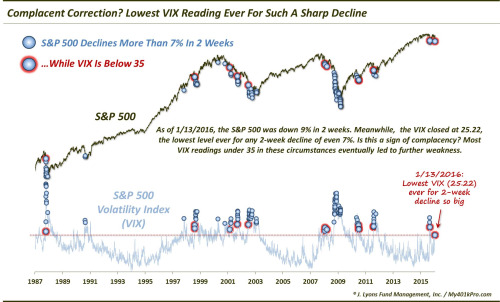

Dana Lyons recently wrote a terrific piece about the level of complacency in the current bout of stock market weakness. The SPX had fallen over 9% in two weeks, but the VIX Index was barely challenging its December highs and it was nowhere near the highs set during the August/September selloff.

He found that past instances of where the market fell a lot but the VIX did not respond in a corresponding fashion foreshadowed further stock market weakness.

Where is the wash-out?

I had also been concerned about the apparent lack of panic during the latest market slide. My Trifecta Bottom Model, which was first described here, uses three somewhat uncorrelated components to spot short-term market bottoms:

- VIX term structure inversion: Which measures rising fear in the option market much better than the absolute level of the VIX Index;

- TRIN: When TRIN is above 2, it is often an indication of capitulative price-insensitive selling, otherwise known as margin clerk market; and

- OBOS: This is an intermediate term oversold indicator which indicates an oversold condition when the indicator falls below 0.5.

The Trifecta Bottom Model has been uncanny in spotting bottoms in the last three years. The chart below shows the record of this model in the last year, where the blue vertical lines indicate that two of the three components have been triggered (Exacta signal) and the red line indicates that all three were triggered. All marked short-term bottoms. The latest bout of stock market weakness saw TRIN hit a high of 1.97 (not quite 2.0) and the OBOS reach a low of 0.52 (not quite 0.5). Are these readings close enough to trigger a buy signal?

The answer is a qualified yes.

Nevertheless, I am highly concerned that TRIN never moved above 2.0. To explain the math in a simple way, TRIN is calculated by dividing the advance/decline volume by the advance/decline ratio. Imagine a day where declining stocks outnumbered advancing stocks by 2 to 1 and declining volume outnumbered advancing volume by 2 to 1. In that case, TRIN would be 1. Now imagine a case where the advance-decline stock ratio was the same, but the declining volume to advancing volume was 4 to 1, which results in a TRIN of 2. This would mean that there was much more down volume than up volume than what would be normally expected – a sign of capitulation, or wash-out

Past market bottoms have seen this kind of wash-out, which is typified by price insensitive selling by margin clerks and risk managers. We have barely seen this kind of behavior during the current sell-off, which is somewhat disturbing.

A volatility mystery

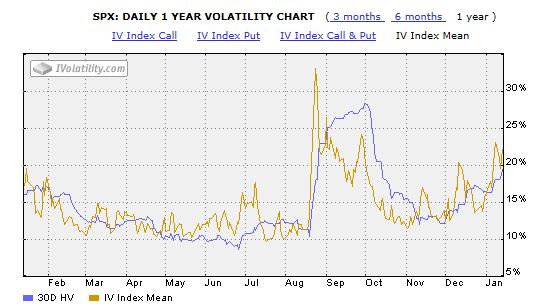

However, the lack of capitulative sell-off can be explained by the behavior of volatility. As all good traders know, the VIX Index is a measure of implied option volatility of stock prices. The higher the index, the higher the perceived volatility. But as this chart from ivolatility.com shows, implied volatility has tracked historical volatility very well. The reason why VIX hasnt spike higher is because historical volatility is lower than it was during the August-September selloff.

More importantly, historical volatility is a key input into the Value-at-Risk, or VaR, models used by risk managers. Imagine that you are a risk manager, or the manager in charge of a trading desk. You use metrics like VaR as a tool to properly size the capital commitment of your trading book. Since volatility, or vol, is a key input, too much noise in vol will cause your book to expand and shrink at a rapid pace. What you need is a relatively stable vol estimate.

The chart below shows the evolution of rolling realized historical one-month and one-year volatility. As you can see, monthly realized vol is far too noisy to be useful as an input into a VaR model, but the one-year vol is relatively stable. As I understand it, most desks uses one-year rolling vol the input to their baseline VaR risk estimates.

You will also notice that the one-year rolling vol spiked during the August selloff and then flattened out. This means that Value-at-Risk estimates did not change very much during the latest stock slide. Hence, there was no need for risk managers to order traders to reduce their position sizes, which would have triggered a price insensitive selloff that drives TRIN above 2.

In effect, the hedge funds and trading desks were not forced to sell by their risk control discipline. I know that I’ll get lots of comments from the last sentence, but don’t forget that most trading desks are hedged in some fashion with long and short positions. Higher VaR estimates (from higher realized vol estimates) would require them to shrink both sides of their book.

To make a long story short, flat historical vol estimates meant that trading desks did not have to sell. Therefore there was no price insensitive capitulative selling.

What does this mean near-term for stock prices? I am not sure. Readings from the Trifecta Bottom Model got close enough to trigger a buy signal, so I am giving the bull case the benefit of the doubt. However, I would not characterize this signal as unabashedly bullish and I will be carefully watching the quality and breadth of the advance, should it continue.

Cam,

Maybe I’m not following, but it seems the problem is that volatility hasn’t spiked on this decline. It seems to me that you are explaining why it hasn’t spiked. Which leaves us with the problem that volatility hasn’t spiked on this decline. My position is that folks aren’t fearful enough to reset sentiment. Should I worry about or even care why ?

What do you mean by volatility?

Implied vol, or VIX, hasn’t spiked very much because realized vol didn’t spike as much as you might expect. But then, realized vol is just the calculation of the standard deviation of past returns.

Not every sentiment indicator hits extremes at a true low. Over the last week, there has been extremes hit in many indicators that only happen at low points. For example, up daily volume average over the 10 days before today was less that 30%. That shows extreme persistent selling pressure. That is a very rare extreme and usually marks a low especially if you get a 75% plus up volume thrust like we did today.

If we have just hit a short term low, that will mean we have a quadruple bottom, October 2014, August and September 2015 and now. If investors feel comfortable that this line marks a firm low, we should see an intermediate upswing with growing confidence. I am in that camp.

My final, most trustworthy sentiment indicator is also flashing bright green. That is me not believing the market will go up and trying to find any excuse not to buy.

I have a friend who is of the opinion that VIX haven’t seen fire works because the short positions haven’t closed, and the bears remain in control. And that this markets shall at least retest the spike low of August before seeing any rebound. I don’t want to believe him, but price action this week have not been promising.

I am a keen watcher of correlations across different markets. I am based in Australia so I am up early morning for the US close, and Australia is the first market to open before Japan and China. Unfortunately, this week, right after an aggressive move to the down side for equities and commodities FX last week, we have seen no recovery. Instead risk was consistently being sold on bounce. The saving grace I guess is that JPY as a fear proxy (that it appreciates as carry trade unwinds) have not progressed. Namely USDJPY is range bound btween 117 and 118.2

Technically, across equity markets, it’s obvious that these are at multi-year resistances. Assuming that the range holds the risk to reward is to the upside, but I am not so sure if the assumption will hold.

Kind regards

Reminds me of crude. Everybody is trying to call the bottom and it has been in a persistent decline. Till we get the talking heads on CNBC making outlandish comments that the Dow is going to 8000 to 10,000 a bottom will not reached. Sentiment is a function of time and price. Price might be down but lets remember we are only a few days (7) in this decline.

Cam do you watch the SKEW. Yesterday it was at 146. The all time high was 151. There might be a “black swan” out there.

I personally want to thank Cam for an excellent blog. It helps me in my thinking. I try to be objective and not try to speak my “book”. Having got that off my chest I would like to discuss capitulation from a behavioral point of view. As most of you are aware there are different stages and emotions an investor, hedge fund trader or a money manager goes through:

1. The market is going up. Buy XYZ stock/futures etc.. I will make a lot of money. My bonus is assured. We will buy a house in the Hamptons.

2. The market went down today. It was short term overbought. No big deal it will go back up.

3. Another sharp down day. I am getting a little concerned.

4. Wow! this is getting bad. What will my boss/wife say.

5. I read Bob the famous investor/market letter writer and he says it is only a short term correction. Nothing to worry.

6. God, I am down 10% correction. There goes my year end bonus. My wife will kill me.

7. I promise I will sell on the next rally when I break even.

8. I have lost too much money. This was an investment and not a “trade”.

9. Stop looking at monthly statements.

10. Help me god. I can’t take it any more. The margin clerk just called. Sell next day at the open at the market.

11. I will never invest in the stock market again

In my previous posting I had mentioned that sentiment/capitulation takes time. If you notice the drop in crude it has taken over 6-7 months before people are now getting to the capitulation stage where they are saying statements like crude can go down to 10 dollars etc.. The only caveat being if Cam is right that we are close to a bottom in a bull market we should then be off and running again with new highs in the indexes on the horizon. If not, then we will have a rally to relieve the short term oversold indicators and then stall at overhead resistance. Also, Cam will agree that sentiment can go to extremes. There is no law that says that the Trin Index cannot be over 2 for 1 or 3 days in a row. The indicators that we use have different parameters in bull and bear markets.