Mid-week market update: I know that this is a trite expression, but the easy money has been made.

The rally off the October bottom has been astounding. My trading model was fortunate enough to spot the exact day of the bottom when insiders started buying an oversold market. The rally enjoyed further tailwinds in the form of a rare Zweig Breadth Thrust buy signal. The trading model took a brief hiatus in November and re-entered on the long side. It took profits when the S&P 500 violated its 10 dma.

The rally off the October bottom was driven by falling Treasury yields, which also violated its 10 dma. While my inner investor remains equity bullish, my inner trader is far more cautious.

Short-term caution

I am seeing numerous indicators of long-term bullishness, but warnings of a short-term consolidation or pullback. The percentage of S&P 500 stocks above their 50 dma recently surged above 90%. This is a powerful signal of price momentum and usually resolved with higher prices 6-12 months later. However, such overbought conditions have also led to short-term pullbacks.

Another warning of near-term weakness comes from % bullish on point and figure indicator, which reached an overbought condition of 80% and pulled back. If history is any guide, investors can expect corrective action over the next few weeks.

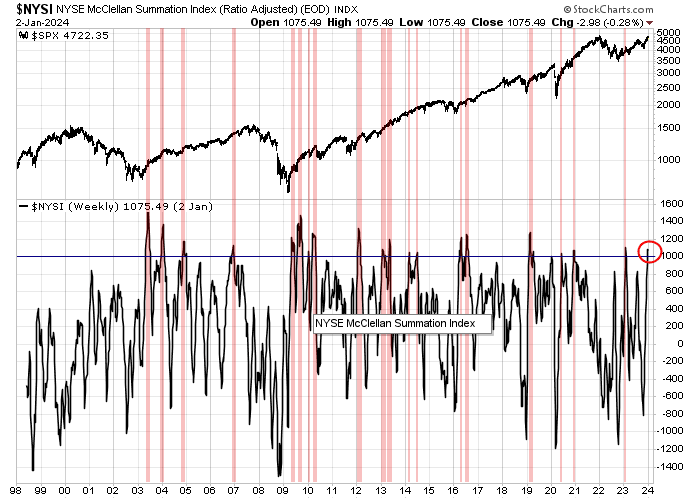

The NYSE McClellan Summation Index (NYSI) also provides a similar view of current market conditions. NYSI recently rose above 1000, which has usually been an indicator of a strong bull market. However, such overbought readings have often resolved in short-term pullbacks.

A decelerating economy

From a top-down macro perspective, job openings from JOLTS edged down in November, which is a welcome sign of a cooling jobs market that opens the door to lower interest rates. Historically, job openings have led nonfarm payroll employment by about six months and current readings indicator further deceleration in NFP growth.

In addition, there were no big surprises in the FOMC minutes, though their release did spark a bond market rally. The Fed is pivoting to lowering rates, though the timing of the cuts is uncertain.

In discussing the policy outlook, participants viewed the policy rate as likely at or near its peak for this tightening cycle, though they noted that the actual policy path will depend on how the economy evolves.

Though the inflation fight isn’t over:

Participants generally stressed the importance of maintaining a careful and data-dependent approach to making monetary policy decisions and reaffirmed that it would be appropriate for policy to remain at a restrictive stance for some time until inflation was clearly moving down sustainably toward the Committee’s objective.

My inner investor is bullishly positioned. Subscribers received an alert on Tuesday that my inner trader had taken profits in his long S&P 500 positions and he is standing aside in anticipation of near-term market volatility.

One of the best trading calls-almost the bottom to almost the recent top.

Great calls, Cam.

Happy New Year to you and everyone here!