“Price leads fundamentals”, or “Don’t fight the Fed”?

Posted by Cam Hui -

Wall Street is full of adages. Technical analysts are fond of, “Price leads fundaments” as a way of dismissing macro and fundamental analysis. But traders are also warned, “Don’t fight the Fed”.

A vast gulf is appearing between bullish technicals and macro concerns. The bulls, who are mainly technicians, point to strong price momentum, which may be interpreted as discounting a soft landing for the economy. The bears can be found in macro and valuation, as equity markets are complacent about tight monetary policy and slowing growth.

Who’s right? Should you believe that price is leading fundamentals, or stay cautious and not fight the Fed?

In the short-run, the market is a voting machine – reflecting a voter-registration test that requires only money, not intelligence or emotional stability – but in the long-run, the market is a weighing machine.

Where you stand on the bull and bear question depends on your time horizon. Do you focus on the voting machine or the weighing machine?

The bull and bear cases

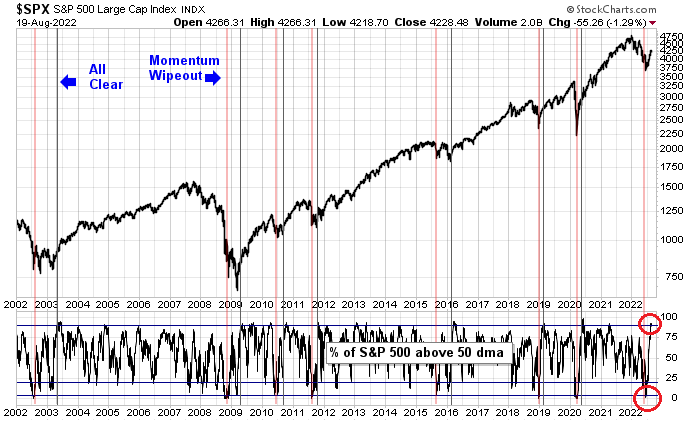

The bull and bear cases can be summarized by two charts I showed last week. The percentage of S&P 500 stocks above their 50 dma fell below 5% in June, a breadth wipeout, and quickly recovered to over 90%. These breadth thrusts are historically impressive and they have always signaled the start of a fresh bull market.

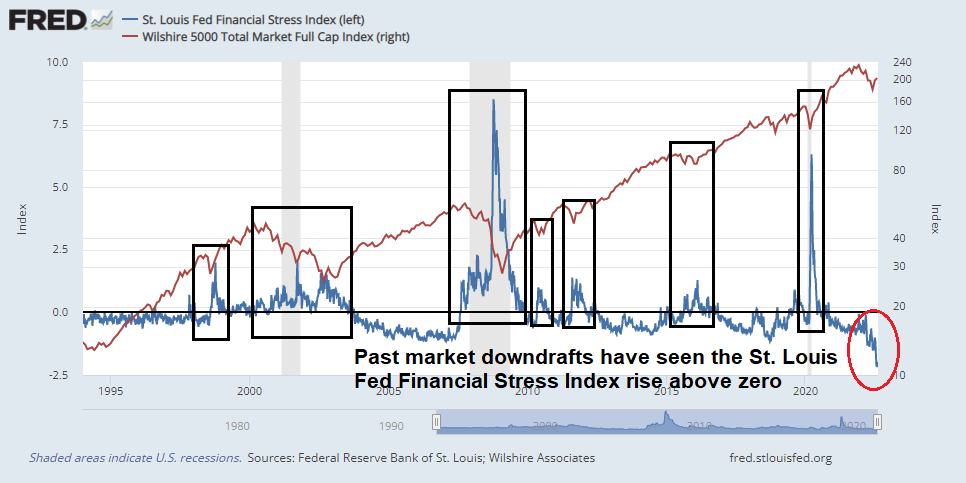

On the other hand, past market downdrafts have never ended until the St. Louis Fed Stress Index has tightened enough to into positive territory. Financial conditions are easing in the face of a Federal Reserve determined to tighten monetary policy. The bear market isn’t over yet.

Both models have shown an accuracy of 100%, but they can’t both be right.

A sentiment rebound

The roots of the breadth thrust begin with a sentiment and positioning wipeout. The BoA Global Fund Manager Survey shows that institutional manager risk appetite had reached a bearish extreme that even exceeded the levels seen at the height of the GFC. The recent softer than expected CPI print sparked a reversal and a stampede to add risk. Prime brokerage data also confirmed that hedge funds had reached a crowded short and reacted to market strength by rapidly covering short positions.

A breadth thrust was born. Rob Hanna at Quantifiable Edges documented the historical record of similar breadth thrusts, and the implications are very bullish for equity returns. The S&P 500 was higher in all cases three, six, and 12 months later.

I would warn, however, that sentiment reversals are not necessarily actionable trading signals. Managers were early in 2008 when they reversed and began to buy, but the market didn’t bottom until several months later.

Macro bears

The bear case consists of two major concerns. The market has totally misunderstood the Fed, which continues to raise interest rates and has no intention of cutting them until inflation is under control. In addition, earnings estimates have only begun to fall and they haven’t fully discounted the probable recession that’s just ahead.

Former New York Fed President Bill Dudley said in a CNBC interview that the markets are misunderstanding what the Fed is up to. Interest rates will be higher and longer, which is contrary to market expectations of a plateau and rate cuts in 2023.

Consider the inflation picture. Dudley stated that underlying inflation is 4-6% and the Fed has a lot more to do in raising rates. The need to be confident that inflation will return to 2%. Dudley dismissed the recent deceleration by attributing the softness to transitory inflation. If your intention is to ignore transitory inflation on the way up, you also need to ignore it on the way down.

Recall that the Fed turned hawkish when the components of CPI began to broaden out, as measured by the Sticky Price CPI and Trimmed-Mean CPI. Both of these metrics remain elevated even as core CPI rolled over.

The July FOMC minutes betrayed a hawkish tilt as there is a “significant risk” that inflation would stay elevated.

Participants judged that a significant risk facing the Committee was that elevated inflation could become entrenched if the public began to question the Committee’s resolve to adjust the stance of policy sufficiently. If this risk materialized, it would complicate the task of returning inflation to 2 percent and could raise substantially the economic costs of doing so.

While Fed officials did acknowledge that the Fed could tighten more than necessary, the risk was not described as “significant”.

Many participants remarked that, in view of the constantly changing nature of the economic environment and the existence of long and variable lags in monetary policy’s effect on the economy, there was also a risk that the Committee could tighten the stance of policy by more than necessary to restore price stability.

In short, the Fed is a long way from easing. Callum Thomas at Topdown Charts pointed out that the global monetary policy cycle is still tilted towards tightening. With the exception of China and Turkey, global central banks have not even begun to ease yet.

As the Fed tightens monetary conditions, a recession is looming. The Conference Board’s Leading Economic Indicator has fallen for five consecutive months. It has never done that other than ahead of a recession.

New Deal democrat, who monitors the economy using a set of coincident, short leading, and long leading indicators have been warning about a likely recession that begins in Q1 2023 and it will likely continue until Q2 2023.

The long leading indicators are those which have a lengthy track record of accurately forecasting a peak in economic activity 12 or more months out.

A majority turned negative as of Q1’s reports this spring, prompting a “Recession Watch” beginning Q1 of 2023.

With Q2’s updates now in hand, there isn’t a single positive long leading indicator left.

The negative forecast thus remains in effect through Q2 of next year.

While they have not turned back positive, two of the indicators *may* have put in their worst readings one month ago, and bear watching for signs of a positive turn.

Since markets are inherently forward-looking, the June panic could be attributed to the market discounting a recession that begins early next year, and the subsequent recovery is anticipating a recovery soon after.

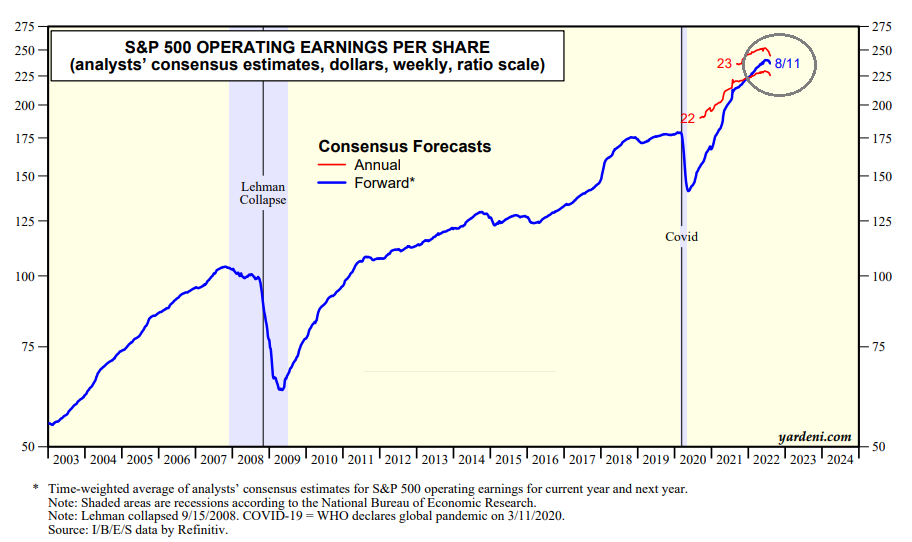

However, earnings estimates are only just beginning to roll over. However, the S&P 500 is losing valuation support. Forward P/E is already 18, and as estimates decline, the P/E ratio becomes even more challenging. After the recent short-covering rally, the market lacks a catalyst to push stock prices higher.

Voting or weighing machine?

Where does that leave us? Short-term price momentum implies the start of a new bull market, but macro conditions argue for caution.

Marketwatch reported that Dan Suzuki of Richard Bernstein Advisors urged investors to “curb your FOMO”.

“Many investors insist on buying early so that they ‘can be there at the bottom.’ Yet history suggests that it’s better to be late than early,” wrote Dan Suzuki, deputy chief investment officer at Richard Bernstein Advisors.

Whether mid-June marked the bottom will only be clear in hindsight. RBA’s Suzuki said an analysis of performance around past bear-market troughs shows that being fully in the market at the bottom isn’t as important as many investors might think.

Suzuki explained:

In a refresh of our previously published analysis, we analyzed the returns for the full 18-month period encompassing the six months before and the 12-months after each market bottom. We then compared the hypothetical returns of an investor who owned 100% stocks for the entire period (“6 months early”) with one who held 100% cash until six months after the market bottom, then shifted to 100% stocks (“6 months late”).

The chart below reflects the findings, which showed that in seven of the last ten bear markets, it was better to be late than early.

“Not only does this tend to improve returns while drastically reducing downside potential, but this approach also gives one more time to assess incoming fundamental data. Because if it’s not based on fundamentals, it’s just guessing,” Suzuki wrote.

In other words, it pays to be patient. The recent rally off the June low was very impressive, but the market lacks a catalyst to push prices higher. Fed easing and earnings improvements are several quarters in the future. A study of past major bear market bottoms and factor responses suggest two possibilities.

The benign outcome will see the market undergo some choppiness for several months in the manner of the 2010 and 2011 bottom. The more bearish scenario calls for a second leg down in the manner of the post-9/11 rally as the full effects of the recession reach culmination.

In all cases, the market is due for a pause. The S&P 500 recently stalled as it tested its 200 dma. I will be watching how the macro backdrop and technical internals evolve during the coming pullback for greater clarity as to which is the more likely scenario.

3 thoughts on ““Price leads fundamentals”, or “Don’t fight the Fed”?”

My answer to whether this is just a bear rally or new bull.

The key is interest rates. How high and how long must they go to satisfy the Central Bankers that inflation is under control. No great revelation there. But let’s look deeper.

Looking back I missed a turning point as strong as the Covid Vaccine Day. From late May to mid-June, Fed futures soared (short-term chart).

At that point, we didn’t know how high rates would go and investors were panicking. But then the December 2023 contract started falling hard until it went below the December 2022 contract. That indicated that rates would peak in early 2023. That was very tame for investor perceptions. The disaster unknown had become the tame known.

The severe Beta Crash of Growth stocks stopped and had a big rally. We are having the biggest bubble since the Tulip Bulb Craze, so it makes sense that its bear rally would be big. Bubbles don’t die with the small amount of damage we have had to date, especially historic ones like this one.

Now we see the 2023 has gone up and is getting close to the 2022. This indicates investors are starting to believe the inflation problem will take the Fed longer and need higher rates. Investor recession worries will grow as the rates move higher and the 2023 rising indicates longer.

If 2022 remains range bound and 2023 stays below it, markets will love a tame rate outlook. If we break out higher, especially if 2023 goes above the 2022 (meaning rate hikes keep going), then the bear market is back on and the rally fails. Powell’s speech at Jackson Hole may direct us.

A most interesting hypothesis! I’ll be watching the chart that you shared. The next few weeks would be interesting (J Hole and FOMC).

Thank you for sharing.

The Saudis and other oil rich states have to stash their profit somewhere and it turns out to be mostly US equities which explained why they didn’t care if they were front running the Fed which resulted in the bear market rally since May and June that is about to turn into something else. The real question is will they keep buying above the long term VWAP which will turn this into a bull market. There is rich then there are the super rich, Aramco $48 billion profit a quarter.

Our site uses cookies and other technologies so that we, and our partners, can remember you and tailor your user experience on our site. See our disclaimer page on our privacy policy, how we manage cookies, and how to opt out. Further use of this site will be considered consent.

My answer to whether this is just a bear rally or new bull.

The key is interest rates. How high and how long must they go to satisfy the Central Bankers that inflation is under control. No great revelation there. But let’s look deeper.

Looking back I missed a turning point as strong as the Covid Vaccine Day. From late May to mid-June, Fed futures soared (short-term chart).

https://refini.tv/3vOS4r5

At that point, we didn’t know how high rates would go and investors were panicking. But then the December 2023 contract started falling hard until it went below the December 2022 contract. That indicated that rates would peak in early 2023. That was very tame for investor perceptions. The disaster unknown had become the tame known.

The severe Beta Crash of Growth stocks stopped and had a big rally. We are having the biggest bubble since the Tulip Bulb Craze, so it makes sense that its bear rally would be big. Bubbles don’t die with the small amount of damage we have had to date, especially historic ones like this one.

Now we see the 2023 has gone up and is getting close to the 2022. This indicates investors are starting to believe the inflation problem will take the Fed longer and need higher rates. Investor recession worries will grow as the rates move higher and the 2023 rising indicates longer.

If 2022 remains range bound and 2023 stays below it, markets will love a tame rate outlook. If we break out higher, especially if 2023 goes above the 2022 (meaning rate hikes keep going), then the bear market is back on and the rally fails. Powell’s speech at Jackson Hole may direct us.

A most interesting hypothesis! I’ll be watching the chart that you shared. The next few weeks would be interesting (J Hole and FOMC).

Thank you for sharing.

The Saudis and other oil rich states have to stash their profit somewhere and it turns out to be mostly US equities which explained why they didn’t care if they were front running the Fed which resulted in the bear market rally since May and June that is about to turn into something else. The real question is will they keep buying above the long term VWAP which will turn this into a bull market. There is rich then there are the super rich, Aramco $48 billion profit a quarter.

https://twitter.com/jnordvig/status/1561199908643901440