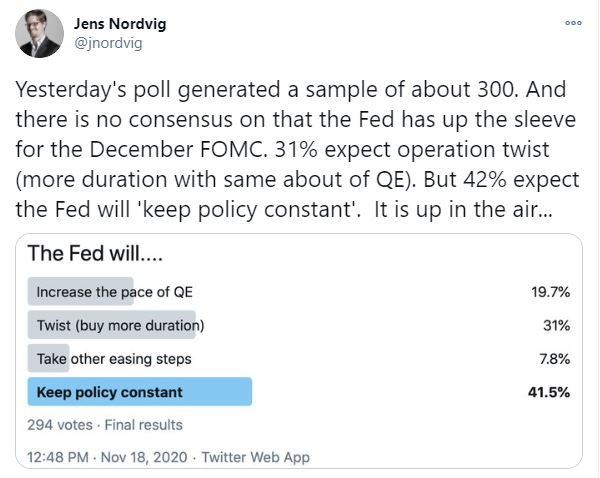

Jens Nordvig recently conducted an unscientific Twitter poll on the FOMC’s action at the December meeting/ While there was a small plurality leaning towards a “steady as she goes” course, there was a significant minority calling for another Operation Twist, in which the Fed shifts buying from the short end to the medium and long ends of the yield curve.

The November FOMC minutes reveal no clear consensus on the prospect of a twist, otherwise known as yield curve control (YCC).

A few participants indicated that asset purchases could also help guard against undesirable upward pressure on longer-term rates that could arise, for example, from higher-than-expected Treasury debt issuance. Several participants noted the possibility that there may be limits to the amount of additional accommodation that could be provided through increases in the Federal Reserve’s asset holdings in light of the low level of longer-term yields, and they expressed concerns that a significant expansion in asset holdings could have unintended consequences.

Here is why that matters.

Implicit yield curve control?

There are several ways of projecting the 10-year Treasury yield based on cyclical conditions. An analysis of the copper/gold ratio and the base metals/gold ratio indicates a range of 1.4% to 1.8%.

Nordea Markets observed that the cyclical/defensive sector ratio is pointing to a 10-year yield of over 2%.

These are all estimates, but they are all giving us the same message. The 10-year Treasury yield should be a lot higher than it is today. While the Fed has not explicitly engaged in YCC, just the threat of YCC may have served to hold down the 10-year yield.

Equity market implications

‘Even at the current level of the 10-year, the NASDAQ 100 should be underperforming the S&P 500.’

How do you determine this? What’s the calculation?

pretty strong close on the indexes today.

Quite the AH rally in index futures.

“There are several ways of projecting the 10-year Treasury yield based on cyclical conditions. An analysis of the copper/gold ratio and the base metals/gold ratio indicates a range of 1.4% to 1.8%”.

“Nordea Markets observed that the cyclical/defensive sector ratio is pointing to a 10-year yield of over 2%”.

I was watching CNBC today (!) and one of the commentators did discuss that the rally in the stock market would only be considered for real if money starts to come out of fixed income market. Current 10 year yields are showing a massive swing into fixed income markets (may be by the Fed and also Mutual funds etc.).

The Pre-Covid yield on the 10 year was around 1.75% and I would like to think that a ten year yield approaching 1.75% should seen as positive for the stock market. The vaccines should do their job and investors should be looking at the glass half full and get ready for a Post Covid economy.

The yields may rise slowly, stocks are likely to be higher once the vaccines get going (may be short term pull back; Cam has alluded to this in his previous missive).

What are the odds that we go through the early 2018 phase (brief negative correlation) again this time?

Namely, on the last graph, the inverted yield was dropping while the NDX:SPX trended up.

If I recall correctly, that was a period when BTC went hyperbolic (not unlike what’s happening today).

Or was that an isolated event unlikely to repeat in today’s environment?

I think Powell has learned his lesson in 2018, namely respecting the market messages. That’s the reason Yellen was so beloved by the Markets. The Markets today are saying to keep steepening in check. So that’s what we will be getting.

What my kids used to call ‘Opposite Day.’ Every position that inflicted pain yesterday is now poised to deliver gains today.

Closing all positions end of day.

Basically, I succeeded in reversing yesterday’s losses via new positions in VEU/ VTIAX + existing positions in EEM/ XLF/ RYSPX/ RYDHX – and right now I’m in capital preservation mode.

Starting the day @ 100% cash.

NIO/ AYRO/ FCEL are gapping down again -> this time to prices that have me interested.

Out of all three.

PLTR looks good for an entry here. ETCG also.