Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Asset Allocation Model is an asset allocation model that applies trend-following principles based on the inputs of global stock and commodity prices. This model has a shorter time horizon and tends to turn over about 4-6 times a year. The performance and full details of a model portfolio based on the out-of-sample signals of the Trend Model can be found here.

My inner trader uses a trading model, which is a blend of price momentum (is the Trend Model becoming more bullish, or bearish?) and overbought/oversold extremes (don’t buy if the trend is overbought, and vice versa). Subscribers receive real-time alerts of model changes, and a hypothetical trading record of the email alerts is updated weekly here. The hypothetical trading record of the trading model of the real-time alerts that began in March 2016 is shown below.

The latest signals of each model are as follows:

- Ultimate market timing model: Sell equities

- Trend Model signal: Neutral

- Trading model: Bearish

Update schedule: I generally update model readings on my site on weekends. I am also on Twitter at @humblestudent and on Mastodon at @humblestudent@toot.community. Subscribers receive real-time alerts of trading model changes, and a hypothetical trading record of those email alerts is shown here.

Subscribers can access the latest signal in real-time here.

A risk-on stampede?

I pointed out in the past that risk appetite in 2022 can largely be attributable to changes in the USD. The S&P 500 has shown a close inverse correlation to the greenback. Now that the USD has decisively violated trend line support, does that mean that it’s time for investors to stampede into a risk-on trade?

What are the fundamentals that explain the technical breakdown in the USD? Has the Fed signaled that it is about to out-dove the European Central Bank and other major central banks, which would narrow interest rate differentials and weaken the dollar? Will other central banks out-hawk the Fed?

A positioning whipsaw

The risk-on rally since the soft October CPI report can mainly be attributable to the combination of a positive surprise and a crowded short, which led to a price whipsaw based on excessive positioning.

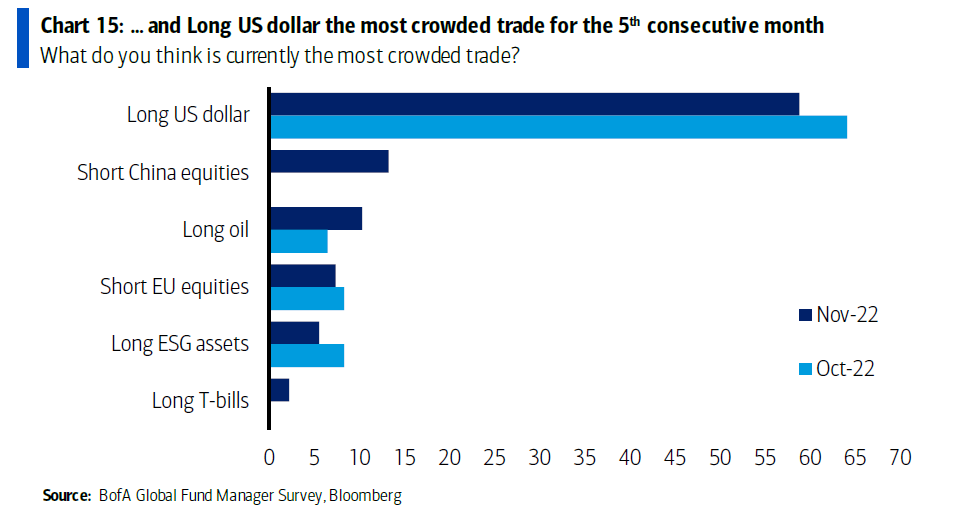

Respondents in the latest BoA Global Fund Manager Survey agreed that the most crowded trade for the fifth consecutive month is a USD long, which is a risk-off position.

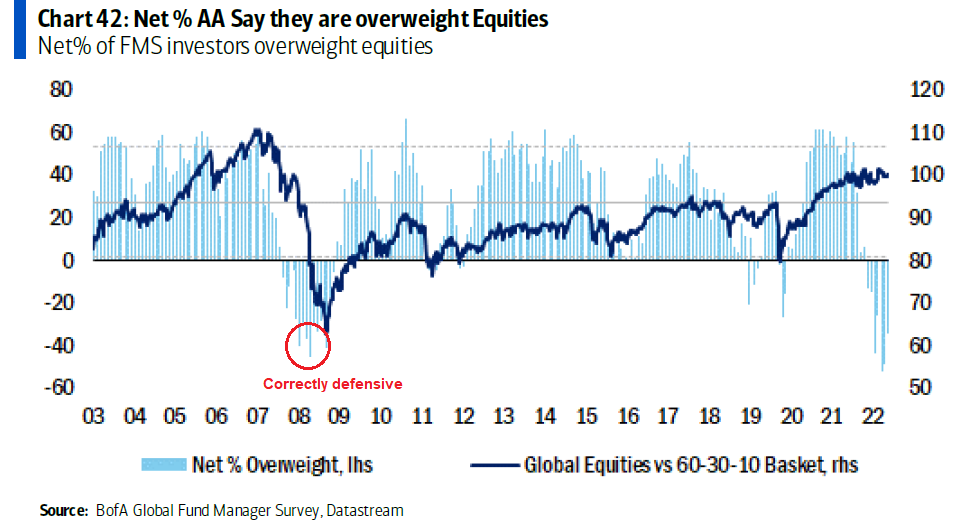

The survey also showed a crowded underweight in equity positioning, with the caveat that respondents were correctly cautious the last time sentiment reached similar lows during the 2008 bear market.

The holdings report of the DBMF active ETF provides a useful window into the positioning of managed futures commodity trading advisers or CTAs. DBMF is short Treasuries and rates, long the USD, and roughly flat equities. It was therefore no surprise that a soft CPI report sparked a risk-on stampede in bond prices.

The bond price surge is probably on its last legs. Garfield Reynolds, Chief Rates Correspondent for Bloomberg News in Asia, observed that the market reaction to St. Louis Fed President Jim Bullard’s remarks that the Fed Funds policy rate needs to reach at least 5% put an abrupt end to the bond buying stampede as bond market volatility turns up.

A look at the action for implied volatility gauges underscores the potential for further wild moves. The classic MOVE Index, based on one-month volatility, tumbled to well below the three-month gauge and has since rebounded. The last two times that happened, in August and June, both indexes soared to fresh highs. Get ready for a wild year-end, because it looks like the bond market is gearing up for one.

A stall ahead?

The equity market’s technical internals indicate that the rally is losing momentum. The S&P 500 advance stalled at the key Fibonacci retracement level of 4000 with a spinning top candlestick on the weekly chart, indicating a possible inflection point. This is the perfect spot for the bears to become more active.

The NYSE McClellan Oscillator recycled from an overbought condition, which is an ominous sign that price momentum is rolling over.

The 5-day correlation between the S&P 500 and VVIX, which is the volatility of the VIX, spiked while NYMO is positive. There were 26 such signals in the last five years, of which 18 resolved bearishly and eight bullishly.

Sentiment isn’t excessively bearishly anymore. The Fear & Greed Index has evolved from an extreme fear reading to greed.

Similarly, the NAAIM Exposure Index, which measures the sentiment of RIAs managing retail investor funds, has steadily recovered from a bearish extreme.

Negative seasonality

The stock market will also face short and intermediate-term seasonal headwinds. While US Thanksgiving week has a record of positive seasonality, Mark Hulbert pointed out that the 2022 FIFA World Cup begins on November 20 and stock returns tend to be weak during the tournament.

Looking into 2023, conventional seasonality analysis shows that stock prices tend to be strong during the third year of a Presidential cycle. However, Jeroen Blokland pointed out that the US economy has never experienced a recession during the third year of a Presidential term. 2023 will be the likely exception, which will create headwinds for stock prices in the first half of next year.

In conclusion, the recent risk-on episode is attributable to the combination of excessively bearish sentiment and a positive inflation surprise. Most of the effects of the buying stampede have likely dissipated. Technical conditions are weak and the bear market is poised to resume.

Subscribers received an alert on Thursday that my inner trader had re-entered a short position in the S&P 500.

Disclosure: Long SPXU

Negative seasonality due to 2022 FIFA CUP is a silly thing, because there is no real link with economy/markets, the correlation with negative markets is because it always runs during summertime (after the “sell in may”)…but not the 2022 edition

Great comment.

Also, the US is not really a big soccer playing nation. Americans don’t care about soccer.

On the other hand, in some countries, esp in Latin American, soccer teams have a disproportionate burden to deliver on national pride. There I can see losing a soccer game having some emotional impact on the stock market.

seasonality wise, mid-term election may mean the recent ‘rip’ has further legs to go. Bear rally generally is surprising in strengthen and duration because of the bearish sentiment (and short positioning).