Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Model is an asset allocation model which applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. In essence, it seeks to answer the question, “Is the trend in the global economy expansion (bullish) or contraction (bearish)?”

My inner trader uses the trading component of the Trend Model to look for changes in direction of the main Trend Model signal. A bullish Trend Model signal that gets less bullish is a trading “sell” signal. Conversely, a bearish Trend Model signal that gets less bearish is a trading “buy” signal. The history of actual out-of-sample (not backtested) signals of the trading model are shown by the arrows in the chart below. Past trading of the trading model has shown turnover rates of about 200% per month.

The latest signals of each model are as follows:

- Ultimate market timing model: Buy equities

- Trend Model signal: Risk-on

- Trading model: Bullish

Update schedule: I generally update model readings on my site on weekends and tweet any changes during the week at @humblestudent. Subscribers will also receive email notices of any changes in my trading portfolio.

It’s all about the election

I have some terrible news to report. As a result of the change from Daylight Savings to Standard Time this weekend, the entire world will have to endure the US election for an extra hour.

All kidding aside, I could see the market anxiety rising all of last week. It wasn’t just the market action, which had taken on an increasingly risk-off tone as the week went on. It wasn’t the rising bearishness on social media. The biggest indicator of concerns over electoral uncertainty occurred when I saw that the traffic on my last post (see Trading the Trump Tantrum) was roughly triple the usual rate.

Despite some half-hearted rally attempts, the SPX ended the week testing its 200 day moving average (dma), and oversold on a number of key metrics. Traders are treating next week’s US election as the same kind of market moving event as the Brexit referendum. There is one key difference. The market was relatively sanguine going into the UK vote and expected a favorable outcome. By contrast, the market is positioning for a bearish outcome, even though the polls show that the bullish scenario, namely a Clinton win, as the more likelyt scenario.

Market analysis in the face of event risk involves answering the following questions:

- How would the market likely behave in the absence of tail-risk?

- How are market participants positioned ahead of the event?

- What are the likely bullish and bearish scenarios after the event?

Good news everywhere

If there had been no tail-risk, the markets would likely be responding with a risk-on tone as there has been good macro and fundamental news everywhere. Evidence of a growth surge is piling up.

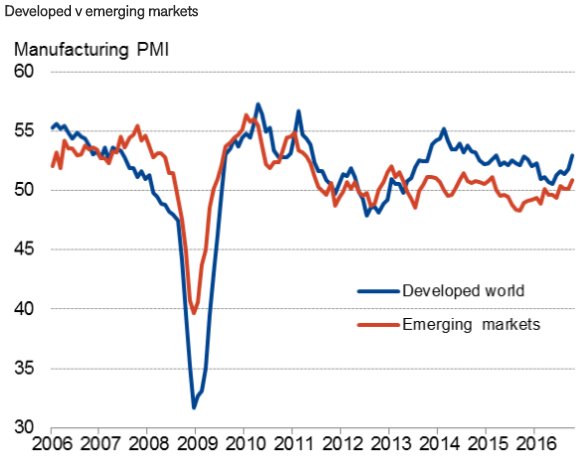

Even better, the growth revival is global in scope. Callum Thomas observed that we are seeing a synchronized upturn in global manufacturing in both the developed and emerging market economies.

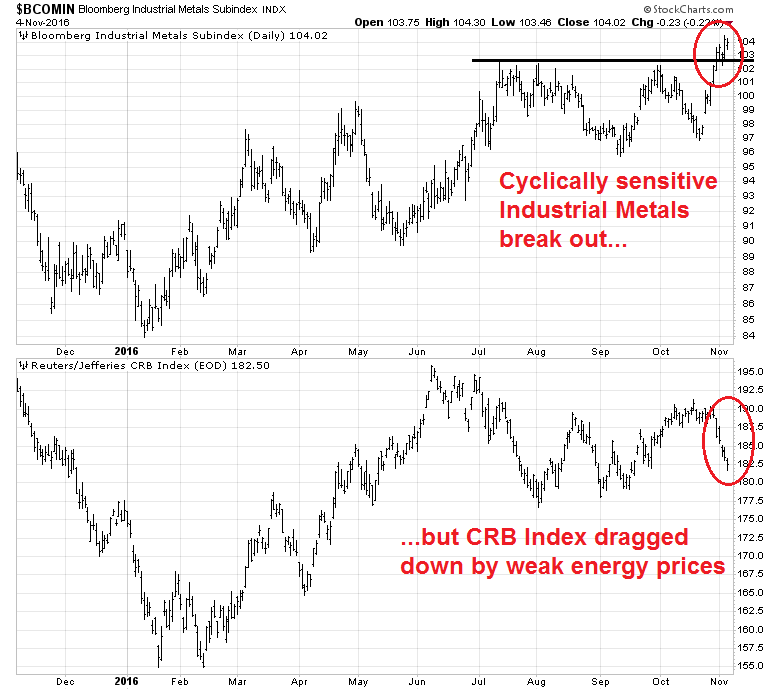

Another sign of the reflationary factors that I cited is the behavior of the cyclically sensitive industrial metals, which staged a breakout to new recovery highs. The broader CRB Index of commodities, however, was dragged down by weak energy prices due to uncertainties over OPEC actions.

Drilling down to the global reflation thesis by going around the world, Markit Economics pointed out that China PMI has surged to its best level since March 2013.

In addition, Bloomberg featured 9 charts showing why the Chinese economy is on fire:

- Chinese growth is firming as monetary conditions ease.

- Manufacturing PMIs are improving.

- Chinese industrial corporate profits are growing again.

- Macau gaming revenues, which is an indirect measure of the Chinese economy, is rebounding.

- Asian container throughput is rising.

- A firmer tone for the Australian Dollar, which is another market based indicator of the China’s “old economy” demand.

- Factory gate inflation is rising, indicating that China won’t be exporting deflation abroad

- The prices of iron ore and copper, which are also metrics of Chinese “old economy” demand, have steadied.

- The Li Keqiang Index, which measures electricity consumption, rail freight, and bank loans, has turned up again.

Does this represent an attempt by Beijing to artificially boost demand? Yes. Will it all end badly? Probably, but it won’t come crashing down on us today. Anyone who thinks that China is about to experience a hard landing will have to wait a bit longer.

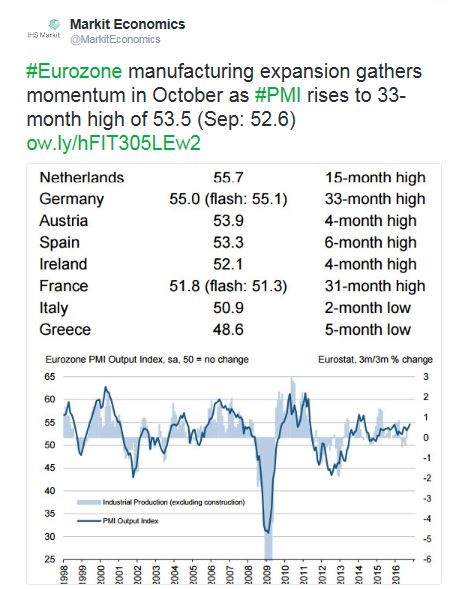

In Europe, Markit Economics showed that the eurozone also also enjoying a manufacturing revival.

In the UK, the political news turned a bit more market friendly. Theresa May’s Tory government suffered a constitutional setback when the High Court ruled that the prime minister could not rely on the “royal prerogative” to invoke Article 50 of the Lisbon Treaty to exit the EU. Any decision to leave must be done by an act of Parliament. While the court ruling will not end the Brexit process, it does create delay and uncertainty, especially when in light of past MPs intentions in the Brexit referendum, which amounted to about 70% in favor of Remain.

The May government has stated that it will appeal the High Court ruling. It does appear that the scenario I outlined before where Theresa May sabotages and discredits the Brexit process in order to call an election in the spring is coming to pass (see Silver linings in Europe’s political dark clouds).

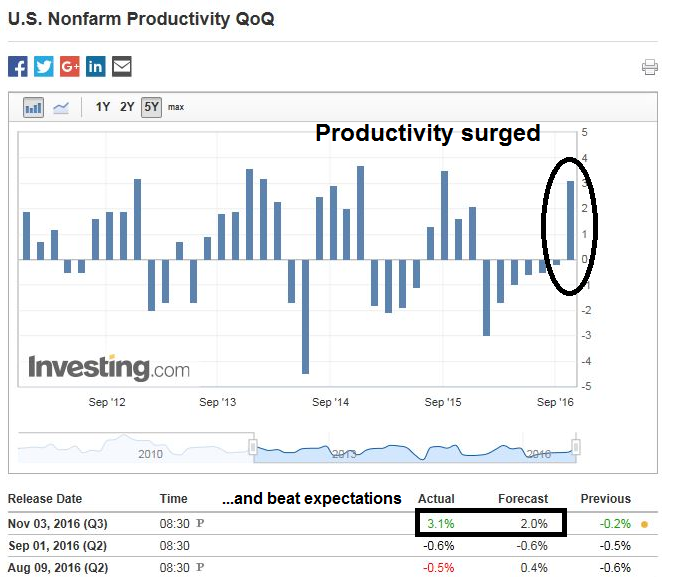

Across the Atlantic, the US economy continues to motor along. Productivity, which had been lagging, surged in Q3 and beat expectations.

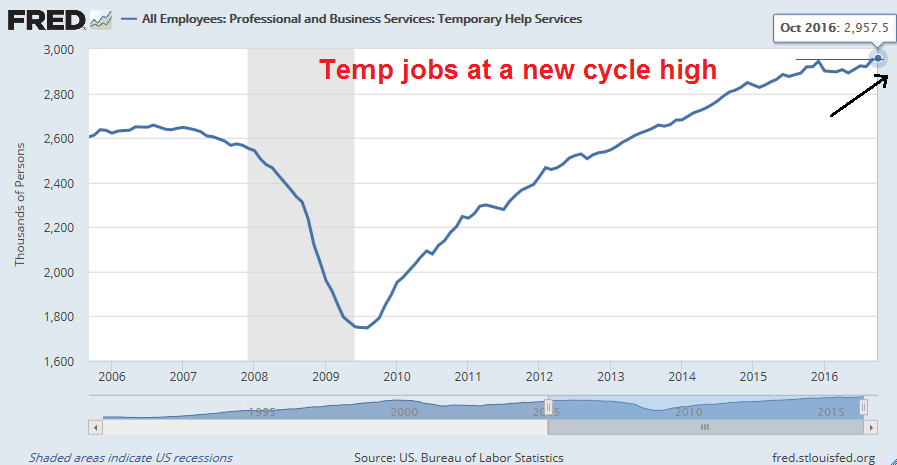

The headline Non-Farm Payroll figure in the October Jobs Report missed expectations, but August and September employment were revised upwards. Unemployment edged down to 4.9% from 5.0%. It was a solid report by most measures. More importantly, temporary employment rose to a cycle high in October. As temp jobs tend to lead full employment by a few months, this is a sign of a healthy job market and there is no sign of any slowdown in sight.

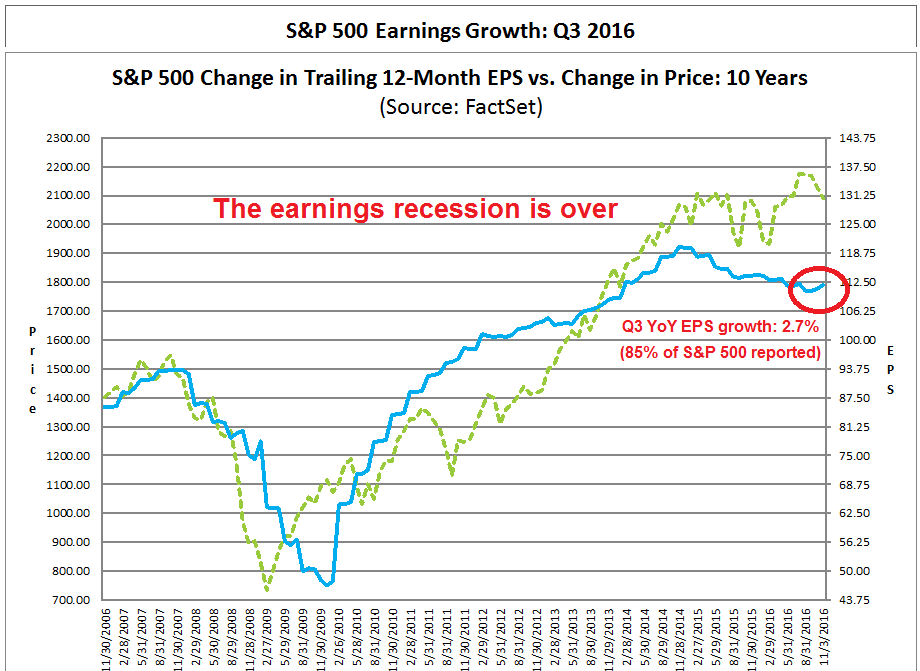

From a bottom-up perspective, optimism about earnings growth continues unabated. According to Factset, 85% of the index has reported earnings. The EPS beat rate is well above average and the sales beat rate is in line with the historical experience. Forward 12-month EPS continues to rise, which is reflective of improving expectations.

Q3 earnings season is nearly over as 85% of the index have reported. Blended actual and forecast Q3 EPS is up 2.7% YoY. We can finally declare an end to the earnings recession.

In conclusion, there has been no shortage of good news on the macro and fundamental front, which creates a bullish equity backdrop in the absence of event risk. In fact, Mark Hulbert reported that former Value Line research director Sam Eisenstadt, who is one of the few market timers with a consistent historical record, is forecasting an April SPX target of 2270-2310, which represents a solid 10% gain from current levels. His October 31 SPX target of 2220 last April was very close to its target.

Rising electoral fears

Despite these bullish tailwinds, risk appetite has taken on a decidedly bearish tone in the last couple of weeks as market participants have turned defensive ahead of the US election. Anecdotal evidence indicates that a pervasive atmosphere of fear. A discussion with a friend and market letter writer for advisers revealed that, while some advisers recognize the bullish factors that are building up, no one was willing to buy equities ahead of the election.

The negative sentiment among advisers can be seen from the weekly NAAIM survey, whose sentiment has fallen to the bottom of its Bollinger Band. In the past, such abrupt declines in NAAIM sentiment have shown themselves to have limited downside risk.

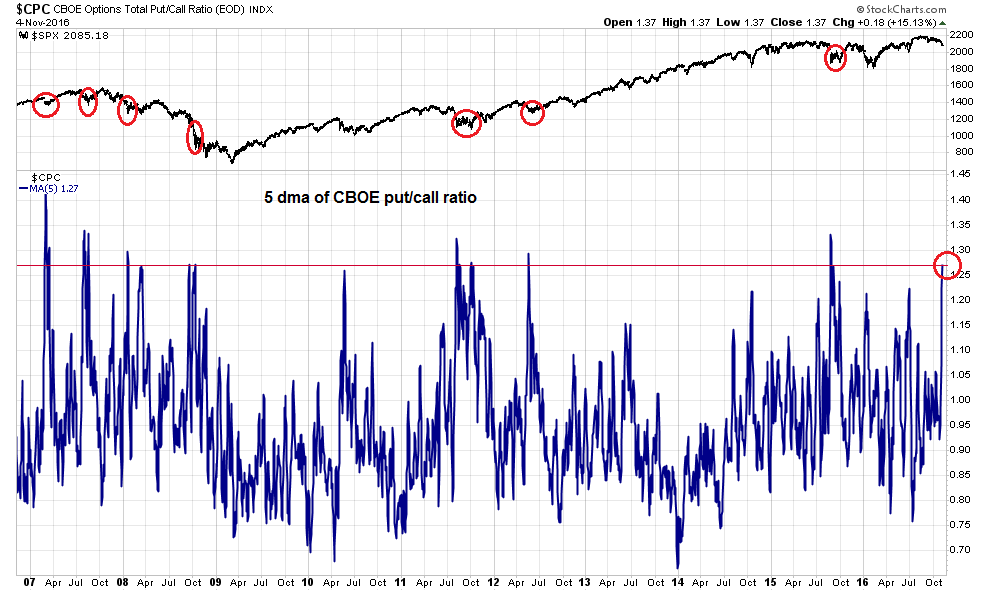

We can see the evidence of rising fear in other indicators. For example, indicators of fear can be found in the CBOE put/call ratio. The chart below shows the 5 dma of the put/call ratio, which is at levels roughly on par with the market crash of 2008.

If you knew where to look, the urgent need to hedge electoral risk is evident. The ratio of 9-day VIX to 1-month VIX has reached its fourth highest in its history. By comparison, the ratio of the 1-month to 3-month VIX (bottom panel) is high, but not as high by historical standards. The cost disparity between the 9-day VIX and other volatility indicators is reflective of the desire to hedge a short-term event, namely next week’s US election.

What happens next?

There is no question that fear is the dominant emotion and the market is oversold. But oversold markets can get more oversold. I have no crystal ball that can tell me the electoral outcome, but we can prepare for different eventualities.

Should Hillary Clinton win the White House, we will undoubtedly see a relief rally. Clinton is the status quo candidate and, in the absence of tail-risk, the growth outlook is bright. Stocks should rally from here.

One of the real-time market-based clues of the election odds can be found in the Mexican peso. As Trump’s popularity rose last week, the peso weakened. As the effects of the FBI inquiry started to wear off, the peso began to rally later in the week.

This is a seasonally positive period for stocks, but the positive seasonal effects the week before the election was nowhere to be seen (chart via Sean Emory, annotations are mine). The market pattern of the current electoral cycle may be reminiscent of the Reagan-Carter contest of 1980. Going into the election, Reagan and Carter were running neck and neck in the opinion polls, but Reagan was well ahead in the betting markets. Stock prices declined into the election and rallied after the results were known. Today, Clinton holds a narrow lead over Trump, and she is well ahead in the betting markets. Stock prices are weakening as the election approaches. Will history repeat itself?

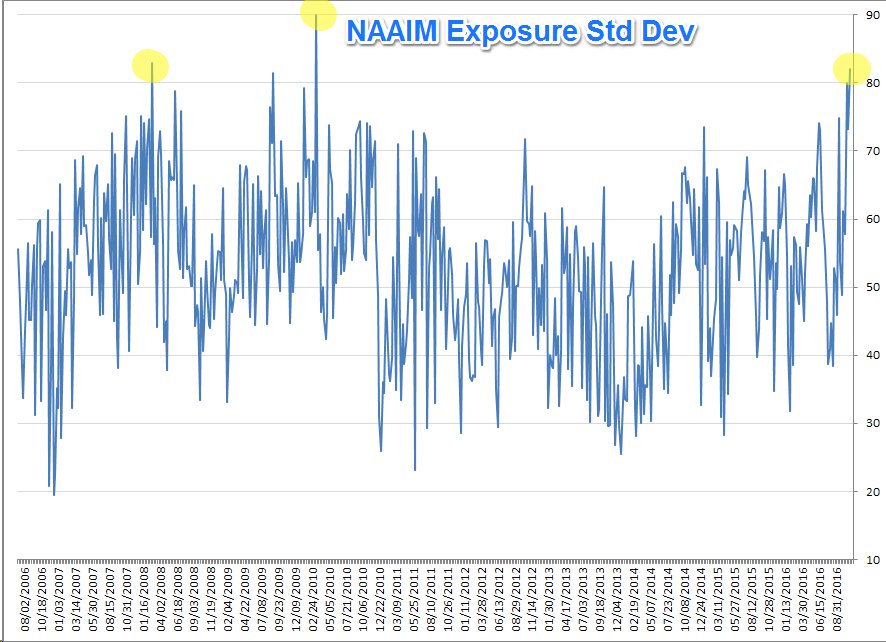

It will be an entirely different story should Donald Trump become president. The markets are already oversold and sentiment is showing a crowded short reading. But there could be even more selling as the uncertainty over the policies of a Trump administration. Even though NAAIM sentiment is already depressed, the dispersion of NAAIM votes is the third highest it has been in its own history. Not everyone has hedged for a bearish outcome. Traders should brace for more volatility regardless of who wins on Tuesday.

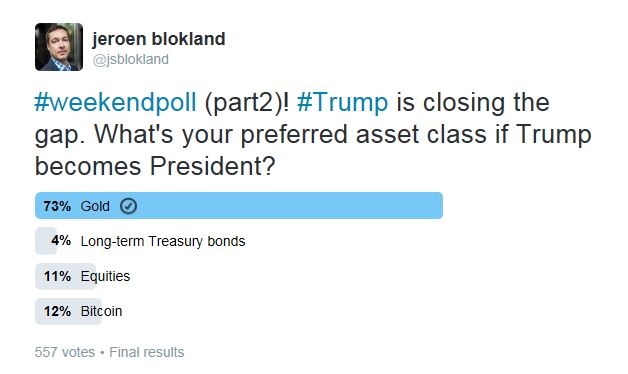

We can also see a similar unfinished business effect in the gold market. A recent (unscientific) poll showed that the asset class most likely to benefit from a Trump win is gold (also see my post The Trump Arbitrage trade).

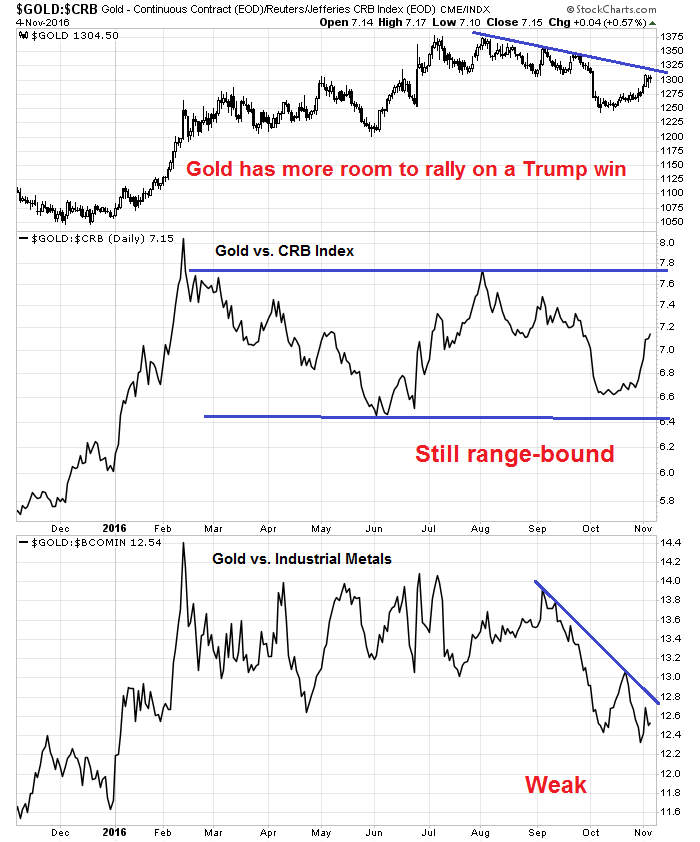

As the top panel of the chart below shows, gold prices haven’t been that strong despite Trump’s revival in the polls. It has yet to rally above its downtrend line. In addition, an examination of the relative strength of gold to the CRB Index and the cyclical sensitive industrial metals suggests that much of the strength in the yellow metal could be attributable to the global reflation effect on commodity prices. In the event of a Trump win, gold has much more upside potential.

Even though gold may soar and stock prices tank, don’t count on a new bear market starting for stocks should Trump prevail next week. On an longer term basis, overly bearish individual investor sentiment is likely to put a floor on any equity decline. This 20-year chart of the 52-week moving average of AAII Bulls – Bears shows that sentiment readings consistent with market bottoms, not stock markets that are within 5% of their all-time highs.

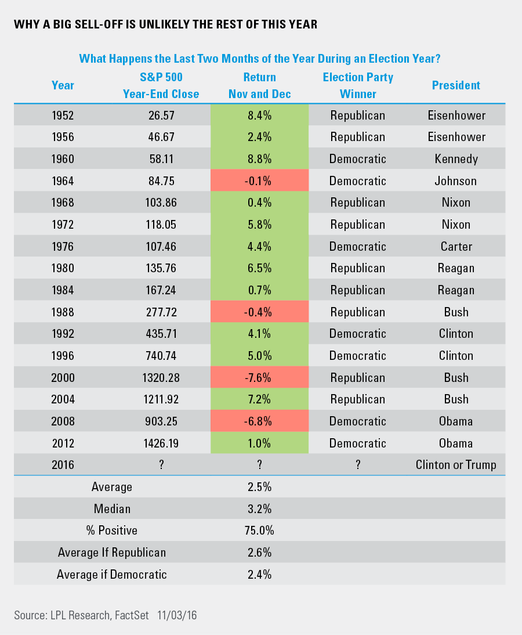

The most likely scenario under should Trump win on Tuesday is a short and sharp sell-off, followed by a bounce back. Ryan Detrick of LPL Research went back to 1952 and showed the historical pattern of market performance in the November and December after a presidential election. There were two instances where the market suffered significant losses. They occurred in 2000 after the bursting of the NASDAQ bubble and the hanging chad electoral uncertainty, and in 2008 because of the Lehman Crisis. Both of those periods marked the start of recessions.

Could a Trump win spark a recession? Notwithstanding his anti-trade and isolationist stance, Trump’s fiscal policy is likely to be highly expansionary and could actually be short-term bullish for the economy and the stock market (see Super Tuesday special: How President Trump could spark a market blow-off). Therefore a panic sell-off, followed by a V-shaped stock market recovery is the more likely scenario. Then be prepared for a period of choppiness and uncertainty as the new administration sorts out its priorities and reveals its policy initiatives.

For my readers who have misgivings over the prospect of a Trump presidency, let me say this. Italy survived the brash, outspoken and larger than life Silvio Berlusconi*. America can cope with Donald Trump as president.

* Berlusconi was once attacked on TV over the frequent stories of his womanizing, he quipped: “They did a poll of Italian women and asked, ‘Would you like to sleep with Silvio Berlusconi?’ 50% said yes. The other 50% said, ‘What, again?'” Donald Trump isn’t even in the same league.

Playing the odds

Looking ahead to next week, what should investors and traders do ahead of the election? In light of the anticipated volatility, it would be inappropriate for me to advise anyone as different people have different risk-reward preferences and pain thresholds.

However, as market participants have largely hedged themselves against and adverse event, namely a Trump win, and the political odds favor the equity market friendly event of a Clinton win, the high percentage play would be to take a measured long position in risky assets.

My inner investor remains constructive on stocks. My inner trader is still nervously long equities.

Some sensible advice

Whatever happens in the election, let me close with a piece of advice. Learn to view the results through a market-driven lens rather than an ideological one. Cullen Roche recently wrote:

A University of Chicago research paper recently found that 50% of Americans believe in conspiracy theories. I see it every day in financial circles. But how is this possible? How do the conspiracy theories about hyperinflation, crashing dollar, the unemployment rate, etc. persist when we have almost a decade of real-time data showing us that these theories and myths were totally and completely wrong?

This is crazy stuff. Especially when it comes to the economic data. Americans are distrustful of government data, but the USA has the most transparent and expansive government data sources of any government anywhere. I know because I’ve tried to compile economic data all over the world and no government comes close to the degree of transparency and sheer quantity of data. Is it perfect? Of course not. But it’s abundant and much of it is confirmed by private sources.

It would be too easy to get into an impotent rage should your favored candidate lose, or if policy doesn’t go in your desired direction. That kind of thinking clouds judgement and leads to subpar investment results.

Disclosure: Long SPXL, TNA

Cam. Can you comment on this? Is this a sign of the long-dreaded China hitting the wall?

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11743471

It’s hard to say what the significance of dropping FX reserves are. On one hand, if FX reserves are falling because they have gone to paying off foreign currency denominated debt, it would be neutral to slightly positive. On the other hand, capital flight does not say much about confidence about the Chinese economy.

For the time being, Chinese growth is reviving so they don’t seem to be hitting the wall just yet.

Hi Amy

I think this is a useful chart that provides guidance on China: where the Dalian Exchange iron ore futures traders are actually putting their money (up 20% since Oct 1st):

https://www.quandl.com/data/DCE/IF2017-Iron-Ore-Futures-January-2017-IF2017

Cheers, Donald

Donald,

Are you saying smart Chinese money is betting on commodities? Why iron ore?

The strength in iron ore and other industrial commodities is probably more reflective of physical demand and better Chinese growth outlook. If so, that begs the question: “If Chinese growth is so good, why should there be capital flight?”

Something doesn’t add up. Either the capital flight story is a red herring, or growth isn’t as good as it seems.

What if Chinese capital flight was just a way of balancing investment globally and among different asset classes and currencies? Multi-national real estate (residential and commercial), mines, metals, major infrastructure development, etc. Maybe all this is done with the half-blessing of the government, similarly to the way certain US immigration programs express what they call dual intent. In other words it’s a contradiction that works. If China fails, so much of their citizenry have investements elsewhere that they may be able to repatriate in a time of crisis.

This is always what I have suspected is the case. Is it possible?

Indeed…..apart from iron ore, coking coal is another interesting graph: https://staticseekingalpha.a.ssl.fastly.net/uploads/2016/11/13631982_14786149532816_rId26.png

At important market junctures it is always a good idea to run a few scenarios and then see how the stock market plays out. At the present time the stock market is at support – 200 day moving average. Cam is right that by any measure we should have a rally. However, I think it is a good idea to pay the devil’s advocate and ask was this decline caused by the Trump Tantrum or was it caused by some fundamental reason that we will only know after the fact. For example, the back up in interest rates. A stock market that declines 8 days in a row is by any measure not healthy. What I did was I also looked at the ETFs of different countries to see whether the decline was US specific or was it universal. U.K., Germany, Canada and Switzerland were some of the ones that were in serious trouble.

So what is my guide post? I am now going to watch the quality of the rally. Advancing stocks compared to declining stocks. Up Volume compared to Down Volume. Percentage follow through day etc.. If the rally has legs it should prove itself fairly soon. If not, it will release the short term oversold condition by rallying to about 2140 on the S&P 500 which would be the ideal point to establish shorts or to lighten the long portfolio. Also, I will be watching Bonds, Gold and the U.S. dollar for clues.

Agree 100%. The ES rally on the FBI news is indicative that the market was spooked by Trump.

Still, we need to watch the quality of the rally and, of course, who wins on Tuesday.

Hi Cam,

“The ES rally on the FBI news is indicative….”

What does ES stand for?

Thank you,

Mark

Hi Mark

ES is the globex product code (ticker) for SP500 electronic futures: http://www.cmegroup.com/trading/equity-index/us-index/e-mini-sandp500_contract_specifications.html

A few comments on China. (I live in hk). 1, capital flight is real, and worrisome. but when we look at this issue, we are comparing the with the old EM crises. there is one step in between that’s currently missing. ie, credit + interest cost going up. that’s what drove the old EM crises, which usually is a result of capital flight. that’s not the case yet in China, due to govt visible hands in various ways. so watch the interest and credit market. 2, iron ore. that’s largely due to the supply side reform (which I think was done with the right intension but poor execution), China economy is doing fine due to renewed property market boom and fixed investment uptick, both of which are govt driven.

Cam,

When your inner trader gets long and the market moves against you nine days in a row but you remain bullish, how do you manage the position? Do you add, reduce or just keep the same exposure?

Mitch

That’s difficult to answer without discussing the level of commitment I have to the long side. While I reveal WHAT I buy and sell in these pages as a disclosure of possible conflicts, I don’t reveal HOW MUCH I buy and sell because my risk/reward preferences are different from yours. I know nothing about you: your return objectives, your risk preferences, your tax situation, or even what tax jurisdiction you live in.

Having said that, let me try and answer your question in a general way. If a trade goes against me, my reaction is a function of the model readings and how quickly the market got overbought (if I am short) or oversold (if I am long). It is also a function of how much risk I have taken in my position (how long or short I got).

In this case, the market got oversold relatively quickly and the decline was relatively shallow, even though the S&P 500 fell for 9 consecutive days. Under those circumstances, I made an assessment of the risk-reward (oversold, positive fundamentals, high tail-risk). I would have been prepared to add to my long positions to achieve the level of risk I was prepared to bear, had the rally not occurred on Monday.

Each situation is different. I calibrate my position to my assessment of my personal risk-reward ratio. That’s why I don’t disclose whether I add or subtract from positions, unless the position goes to zero. Your risk tolerance is different from mine.

Otherwise, I would be managing a fund with all the proper disclosures about how much risk the fund would be taking. In that case, it would be up to you to decide whether such a fund would be appropriate for you.