I thought that, as a change of pace, I would write about where my inner investor is finding opportunities, instead of focusing on the daily gyrations of the stock market and whether it has found a short-term bottom, which is a topic I will cover in a post this weekend.

The art of bottom fishing requires a strong constitution, which is suitable for people like my inner investor who has a longer time horizon. You have to go into the exercise thinking that you don’t care that you catch the exact bottom, but with a mindset that Mr. Market has put a sale price on an investment. You may buy X at $10, see it fall to $7, but be ultimately rewarded in several years when it rises to $20, $30 or $40 (note that these are just examples and not return forecasts).

With that framework in mind, here are a couple of opportunities identified by my inner investor.

Value stocks

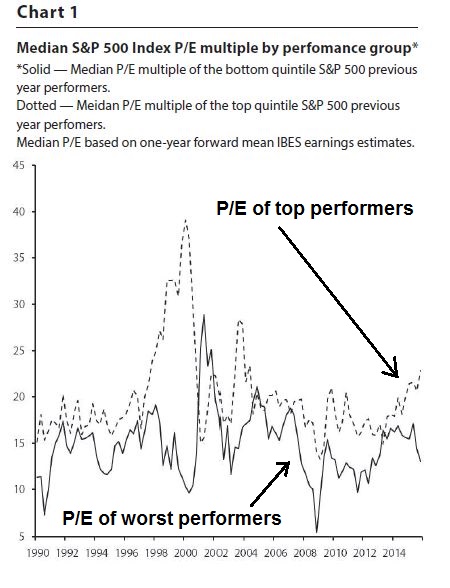

Jim Paulsen at Wells Capital Management recently wrote a terrific article about the valuation differences between the high momentum stocks (top quintile of rolling 12 month return) vs. the low momentum stocks (bottom quintile). He called these groups Popularity and Disappointment. The chart below shows the P/E ratios of the two groups, whose spread is getting a bit stretched.

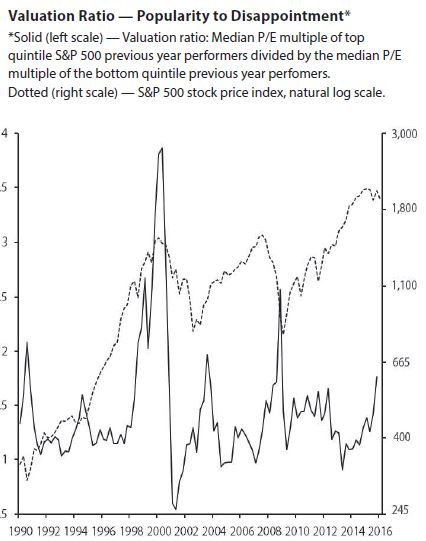

The chart below shows the relative P/E of the Popularity vs. Disappointment (solid line) with the SPX (dotted line).

I make the following two observations based on the above chart:

- The relative P/E ratio is nearing levels where it has reversed in the past; and

- Reversals in relative P/E ratios have either been associated with bear markets or changes in market leadership, which usually occurs during transitions between bull and bear markets.

I am on record as believing that the bull market isn’t over, but it is in the process of topping out (see

The road to a 2016 market top). The second alternative of a simple leadership change is therefore my base case scenario. Incidentally, analysis from JP Morgan (via

Business Insider) shows that, despite all of angst over the narrowness of the leadership of FANG stocks (Facebook, Amazon, Netflix, Google), market leadership is by no means dangerously narrow by historical standards.

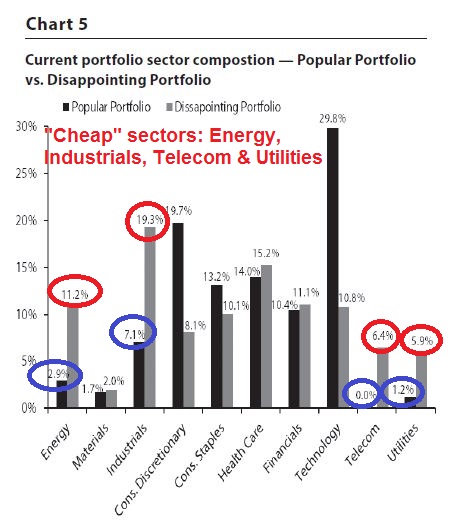

Jim Paulsen went on to show that the unloved “Disappointment” portfolio was overweight in Energy, Industrials, Telecom and Utilities, which is consistent with my view that the US economy is undergoing a late cycle expansion.

The way my inner investor is choosing to play this theme is to buy into value stocks. If you are going to play value, then why not go with the Oracle himself and buy Berkshire Hathaway (BRKb)? I have written before about BRKb has shown only so-so performance in the last few years and underperformed the market in 2015 (see

Is Warren Buffett losing his touch?). The chart below shows the relative performance of BRKb against the market. As the chart shows, BRKb is seeing a minor revival in relative performance, which indicates that 2016 may mark the start of a new Renaissance in value investing.

Energy stocks

Within the most unloved and washed out parts of the stock market, energy stocks are a stand out. Sure, the supply-demand fundamentals of oil look awful and it seems that every day, analysts are scrambling all over themselves to downgrade their oil forecasts. Here are just a few examples:

- Citigroup (Ed Morse): Oil could drop as low as $20 (via Bloomberg)

- Standard Chartered: Oil could hit $10 (via The Telegraph)

- Dennis Gartman: Oil could sink as low a $15 in a panic (via CNBC)

Then you have this

Andrew Thrasher tweet, which is reflective of the washed-out sentiment.

On the other hand, there are a number of bullish signs for the energy sector. From a technical perspective, the recent action oil prices is constructive as it is experiencing a positive RSI divergence.

Scott Grannis pointed out that oil prices are extremely cheap when compared to gold. If I am correct about the late cycle expansion, then cost-push inflationary pressures will start to rise and begin to lift the entire commodity complex. The most oversold major commodity in the complex is energy.

Trying to value energy stocks is tricky at this point, because the E in the P/E ratio is volatile and fading fast. An alternative technique is to consider the P/B ratio, as book value is more constant and useful for valuing integrated oil companies. As

Lawrence McDonald pointed out, the sector is cheap on a P/B basis.

From a tactical viewpoint, I have no idea if the decline stops at $30, $20 or $10. Valuations are sufficiently cheap and the risk-reward ratio is sufficiently attractive for my inner investor to go bottom fishing in the sector. My main focus in the large integrated oil companies that are well-capitalized enough to survive a downturn in oil prices.

My choice in this sector is Suncor, largely because of my inner investor`s innate laziness and the Suncor position in the Berkshire Hathaway portfolio as a signal of its value (see

The right way to ride Warren Buffett`s coattails). However, virtually any well-capitalized large cap integrated energy company is probably suitable as a vehicle and so is a well-diversified ETF like XLE.

In effect, my inner investor is make a double bet on Berkshire Hathaway. For someone with a long term time horizon, that`s probably not a bad position to take.

Disclosure: Long BRKb, SU

Cam

Thanks for the insightful analysis. There are some important considerations that you have discussed in this write up. Thanks so very much for your deep reading and analysis.

A couple comments/questions:

I don’t keep track of the numbers, but somewhere recently I saw someone saying that, although the price of oil, the commodity, has crashed, energy stocks have not fallen as much as they should have. Or putting it another way, the stocks are priced for $45-$50 oil, a big discount from the $100 oil they assumed a year ago, but are still overpriced relative to oil itself. So oil could have a strong 33% rally to $40 roughly, and the stocks still go down. Again, this is hearsay, and I can’t vouch for any of those numbers. Just wondering whether you think that might be the case, and if there is anyone you know whose work matches up energy stock prices and the implied oil price, and shows that the stocks are cheap on that basis?

Also, re: the gold/oil price ratio, it isn’t as if gold has been zooming, it is just that oil has been plummeting. You could take the price of anything, divide it by the oil price (let’s try the roll of toilet paper/oil ratio) and you will see it soared in recent months.

If, as some suggest, the collapsing price of oil, copper, and other base metals, along with the plummeting Baltic Dry index and rail car loadings, all suggest a world heading into a long overdue recession, combined with a financial collapse of over indebted companies and governments, then one would expect the gold/oil ratio to shoot way up from here. Oil would get weak as demand keeps dropping with the economy, and gold would shoot up as central banks do the only thing they know how to do, which is print money even faster.

Even if you believed that the US is entering a recession, which is a view that I don’t agree with (more on that this weekend), then oil should be a “defensive” commodity because of its value characteristics.

I agree Cam, oil is a defensive commodity in a recession. And oil itself may have a good bounce from here and be back to say $50 in a year.

It just seems like so many fund managers have been calling the bottom in oil stocks all the way down. It may be that the prices of the stocks haven’t yet adjusted to $30 oil, and are still assuming that oil will settle at $50. If oil stays in the $30s or lower for a while, they may have another leg down. Ideally, you would want to have the oil companies stocks priced for $20 oil when it is actually $30, so you have some margin for safety if you aren’t right on your commodity call.

I’m just wondering if you, or anybody you know of, can make a case that the oil companies stocks can have a nice bounce even if oil itself is flat? If not, there is a risk that you could be right on the commodity but wrong in the stocks.

Kirk Kirkorian, the American billionaire who died recently made a significant amount of money buying Chrysler and Ford in the depths of a recession for pennies and then rode them right through a bull market. The strategy is viable with a few caveats.

Your time horizon and the investment choice. Today, the same criteria can be used to say Dry Bulk Shipping and Gold Mining are cheap. Both of them are in prolonged down trends and though they may be close to a bottom the recovery does not have to be V shaped. They can bump along sideways for a very long time. If you are a young investor (in age) you might have the luxury of time, if you are retired or close to retirement or a money manager whose performance is measured every quarter this may not be the right strategy.

Cam and I disagree on whether we are in a bear market or in a correction of a bull market. By my definition even if we take the criteria of 20% correction constitutes a bear market, today, besides the Dow Jones Transportation Index, the Russell 2000 has corrected over 20%. The NY Composite, the Value Lines Index that are broadly based are down close 20%. The reason I point this out is not to prove how smart I am but to make a point and that is that if we are in a bear market the decline can be protracted. Most investors since 1982 have seen intermittent corrections (sharp declines) and then strong rallies. After 1929 there was a generation of investors and their children that swore never to invest in the stock market. From mid 1960s to 1982 the stock market traded in a broad trading range. At one time Insurance companies and Pension Funds were only allowed to invest in Bonds only. The Federal Reserve has tried something new of keeping interest rates down at zero for the longest time. The consequence of that has been to distort the economic cycle. Therefore, to expect the normal sequence of sectors going through the logical rotation may not happen. That is one reason the strategy Cam is suggesting should come with a label: caveat emptor.

A rally should be around the corner and the quality of the rally will tell us where we are : a bull market or a bear market.

I am going to say something that if there are any children are in the room, please cover their ears and hide the text. THIS TIME IT’S DIFFERENT. Sir John just rolled in his grave. Forgive me. but I truly believe we are in a period of incredible creative destruction. The digital revolution and globalization are creating winners and losers at an increasingly faster pace. The average time a company is in the Fortune 500 now is fifteen years, down from seventy in the 1950’s. This time of change leads me to look at market statistics differently.

I would label outperforming stocks as “Successful Navigators of Change” and the underperformers as the “The Road-Kill of Technology”. A label can certainly change the narrative. It sounds a whole lot different when you say, “I think it’s time to sell the Successful Navigators of Change and buy the Road-Kill of Technology because the Successful stocks have gone up more that the Road-Kill.”

I am not a novice who is swept up in the popular flavor of the day. I have been in the investment industry longer that almost everyone. My first job was looking at ticker-tape and marking up a quote board before there were electronic quote terminals. Technology is my passion and I keep abreast of what’s happening. What is happening now curl’s my toes as I’m sure it does with every smart CEO.

So much thinking in the investment business revolves around “reversion to the mean”. That used to to be valid… not any more. It used to be true that investing in new companies or reinvesting profits in existing companies was done with a common return on capital projected. So over a long term an industry such as steel might make the same return on capital as let’s say grocery stores. The cyclical steel industry stock would go up and down more than the grocery and this would create opportunities to buy steel when there was a recession and cheap and switch back to grocery when the business cycle peaks. But back then, in the long, long run all would return to the mean return on capital. This was the world of we battle hardened, successful-investor Cam Hui readers. But that slow-changing, tariff protected business environment does not exist today. Companies that are not adapting have stocks that are underperforming because they are heading for the scrapyard not because they are unpopular or because the general business cycle is at a certain place.

Case in point, the oil business. I am in oil country and have several clients in the drilling business. The technology advances are simply incredible and they keep improving. It has caused a crash in crude prices. My oil veteran friends say platitudes like “I’ve been through these busts so many times blah blah blah.” They are thinking we will revert to a mean, to a norm, but my driller clients say the industry is undergoing a profound permanent technology change. Veteran investors also say these stocks are down because they are unpopular like the old days and will go up when things return to “normal”. I believe, “This time it’s different”.

Other sectors in the “Disappointing Sectors” above are telecom, industrials and utilities. These industries just happen to be the most in the cross-hairs of technology trends. Are they simply cheap in relation to fundamentals because they are unpopular and will go back up when things “return to normal”. Or are they, feeling the sting of change that will get worse with no return to a past normal.

Using the phrase “Popular Portfolio” to denote the outperforming stocks is also a veterans term. After a long bull market, we would have general investor sentiment very optimistic and the flavor of the day group would get very over-priced. Our experience makes us quick to label today’s stock market environment as such. After all, the S&P 500 is near a seven year high. We search for examples of this folly and today find FANG. People try to equate these with the folly of the Dot.com’s in 2000. But these are extremely valid and profitable businesses with a growth profile involving billions of people. The smart phone in our pockets would be considered magic just ten years ago. Billions of people have these and billions more will. The proof that we are not at a bubble high is all around us. Investors are extremely nervous and skeptical of everything. They panic at the drop of a hat. Mutual fund investors are cashing out like the bottom in the 2008 Crash. Investors equate lower commodity prices with recessions so they are frantically trying to find recession that is simply not there in the developed world and in major emerging countries like China and India.

So I say don’t jump from the “Successful Navigators of Change to buy the Road-Kill of Technology.”

Momentum-style of investing will be the key to being on the right side of the digital revolution and globalization. Combining value with momentum is even better. But to buy only using value runs the risk of being side-swiped by some new technology or foreign competitor that even veteran analysts covering the stock might not appreciate. Once one buys a loser, it is extremely hard to get out (whole set of behavioral biases kick in).

I’m with Ken on this one. Value yes, but only when technicals say so. I’ll need some moving averages before I dip my toes into those waters.

…and I listen when Kostohryz says, “Oil stocks EXPENSIVE relative to futures deck. Majors won’t benefit from acquisitions without further capitulation from targets”, or, “From a fundamental standpoint, nothing prevents #oil from falling to $20, $10 or $5 on a very short-term basis IF storage becomes exhausted”, or, “$30-$40 #oil can potentially be sustained for up to a year. $40-$50 could POTENTIALLY sustained indefinitely in a worse-case scenario”.

And I take comfort when he agrees with Cam that there is no sign of a recession in 2016, and also this: “My best judgement right now: Minimum 10, Maximum 20 trading days away from actionable bottom in #SP500.”

Remember what I said about my inner investor. You need a strong stomach and go into a position at $10 and be prepared to have it go down to $7, but recognize that in a few years that it will be $20, $30 or $40. If you don’t have that kind of time horizon, then don’t do it.

Indeed, and I’ll keep that in mind… The idea of emulating Buffett sounds even more reasonable, btw!

This just in: Warren Buffett buying Philips 66 even as oil prices were crashing:

http://www.businessinsider.com/warren-buffett-energy-2016-1

What about bottom fishing REITS and other dividend payers. Waiting not as painful.

Sorry, I don’t know enough about the REITs sector to give an informed opinion.