Mid-week market update: Posting will be lighter than usual, I was hit by a nasty flu bug this week and I am barely recovering.

It was the best of times, it was the worst of times. Two treaties (actually one of them isn’t a treaty but an MOU despite Trump’s objections to the term) have either been signed or about to be signed.

The lessor known agreement is the Treaty of Aachen, signed Macron and Merkel, to revive the EU, and as update to the Franco-German friendship pact the Élysée Treaty signed by de Gaulle and Adenauer in 1963. The Élysée Treaty was one of the key foundations of the European Union. No sooner than the treaty was signed, Der Spiegel wrote about the bickering than nearly scuttled the agreement:

Indeed, despite all the ceremony and pomp in Aachen, fundamental differences between the Germans and the French very nearly prevented them from reaching an agreement. To make matters worse, the two countries have trouble seeing eye to eye in an area that is particularly vital to Europe’s future: forging a joint defense and common policies on arms exports. German and French negotiators only barely managed to save the deal thanks to a secret supplementary agreement.

To be sure, the Élysée Treaty needed an update as the challenges for Europe have changed since 1963:

Throughout the history of the European Union, Germany and France have always served as both the leaders and the driving force of the European project. Close cooperation between the two countries is today more important than ever to counter everything from attacks by right-wing populists, to Russian subversion and American threats to impose import tariffs on European goods — not to mention the looming Brexit chaos that threatens to engulf Europe.

Then the squabbles began:

The crisis began more than a year ago, when Macron unveiled his vision for Europe in a speech at Sorbonne University in Paris — and received nothing but silence in response from Berlin. Since then, the two partners have quarreled like an old married couple nearly every chance they get, bickering over everything from a joint budget for the eurozone to the details of the digital services tax on major tech companies like Google and Apple and emission limits for nitrous oxide. In addition, Germany’s aspirations to become a permanent member of the United Nations Security Council are only halfheartedly supported by France. “I’m afraid there are a ton of issues where we have to get our act together,” a government official in Berlin complained.

One of the points of contention was over Nord Stream 2:

But their differences rarely surface as openly as they did in last week’s conflict over the Nord Stream 2 natural gas pipeline. The French had long embraced a neutralité politique, as they call it, to avoid sabotaging the German-Russian plans. But only a few weeks after the declarations of mutual devotion in Aachen, the two countries came within a hair’s breadth of a major diplomatic spat.

The evening before a vote on a contentious EU directive that would have severely impeded the gas project, the French Foreign Ministry released a statement that left officials in Berlin completely taken aback.

“France intends to support the adoption of such a directive,” it said in the press release. The Foreign Ministry showed little sympathy for the shocked reaction in Berlin, adding that the Germans were well aware of French reservations concerning the project, “but perhaps didn’t want to hear them.”

Both sides have differing views of defense policy:

There’s been much talk recently of Europe’s “strategic autonomy,” which is the official objective of EU defense policy. If the importance of NATO is likely to wane, Germany and France have no choice but to cooperate with each other, as officials in Paris and Berlin know perfectly well.

There is no lack of lofty intentions, but the reality of the relationship is an entirely different matter. “Germany and France have completely different traditions in some areas,” says Michael Roth, state minister at the Foreign Ministry in Berlin.

When it comes to security issues, the Germans always initially react with restraint, and military missions by the German armed forces, the Bundeswehr, are viewed as a last resort. By contrast, France sees itself as a global power capable of restoring order around the world, and Paris views its military as a natural instrument of foreign policy.

…and on it goes.

The other “treaty” is the upcoming US-China trade agreement, which was announced by Presidential tweet on Sunday. Despite Trump’s objections over terminology, it is being negotiated as a Memorandum of Understanding (MOU) rather than as a treaty. That’s because treaties are subject to Congressional ratification, whereas MOUs are not.

Soon after Trump tweet, doubts began to surface. Bloomberg outlined a series of analyst reactions summarized as “Trump Tariff Delay Doesn’t Mean Trade War Is Over, Analysts Say“. Bloomberg also reported that much of the objection related to how credibly the Chinese could commit to maintaining a stable exchange rate, and what that precisely means:

The U.S. and China haven’t yet agreed on the critical issue of enforcement in a proposed currency deal that would ensure Beijing lives up to its promise to not depreciate the yuan, four people familiar with the matter said.

Treasury Secretary Steven Mnuchin on Friday touted the currency pact as the strongest ever, though he offered no details, following two days of high-level talks in Washington between U.S. and Chinese officials. The discussions were extended into the weekend in search of a broad trade deal to prevent the U.S. from increasing tariffs on Chinese goods next week.

President Donald Trump has previously accused China of gaming its currency to gain a competitive advantage, though his Treasury Department has repeatedly declined to name the Asian nation a manipulator in its semi-annual reports on foreign-exchange markets.

Still, the U.S. asked China to keep the value of its currency, the yuan, stable as part of trade negotiations between the world’s two largest economies. If successful, that would neutralize any effort by Beijing to devalue its currency and make its exports cheaper to help counter American tariffs, people familiar with the ongoing talks said this week.

In addition, James Politi of the Financial Times noted that ending forced technology transfer would make China a more attractive place to invest, and therefore have the perverse effect of raising the trade deficit.

International agreements tend to be well-intentioned, but the devil is in the details of their implementation. More importantly for investors, here are the investment implications of these agreements.

Defining intention

Instead of getting lost in the weeds of the difficulties with each agreement, the critical question to ask is, “What is the intention of the agreement?”

In the case of the Treaty of Aachen, it is a re-affirmation of Franco-German leadership of the European Union. Both France and Germany are committed to the idea of a united Europe. Outsiders may be dismayed by the squabbles, but it is nothing more than the bickering of an old married couple committed to the relationship.

The choice of Aachen as the site to sign the treaty is highly symbolic. Aachen was the seat of Charlemagne`s Holy Roman Empire, which united central Europe during the Early Middle Age.

The choice of Annegret Kramp-Karrenbauer (AKK) to succeed Angela Merkel as the head of the CDU is equally significant for European unity. AKK hails from Saarland, which The Economist described as “a hilly federal state of only 1m inhabitants abutting Luxembourg and France”. The grandmother of Heiko Maas, Germany’s foreign minister and also a Saarlander, held three passports in her life without moving, Saarlanders are therefore have a high historical sensitivity to European conflict:

“Saarland was always marked or threatened by war,” adds Oliver Schwambach, an editor at the Saarbrücker Zeitung, the state’s most-read newspaper. He notes that Mr Maas’s grandmother never moved but held three passports during her lifetime: “So people here hate conflict of any sort. Elections here are less angry, politics is more mild than elsewhere.”

To be sure, this treaty will not fix everything that`s wrong with Europe, but Europe cannot exist without the foundation of a strong Franco-German relationship, and the Treaty of Aachen re-affirms that commitment. All the squabbling, and everything else is European Theatre.

Despite all of the hand wringing about a growth slowdown in Europe, and Germany barely avoiding a technical recession, major European stock indices are bottoming and turning up. I interpret this reaction as the market has already priced in much of the bad news.

In addition, the fragile European banking system, which did not entirely fix their problems from the last crisis, is not showing significant signs of stress. The relative performance of European financials are not very different from the relative performance of US financials. This is a sensitive barometer of possible trouble in Europe, and no alarms are ringing.

US-China: Cold War 2.0

By contrast, the intentions behind the US-China trade deal are very different. Its purpose is only to tone down and manage the trade tensions between the two countries, while other sources of friction remain unresolved. I warned about this over a year ago (see Sleep walking towards a possible trade war) when the US branded China as a “strategic competitor” in its National Security Strategy of 2017 (NSS). I had also highlighted a New Yorker article that the competition is occurring in the military dimension as well:

The Defense Department is trying to change that, an effort reflected in its latest National Defense Strategy. Syntactically, the document is fairly straightforward: the Pentagon wants more money to buy more stuff. But the type of war it plans to fight is novel. In short, the Pentagon is trying to move on from the war on terror. “Inter-state strategic competition, not terrorism, is now the primary concern in U.S. national security,” the strategy, which is being released later today, reads. China and Russia are now America’s “principal priorities.”

Even as the US and China negotiate on trade, the SCMP reported the US Navy is sending two ships through the Taiwan Straits, which exacerbates tensions with Beijing. In this context, trade frictions will remain under control as long as US-China relations remain calm in other dimensions.

As well, the US demand for exchange rate stability has the potential to increase future volatility. Supposing that in the not too distant future, China hits the debt wall and the economy hard lands, which results in and a depreciation of the RMB beyond Beijing`s control. Would the US interpret such a development as a breach of the MOU, retaliate with trade sanctions, and exacerbate China’s downturn? Notwithstanding the catastrophic scenario of a hard landing, the Caixin editorial “The Unbearable Lightness of a Stable Yuan” raises some practical problems with a demand for exchange rate stability:

But there are two key structural sources of downward pressure on the yuan that will continue in 2019 and beyond. First, China’s economic growth will likely continue to slow, which may make investing in yuan-denominated assets less attractive. Second, the country may run its first full-year current account deficit in more than 25 years after its surplus plummeted in 2018. Large surpluses have meant there’s been a steady flow of capital into China, and have given the country a war chest of foreign-exchange reserves with which to support the yuan. The end of surpluses erodes this important backstop, and deficits mean net outflows, which will reduce demand for the yuan.

Under these conditions, a demand from the U.S. that China’s currency remains strong seems a big ask.

Meanwhile, back in the financial world, we have the contrast of two markets. Chinese stock indices surged on Monday between 5-6% on a combination of favorable trade news, and the news of the Politburo meeting confirming push for growth, and end of deleveraging. On the other hand, the SPX rose a mealy 0.1% on the news. Similarly, we saw China equity ETFs surge and decisively broke above resistance, while it has pulled back, current price levels remains above resistance turned support. By contrast, US-centric prices like soybeans failed at resistance and weakened.

Over the next couple of quarters, the Chinese and Asian outlook will be underpinned by another round of stimulus. The latest figures show that infrastructure investment went vertical in January. While the pace is not sustainable, Beijing is pulling out all stops once again to dress up growth ahead of the October celebration of Mao`s revolution

Investment implications

What does this mean for investors? The US market is at or near “peak good news”. The Fed has turned dovish, and news of the upcoming trade deal has taken off the tail-risk of a full-blown trade war. What other good news could lie ahead?

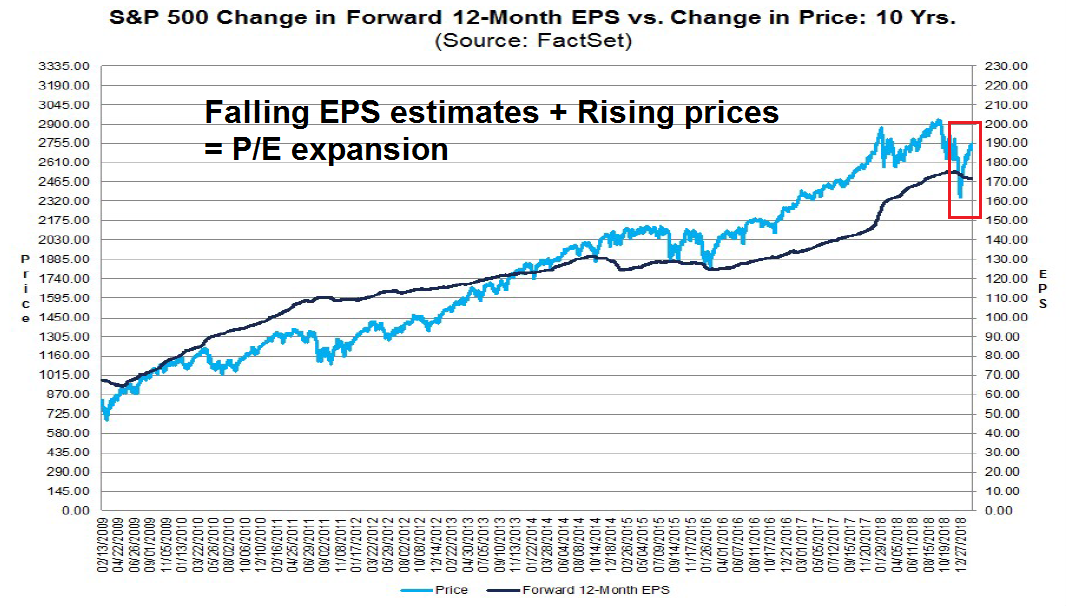

I have pointed out before that the stock market rally off the December lows was accompanied by declining EPS estimates, which translates into P/E expansion.

But the market is no longer cheap based on a forward P/E ratio, but roughly fairly valued. This makes US equity prices vulnerable to a setback on bad news, now that most of the good news is out.

From a technical perspective, this analysis from Chris Verrone of Strategas tells a similar story. Small cap price momentum has been powerful, and such episodes are typical characteristics of strong rallies off market bottoms. While this kind of market action is bullish longer term, short-term setbacks are very common.

At a minimum, US stocks are likely to underperform over the next few months. Relative to the MSCI All-Country World Index (ACWI), US equities are rolling over, while non-US equities are bottoming and turning up.

My inner trader remains short the US market.

Disclosure: Long SPXU

Hope you get well soon Cam!

One could argue that the bottoming of Euro stocks is due to looser money policies globally, end of QT and relative to the US, depressed prices.

America needs to up its game, to compete with China. This is proving more difficult than loose talk. A MOU, is just that, not a treaty.

Euro treaties are artifacts of history compared to today’s geopolitics. A flawed currency union, the final chapter on the Euro Union is yet to be written, IMHO.

Wish you speedy recovery.

Cam, get well soon. I was also uder attack of some viruses so I know well what is going on. 🙂

Thank you for your great work.