An equity rally ahead?

While stocks did briefly advance this week, the S&P 500 was sideswiped by disappointments over the earnings results from META and GOOGL, though MSFT beat and was rewarded with a positive reaction. This kind of volatility is to be expected during earnings season. Even though the market is probing its recent lows, it’s exhibiting a series of positive RSI divergences, which is constructive. The likely peak in the 10-year yield will also provide a tailwind for stock prices.

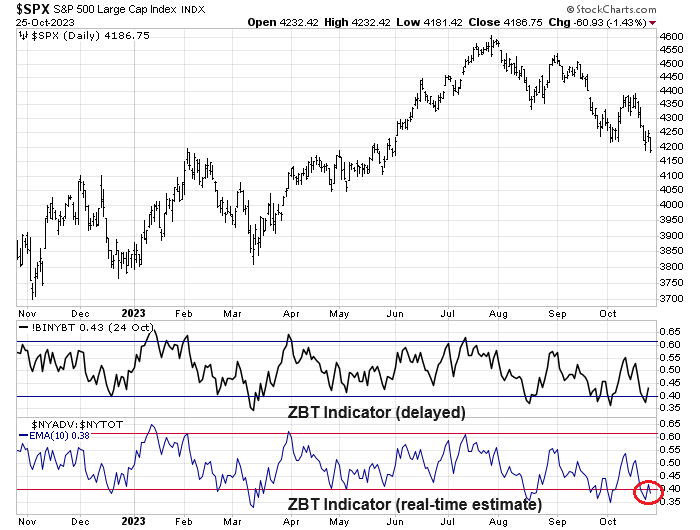

In addition, the stock market is very stretched to the downside, as evidenced by oversold condition shown by the Zweig Breadth Thrust Indicator.

Nevertheless, this market makes me uneasy about being overly bullish.

Not scared enough

Even though the stars appear for a relief rally and possibly a rally into year-end, which is my base case, I am approaching this market with some caution. Although bond market sentiment reached a crowded short level and bond prices were ready to rally, equity market sentiment looks too bullish. As the S&P 500 tests the 4200 level, the put/call ratio hasn’t spiked, indicating complacency.

Helene Meisler conducted an (unscientific) Twitter/X poll on the weekend and found that most respondents are expecting a year-end rally. In other words, equity sentiment hasn’t capitulated yet.

This leaves us with an oversold market ready to bounce, but the risk is any bounce could be very brief. We may need a final flush before the market can rally into year-end.