I pointed out two weeks ago the strong disagreement between technical analysts, who were bullish because of strong price momentum, and macro investors, who were bearish because of concerns over hawkish central bank policy and a slowing growth outlook (see “Price leads fundamentals”, or “Don’t fight the Fed”?). In the wake of the market reaction to the Fed’s Jackson Hole symposium, it seems that macro investors have won the argument, at least for the time being.

In Fed Chair Powell’s

speech, he underlined that tight monetary policy will “bring some pain to households and businesses” but vowed to “keep at it until the job is done”, which was a signal that there will be no dovish pivot until inflation is beaten. The only exception to that rule is a financial crisis. Historically, equity markets haven’t bottomed until the St. Louis Fed Financial Stress Index has risen to positive. While the index has begun to turn up from a very low level, stress levels are still very tame, indicating that financial crisis risk is still relatively low.

The hawks at Jackson Hole

The speeches at Jackson Hole were, on the whole, brutally hawkish.

Powell’s speech, which contained 47 instances of the word “inflation”, began with a stark warning about the effects of Fed policy:

Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. Reducing inflation is likely to require a sustained period of below-trend growth. Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.

Powell went on to outline the extent of the Fed’s hawkishness: “With inflation running far above 2% and the labor market extremely tight, estimates of longer-run neutral are not a place to stop or pause.” He went on to discuss how inflation expectations ran out of control during the 1970’s.

During the 1970s, as inflation climbed, the anticipation of high inflation became entrenched in the economic decisionmaking of households and businesses. The more inflation rose, the more people came to expect it to remain high, and they built that belief into wage and pricing decisions.

A San Francisco Fed study found that “wage inflation is sensitive to movements in household short-run inflation expectations but not to those over longer horizons”. The latest ADP report shows that job stayers saw annual wage gains of 7.6%, while job switchers saw gains 16.1%. Fed officials will undoubtedly be closely monitoring wage gains and short-term inflation expectations. Powell concluded, “We must keep at it until the job is done.”

That was just the appetizer. A closely watched

speech by Isabel Schnabel, who is a Member of the ECB Executive Board, was equally hawkish. She acknowledged that supply shocks are mainly responsible for the latest bout of inflation, which is beyond the control of central banks. Nevertheless, she laid out a case for tight monetary policy as a response.

- Uncertainty about inflation persistence requires a forceful policy response.

- Risks of a de-anchoring of inflation expectations are rising.

- Central banks are facing a higher sacrifice ratio when high inflation has become fundamentally entrenched in expectations.

Schnabel echoed Powell’s sentiments about the risks of allowing inflation and inflation expectations to run out of control.

Both the likelihood and the cost of current high inflation becoming entrenched in expectations are uncomfortably high. In this environment, central banks need to act forcefully. They need to lean with determination against the risk of people starting to doubt the long-term stability of our fiat currencies.

Regaining and preserving trust requires us to bring inflation back to target quickly. The longer inflation stays high, the greater the risk that the public will lose confidence in our determination and ability to preserve purchasing power.

I don’t want to sound like a broken record, but Gita Gopinath, First Deputy Managing Director of the IMF, sang from the same songbook in her

remarks: “Central banks must act decisively to ensure inflation expectations are anchored”.

As well, an important financial market plumbing

paper by Acharya et al about the effects of quantitative tightening concluded that the effects of QT are not a mirror image of QE. Instead, “the shrinkage of the central bank balance sheet is not likely to be an entirely benign process” as QT effects are non-linear.

During quantitative tightening, the banking sector may not shrink the claims it has written on liquidity at the same pace that the central bank withdraws reserves. This may lead to tightened liquidity conditions and the greater possibility of episodes of systemic liquidity stress.

The paper’s discussant,

Wenxin Du, pointed out that the Acharya paper found that “no robust relationship between aggregate reserves and the price of liquidity”, as measured by the spread between the effective Fed Funds rate (EFFR) and interest on reserve balance rate (IOR). However, there is a strong relationship between liquidity and reserves in foreign entities (FBOs) instead of US banks. When QT drains liquidity from the financial system, it raises the risk of emerging market instability.

For investors, the key takeaway from Jackson Hole is hawkish Fed and other major central bank policy for as far as the eye can see.

Subsequent to the Jackson Hole symposium, Minneapolis Fed President Neel Kashkari astonishingly admitted in a

Bloomberg podcast that the Fed wants stock prices to fall: “I certainly was not excited to see the stock market rallying after our last Federal Open Market Committee meeting, because I know how committed we all are to getting inflation down. And I somehow think the markets were misunderstanding that.” Kashkari went on to underscore the Fed’s seriousness in its inflation fight by stating that “a commitment of returning inflation to 2%” is a form of forward guidance.

In other words, if you’re an equity bull, you are fighting the Fed.

Signposts to watch

In light of the hawkish rhetoric from Fed officials, the next important signpost is the Summary of Economic Projections, which is scheduled to be published after the September FOMC meeting on September 21, 2022. Watch for how the neutral rate evolves, which stood at 2.5% in June. As well, watch for how much over and overshoot of the neutral the Fed is willing to tolerate based on its projections for 2022, 2023, and 2024.

At the extreme, the Taylor Rule prescribed Fed Funds rate under “normal assumptions” is 11.4%, indicating that there is enormous upside potential in rates should the Fed turn really, really hawkish. To underline that point, Cleveland Fed President Loretta Mester expressed a preference “to move the Fed Funds rate up to somewhat above 4% by early next year and hold it there.” She added, “I do not anticipate the Fed cutting the Fed Funds rate target next year”.

Investment implications

What does all this mean for investors? Needless to say, most projections are equity bearish. CEO confidence has fallen to levels which makes a recession unavoidable. Historically, recessions have always resolved in bear markets.

Rob Anderson of Ned Davis Research found that high inflation and below potential growth is a bad combination for equity returns.

There are few historical instances when the Fed deliberately tightened into a recession.

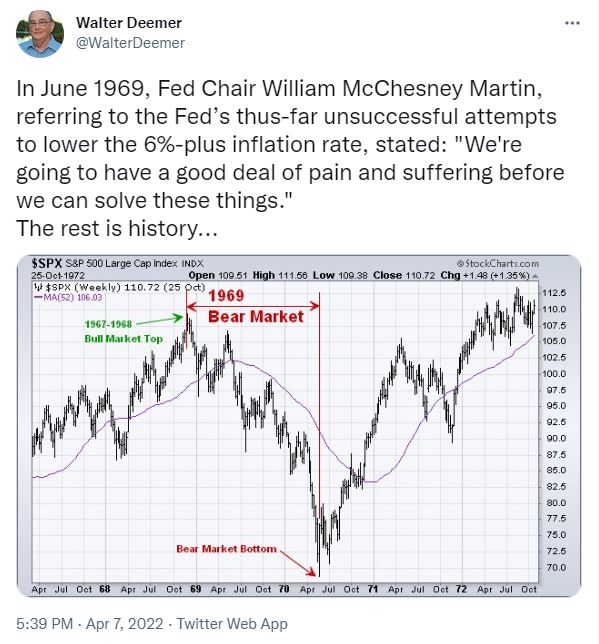

Walter Deemer invoked the 1969 template.

The other is the Volcker Fed of the early 1980’s. Even Volcker pivoted when the Mexican Peso Crisis threatened the stability of the US banking system.

There is one narrow path for the bulls. Central bankers could wrong about the inflation outlook. Inflation surprises have generally been moderating all over the world.

Markets are forward-looking and yield curves are inverting, indicating slower economic growth ahead. In the past, the peak in the long 30-year Treasury yield has been either coincident or slightly led the peak in the Fed Funds rate. While the signal hasn’t been perfect, those episodes have tended to be bullish for risk assets such as equities, and the long bond yield may peaking today.

The August Employment Report came in slightly above expectations, with payrolls rising at 315,000 (300,000 expected) and significantly decelerating from the July rate of 526,000, Both average hourly earnings and average weekly hours were worse than expectations, which indicate a gradually weakening economy. This report is consistent with the Fed’s desire to cool growth and inflation.

Whatever it takes, or…

In reference to the euro, then ECB president Mario Draghi uttered the phrase “whatever it takes” in 2012. Today, central bankers have taken a “whatever it takes” position to fight inflation at the Federal Reserve’s Jackson Hole symposium.

If you believe the Fed and other central bankers, monetary policy is hawkish as far as the eye can see. However, there are two non-linear and narrow paths forward for equity bulls. One is a financial crisis that forces central bankers to pivot to an easier policy to preserve financial stability. The other is the central bankers have misjudged the inflation outlook and markets are right. If long Treasury yields fall in a convincing fashion, it could be the signal for a market-led dovish pivot.

I recognize the tone of this publication is very bearish. Tomorrow, I’ll discuss the bull case from a technical analysis perspective. Don’t slit your wrists just yet.

“I recognize the tone of this publication is very bearish”.

On the contrary, you have made a cogent case of how inflation expectations (CITI Index), are slowly coming down and moving in the right direction (in support of this is the slowing employment numbers, and peaking long bond yield).

The one caveat I would consider is a policy mistake by the Fed that produces a much greater downside to equities, than what we can predict here and now.

Nothing wrong with a ‘very bearish’ outlook if one embraces the bear. Embracing the bear will mean different things to different people, but in general holding high levels of cash or cash equivalents during a downdraft is a very enjoyable experience – one that includes the anticipation of putting the cash back to work at some point.

Excerpt from Bespoke which ties into inflation path discussion.. chart not shown but the concept is clear…

“Aside from last month’s jobs report, we’ve seen a steady number of disinflationary readings over the last month or two. Last month’s CPI number actually showed a slight MoM decline, and another flat reading is currently expected for the August number that’s due out in a couple of weeks. The eye-popping year-over-year CPI readings dominate Main Street headlines, so we thought it would be helpful to show potential trajectories for YoY CPI going out to late next year based on various theoretical constant MoM CPI moves of 0% to 0.4%. Barring another big spike in costs that would go against everything we’ve seen recently, we think a range of 0.0% to 0.4% for MoM headline CPI over the next year is reasonable.

As shown in the chart above, if CPI were to remain unchanged and stay at 0.0% MoM, we would see YoY CPI quickly fall to 3% by next March, and it would be down to 1.36% YoY by next May. If we saw a constant 0.1% MoM move going forward, we’d see YoY CPI down in the 2-3% range by next May. A 0.2% MoM move for CPI would cause the YoY reading to dip to 2.2% by next June, while a 0.3% MoM reading gets YoY CPI down to 3.3% by June. What this shows is that while YoY CPI remains sky-high right now, barring any big surprises, we could see it get back down in the 2-4% range sometime next spring or summer. At the same time, current Fed Funds Futures pricing has the Fed Funds Rate projected to be just under 4% from next March through July when YoY CPI could easily already be back down in the 2-3% range. Earlier this year we heard a lot of talk that we’ve never seen inflation come back down from such elevated levels without the Fed hiking rates above YoY CPI. As our chart shows, this could happen by next spring without the Fed having to hike past 4%. Chair Powell and Co. have certainly done plenty of hawkish jawboning lately, but as long as MoM inflation readings stay around or below 0.3% over the next 6-9 months (which we think is a reasonable expectation based on recent data), YoY CPI will be back down to more normal levels and actually below where futures pricing projects the Fed Funds Rate to be.”

Bespoke’s Twitter account has a lot of good data. These guys are firmly in the camp of lower inflation and decelerating economy.

https://twitter.com/bespokeinvest/with_replies

Cam,

You outlined the bearish case entirely centered on the Central Banks’ hawkishness beautifully.

No disagreement there.

However, as you state, the bull case relies on inflation peaking and declining swiftly, and the economic growth decelerating in months and quarters ahead. I think it is only fair that you expand the bull case in full as well beyond just mentioning a few lines.

There is no doubt that inflation is decelerating. We will likely get down to the 4% level by the end of the year.

The hard part is going from 4% to 2%. If the Fed is intent on staying hawkish until we see the whites of 2%’s eyes, the economy is going into a deep recession and the stock market won’t like that.

The Fed is raising rates and definitely jawboning to bring the market and the economy into submission.

The question is if we enter into a significant economic slowdown, and rising unemployment and the inflation is expected to come down to 4% by year-end, will the Fed pause or will they continue to tighten to bring inflation to their target of 2% and risk a severe recession?

Why is nobody talking about the gov’t? The Fed can raise rates to the moon, but if congress keeps tossing out free money to spare us from the pain, guess what, we’ll have inflation.

For years we have gone down the path of lowering rates, and QE to avoid pain. This was helped by outsourcing to where things could be done more cheaply, and also technology which kept inflation low. That would not have gone on forever, but Covid pulled back the curtain.

So we have supply chain issues, and energy issues, and free money. These all boosted prices.

My fear is that now that the gov’t has done “helicopter money” for the Covid crisis (and I agree that with a lockdown, many businesses would have failed and people gone bankrupt. Could have been done differently), that now helicopter money will become the new normal. After all, a huge chunk of the electorate has little money and is struggling. Who will they vote for?

Please search a paper by Francesco Bianchi of Johns Hopkins University and Leonardo Melosi of the Chicago Fed, “Inflation as a Fiscal Limit,” recently presented at Jackson Hole. It postulate a thesis just like you mentioned here. It is 36-page long, but quite readable. You can skip the math portion you are not into it. The key theme is:

Central banks can always pull the emergency brake. They can always destroy demand. But there’s a problem: Rate hikes may not matter if fiscal policy is perceived as too lax. In fact, the rate hikes may even make the situation worse.

So both of our major parties have found that buying votes work. There will be no turning back. Biden certainly kicked it into higher gear. So we get to witness the unfolding of the postulation. And we will find out if Powell and co can get it done under these circumstances.

‘CEO confidence has fallen to levels that makes a recession unavoidable.’

Looking at the chart, we should be in one or close to entering one. However, the hiring remains robust. A divergence.

The expectations of a likely recession in early ‘23 (in earlier posts) implies a significant decline in demand in coming months. (Other than in 2001-2002 and 2008-2009, recessions have been brief.)

Reported inflation may not come down as fast as many components work with a long lag but the forward trend should be clear.

I think the market was early in its thinking of a pivot in June- august period. Fed’s posture is overly hawkish in face of signs of slowing economy and declining inflation.

Fed’s messaging has been inconsistent, imo. From being data dependent in July to Mester’s forecast of rapid ascent and holding pattern at or above 4% are inconsistent.

https://www.marketwatch.com/story/the-forgotten-depression-of-the-post-pandemic-1920s-has-stark-lessons-for-investors-now-11661973818?mod=mark-hulbert

Big if, but what if we’re headed for another epic crash – we always think it’s not possible, but impossible things happen all the time.

Kashkari made a mistake which raises the odds of a big decline in price. This game is supposed to be covert, opaque, and obfuscating. It is especially important in today’s markets which are 80%+ algo-driven. It risks of a very lopsided imbalance in a very short period of time which our systems cannot handle.

Since Jackson Hole, in merely a week, the put options volume on e-mini sp500 has increased to the highest in five years. Thus a big decline in sp500. If it reverses then it is OK. What if the algo’s continue to drive it further down? It will induce all kinds of mechanical flows into selling.