Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Model is an asset allocation model which applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. In essence, it seeks to answer the question, “Is the trend in the global economy expansion (bullish) or contraction (bearish)?”

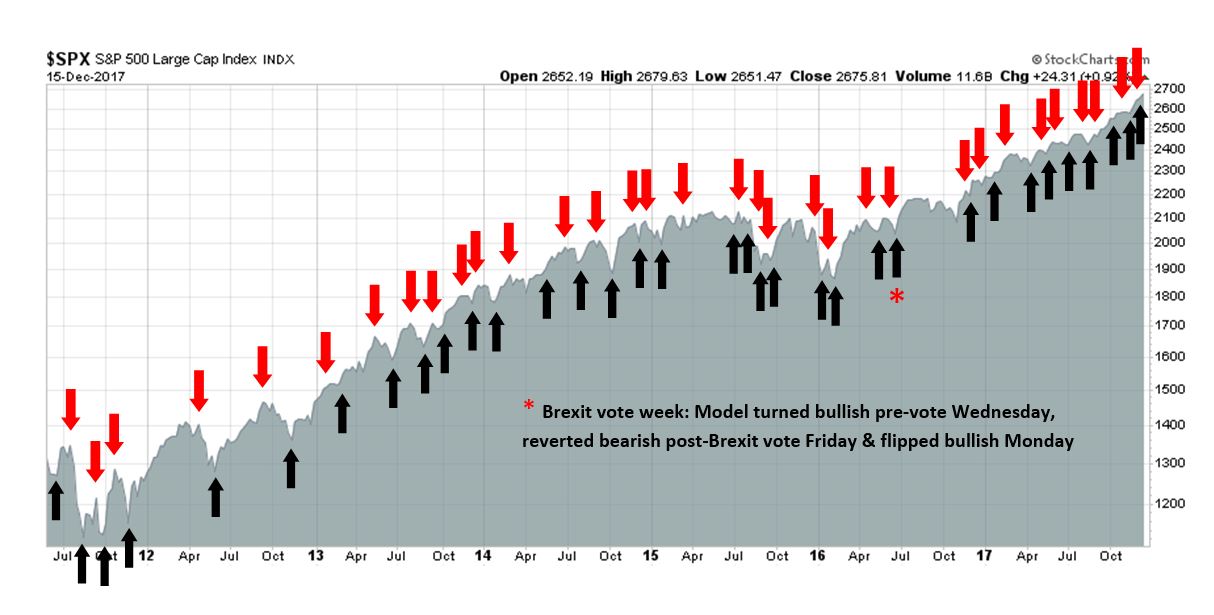

My inner trader uses the trading component of the Trend Model to look for changes in the direction of the main Trend Model signal. A bullish Trend Model signal that gets less bullish is a trading “sell” signal. Conversely, a bearish Trend Model signal that gets less bearish is a trading “buy” signal. The history of actual out-of-sample (not backtested) signals of the trading model are shown by the arrows in the chart below. Past trading of the trading model has shown turnover rates of about 200% per month.

The latest signals of each model are as follows:

- Ultimate market timing model: Buy equities

- Trend Model signal: Bullish

- Trading model: Bullish

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers will also receive email notices of any changes in my trading portfolio.

What happened to 3 steps and a stumble?

As expected, the Federal Reserve raised rates by a quarter point last week and re-affirmed its dot-plot projection of three more quarter-point hikes next year. What happened to “three steps and a stumble”?

The old Wall Street trader’s adage of “three steps and a stumble” refers to the stock market’s reaction to Fed rate hike cycles. At first, stock prices don’t react to the Fed raising rates, but eventually the market succumbs to the economic cooling effects of monetary policy, and a bear market usually begins after three rate hikes. Hence, “three and a stumble”. The chart below from Ned Davis Research shows the effects of this rule on the Dow. Historically, the DJIA has declined a median of -17.9% from sell signals to NDR market bottoms.

Historically, the sell signals have been fairly prescient, though sometime early. This expansion cycle has been unusual in that the Fed began raising rates two years ago. We have seen five consecutive quarter-point rate hikes, so where’s the stumble?

When is the next recession?

Another way of framing the question of timing the next market stumble is, “When is the next recession?” Historically, recessions have been bull market killers, and they are caused by Fed tightening.

Fed watcher Tim Duy observed that there is recession embedded in the Fed’s latest forecast:

There is a recession in the Federal Reserve’s forecast. You won’t see it in the growth projection, but it’s staring you in the face in the unemployment forecast. And it’s a doozy.

The Fed’s Summary of Economic Projections, or SEP, released at the end of this week’s Federal Open Market Committee meeting, projects an unemployment rate of 3.9 percent at the end of 2018. This is well below the Fed’s current estimate of the longer-run rate of unemployment, equivalent to NAIRU, or the non-accelerating inflation rate of unemployment, which remained at 4.6 percent.

Sustained unemployment rates below NAIRU would, in the Fed’s framework, eventually trigger above-target inflation. To counter these pressures, the Fed anticipates tighter policy to guide the unemployment rate back to 4.6 percent. This is evident in the SEP. Central bankers now project a benchmark federal funds rate of 3.1 percent by the end of 2020, compared with a neutral (or longer-run) rate of 2.8 percent. Monetary policy thus will turn from accommodative to slightly restrictive in the next couple of years.

The somewhat restrictive policy tempers economic activity sufficiently to nudge the unemployment rate back up to 4.6 percent. But therein lies the problem in this forecast. There is no evidence that the Fed can nudge the unemployment rate up 0.7 percentage points (from the projected low of 3.9 percent to 4.6 percent) without more aggressive rate increases that would trigger a recession.

In other words, the Fed is projecting that its own actions would cause a recession some time in the future. Historically, it has not been able to raise the unemployment rate by 0.7% without inducing an economic slowdown.

Timing the slowdown

When will the slowdown take place? A review of current monetary conditions show that financial conditions are still easy, so there is nothing to worry about for the immediate future.

Despite the general lack of financial stress, the Fed`s program of policy normalization is slowing down money supply growth. Real money supply growth, whether M1 or M2, has turned negative ahead of past recessions. In this cycle, real M2 growth is decelerating quickly, and could turn negative in Q1. That would be the first sign that the Fed’s actions are having a substantial effect.

The yield curve, as measured by the spread between 2 and 10 year Treasury paper, stands at 51bp. Even though the yield curve is flattening, it is not inverted. Therefore there is no need to panic yet. In the past, the stock market has boomed just as the yield curve flattens. The yield on the 10-year Treasury note has been range bound for all of 2017, and in an even narrower range between 2.1% and 2.4% since April.

If the Fed keeps its commitment to raise three more times in 2018 and 10-year yield remains range bound, the yield curve could invert by mid-year or in Q3. Historically, stock prices have performed well in the period leading up to yield curve inversions.

Here is a table of the same analysis. The highest level of excess returns seem to occur 9-12 months before a yield curve inversion.

Assuming that it inverts in late Q2 or Q3, it means that we are in a sweet spot for stock market returns. If history is any guide, expect an SPX target of 2860 to 2970 in 6-9 months.

Global momentum

Another bullish tailwind is the synchronized global upturn, as evidenced by the rising regional Citigroup Economic Surprise Indices, which measures whether economic data is beating or missing expectations.

Further indications of a cyclical upturn comes from the copper/gold ratio, which distills the economically sensitive element of the copper price from its commodity and hard asset component. Historically, a rising copper/gold ratio (red line) has been correlated with a positive risk appetite, as measured by the stock/bond ratio (grey bars).

The latest update from John Butters of FactSet shows that Street earnings estimates are rising, which is a bullish indication of fundamental momentum. Q4 earnings season also looks bright.

The Q4 earnings season looks bright. Butters also reported that consensus Q4 2017 EPS estimates have fallen by -0.6% since September 30, which is substantially better than the five-year average of -3.3% and 10-year average of -4.3%. As well, we may see further price upside as Q4 earnings season gets underway in January, as Street analysts raise their estimates based on corporate guidance on the effects of the tax bill. Stay tuned!

Ned Davis Research recently pointed out that EPS growth acceleration is already as good as it gets. The market is in the sweet spot of earnings growth, where stock prices achieve the best level of gains (via Callum Thomas).

Enjoy the party while it lasts.

When the yield curve inverts

Looking ahead, what happens if the yield curve inverts next year? A number of analysts have trotted out studies that indicate stock prices continue to rise once the yield curve inverts. Rather than rely on historical studies, here is what I am watching for.

What happens to inflation, and inflationary expectations? So far, some Fed officials have been reluctant to be overly aggressive in raising rates as inflation has not appeared. Greg Ip of the WSJ observed that the Fed did not react by projecting further monetary tightening in light of the fiscal stimulus from the GOP tax cuts. They are watching to see if the tax cuts will spur productivity growth through greater capital spending:

The reasons are twofold. One is that inflation is still too low, and that completely changes the equation: It suggests overheating is to be welcomed, not resisted. The other is that officials are open to the possibility that the tax cut will raise the economy’s potential growth rate, which means faster growth wouldn’t necessarily lead to more inflation.

That isn’t their base case, which may irritate President Donald Trump. But more important for Mr. Trump is that Ms. Yellen and her likely successor, Fed governor Jerome Powell, aren’t yet the party poopers many supply-side tax cut advocates feared.

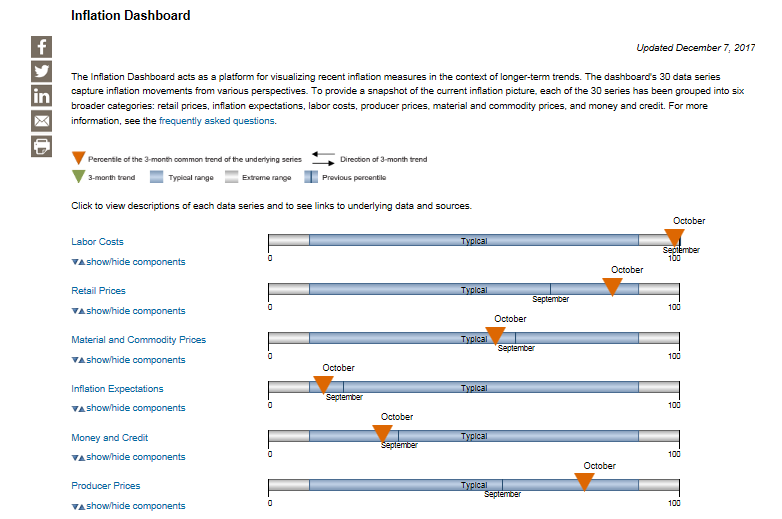

At the same time, underlying measures of inflation, such as the New York Fed’s Underlying Inflation Gauge, is running a little hot.

Some components of the Atlanta Fed’s inflation dashboard are also starting to heat up, namely labor costs, retail prices, and wholesale prices.

Another key question revolves around the evolution of the voting membership of the FOMC next year. Dovish regional presidents such as Charles Evans and Neel Kashkari will be gone, to be replaced by John Williams, who is more centrist, and uber-hawk Loretta Mester.

As well, there are several open seats on the Fed’s Board of Governors. The Trump administration has already nominated monetarist hawk Marvin Goodfriend to one of the positions. Who will be the new vice chair, and who will fill the other board seats? The FOMC could conceivably take a dramatic hawkish turn should Trump appoint rules-based Republican economists to the board. Four, or even five rate hikes are not inconceivable under such a scenario.

Should the market start to falter, one of the technical warnings would be a negative divergence on the 14-month RSI of global stocks. Historically, major tops have been characterized by an initial top, a pullback, and a rally to either a second high, or a test of the old high with a negative RSI divergence. So far, the first pullback has not occurred yet.

Barring any surprises, such as a trade war, a market melt-up is ahead for the next few months.

Key risks

There are a couple of key risks to my bullish outlook. The main one is, in fact, a trade war. The Trump administration is scheduled to unveil its National Security Strategy (NSS), which is an important document that outlines its foreign policy initiatives, on Monday. A Financial Times article gave a preview of the document. It appears that Trump is turning his sights to China, and not in a market friendly fashion:

Donald Trump will accuse China of engaging in “economic aggression” when he unveils his national security strategy on Monday, in a strong sign that he has become frustrated at his inability to use his bond with China’s President Xi Jinping to convince Beijing to address his trade concerns.

Several people familiar with the national security strategy — a formal document produced by every US president since Ronald Reagan — said Mr Trump would propose a much tougher stance on China than previous administrations.

The market has learned to discount Trump’s tweets, as they tend to be spur-of-the-moment thoughts, but the NSS is a policy paper produced by staff:

“The national security strategy is likely to define China as a competitor in every realm. Not just a competitor but a threat, and therefore, in the view of many in this administration, an adversary,” said one person. “This is not something that they just cooked up. Mar-a-Lago interrupted the campaign rhetoric, and Xi Jinping took a little gamble and came here and embraced Trump. Trump said ‘fine, do something on North Korea and on trade’, but that didn’t work out so well.”

The NSS could contain highly protectionist language that could spook the markets:

Some people familiar with the strategy said it would be the most aggressive economic response to China’s rise since 2001 when the US backed its entry into the World Trade Organization. It points to the waning influence of Gary Cohn, the White House National Economic Council head who many people believe will leave the administration next year, and the growing power of Robert Lighthizer, the US trade representative, and other China hawks in the administration.

“It’s like a Peter Navarro PowerPoint presentation,” said one person, referring to the provocative economist and author of “Death by China” who is now a White House official…

Mr Lighthizer, an unapologetic economic nationalist, has long advocated a more muscular trade policy toward China. Critics worry that if the US pushes too hard, it may provoke a trade war that could have devastating consequences for US business and the global economy. Former officials said accusing China of economic aggression and labelling it a strategic rival was likely to lead to carefully calibrated retaliation by Beijing, with US companies bearing the brunt of any response.

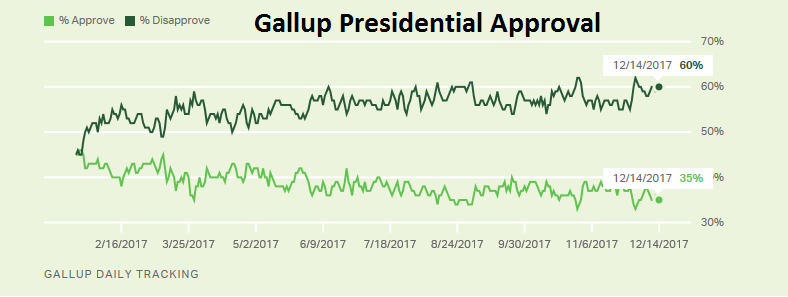

Another key market risk is Trump’s faltering political support. Gallup’s tracking poll of presidential approval has fallen to 35%. Ned Davis Research has found that stock prices tend to be sloppy when presidential approval ratings fall to 35% or less, but this is a purely tactical call as recent low approval ratings have only led to shallow price corrections.

The week ahead

In my last post (see Do you believe in Santa Claus?), I suggested that a small cap seasonal rally is about to get underway. Subscribers received a trading alert that my trading account had bought a long position in small cap stocks on Thursday. An update of the relative return of small cap stocks in 2017 shows that they appear to be bottoming right on schedule.

Breadth indicators from Index Indicators show that small caps bounced off an oversold reading, indicating further near term upside.

The SPX is in a similar position as it rallied off an oversold position and displaying positive momentum.

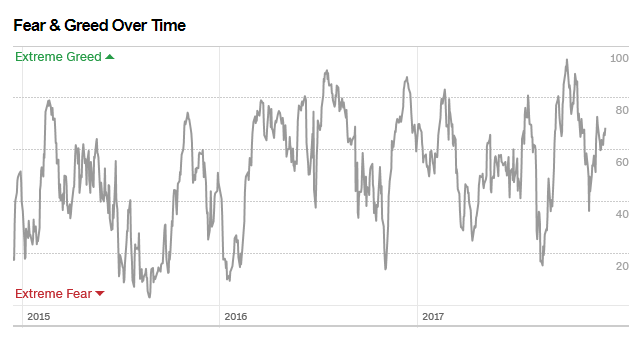

Similarly, the Fear and Greed Index is rallying, but it is nowhere near a crowded long reading.

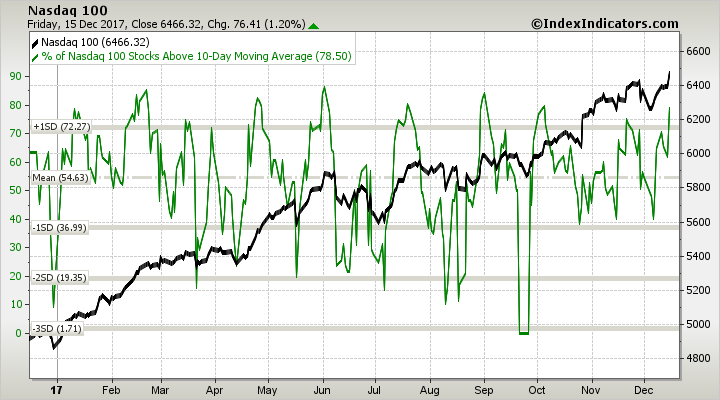

However, the NASDAQ rally may be nearing an inflection point, as readings have become overbought. It may be time for these stocks to pause after staging an oversold rally.

The year-end seasonal rally is underway. My inner investor remains constructive on the market. My inner trader is long equities up to his neck, though he may take some profits on his NASDAQ 100 long position early next week.

Disclosure: Long TQQQ, TNA

Tim Duay comments that: “Monetary policy thus will turn from accommodative to slightly restrictive in the next couple of years.”

Cam reports that: “In this cycle, real M2 growth is decelerating quickly, and could turn negative in Q1.”

Neither seems to consider that monetary policy consists of two factors. The first is the quantity of money. This can be measured directly. The second is the velocity of money which can only be measured indirectly.

During the overlong period of ZIRP (zero interest rate policy) the velocity of money has been uncommonly low. Other commentators suggest it is due to a lack of incentive for banks to push end use of those funds so they languish in reserves.

These commentators now suggest that the so-called, “normalization” of interest rates has the potential to increase the velocity of money. As interest rates rise bank have incentive to push the end use of that money – loans – and that will increase the velocity of money.

The result is that while the quantity of money may stabilize if the velocity increases along with rates then inflationary pressures may rise as well.

This economic beast may not yet be ready to lie down.

Agree 100%. Real money growth is only one component of my set of leading indicators and any indicator can fail. Monetary velocity will be one metric to watch in the months ahead.

Jeff Miller

The current administration is trying hard to reduce regulatory burdens that have been seen to keep GDP growth on the low end of the scale. Cam has shown on many occasions that financial conditions have “loosened”. It remains to be seen, how much inflation would rise or not. Yes, asset inflation is for all to see, in rear view, wage inflation and pass through into the rest of the economy, remains subdued.

Cam, you shared that S&P may reach 2860-2970 over the next 6-9 months. Do you have a target for R2K? Also, any thoughts on gold? Shouldn’t it rise a bit with $1.5 trillion in tax cuts over the next 10 years?

Sanjay

Watch the $ index. 92.xy is support (see Jeff Gundlach’s missive in the last few days). A weak $ may generally be harbinger of inflation (not the only cause of inflation). Key to your question is to watch inflation, and inflationary expectation, wage growth and the pressure on the bond market. If inflation remains subdued, gold may not rally significantly. If the $ index does not collapse, gold may not rise much. A trillion $ deficit in a decade, is not the same as what happened circa 2008. Velocity of money, also remains a proxy for inflation and gold. We are embarking on a new tax regime in the US that will have unclear consequences. Inflation has remained subdued for several decades now, and inflation may be the genie that unleashes out of the bottle. It will be interesting to watch. A slight uptick in inflation is generally good for the stock market, a large rise is not, as it forces the federal reserves to raise rates. Sustained rise in inflation will likely push inflation higher. That said, deflation like what we saw circa 2008 will also push gold higher. As an aside, gold bottomed in year 2000, and had a significant rise until 2008 for reasons somewhat unclear to me. The significant rise in gold against the US$ between 2008-11 was because of deflation (we saw some of the largest deflation of asset prices in recent times). So, gold, may rise with high inflation (1970s) or with deflation. Buy some bullion (not ETFs), as a life long insurance. Just my 2 cents.

Of all the “fundamental” issues you have raised here that represent a possible threat to the bull market it is the harsh approach to China, which in his belligerence and myopia, Trump seems to favor. Or is this his way to get China to contain North Korea? Prediciting the actual outcome with Trump is made especially difficult given his tendency to react at the moment in disregard of his previous positions on a given issue. Bob Millman

Robert/Bob

I read a book titled Monsoon, Indian ocean and future of American foreign power, a few years ago. Robert Kaplan elegantly describes the center of gravity of the world up until now (past five decades) as being squarely in the Atlantic, between the US and Europe. With Europe having become largely irrelevant, the world will remain bipolar, on one side, the US and on the other hand China, as the next super power wanna be. The Indian Ocean sits right where the drama is likely to unfold is one premise of the book. On the western side of the Indian ocean are energy sources of the world, i.e. the middle East on the other side is the manufacturing centre of the world, i.e. China. China, so far, has largely marched to the tune of its own drummer, much to the chagrin of the US. America wants to engage China, but China has largely been successful in engaging in the US on its own terms. There are very large differences between the US and China on many fronts. Another book that highlights the differences is by Tom Friedman and Michael Mandelbaum titled “This used to be us”. From a Chinese perspective, with respect to North Korea, the question they have posed to the POTUS is “what is in it for us”? That should explain the Chinese stance to the question of NK, in a simple sentence.

Hi Cam, thank you very much for your recommendation. Do you still think that Santa will arrive? Today and tommorow are the one of the worst days in December. Would you recommend to add long positions in TNA? Thank you.

Petr

The seasonal pattern favoring small caps is still holding. It should continue until year-end or early in the new year. As well, the market should get some buzz about small caps being the beneficiaries of the tax bill.

Keep in mind, however, that this is a volume light tape as most of the professionals have packed up for the year.