Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “

Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post,

Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The

Trend Asset Allocation Model is an asset allocation model that applies trend following principles based on the inputs of global stock and commodity prices. This model has a shorter time horizon and tends to turn over about 4-6 times a year. The performance and full details of a model portfolio based on the out-of-sample signals of the Trend Model can be found

here.

My inner trader uses a

trading model, which is a blend of price momentum (is the Trend Model becoming more bullish, or bearish?) and overbought/oversold extremes (don’t buy if the trend is overbought, and vice versa). Subscribers receive real-time alerts of model changes, and a hypothetical trading record of the email alerts is updated weekly

here. The hypothetical trading record of the trading model of the real-time alerts that began in March 2016 is shown below.

The latest signals of each model are as follows:

- Ultimate market timing model: Sell equities

- Trend Model signal: Bearish

- Trading model: Neutral

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers receive real-time alerts of trading model changes, and a hypothetical trading record of those email alerts is shown here.

Subscribers can access the latest signal in real-time here.

Here we go again

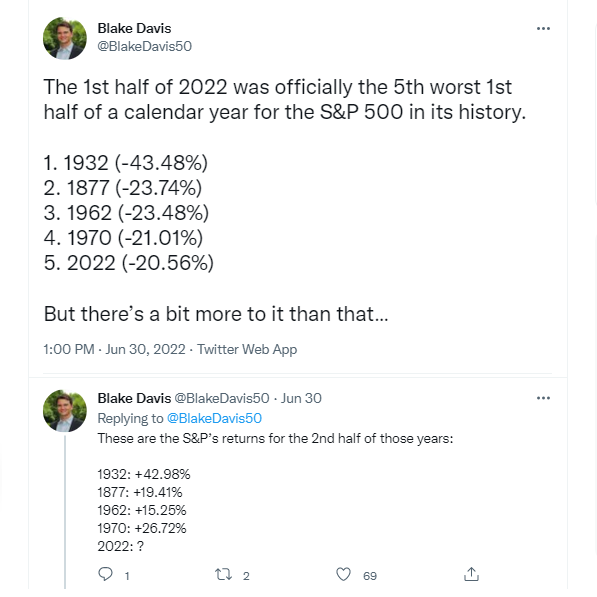

June was awful month and 2022 was even worse for investors. The S&P 500 has been falling all year, though it constructively ended the week with a continuing positive 5-week RSI divergence, indicating waning downside momentum.

Where’s the bottom?

A history of pain

The historical studies give a good sense of the carnage. There have only been seven other occasions since 1946 when the S&P 500 has fallen -15% or more. If history is any guide, the market rebounded in the next three, six, and 12 months.

The first half was also ugly, with similarly positive results for the remainder of the year.

Not only did stocks perform badly, but also the 10-year Treasury hasn’t had such a rough time since 1788, which was the year before George Washington first became President.

Even my Trend Asset Allocation Model was substantially in the red, though it did beat its benchmark. The model portfolio one-month return was -3.7% vs. -4.3% for a 60/40 benchmark. The one-year return was -7.5%, vs. -9.0% for the 60/40 benchmark (full details

here).

A nadir in confidence?

Do these historical studies mean that the markets are poised for a rebound? Here are some clues.

A recent Deutsche Bank survey found that “90% expect the next US recession by the end of 2023 or before, with 20% anticipating one this year. That is up from 37% and 2% in January, respectively, and 78% and 13% last month.” A recession is now the overwhelming consensus.

Households are similarly pessimistic. Bottoms in consumer confidence has historically resolved in strong equity price returns. The key question for investors is whether confidence can turn up in the near future.

Consumer confidence has shown a strong inverse relationship with oil prices since the mid-90’s (WTI price is inverted).

Crude oil prices are looking a little toppy, but can they drop in light of the supply difficulties caused by the Russia-Ukraine war? The New York Fed produces a weekly

oil price dynamics report, which decomposes the different elements of oil prices. Supply dynamics (red) are tight, but demand (blue) is falling. The gold region, or residual, can be best thought of as speculative investor demand, which is also falling. Consequently, oil prices have encountered difficulty advancing in the face of falling supply.

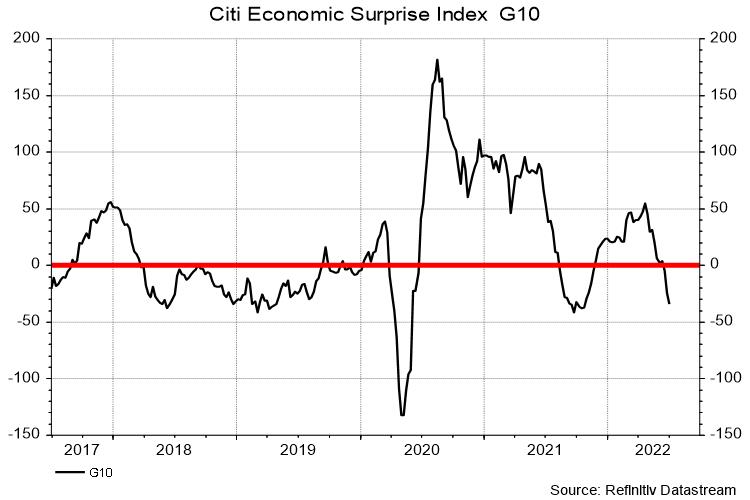

Already, growth expectations are skidding. As the growth outlook slows, the combination of slower demand and waning speculative activity will be bearish factors in oil prices. As energy costs ease, consumer confidence should begin to recover.

Sentiment support

Sentiment and technical conditions point to a washout. Jason Goepfert at SentimenTrader found that 5-week market volatility is at its highest since 1928, which has caused sentiment to tank. Over the past 80 years, similar instability coincided with the ends of bear markets. The catch is such conditions don’t always pinpoint the precise bottom.

SentimenTrader also has built a proprietary Risk On/Off Indicator, which combines 21 unique components into a weight-of-the-evidence approach to assess market conditions. It just fell to zero for only the sixth time in the last 20 years.

Valuation signals

As well, JPMorgan Asset Management found that the percentage of companies trading at below cash and short-term investments has risen to a fresh high. Before becoming overly excited, keep in mind that these companies are from the CRSP universe, which contains many micro-cap stocks that are not investable for liquidity reasons. Nevertheless, this is a useful signal that the stock market is becoming very cheap.

No Fed Put

The bears will argue that this time is different. While the market is becoming stressed and sentiment looks washed out, global central bankers have affirmed their commitment to fighting inflation. Better take a little pain now than have to take a lot more pain later if inflation expectations become unanchored. In other words, there’s no Fed put.

Financial conditions are becoming stressed, but readings are hardly at crisis levels and the unemployment rate is 3.6%.

It is said that the Fed will raise rates until something breaks, nothing in the U.S. is at imminent risk of breaking. Across the Atlantic, the situation looks a little more precarious. The German utility Uniper announced that it was withdrawing guidance as the company relies on Russian Gas for 50% of its supply. Uniper is losing €30M a day from buying missing gas volumes at spot prices. The situation was resolved when the German government indicated that it stood ready to support the company with a bailout. There’s nowhere to hide. Not even utilities are safe.

The Uniper situation highlights the EU’s fragile position. Gazprom is scheduled to shut down the Nordstream 1 pipeline July 11–21 for planned maintenance. The concern is that Moscow will take the opportunity to permanently shut gas supplies to the EU in retaliation for supporting Ukraine in the war. Notwithstanding the effects of tighter monetary policy, a shutdown will have the double whammy effect of cratering European growth.

Does this meet the criteria of something breaking?

Seasonal tailwinds

Where does that leave us?

While I am somewhat skeptical of seasonal patterns, the NDR Cycle Composite takes three historical cycles made up of the one-year, Presidential, and 10-year decennial cycles. It has been almost perfect in 2022. It’s pointing to a strong stock market rally in the second half.

While I am not brushing aside the downside risks to growth, investors have to play the odds in these times of apparent market panic. The market is very worried about falling growth and an inflation rate that’s slow to decelerate. Few have considered a scenario of a combination of small improvements in supply and demand destruction from higher rates is just enough to soft-land the economy. The rise of recession hysteria has meant that risk/reward is becoming tilted to the upside for equity investors.

I think traders and investors have become accustomed

to the stock market become a “V” bottom. With the expectation that earnings have yet to be revised downwards one should not rule out the possibility that we enter into a trading of 7-10% with a downward bias. 1970’s was a great example of that.

I try keep an open mind. In the past becoming too entrenched in a single outcome has generally worked against me. I lean pessimistic by nature and therefore guard against gravitating to worst case scenarios. I think that’s where TA, sentiment and seasonal analysis plays a key role. It removes personal bias and emotion and identifies lower risk entry and exit set-ups. It’s all about probability. Some work, some don’t. The key in my view is risk management and early exit of losing positions to limit losses and preserve capital.

I think you are on the right track. Together with risk control i.e. using stops etc., one can enhance returns by adding to positions that are working. I normally scale up by adding to positions in a form of a pyramid. This way when you are right you make more money.

Anecdotal evidence re Asia.

One younger brother has specialized in structured finance for an international law firm with a large presence in Asia. After thirty years overseas, he recently semi-retired to a small vineyard in Sonoma County. We drove up for a visit yesterday, where incidentally the tourist trade was in full swing. Probably the July 4th crowd, but a local restaurant he likes was only able to manage four seats at the outdoor bar for lunch. No recession here.

How are things in Asia? Booming. He now works from home, but in the past six months he’s managed several deals which together have already brought in 4x the revenue he averaged in a typical year while based in Hong Kong.

You are right. Greater SF Bay area is prosperous for the most part, as is Asia outside of northeast and China. It is uneven.

Bay Area is a prosperous place to live for sure. I’m in the South Bay, aka Silicon Valley. Two data points from my past week:

Houses in my neighborhood have been selling fast (10-15 days) and 10-15% above asking. Last week, two nice houses that I can see from my front porch that were on sale were withdrawn from the market. They were priced fairly based on the recent market.

Two of my biggest clients pushed orders out, both due to increased finance scrutiny in the c suite. The deals aren’t dead, but dragging. Previously there was urgency to move forward before prices went up and/or to get ahead of the supply chain curve. It has been some time since this was the case, summer 2020 or so, and tells me that people are starting to batten down the hatches.

Maybe it’s all the talk of recession. Maybe it’s the time to be greedy when others are fearful. So hard to know. Q2 earnings and forward guidance will be a big factor for how the remainder of the year goes. I’m remaining cautiously optimistic, but still heavy cash.

Could be construed as good news – ie, the kind of evidence that Powell is looking for.

Bad news is good news Fed wise eh? Possible for sure, depends on how serious they are about inflation.

Cam, if I recall correctly you recently mentioned that we’re probably going to test the bottom with a double or triple bottoming pattern. Do you still believe that?

Many keep saying there’s causal correlation between size of Fed balance sheet and the market so QT will do the reverse. If this is credible, will waiting 1-2 months (for example) after QT starts be enough to judge if it’s as apocalyptic as many claim? I guess the Fed can always reverse the QT like they would with interest rates so shouldn’t be too bad in the end but the middle part might have a ‘patch of volatility’ that I want to avoid.

When does the pain end?

Every encounter I’ve had with pain – physical, mental, emotional, economic – resolves only over extended periods of time. That’s how life is.

Give it time. Markets/stocks will be basing for a while.

Nice outperformance by the Nasdaq this morning.

Rallies in bonds and growth stocks.

WTI settles under $100.

SPY green.