuters report that BASF needs to permanently curtail some of its European operations because of high energy costs.

Joe Wiesenthal at Bloomberg pointed out that, beneath the surface of weak PMI readings, the industrial sector is mostly showing signs of strength.

By contrast, small cap financial stocks are not showing the same degree of outperformance as their large cap counterparts.

Why the bond market matters

The relative performance of financial stocks has been correlated to the shape of the yield curve. While the 2s10s yield has moved sideways since early August, large cap financials have outperformed. Large cap financials are anticipating a steepening of the yield curve, which is the bond market’s signal of a cyclical rebound, while small cap financials have not.

The bond market also matters from a cross-asset perspective. The poor relative performance of large cap growth, as measured by the NASDAQ 100, is inversely correlated to the 10-year Treasury yield. What the Fed does in the upcoming meeting and in future meetings matters.

Waiting for the Fed

How is the Fed likely to react? While the Fed is likely to raise rates by 75 bps at the November meeting, a debate is raging about the pace of future rate hikes. Fed Governor Lael Brainard and San Francisco Fed President Mary Daly have cast their lot with “Team Decelerate” (rate hikes). The Bank of Canada surprised the markets last week by raising by 50 bps instead of the anticipated 75 and cited financial stability concerns in its statement. Will this be the start of a trend of central bankers tempering their rate hikes?

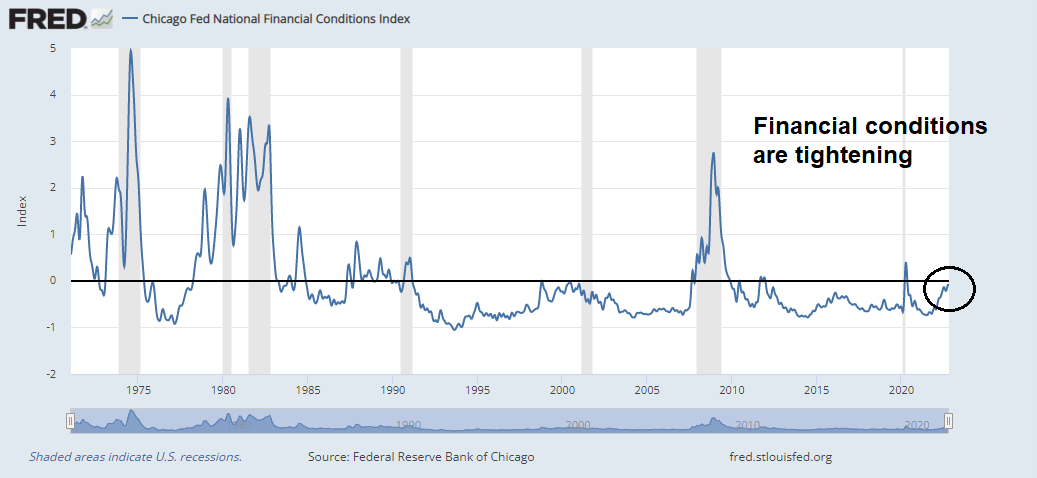

Here are some of the data points that Fed officials are watching. Financial conditions have tightened, but monetary policy operates with a lag. Is it time to slow down the pace of the rate hikes and monitor the effects of past monetary tightening?

Since Brainard and Daly made their “Team Decelerate” pivot, the market reacted by edging up inflation expectations, though they retreated slightly later. This raises the risk of inflation expectations becoming unanchored.

Yield spreads shows a mixed picture. US high yield spreads have narrowed while emerging market spreads have widened, indicating a rising risk of global financial instability from growing offshore USD stress.

The closely watched September core PCE release, which is the Fed’s preferred inflation metric, came in at 0.5%, which was in line with expectations. Moreover, the August figure was revised down from 0.6% to 0.5%. The Dallas Fed’s Trimmed Mean PCE also showed similar signs of deceleration.

As well, the Q3 Employment Cost Index came in at 1.2%, which was also in line with expectations, and represents a slowdown from 1.3% in Q2. As a reminder, Fed Chair Jerome Powell explained one of the reasons why he pivoted to a tighter policy was because of the strong ECI at the

December 2021 FOMC press conference.

So coming to your real question, we got the ECI reading on the eve of the November meeting—it was the Friday before the November meeting—and it was very high, 5.7 percent reading for the employment compensation index for the third quarter, not annualized, for the third quarter, just before the meeting. And I thought for a second there whether we—whether we should increase our taper, [We] decided to go ahead with what we had—what we had “socialized.” Then, right after that, we got the next Friday after the meeting, two days after the meeting, we got a very strong employment report and, you know, revisions to prior readings and, and no increase in labor supply. And the Friday after that, we got the CPI, which was a very hot, high reading. And I, honestly, at that point, really decided that I thought we needed to—we needed to look at, at speeding up the taper. And we went to work on that. So that’s, that’s really what happened. It was essentially higher inflation and faster—turns out much faster progress in the labor market.

These releases should keep the Fed on a path to the more dovish policy that was telegraphed just before the media blackout.

Not all pivots are the same

In conclusion, the market is starting to discount a cyclical rebound, but much depends on Fed policy. Even if the Fed were to signal an imminent pause in rate hikes, that’s not necessarily very equity bullish.

Rob Anderson at Ned Davis Research observed that not all Fed pivots are created equal. Rate cuts and QE announcements are the most bullish, while rate pauses and the end of tightening cycles have resolved with below average gains in the S&P 500.

The Fed can do what it wants, but what about congress?

So no matter what rate we end up at, will this stop government spending? Short answer, NO!

There are so many examples of super high inflation rates and high interest rates, how often do the governments willingly cut back on spending? When the interest cost on the debt exceeds 1 trillion a year, will they cut back on SS, Medicare, the military….not willingly. What will this do to inflation? My take is it will go up even if the Fed takes it to 20%…but if the USD is strong enough, and we get a recession, they may use the temporary dip as an excuse to get out of Dodge. Never mind supply chain bottlenecks, what about resource scarcity, pick a commodity like oil or copper or lithium or gold….have there been any huge discoveries of really rich deposits? Will they be cheaper to extract, and what will replace them. So I will bet on inflation…not sure how to do that, but it’s in the cards. Oh yes, if we get a baby with the bathwater moment, buy blue chip resource companies, and sell some before the politicians want to tax their “windfall profits”

Agree with your premise of commodities and oil. I also like gold.

Gold I am mixed about.

It has a long tradition which is a plus, it is concentrated wealth and can be moved easily. But it has been hoarded for millennia, and the above ground stockpile is enough to last over 100 years of commercial use. Imagine if the strategic petroleum reserve was I dunno a few trillion barrels, would one expect the price of oil to go to the moon? Of course if they use gold to back a digital currency, the price would go to the moon, so would oil. But gold has this history, and is widely accepted, and you can carry a good amount in a pocket.

But I prefer silver because it is consumed, it has a built in supply bottleneck in that 75% mined is as a byproduct, and it is incredibly useful and built into the electronics manufacturing. You can’t simply put something else in it’s place. Also if they find a way to get gold from seawater, there are a few cubic miles in there…it would put a ceiling on the price a ceiling which likely would be higher proportionately for silver.

But some gold is a good idea…for now I am looking at writing some puts on slv, if the price holds I get the premium, if it goes down I can either roll over the put, or take the SLV as a way of accumulating at a better price. I am waiting for a recession which should make SLV drop to buy in quantity.

Just remember that gold is inversely correlated with USD. USD is affected by Fed policy, or expectations about Fed policy.

All eyes on Wednesday’s FOMC meeting.

Yes, but I am thinking long term.

The Fed will do as it wishes (or has to) but ultimately the debt will prevail. I think gold and silver are currently in downtrends but long term unless there is some kind of technological breakthrough, I expect a higher price unless this time is really different.

Human nature, the elites, they don’t change, which is why I think it is time to reread the book by Rogoff and Reinhart. I think the magician the Fed will cause a recession and ergo inflation will drop and then while we are all watching this, they do something else while saying inflation is down.

I keep expecting a new rule change mandating that a certain % of our IRAs is in treasuries, which considering how in 1933 we had to turn in our gold is not impossible, but not something one can do much about. It would provide a big buyer for debt, which is in the same in a sense to 1933…more money for the gov’t to spend.