I got some pushback from a reader to my weekend post (see How to spot the bear market bottom) about the FT Alphaville article indicating that former Secretary of Defense Mattis raised concerns about how the White House lacked a decision making process. The reader went on to defend Trump’s decisions.

I try very hard to remain apolitical on this site. Everyone is entitled to their own opinion, but there is a distinction between a decision, and a process. Here is an example from the investment realm. Josh Brown recently ranted about people “who called the correction”. Click this link if the video is not visible.

Josh Brown’s main complaints can be summarized as:

- Anyone can make a market call. If you are wrong, very few people will remember, or you can delete your articles or tweets.

- Managing a portfolio is a much tougher task. Portfolio managers are measured by actual returns. As an example, if you decide to sell out, what is your discipline for buying back in?

- Just because someone doesn’t say anything, it doesn’t mean that they are unprepared for market volatility. Most firms have compliance guidelines about what individual portfolio managers or advisors can or cannot say or publish.

Despite my own efforts at transparency (see A 2018 report card) where I have published my track record, and owned up to bad calls, I sympathize with Brown. Josh Brown’s rant amounts to distinguishing a decision (market call) to an investment process. A timely market call means little if there is no investment process behind it.

What is an investment process?

At a minimum, here are the steps that professionals have in an investment process. They may call it different things, but the steps are more or less the same:

- Decide on what to buy and sell, otherwise known as alpha generation;

- Decide on how much to buy and sell, otherwise known as portfolio construction, or risk control;

- Timing the trade so that you take maximum advantage of short-term conditions, and, if you are responsible for lots of assets, make sure your trading leaves a minimal footprint in the market; and

- Periodically review and diagnose steps 1-3 to ensure that they are working as intended. In particular, good organizations learn from their mistakes, and make adjustments when things go wrong.

We focus most of our energy on step 1 because that’s the sexy part of investing. My timely call for a top in August (see Market top ahead? My inner investor turns cautious) was exciting. On the other hand, I would lose most of my readership if I devoted most of my time discussing the different ways of dissecting factor risk, or the pros and cons of arrival price vs. VWAP as a trading benchmark.

That’s the essence of the difference between a decision and a process. The market call is the decision. The process is how you implement that decision. The returns of your portfolio depends the strength of the investment process.

What I try to give you is step 1, the rest is up to you. Incidentally, the decision making process in step 2, how much to buy and sell, is a function of each portfolio’s return objectives, risk preferences and pain thresholds, tax situation and jurisdiction, and a whole host of other factors. Most portfolio managers will develop an investment policy statement (IPS) as a framework for step 2, which I know nothing about. That’s why nothing on this site can be construed as investment advice.

My limited guidance for investors

While I cannot give specific advice, here is some guidance that I can offer.

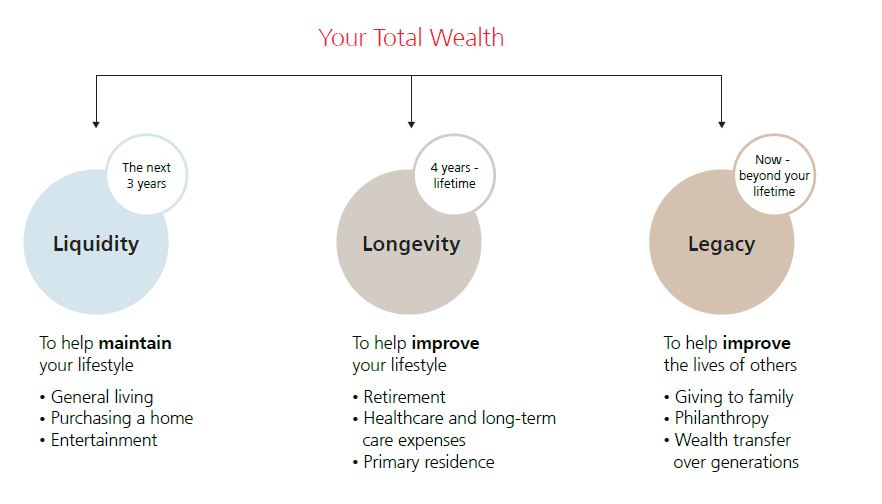

Over the years, I have been asked by readers on guidance on how to develop their personal IPS. I have hedged my answers, since I am not in a position to give investment advice for the reasons I cited. However, this liquidity based strategy from UBS can served as a useful framework for creating an investment plan.

The approach calls for splitting an investment portfolio into three buckets:

- Liquidity: What you need for the next three years, which includes considering life and disability insurance needs.

- Longevity: What you need to for the next 4 years and your lifetime.

- Legacy: What you are going to leave for the kids.

On a separate topic, the recent equity market weakness would have moved the equity portion of many balanced portfolios below their equity target weight. The question then becomes, “When should you rebalance your portfolio weights as part of a disciplined investment process?”

The most obvious approach is to rebalance either periodically (quarterly, or annually) back to target weights. I call that the value approach of buying assets when they are cheap (gone down) and selling assets when they are expensive (gone up).

However, a past post from 2014 (see Rebalancing your portfolio for fun and profit) uncovered a research paper that indicated a price momentum strategy could yield better results. Here is the abstract [emphasis added]:

While a routinely rebalanced portfolio such as a 60-40 equity-bond mix is commonly employed by many investors, most do not understand that the rebalancing strategy adds risk. Rebalancing is similar to starting with a buy and hold portfolio and adding a short straddle (selling both a call and a put option) on the relative value of the portfolio assets. The option-like payoff to rebalancing induces negative convexity by magnifying drawdowns when there are pronounced divergences in asset returns. The expected return from rebalancing is compensation for this extra risk. We show how a higher-frequency momentum overlay can reduce the risks induced by rebalancing by improving the timing of the rebalance. This smart rebalancing, which incorporates a momentum overlay, shows relatively stable portfolio weights and reduced drawdowns.

Go check it out.

Cam, Happy New Year and great post! I loved this guy’s video! As a broker, I can tell you he is spot on with regards to how we think! Answering to clients makes all the difference! Just as a small request, it would be great to get your current perspective on relative sector strength in this market!

Regards,

Mike

Friends

Happy new year and kudos to Cam, for the prescient calls he has made.

As regards portfolio construction (see above), Meb Faber’s book, Global Asset allocation (free on his website), gives a very good analysis of about a dozen or so portfolios, and their life long performance. As a rule of thumb, 20% each in real estate, stocks, bonds, cash and alternatives (gold, farm land, etc.), gives an excellent asset diversification. This lay out is much less volatile, than a portfolio of larger component of stocks, and has created competitive (REAL) returns with lower volatility than stocks. Read the book.

To Ken’s point, 50-60% stock market losses are an anomaly. He is right. We have had two so far, this century! The average market loss is more like the 33% (Fibonacci retracement) pull back from a peak value. Cam has circled 2100 level as the first level of massive support (see above graph). We may not get there unless there is a US recession (so far no one is taking about it).

What Cam has not penciled in is a time frame. Let us try and estimate the time frame of what could be a point in time of maximum pain. This may be end March, 2019, when the China “90 day deadline” comes into play and also the Brexit drop dead date. Furthermore, President Trump, would soon find out what a democrat House really means, by that time. So, end March could unleash an “Unbridled Trump”.

So, let us ask what an “Unbridled Trump” could mean. It may mean, simply firing Mr. Powell or fire Mr. Mueller, or one of the inner coterie of Trump House under spotlight of Mr. Mueller, or a “deep throat” that leaks Trump taxes. Let your imagination run wild, and yes, Cam is right, it shall not be a Bay of Pigs or Mr. Khruschev in the back yard this time. But, there will be a similar event, like a disorderly shadow that eclipses the White House. For now, we have only had 2% losses per day in the stock market. For a bear market bottom, how about 5% pullbacks? How about spot VIX that rises to 50-100? Such market action(s) will need a catalyst, and Trump unleashed, may do it. So far, the market sell off has been too orderly, too nice. No panics have set in yet (remember February 2018 bottom when massive short bets on VIX, took the market down? So far, market has been playing Mr. nice. There are still too many bulls out there (see graphs in the last two missives), there are no big buyouts or bail outs (of the Buffet type).

So, for longer term buy and hold portfolios, this could well turn out to be an awesome time to get fully invested (Ken is probably correct on his call), gradually, over say a 6-12 month time frame. Bull markets are not a decade long affair, but more like a two decade affair. Most investors in their life time see three bull markets. The first one when they have no money, the last one when they are too old to invest and a middle one in between. Starting circa 2000, this could well turn out to be a secular bull, that may have another decade to run (from the 2009 bottom; the 2009 bottom was the “echo” of the 2000 bear bottom; again, what I have written here, plays into Ken’s hands, though he has not said it in so many words).

As assets go, 2010-12 was a bear market bottom in real estate. It was a great time to buy investement real estate on the cheap for a lifetime buy and hold, for those who were building a portfolio for longevity.

Hopefully the bear market that we are now seeing, is a cyclical bear, in a secular bull (secular = longer term). For those who are underinvested, this may create an opportunity to buy stocks at cheaper valuations. So, who has been underinvested in the market? Mr. Buffet himself has been hoarding cash since circa 2012 or so. Why has Berkshire been hoarding cash? We are seeing the reasons why, as I write this.

A lot of what I have written here are guesses. Only time will tell, how equity markets play out or not. For now, we are not seeing “credit events”, though that does not mean, they will not happen. For now, it appears that we do not have a “house of pain” for a convincing bottom. So, cheers, despite all my Grinchy writing.

2100 support circled on a graph above, …not in the post I’m looking at. Is there a link you followed to get this graph?

I truly believe the old, widely diversified structured 60-40 or similar portfolio that gets rebalanced occasionally will do very poorly. That philosophy is based on return to mean. The world is no longer a place that returns to means. One must have a tactical asset allocation strategy that reduces equities when they are more risky and buys when safer. Using momentum to own sectors or countries that are outperforming and avoiding those that stumble is critical. The old return to mean approach for example would own an allocation to an area like Europe, America or wherever that could be in decline for a decade and rebalance to buy more (selling winners) as it falls. Momentum strategy avoids the losers.

So, today’s job numbers paints a picture of how the US economy is humming nicely. Politics and fear of fear itself has gotten the US markets to one of its fastest quarterly loss. That said, it does not appear that the US economy is entering a recession. One really needs to worry if the US economy enters a recession, otherwise, this may be a pull back without recession (it happens).

Next pit stop to watch: Earnings in about ten days. Watching what happens as the S&P 500 retraces to 2500. A failure here would be bad.

The nice thing about investing for yourself is you only have to answer for yourself. This simplifies decision making and process.

One thing that confuses a lot is survivorship bias…You have a process and it worked well, but was it the process or luck?

Keeping things simple is a good process I think. For example, taking a beaten down sector where prices are way down, but you know that demand will be around for a long time, buy and just wait.

Long term indicators like monthly closes are simple to follow, but they don’t come very often.

Another example is the “let the winners ride vs don’t be greedy” it’s tough because these two philosophies can contradict each other…then survivorship shows up…Look at NFLX, or AAPL…should u still hold them?

But how does a money manager buy down and out stocks or sectors, or just follow monthly closes above or below a moving average? They cannot…this is the advantage of the solitary investor….at least I think it is.

Meanwhile, trade a small position, read and inform yourself.