There is a growing acceptance among investors that the global economy is sliding into recession. S&P Global, which was formerly known as IHS Markit, reported:

The global manufacturing PMI survey’s Output Index, which acts as a reliable advance indicator of actual worldwide output trends several months ahead of comparable official data (see chart 2), signaled stalled production in July. The stagnation signals a faltering of the global production rebound seen in June from two months of contraction in April and May.

The conventional view suggests a synchronized global recession. The more nuanced view is the world is undergoing a rolling recession, which offers more opportunities for investors.

A rolling recession

A more detailed analysis of the new orders component of manufacturing PMI shows that not all regions are the same. In particular, new orders in the eurozone have been the worst, while Asia ex-Japan and China have performed the best. In other words, it’s a rolling recession as economic weakness rolls from one region to the next. Investors should position themselves accordingly.

With that preface, I will examine the outlooks for the three major global trade blocs, Europe, China, and the US.

Eurozone: Recession leader

Staring in Europe, the eurozone manufacturing PMI has turned sharply lower, indicating an almost inevitable recession.

The weakness is also reflected in the Citigroup Eurozone Economic Surprise Index, which measures whether economic indicators are beating or missing expectations.

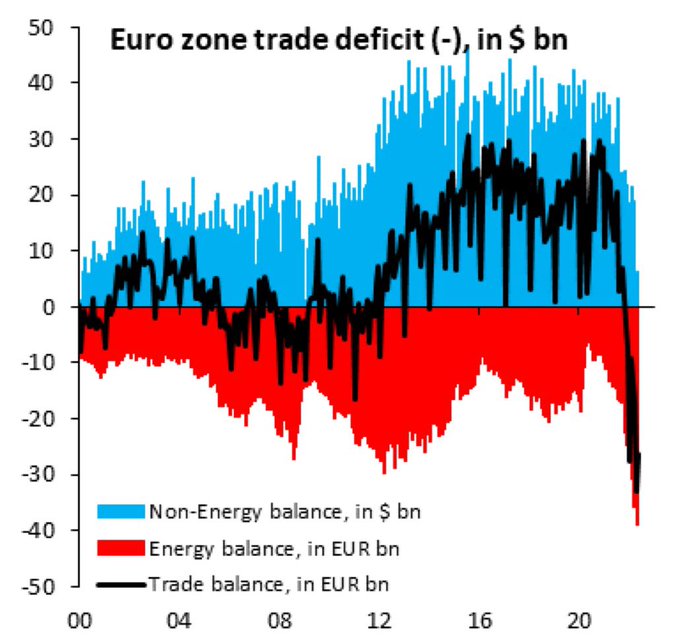

There are two explanations for economic weakness in the eurozone, as shown by the eurozone trade balance. The more obvious reason is rising energy costs as a result of the Russia-Ukraine war. But the trade balance in the non-energy sector has been plunging as well. The reason is weakness in China.

A slump in China

An analysis of the Chinese economy reveals a broad picture of softness. Its trade balance with Germany and Korea, which export capital equipment to China, is in deficit, indicating weakness in manufacturing and exports.

China is beset by the triple whammy of property market troubles, falling consumer confidence, and a lack of stimulus. Shehzad Qazi of China Beige Book International, which monitors the Chinese economy on a bottom-up basis, stated in a CNBC interview that he is seeing widespread weakness and the country’s manufacturing, services, and retail sectors are all struggling.

Evergrande failed to deliver a promised US$300 billion restructuring plan last week, which caused further loss of confidence in China’s property sector. Developers are facing a liquidity crunch and high leverage ratios. Half-built and incomplete projects are leading to a mortgage boycott groundswell, which is feeding into a negative feedback loop as suppliers to property developers are in turn facing liquidity problems. Bloomberg reported that Chinese banks may face up to $350 billion in loan losses from the property crisis – and that figure doesn’t include the non-bank financing that developers tapped from the shadow banking system.

As Chinese developers encounter a cash crunch, the overdue accounts of their suppliers are growing, which is creating a domino effect and negative feedback loop for the economy.

In addition, China’s zero-COVID lockdowns have shaken consumer confidence, which is also leading to the malaise in the labor market as employers are hesitant to hire in an uncertain and weak environment. Shehzad Qazi of China Beige Book International recently testified before the U.S.-China Economic and Security Review Commission. He had a sobering outlook for China’s zero-COVID policy and forecasted that it’s here to stay for some time.

At this point it can be reasonably assumed, that China’s zero-COVID policy is here to stay until the country has access to mRNA vaccines with high efficacy rates and is also able to vaccinate a vast majority of its population, especially the elderly. This pushes any lifting of zero-COVID as it is implemented today well into 2023 if not beyond.

This then suggests that the Chinese economy will remain under pressure for the foreseeablefuture as new virus outbreaks emerge and lockdowns go into effect, especially in more economically developed regions. Furthermore, it paints an especially concerning picture for the services and retail sectors of the Chinese economy which have suffered the most from lockdowns. This, of course, has long-term consequences as it will only push any rebalancing to a consumption-driven economy further into the future.

In the past, Beijing has stepped in with new stimulus whenever the economic outlook has skidded this badly. However, the July Politburo meeting offered little relief. Officials affirmed that the zero-COVID policy takes priority over growth imperatives. Policy makers indicated that they will stay their current course and not look to ramp up policy support.

Current economic operations are facing some prominent contradictions and problems. We should maintain strategic concentration and firmly do our own work.

Officials made it clear that COVID policy tops the agenda as pandemic containment is the pre-condition to stable economic growth: “When an outbreak occurs, we must immediately and strictly prevent and control it.” In short, senior officials offered no new ideas for economic management in the second half of the year and no initiative that hasn’t already been telegraphed:

- Boosting infrastructure investment through special purpose bonds issued by provincial authorities and supplemented by policy bank credit.

- A continued focus on risk, which further limits stimulus programs.

- An acknowledgment that there is a need to ensure housing is delivered in reaction to recent mortgage boycotts.

The WSJ reports that tension is growing between the central government and regional authorities. Regional governments are becoming increasingly growth constrained and their finances are shaky as the source of funds has been land sales in the past. As Bejing increases its focus on risk control, it is creating a credit crunch for local governments.

China’s property market slowdown and strains from the country’s zero-Covid-19 campaign are putting new pressure on local governments’ finances, forcing some to rein in spending, adding another drag on China’s weakened economy.

Local governments, which shoulder much of the expense for education, healthcare and other services in China, were already struggling with high debt loads and unsustainable expenses as 2022 began.

Now the strains are getting worse. Cities must fund costly mass Covid testing programs imposed by Beijing to try to keep Covid-19 caseloads near zero. They are also being asked by Beijing to support stimulus meant to revive growth, including tens of billions of dollars’ worth of railways and other infrastructure projects.

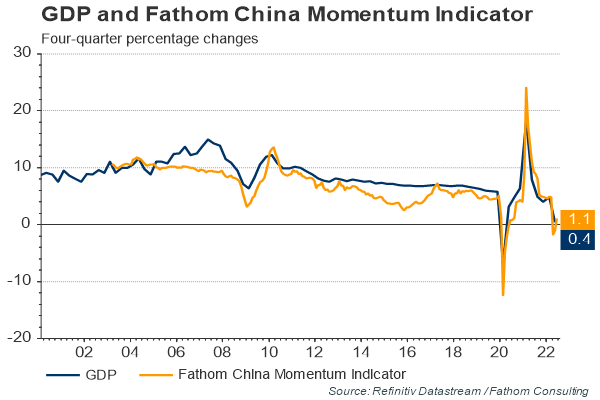

Is China in a recession? It’s a close call. The Fathom China Momentum Indicator has fallen to 0.2%, indicating extremely grim growth conditions.

While the initial read of the manufacturing PMI of Asia ex-Japan and China was one of the bright spots, investors shouldn’t interpret that in an overly positive way. When China sneezes, the rest of the region catches a cold. Already, the manufacturing PMI of cyclical bellwether South Korea slumped into contraction territory in July.

Recession in America?

Across the Pacific, America isn’t in recession despite two consecutive quarters of negative GDP print. Ryan Detrick pointed out that NBER, which is the committee that is the ultimate arbiter of recessions, focuses on six metrics: nonfarm payrolls, household survey, real personal income (less transfers), real PCE, industrial production, and real manufacturing. Five of the six are positive on a YTD basis, indicating there is no recession. That’s the good news.

The bad news is the economy is weak and sliding into recession. New Deal democrat, who maintains a disciplined process of recession forecasting with a set of coincident, short-leading, and long-leading indicators, recently conceded that a recession in Q1 is almost a certainty.

The long leading forecast continued to be negative, despite even more resilient corporate profits. My “Recession Watch” start time of Q1 of next year continues. The short term forecast also remains negative, as initial jobless claims and the regional Fed new orders indexes continue to trend more or to remain negative.

NDD did leave the door open for a soft landing:

Hopes for a “soft landing” must rely on the possibility that gas prices will decline further enough fast enough to make a big dent in inflation, assisting consumer spending, and perhaps making the Fed pause, as otherwise all the signs point to recession soon, with only the start time – and the intensity – open to discussion.

Joe Wiesenthal at Bloomberg also cited some encouraging signs of a soft landing.

- Housing may already be stabilizing a little bit after the initial mortgage-rate shock

- Yesterday we got an ISM Services reading showing an unexpected gain in July

- June durable-goods orders also came in better than expected

- ISM Manufacturing index came in better than expected as well. And not only that, there was a major drop in the prices paid index.

- Gas prices have fallen for 50 straight days.

- Earnings have been decent, not amazing, but no widespread signs that the bottom is falling out of demand. Yesterday, Booking Holdings, the online travel company, warned of some softness out there, but it noted that North America was holding up the best of all regions.

However, the Fed has embarked on a concerted push to convince the markets that it is not on the verge of a dovish pivot. It flooded the speaker circuit with a variety of interviews and speeches by Fed regional presidents, beginning with Minneapolis Fed President Neel Kashkari, who is regarded as a dove. In a NY Times interview, Kashkari said officials are a long way from backing off the inflation fight. San Francisco Fed President Mary Daly, another dove, told a Reuters Twitter Space that the neutral rate won’t be reached until about 3.1%. And it will need to be restrictive. St. Louis Fed President James Bullard, a hawk, said he favored a Fed Funds rate of 3.75-4.00% by the end of 2022.

The strong July Jobs Report cemented the expectations of a hawkish Fed. Non-Farm Payroll came in at 528K (250K expected). Average hourly earnings rose 0.5% for the month (0.3% expected), and the unemployment rate fell from 3.6% to 3.5% (3.6% expected). These figures are all above expectations indicating a strong economy and room for the Fed to take more aggressive steps to tighten monetary policy.

My base case calls for the US to enter a recession in early 2023.

Investment implications

What does this all mean for investors? The conventional recession trade is to buy USD assets, with Treasury assets as the safe haven. A better way might be to buy JPY assets. The BoJ has bucked the global trend with a continued easy monetary policy while all other major central banks have tightened, which has caused incredible weakness in the JPY. If the world goes into recession, global central banks will be moving towards BoJ policy and not the other way around. This form of reverse policy convergence will put strong upward pressure on the JPY exchange rate.

For investors with equity holdings, regional rotation will be the name of the game. Investors will have to consider the tension between valuation and price momentum. The accompanying chart shows the relative performance of regional markets relative to the MSCI All-Country World Index (ACWI). The US is the market leader, and the NASDAQ 100 has been the standout since early June. Japan has gone sideways while Europe, China, and other EM have been weak.

Valuation, as measured by forward P/E, tells a different story. The US is the outlier and highly valued relative to the other markets, whose forward P/E ratios are all clustered together.

Here is how I would approach rotation among the global regions.

- Overweight the US: It’s not in a recession yet and it’s the relative strength leadership. But don’t be overly complacent. Analysis from Ned Davis Research indicates that if a recession is on the horizon, the market is likely to re-test the June lows.

- Wait for Europe to turn: There is a reason why some markets are cheap. Europe is probably already in recession, but the markets may have already discounted the region’s anemic growth outlook. However, European equities present strong upside potential. Wait for a turn in relative strength and rotate from the US to Europe. The relative performance of MSCI Poland (bottom two panels) may serve as a useful barometer of geopolitical risk, which could be a buy signal for the region if risk premium fades.

- Avoid China and Asia: China is the wildcard. Investors should wait for greater policy clarity from Beijing before committing funds to the region.

As important as Cam’s analysis is one should not over look the valuation and role that the US dollar is playing presently. My personal view is that the dollar is over valued. You can already see a topping process beginning to appear in the charts. If my analysis is correct the normal beneficiaries will be resource rich countries like Brazil and precious metals. I personally like Gold and Silver. Gold and Silver equities are extremely under valued and offer a good risk reward for long term investors with the normal caveat that I could be wrong and everyone should do they are own personal analysis.

I forgot to mention that in the interest of full disclosure I normally am long or I am going to be long any position that I mention. The last position was QQQs which I mentioned and traded from the long side.

At some point there will be a move to gold when a crisis hits. I have to say that I am not a gold bug simply because most of the gold just goes into some vault, which seems to be pretty pointless. I think that the above ground gold is enough to supply the industrial need for something like 100 years. But yeah the knee jerk will happen and gold will shoot up. Of the PMs my favorite is silver because it is so useful and gets used, most supply is as a byproduct of other mining and because of it’s industrial use the price will go down if the market tanks which would present a good entry point. Platinum has lagged gold and palladium I wonder about it’s future as more and more EVs are produced.

The dollar may go higher if things get worse elsewhere, of course eventually it goes down, but what time frame?

Fed’s North Star, as they have made it abundantly clear, is inflation. The progress in reducing inflation, as measured by CPI/PCE is likely to determine the path. Fidelity thinks inflation may drop to 7% by end of 2022 and get to 3-4% in 12-24 months. Would that trigger rate cut in first half of 2023? A pause at best in my view due to lag in monetary policy.

Investment implications-China and Europe are in economic distress and US is slowing. What’s the catalyst to turn around the economies? Peace breaks out in Ukraine, Russia becomes a rational actor, Xi Jinping stops flexing his might?

I think a period of heightened uncertainty and turmoil is ahead of us inspite of the rally in US.

I am staying cautious! Short duration, higher quality bonds and stocks are my focus along with careful trading profits, if possible.

The only exception is something breaks – a financial crisis that threatens the banking system. Not happening in the US, but some EM and overleveraged DMs with hot property markets are vulnerable (Australia/NZ/Canada/Norway/Sweden).

Let’s just say nobody has any idea, including Fed. What if equities continue to move up and on a collision course with the Fed intent. Does Fed needs to crush the Markets in any which way possible? Same as for labor market.

Many things happening now are defying what textbooks say. These facts should give policy makers something to ponder on, not fixated on dogmatic and rigid beliefs. People like Jim Bullard should remember that opening mouth would remove any doubt of being seen as a fool. Ditto talking heads on TV. Just say you don’t know and you will earn respect.

Current context is like a few random processes going at the same time. During this optimization/minimization phase it is best just to observe and be prudent. Coming out of this period, we will learn something new and adjust.

Remember what Bill Dudley said. One of the ways the Fed cools off the economy is through the asset price mechanism. In other words, they have to crush the balance sheets of the rich (because that’s where the money is) in order to cool inflation and inflation expectations.

So yes, the Fed wants the stock market to go down in order to drive inflation down. If the market continues to go risk-on, the Fed will turn more hawkish.

Right.

Fed will drive inflation down. The main tools are rates and QT. Strong labor market gives them more room to stay aggressive.

Lot of other stuff that’s going on may help or hinder Fed’s mission. Market is expecting Fed to blink much sooner based on expectations coming down. I think that’s where volatility will come from.

Just a further thought on the causes of inflation. My impression is that people seem to think that inflation will simply come down because of energy prices declining and supply bottlenecks are being fixed.

However if we do think about our “father’s recession” the normal reason for inflation is the Phillips curve that states that inflation and unemployment have an inverse relationship. Maybe this is what we are now seeing here with a very tight jobs market and unemployment forecast to go even lower. That is, the primary cause for inflation will now become wages growth.

It’s a bit of both. Energy and supply chain bottlenecks began with the COVID Crisis and pushed inflation up. Initially the Fed thought that this would dissipate, hence the transitory narrative.

Inflation pressures eventually broadened out to other items not directly affected by above and services inflation rose. That’s why the Fed became more aggressive.

The conventional way of breaking inflation expectations is through the wage channel. Make sure wages don’t catch up with inflation pressures and inflationary expectations eventually fade. Of course that creates inequality problems as labor alwyas gets shafted in the end. Both Powell and Yellen have spoken extensively on this issue.

Ya, once the primary contribution for inflation becomes wage growth, inflation tends to stick around for much longer.