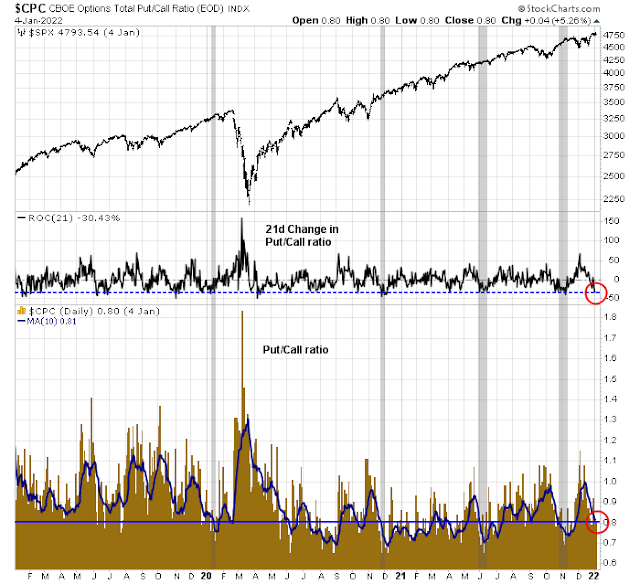

Mid-week market update: As 2022 opens, I have become increasingly cautious about the stock market. The put/call ratio (CPC) is a bit low, indicating rising complacency. Past instances of a combination of a rapidly falling CPC and low CPC have seen the market struggle to advance. While this is not immediately bearish, it is a flag for caution.

Bearish triggers

As long as central banks were in unconventional policy mode, the party could keep going. But the asset and credit bubbles may deflate in 2022 when policy normalization starts. Moreover, inflation, slower growth, and geopolitical and systemic risks could create the conditions for a market correction in 2022. Come what may, investors are likely to remain on the edge of their seats for most of the year.

Participants generally noted that, given their individual outlooks for the economy, the labor market, and inflation, it may become warranted to increase the federal funds rate sooner or at a faster pace than participants had earlier anticipated. Some participants also noted that it could be appropriate to begin to reduce the size of the Federal Reserve’s balance sheet relatively soon after beginning to raise the federal funds rate. Some participants judged that a less accommodative future stance of policy would likely be warranted and that the Committee should convey a strong commitment to address elevated inflation pressures. These participants noted, however, that a measured approach to tightening policy would help enable the Committee to assess incoming data and be in position to react to the full range of plausible economic outcomes.

Some participants judged that a significant amount of balance sheet shrinkage could be appropriate over the normalization process, especially in light of abundant liquidity in money markets and elevated usage of the ON RRP facility.

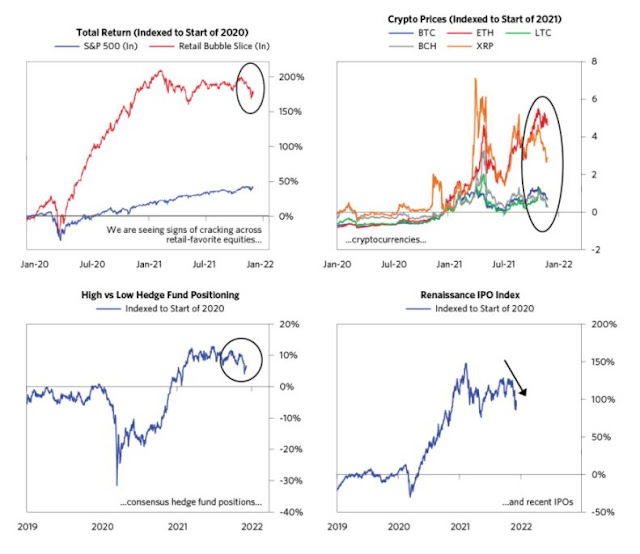

The popping speculative growth bubble

As the Fed has shifted toward tapering and a slowing in the flood of liquidity has begun to get priced in, we are seeing cracks emerge in the bubbliest segments of the market.

As we have noted before, the unprecedented flood of liquidity following COVID has caused our bubble measures to flash red in certain pockets of global markets. We have studied bubbles and built measures of whether economies or individual markets are in them. By our measures, there are likely bubbles in emerging technology stocks, SPACs, cryptocurrencies, NFTs, collectibles, etc. These bubbles have been particularly pronounced in the US, where households piled savings into the markets as their incomes were supported by massive government checks, their spending was curtailed by the lockdown, and lower-cost trading driven by competition and technology made investing (and speculation) easier than ever before.

Of the several key risks that Bridgewater outlined, there are two that I am most concerned about:

- Forced retail liquidation effect: “If the bubble turns, retail traders, especially those who have used leverage either directly or via options, may be forced to liquidate other positions, widening the breadth of the sell-off.”

- Cash generative large-cap growth stocks are not immune to a popped bubble. “These [startup] companies, as well as the broader venture capital ecosystem, have important implications for the earnings of the most important companies in the S&P 500. As shown below, early stage companies deploy a significant share of their cash on things like cloud services and online advertising, which then ends up being revenue for the US tech giants… customer acquisition (Facebook, Google) and cloud providers (Amazon, Microsoft), these companies end up earning significant profits from startup spending.”

Santa Claus has left the building

In conclusion, I don’t mean to imply that the market is about to crash, but the stock market is vulnerable to a setback. I don’t know if today’s risk-off reaction to the release of the FOMC minutes is the bearish trigger.

Subscribers received an alert that my inner trader sold all his long positions yesterday and stepped to the sidelines, citing event risks such as the release of the FOMC minutes today and Friday’s NFP report. If this is the start of a major bear leg, my inner trader is waiting for the sell signal and believes there will be sufficient time to profit accordingly in a falling market.

Hi Cam,

I want to congratulate you on your exit from your long trade. You could not have timed it better.

Cam

I agree with Mr. Intrepid.

Even more impressive as this makes it 8 straight profitable trades for the trading model. Congrats!

Excellent timing/Call. Congrats, Cam.

Good timing on your sell Cam. I used used that signal to trim my investment positions substantially. Felling good right now.

I think Cam’s note about de-risking the portfolio was pivotal. It provided the nudge I needed to do it.

Katie Stockton expects a 10%+ correction in the first quarter. She suggested macro level hedges( inverse ETFs, options etc). Cam’s analysis will guide us with timing.

Well, here is for the hate mail lol, it wasn’t so much timing as luck….because these things cannot be timed. But the FOMC minutes release was a known factor, and the moral of the story is “it’s worth paying attention to these things if you are contemplating a move to the sidelines” I say this not to diss Cam but to dissuade people, including myself from trying to pinpoint tops or bottoms. If it happens thank your rabbit’s foot.

A lot of smoke and mirrors going on. The Fed had telegraphed quite well what was coming. Words like could mean little, at least should implies intent, even if just posturing. Hey an asteroid “could” strike earth in 2032 with mass extinction, or we “could” get one of those solar outbursts that fries globally electronics, or even better the Yellowstone caldera will erupt, almost certainly, “could “be next year or in 100,000.

This is a knee jerk. Could things go down, of course, but I think the trillions tossed to retail and companies is not all gone. There will most likely be many buybacks, gotta get those options out.

Today’s volume was not huge, so we could easily go lower for a while but I don’t think this is it for the bull, have to see how the credit markets behave. What if in 2 weeks we see signs that Omicron has burned itself out, nobody left to infect? What will the market do? My impression was that rising rates leads the market, in the sense that before we tank, rates had to go up for a while…well they have not…they are talking about it, so is the market leading rates? Could be, because things are truly messed up, negative rates in Europe, oil went negative, briefly, but really? Could Tesla go negative?

If this drags on we can use Cam’s bottom spotting for us….went full circle huh? Spotting possible bottoms is not timing to the day. I’m sure Cam would say when his models ding “This “could” be a bottom”

The most important influence on stocks and house prices since 2012 has been the “Wealth Effect” by the Fed. They announced the start of this economic strategy and have used it ever since. The Wealth Effect is when the Fed forces interest rates down to artificially low levels (QE and other hocus pocus) to boost the prices of houses and stocks. They calculate about 3% of extra wealth will be spent.

When they reverse the stimulus and ‘normalize’ interest rates like they did in 2018 (to cause a quick 20% drop) you have the Negative Wealth Effect. That is what’s coming in 2022. Like it will be nasty.

This is a big deal because the amount of Fed Wealth Effect stimulus has been off the charts in the last two years. They caused $27 trillion in wealth to be added from the beginning of 2020 to mid 2021. Stock wealth for the top 50% of households was up 40% and homes 16% during a downturn. Did these folks become Warren Buffett type experts or did everyone renovate their homes? No, they got free money via asset value growth from the Fed.

The folks in the bottom 50% that don’t own stocks and houses are getting the inflation and front-line Covid jobs. The huge increase in home prices means their dreams of owning a home are crushed. The wealth divide has shot much wider in the last two year. According to some experts, we can expect social unrest due to the unfairness of this.

Let me also say, the upper 50% that got the 27 trillion free money gift from the Federal Government don’t want to pay extra taxes to fund the Build Back Better to the tune of 175 billion for ten years or 1.75 trillion total. That is 1.5% of the gift per year. I can only think people are not understanding where this free money came from to be so greedy on not wanting to send some small portion back to to the government to help some good causes. It’s one thing to object to taxes when the government wants to take back hard earned income i the past but when you are showered with huge amounts of free money and want to keep it all with the unfortunates suffering, that’s nasty.

Yes when this reverses it will get nasty. But I expect it to come in a bumpy fashion. People are selfish and so they don’t wish to give back.

Yodoc2003,

I think there is “Selfish” and then there is Foolish. We have to All live on this one, same planet, and I am not talking about Climate change here. But you are Right, humans are Selfish, maybe less then some animals, mostly more than others. However you can only EAT, OWN, ENJOY to a limited amount, rest can be shared for the common good. Anything that is overindulged in, will become toxic to you in one way or the other. We are as far as we humans are is because of first and foremost being a Social animal. We are forgetting that.

Look at the political divide we have in the USA, and elsewhere. Some people are willing to compromise and do things by consensus, the USA is not so good at that in my opinion, which is why we had all the problems during and after the last election, and this was back in the good old pre-covid days, when there was no recession, no inflation etc etc. How will things pan out when times get nasty? Keep a low profile

I think it is about process. Stick with a good process. One could argue that allowing divisions of wealth to become extreme is not good process, and that making a sacrifice for the greater good could be good process, but many will just do as they wish, blame others etc, I could go on, but it’s not necessary

And, the Sad truth is, You are RIGHT!! No compassion, or understanding of the other person’s plights. Everyone feels entitled to more than what they got, even though some actually do need help.

Lot of socialism implied in the note. I don’t mind if you want to be one but to say everyone should be is an overreach. I am also surprised as your profession is to help people make more money but now also want to tell people what they should do with it.

How much do you know about BBB? The true cost is not 1.75 but closer to 5.8 trillion. Or is that an inconvenient truth?

I for one would like to keep these pages apolitical.

Well, you are sovereign over what you think and the choices you have the power to make. So, make good choices, follow your beliefs and if others choose to be selfish, it is on them. Do what you think is right, not because everyone else agrees to it, but because you think it is right.

Isn’t it ironic that Jan 6 when the mob stormed the capitol with shall we say encouragement from Mr T is the feast day of the Epiphany, the 3 wise men?

Hahaha,

That’s true, I never made that connection. Also Coptic Christmas.