China’s malaise explained

To the outside casual observer, the most immediate and visible part of China’s problem is cratering stock prices. But her difficulties didn’t just appear overnight. It was the product of decades of misallocation of capital in two sectors. The first was infrastructure, which was initially productive but eventually became overbuilt. The second was the export sector, whose competitiveness was subsidized by the household sector of the economy.

The credit-driven infrastructure building initiative set off a stampede of residential construction and a property bubble. Eventually, infrastructure became overbuilt and the property bubble collapsed. China Evergrande, which was once the world’s largest property developer, is now bankrupt and undergoing liquidation. A more serious threat to social stability appeared when over-levered developers were unable to complete and deliver apartments that were bought and paid for by individuals.

The collapse in property can be resolved with a deflationary spiral, not only for consumer prices, but in producer inputs as well. Bloomberg reported that pork prices are falling ahead of the Lunar New Year. As Chinese consumption of pork tends to spike during such festivals, weakness in pork demand and prices is an informal signal of a consumer slump.

The one bright spot in the economy is exports. China’s manufacturing trade surplus has been strengthening since the onset of COVID-19, but the strength in manufacturing is supported by the export of deflationary pressures to China’s trading partners.

An SCMP article reported that wage growth has been weak. “Average monthly salaries in 38 major Chinese cities dropped by 1.3 per cent in the fourth quarter of 2023”. With the combination of weak wage growth, which reduced household income, and the weakness in the property sector, which hit household balance sheets, is it any wonder why consumer spending is so weak?

The policy response

In response to the latest stock market rout, Beijing has implemented a series of measures aimed at stabilizing stock prices, including banning short selling, the deployment of SOE’s offshore USD reserves to buy stocks, and the termination of the securities regulator.

China’s well-rehearsed industrial policy can be staggeringly wasteful but still produce stunning results. This same pattern of fattening up companies with subsidies and protection and then cutting support and introducing market discipline to weed out the weak has already produced domestic and export juggernauts in steel, shipbuilding and solar panels.

The market’s response

By now, it should be increasingly evident that the Chinese economy is becoming more state directed and subject to the uncertainty of regulatory policy. I believe Chinese stocks are at best trading vehicles and not investment vehicles. Nevertheless, investors can participate in Chinese growth by investing in the stock markets of China’s Asian trading partners, which are all in flat or falling relative downtrends.

Investors can also find some clues to the state of China’s cycle by analyzing sector relative returns. China has been a voracious consumer of global commodities and commodity prices can give some clues to her economic strength. Commodity prices have been flat to down over the past few months. More importantly, the cyclically sensitive copper/gold and base metals/gold ratios have been trading sideways. These chart patterns could be constructively interpreted as stabilization and not the sign of a growth deceleration.

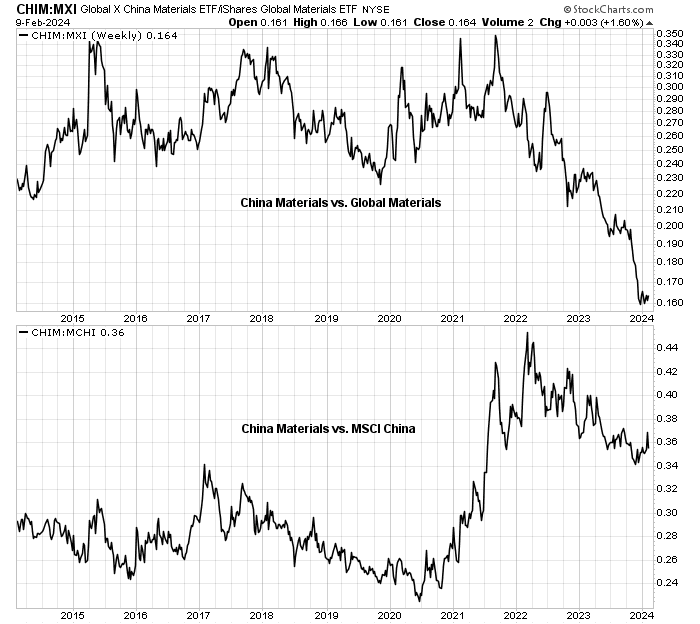

However, the relative performance of Chinese material stocks to global materials is more concerning. Chinese materials have been extremely weak against their global counterparts (top panel) and they have also been weak against the Chinese market. This is a signal of more cyclical weakness in infrastructure spending.

Even though the macro backdrop for China is weak and investors should wait for signs of a turn before committing funds to Asian equities, I offer the following two tactical trading signals for the Chinese stock market.

Jeffrey Hirsch offered the seasonal observation that Chinese and Hong Kong stocks perform well around the time of the Lunar New Year.

In conclusion, I reiterate my view that long-term investors in China are likely to face subpar returns coupled with high volatility, with the added view that the Chinese equity market can be a useful trading vehicle. China hasn’t addressed even trying to reverse the imbalances from long-standing past economic policies. However, investors can gain exposure to Chinese growth through the equity markets of China’s major Asian trading partners. Real-time market signals indicate further weakness in China, which investors should avoid. In the short run, the Chinese stock market looks washed out and traders may be able to profit from a tactical rebound over the next month or two.

About 15 years ago I had invested in a Chinese ADR that traded on the NYSE. The stock blew up on me because of accounting irregularities (read fraud). Since that time I have never invested in developing countries. India has had it shares of problems. The latest – The Adani Group.

I guess investing investing in an index will mitigate that issue.

On second thought that problem is not to limited to overseas markets. We have had our shares of scandals with Enron, Bernie Madoff etc.. Caveat Emptor should be the common denominator.

Is China cheap? Market cap of Nvidia is now more than the total Hong Kong H share market.

Cheap or not, you can go back thru Chinese history and get a feel of Chinese culture. One can safely say that deceit is now a substantial part of Chinese culture. It is a byproduct of trying to survive in that land for such a long time. Juxtaposed with Japanese culture it is even more striking. I am not here to denigrate China. I just report what I see and understand. One part of my ancestry is Chinese. It is almost like an intuition when I saw things going on in China that I don’t even need detailed analysis to figure it out.

In a system where there is a culture of an impartial bureaucracy, trust tends to be higher and trust in institutions is high. Call that the “Western norm”.

In a system where there isn’t such a culture, trust tends to be based on family and long-standing relationships. You see that more in many parts of Asia and southern Europe.