After I wrote my last post about the GAAP gap, which addressed many of the concerns about shortfalls in earnings quality (see The GAAP gap as Rorschbach test), I had a number of discussions about the vulnerability of the stock market to buyback activity. I had been meaning to write more on this topic, but Cullen Roche and Ben Carlson both beat me to it with some balanced perspectives on fundamentals behind buybacks. Nevertheless, here is my two-cents on the topic.

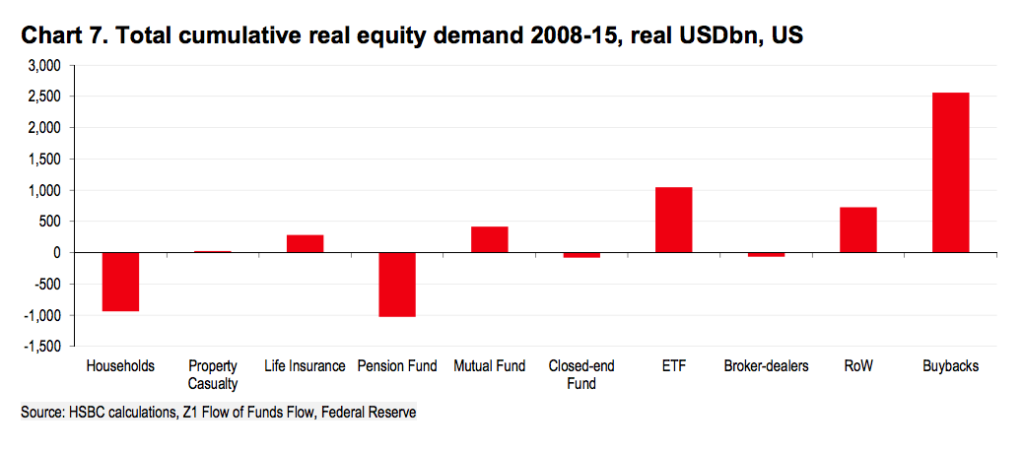

The concerns about buybacks gained prominence from a post from Josh Brown, who highlighted analysts from HSBC showing that buybacks accounted for much of the equity demand since 2008. As the market enters a buyback blackout period during Earnings Season, could the stock prices weaken as this key demand slackens?

Despite the above chart, the relationship between buybacks and equity returns is tenuous at best. Let me explain why.

Why do companies purchase their own shares?

Let’s start at the beginning. Why do companies buy their own shares. Share buybacks can be thought of as a return of capital to shareholders. Companies can do return capital by way of buybacks, or dividends.

The cash for dividends and buybacks either come from the excess cash flow generated from operations, or debt. But isn’t borrowing to pay dividends or buy back stock a bad thing to do?

Not necessarily. Interest expense on debt is tax deductible, while dividends and share buybacks are financed with after-tax dollars. With interest rates so low, is it any surprise that corporate management are putting debt on the balance sheet in order to maximize shareholder returns? As a sign of the times, Ireland sold a 100-year bond at an astounding yield of 2.35% last week (via Bloomberg). In February, Apple took advantage of the low rate environment and sold a 30-year bond at a yield of 2.05% in order to “return capital to shareholders” (via Bloomberg).

Doesn’t all this increased debt represent a ticking time bomb? Eric Bush at Gavekal pointed out that corporate leverage doesn’t seem that excessive compared to past history. Sure, debt levels are elevated, but they are below historical norms.

Buybacks vs. dividends

The issue of how companies return capital to shareholders deserve some mention. To be sure, buybacks are more attractive for management as they tend to boost the stock price and there are numerous option-based incentives compensation schemes around. So are buybacks a better or worst way to return capital to shareholders?

In a subsequent post to the one above highlighting the influence of buybacks, Josh Brown referenced a paper by Michael Mauboussin studying the issue. Brown concluded:

Probably the best way to think about dividends vs buybacks is not to think of them as facing off against each other, but as working in concert to return capital to shareholders when there is no better use for it. Meb Faber calls this combination “shareholder yield”. But still, it’s also worth thinking about buybacks as being market-following and mercurial, versus dividends as being steadier and, often times, more responsible.

Despite Mauboussin`s assertions, the historical record is unclear whether a tilt towards buybacks or dividends yield useful market signals. The chart below shows the relative returns of the high backback ETF (PKW) against the high yield ETF (DVY). The market has undergone several regime changes in the nine-year history of this pair. High buyback stocks have beaten high yielding stocks for most of this period, but they have also undergone prolonged periods of range-bound relative performance.

Moreover, the relative returns of this pair does not seem to have a strong relationship to stock market direction. We have seen several periods where the PKW-DVY pair show a high correlation to SPX returns and other periods where the correlation was minimal. Changes in correlations regimes does not appear to be related to market direction.

For a different perspective, Ben Carlson at A Wealth of Common Sense framed the buyback vs. dividend narrative this way:

The problem with the buyback story is that the narrative would be totally different if all of that money was being used as dividends. We would be seeing headlines about how mom and pop are propping up the market by re-investing their dividends back into their mutual funds. In the grand scheme of things buybacks and dividends are basically identical to the end investor (see Stock Buybacks Demystified).

Spot the pattern

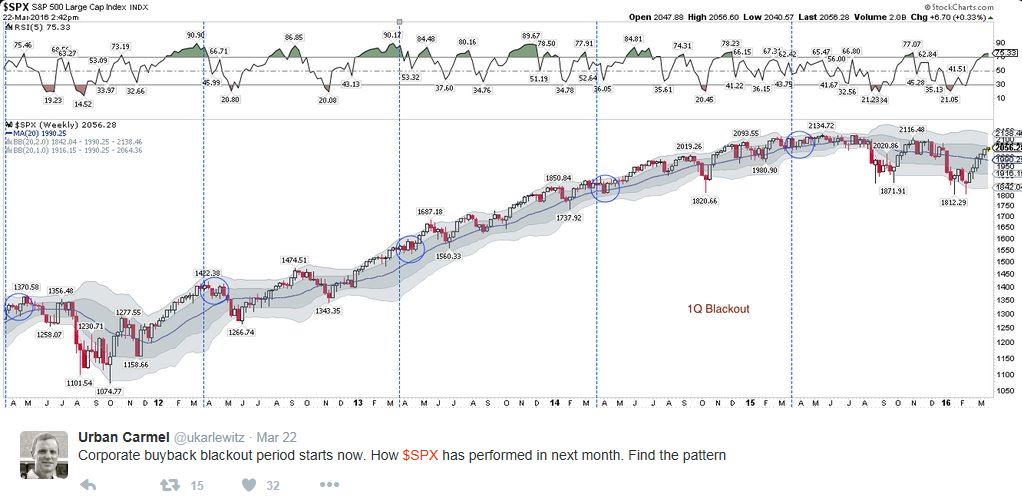

As for the fears that the upcoming buyback blackout period could depress stock prices, Urban Carmel recently showed the SPX returns (circled) during 1Q Earnings Season blackout periods. Do you see a pattern? (Remember we are analyzing market behavior during the circled periods, not before or after).

Here is the same chart for the 2Q Earnings Season blackouts. Spot the pattern for me.

Now, stop reading Zero Hedge and tell me again: Why are you worried about buybacks depressing stock returns?

I guess banks earning and balance sheet got more concern as DB share price & CDS are showing signs of weakness that keeps me worry on this rally.

In the past underperformance of banks was a key reason to worry about the general market. But that was when the Central Bankers caused recessions on a regular cyclical basis and all industry groups went up and down more or less together. But now we are in a Moonless world (Central Bankers being the Moon causing tides) where industry sectors have their own rhythm and there are no general recessions.

This new world caused confusion with the energy sector when its technology revolution cause a surge in supply and hence lower prices. Demand kept rising even as prices plunged. In the past, plunging prices ala 2008-9 were caused by recessions so investors kept trying to find a recession which wasn’t there. Unfounded worries about the general stock market.

I believe this is what will happen with banking too. Bank stocks are not going down because the general economy is bad, it’s because of their own dynamics. Fintech is eating into their business and forward looking investors are repricing future prospects. Mobile phone technology is making banking a commodity product not the warm and fuzzy client/banker personal relationship. Banks have huge legacy buildings and systems that will hamper their ability to compete with nimble new competitors. Also, think about the tens of billions in fines the banks have paid for past practices. Why the large payments, because those practices were very, very profitable. They don’t do those profitable shady things any more. So profit margins will not go back to the heady days. Banks are morphing into a utility type businesses that are under attack by a swarm of digital technology piranha fish taking bites.

So there will be another bout of confusion among veteran investors whose experience tells them when banks are doing badly, the stock market is at big risk. Just like the oil industry scare, the risk is to the banking industry not the general economy or other industry sectors.

Thanks Ken.