Preface: Explaining our market timing models

We maintain several market timing models, each with differing time horizons. The “Ultimate Market Timing Model” is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Asset Allocation Model is an asset allocation model that applies trend following principles based on the inputs of global stock and commodity prices. This model has a shorter time horizon and tends to turn over about 4-6 times a year. The performance and full details of a model portfolio based on the out-of-sample signals of the Trend Model can be found here.

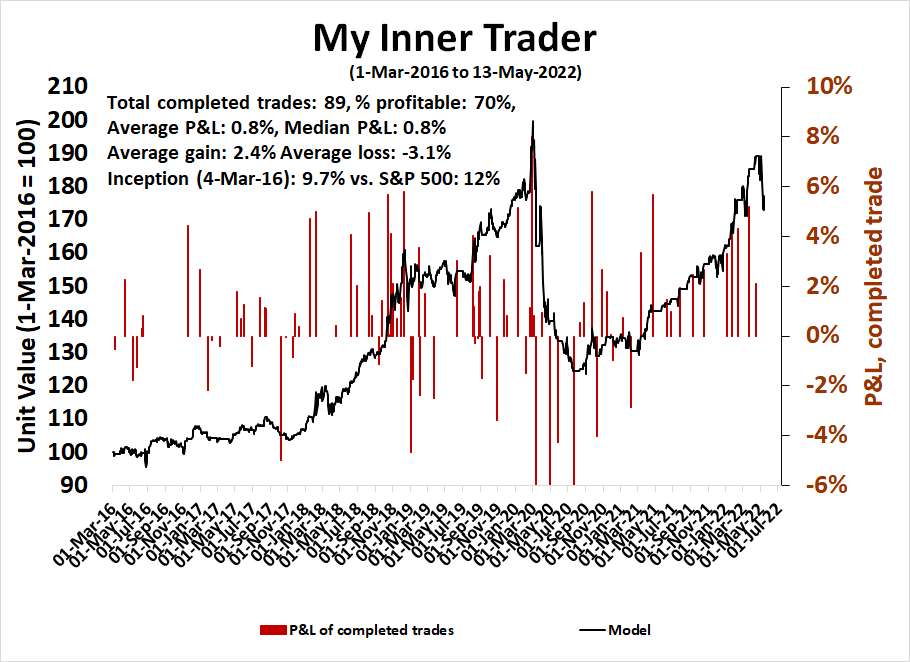

My inner trader uses a trading model, which is a blend of price momentum (is the Trend Model becoming more bullish, or bearish?) and overbought/oversold extremes (don’t buy if the trend is overbought, and vice versa). Subscribers receive real-time alerts of model changes, and a hypothetical trading record of the email alerts is updated weekly here. The hypothetical trading record of the trading model of the real-time alerts that began in March 2016 is shown below.

The latest signals of each model are as follows:

- Ultimate market timing model: Sell equities

- Trend Model signal: Bearish

- Trading model: Bullish

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers receive real-time alerts of trading model changes, and a hypothetical trading record of those email alerts is shown here.

Subscribers can access the latest signal in real-time here.

A crypto bank run

I had voiced my reservations about the cryptocurrency ecosystem in the past (see The brewing Lehman Crisis in Crypto-Land) and the risks manifested themselves in the last week. To briefly recap the problem, cryptocurrencies are mainly traded in the offshore market. A crypto trader can exchange USD for crypto, but banks do not allow direct access to crypto exchanges, with some exceptions. The crypto trader can exchange his USD for a stablecoin, which is a token that is theoretically backed 1 for 1 to the USD. He then exchanges his stablecoin to buy cryptocurrencies and back when he sells. When he wants USD in his account, he instructs the stablecoin provider to convert his stablecoin into USD, which is deposited to his onshore USD account.

The important piece of the crypto ecosystem plumbing is confidence in the stablecoin system. Stablecoins are supposed to be like money market funds, they shouldn’t be trading below par. Last week, the TerraUSD stablecoin, also known as UST, broke its USD peg and sparked a crisis of confidence. Within the space of a few days, the value of LUNA had evaporated to zero. Crypto traders began a virtual bank run on stablecoins. Tether, the largest stablecoin, broke its peg last week, While prices have partly recovered and stabilized, Tether is still trading slightly below 1.

The crypto bank run set off a stampede of selling in cryptocurrencies and other speculative risk assets.

The big question for investors is whether the crypto meltdown will have a long-lasting effect on global risk appetite and risk aversion leak into the equity market. Was the Crypto meltdown last week the new LTCM moment for asset markets?

Tightening until something breaks?

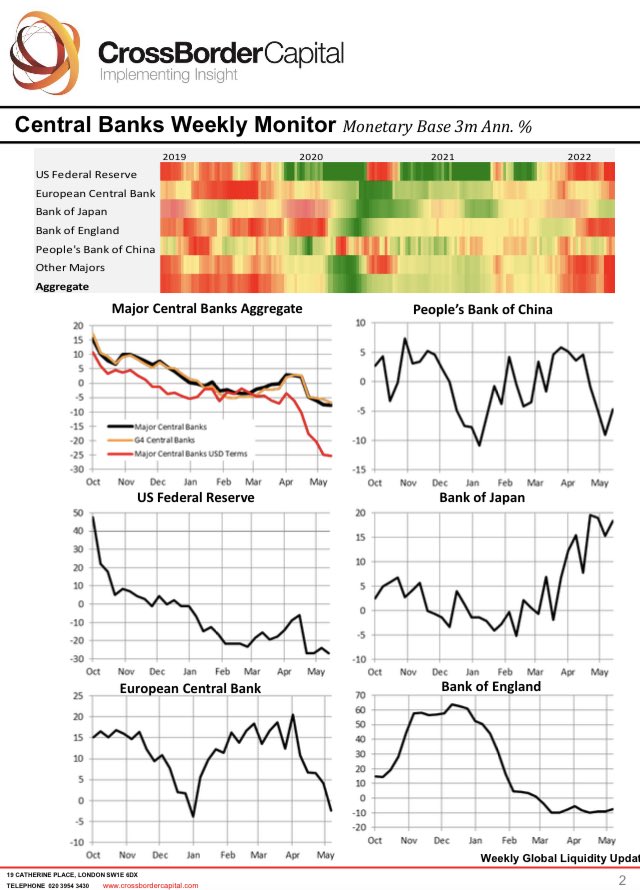

One way to explain the crypto crash is the tightening of financial conditions because of central bank monetary policy. Cross Border Capital has documented the collapse in global liquidity, which would have been even worse without the BoJ.

The retreat in crypto values can be attributable to the financial system wringing out some of the speculative excesses from the last boom. Simply put, crypto assets went up a lot and they’re now retracing their gains.

In the past, the Fed has halted its tightening policy when something breaks, such as the Russia Crisis which sank LTCM. Does this mean that the Fed will come to the rescue of crypto investors? Probably not. Remember the underlying reasoning behind cryptocurrencies is they exist outside the fiat currency system. If you crash, you’re on your own, unless the crash threatens the fiat banking system. The Fed won’t act unless credit spreads blow out, which hasn’t happened. Financial conditions have tightened, though not a lot by historical standards.

Nevertheless, the high level of correlation between cryptocurrencies and the relative performance of speculative growth stocks, as exemplified by ARKK, is a measure of risk appetite. Last week’s stabilization of ARKK on high volume is a constructive sign for short-term risk appetite. The worst of the crash may be behind us.

Waiting for capitulation

Still, market analysts have voiced concerns about a lack of capitulation in the market. While technical internals are oversold, the signs of panic and capitulation that mark tradable bottoms have not been present.

The term structure of the VIX at the 1-month and 3-month level hasn’t inverted, indicating fear.

As well, some analysts observed that ARKK was seeing substantial inflows even as the ETF tanked. However, Jason Goepfert pointed out that ARKK experienced a surge in short sales and the inflows could be explained by unit creation to accommodate short sellers.

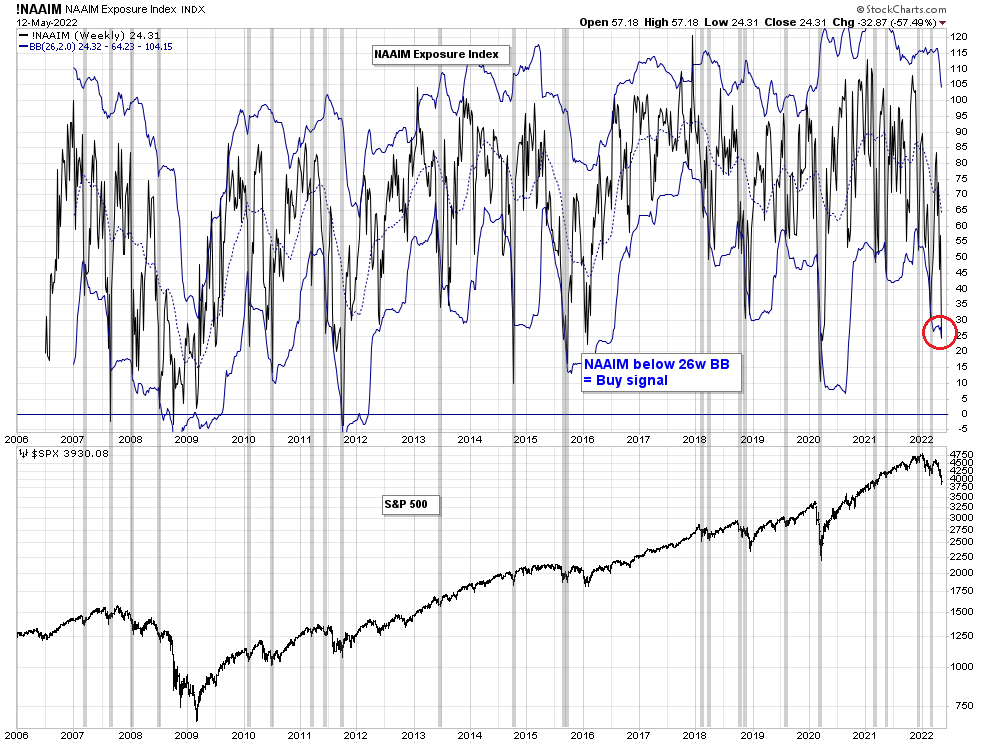

Here’s a sign of capitulation. The NAAIM Exposure Index, which measures the sentiment of RIAs managing individual investor funds, fell below its 26-week Bollinger Band last week. Historically, this has been a buy signal with an excellent track record with strongly bullish risk/reward implications.

SentimenTrader also pointed out that Lipper also reported that investors redeemed $44 billion from equity funds and $39 billion from bond funds in the last six weeks. This is a very unusual condition that only happened four times in the last 20 years, usually at stock market panic bottoms.

An oversold market

The stock market is oversold by a variety of indicators. One of the most effective trading signals is the Zweig Breadth Thrust Indicator, which has a strong record of marking short-term bottoms in the last five years. Friday’s rebound starts the clock at day 1. The market has 10 trading days to reach an overbought condition for a ZBT buy signal, but don’t hold your breath.

Jonathan Harrier observed that the S&P 500 was down six weeks in a row. There have only been 20 such events since 1950 and the market made it to a seventh consecutive decline on only five occasions. These instances of bearish market action appear exhaustive and they have historically resolved bullishly.

I highlighted the S&P 500 head and shoulders breakdown last week. The pattern showed a measured downside target of about 3830, which is roughly the same region as the Fibonacci retracement level of about 3800. As the 3800-3830 zone is well known to chart watchers, in all likelihood the index will either never reach there or blow past those levels in a downdraft.

Friday’s strong market rebound represents a hopeful sign for the bulls. The NYSE McClellan Oscillator flashed a buy signal by recycling from an oversold condition, with past buy signals of the last two years shown as vertical lines on the chart.

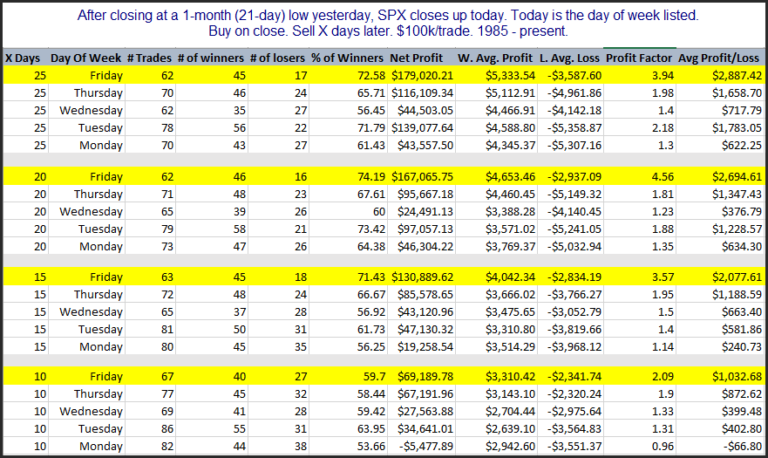

As well, Rob Hanna at Quantfiable Edges found that Friday rebounds after a 21-day low tend to be far more sustainable over multiple timeframes compared to turnarounds on other weekdays.

In the short run, the VIX Index will have to violate the rising trend line for the bulls to prevail.

Keep an eye on cryptocurrencies, which are experiencing some volatility this weekend. Despite Friday’s strong recovery, cryptos may be the tail that wags the stock market dog.

Portfolio positioning changes

Even though I believe the market is poised for a multi-week relief rally, the combination of deteriorating global equity and commodity prices is a cause for long-term concern.

One disturbing development is the continual decline in bottom-up aggregated EPS estimates. The latest update of S&P 500 consensus EPS estimates from FactSet shows that the Street has reduced EPS estimates for the next three quarters of 2022 for a second week in a row.

New Deal democrat, who maintains a set of coincident, short leading, and long leading indicators, is still on the fence about a recesion call, though “a recession may be in the offing beginning in Q2 of 2023”. There is sufficient evidence for a global slowdown for a sell signal on the Ultimate Market Timing Model. As a reminder, this model issues a sell signal whenever both the Trend Asset Allocation Model is risk-off and a recession is at hand. Investors should sell into the anticipated rally to raise cash and wait for the all-clear to re-enter the market.

The weakness in commodity prices is also a signal to unwind many of the long commodity and short cyclical pair trades I suggested in the past.

Of the four regional long producer-short importer country pairs and only the long Indonesia and short Vietnam pair has performed well. The other three have faltered and it’s time to close this factor exposure.

From a US perspective, only the quality pairs of long S&P and short Russell indices and the defensive pair of long consumer staples and short discretionary are performing well. The rest, which are long commodity and short cyclical pairs, are rolling over and should be unwound.

The performance of these pairs underscores the underlying factors that are driving the market. Even the commodity and inflation hedge plays have lost their leadership status. Only high quality and defensive factors remain dominant. I interpret these conditions to mean that while the market may be poised for a relief rally, the bears are still in control of the tape.

Investors should also unwind the long gold and short gold miners pair. The relationship is nearing a short-term resistance level in a very short time that it’s time to take some profits.

In conclusion, signs of possible stabilization in crypto assets and speculative growth stocks are pointing to an imminent equity relief rally. Factor analysis shows that the bears are still in control. Investment-oriented accounts should be cautiously positioned and sell into market strength. Traders can try to position for a relief rally, but don’t overstay the party.

Maintaining risk control

Finally, I would like to add a word about the trading model and positioning. My inner trader was too early in entering his long position and he held his position even as the market fell, and some readers raised the question of a sufficient risk control discipline.

Not every trade works. While the current drawdown may be painful, it leads to a useful lesson about the formulation of a risk control discipline.

Portfolio construction consists two decisions. Deciding on what to buy and sell and how much to buy and sell. A strategy of going all-in on a trade signal and all-out on an exit signal will yield different result than a discipline of scaling in and out of positions. I publish long and short positions to disclose possible conflicts. I don’t publish how I scale in and out of positions because it assumes that we have a similar risk profile.

I know nothing about you. I don’t know your risk preferences. Your pain threshold isn’t my pain threshold. I don’t know your tax situation, or even what jurisdiction you live in. If you try to mirror incremental changes in long and short positions is mirroring my risk profile, which is probably not the same as yours.

That’s why this isn’t investment advice. Otherwise, I would be offering a fund, with all the appropriate risk disclosures so that you can decide on whether it’s appropriate for you.

Disclosure: Long SPXL

Cam

Is it time to increase bond market exposure and if so, what duration (still short term maturities)?

Thanks.

If we get a counter-trend equity rally you wouldn’t want to be in the bond market.

Cam, This is, I am assuming, a trading call.

As the expected equity rally stalls and more importantly the growth continues to slow, the long end of the bond market should rally and provide a ballast to the equity positions.

What are your thoughts?

Ken

You had suggested EWC (Canadian ETF) a few quarters ago which has remained stable but not produced mega returns. In fact, last I checked, it is close to a 52 week low, despite its exposure to energy/commodities banks. It does not have significant dividend either.

What is your opinion on it now? Thanks.

I have said again and again that I use an objective moving average exit strategy during Investment Winter. Canada was sold a while ago. It is not on my rebuy list since our vastly overpriced real estate market is starting to seize up.

I use a 90 day line or 200 day on a given ETF depending on whether I want to exit or whether I’m reluctant to exit. I try to fit this with the sector’s evolving narrative. For example, I used 90 day to exit metal mining because of the China lockdown that could hurt metals demand. I use the 200 day for fertilizer because at that level it’s around the Feb. 24 invasion level and I think fertilizer should be MUCH higher due to the war. I’ll admit ahead of time, I likely won’t sell if they go below the 200 for that reason (same for uranium).

With gold bullion , I used the 90 day to exit because I am completely and continually baffled about what’s happening with it. The miners are too volatile for my needs until the bullion starts to make some sense.

Canada was the 90 day because of the metals collapsing and topping out of oil as global recession forces are building. This also works against the Canadian dollar.

I’m using 200 day for Consumer Staples and also Food and Beverage ETFs since I have to hold some equities and Winter is when they do well. Low Volatility ETFs may be on the menu list. When MTUM rebalances later this month, it may be on the buy list since it will then be invested in Winter winners.

Starting last November, you would have seen me in this blog starting to use Alternatives of the long/short equity type. Some advisors recommend holding small amounts of these all the time. Not me. I time the stock market cycle and only load up on Alternatives in Autumn and Winter. They are the reason my clients are sleeping well. When Spring arrives, I will sell them. Why own anything that is shorting stocks when a new bull market starts?

I hope this explains what I’m doing and why. I don’t do short term trading. I make strategic shifts as to where we are in the stock market/factor cycle and use momentum strategy to identify outperforming sectors and those that are failing as we go along.

As Cam says, I am not recommending anything since I don’t know your situation.

I subscribe for Cam’s excellent analysis of the evolving economic and narrative conditions.

Hi Ken, I have an RRSP at RBC and I often wonder about the Canadian banks and their mortgage exposure. The bigger the bubble I suspect the bigger the risk to banks.

There is no jingle mail in Canada like in California, what impact a recession would have on the banks scares me to say the least.

Back in the US housing bubble, the bust did spread and we had the GFC. My understanding is the Canadian bubble is even more extreme.

Any suggestions as to what to watch in the Canadian housing market?

Thanks

The Canadian banks are safe.

The Canadian housing market has confounded me forever so no help there.

Thanks, is that because the Canadian banks have the equivalent of Glass Steagall?

This is not uncommon as I heard from my real estate agent friends. Despite of government control, many rich Chinese can still find a way to get their money out of China. They buy houses in Vancouver and Seattle with cash before they even visit the properties in person. https://biv.com/article/2021/10/man-making-40kyear-bought-32m-vancouver-real-estate-ccp-linked-offshore-accounts#:~:text=A%20citizen%20of%20the%20People's,Party%2C%20a%20case%20study%20by

For traders in this group: One of the most profitable and almost sure shot trade has been selling ten year treasury in the futures market, the symbol is ZN. As prices come down, the goal is to keep selling on every 20-30 ticks rally (I have used pivot points extensively for these trades). Margin money for this contract is also low (1700-1800 $s depending on broker). I am being careful with this trade as the Ten year treasury runs into resistance (at yield of around 3.20%). One expects a rally in this and ZN prices to go higher, as a countertrend rally develops in stocks. This is my base case, in the short term. However, if the ZN contract rallies, I would be waiting to sell/short the contract at higher prices. Cheers and good luck.

For the first time since the Covid Vaccine Day November 9, 2020, I have bought a bond ETF. Not that I am super bullish but at 3% we are at 2018 highs plus we are galloping towards a recession. Note also the Fed Funds Futures look toppy. I cannot justify owning NO bonds any longer for conservative clients.

All to say a leveraged short on bonds might now be more risky that you realize.

Re risk control. I almost always scale into positions for many of the reasons that can be inferred from the comments above.

(a) I tend to be early. Sure, I could simply wait – but scaling in makes more sense as I’m not always early.

(b) Scaling in is a means of emotional control. The market does its best to confuse/frustrate – having an initial position in place keeps both FOMO and regret in check, and I’m less likely to be whipsawed.

(c) I’m sure Cam trades around all of his ST positions – but that would probably result in the kinds of posts that I make 😉

Here is an interesting article on risk control written by a person, Nicolas Colas who worked for Steve Cohen:

https://www.zerohedge.com/markets/we-are-all-traders-now

Personally, I think it is important to understand yourself and the type of trader or investor you are. For example, I am a trend trader. That means I wait for a trend to develop by some objective manner i.e. moving average and then I trade in size making up for not trying to catch the bottom which statistically is bad odds. Famous name like Granville, Precther have gone down that rabbit hole in a blaze of glory.

Also, with no offense meant to Cam his objective may not be the same as mine. He gets to increase his reader subscription by calling a bottom where as mine is to make the maximum amount of money with the least amount of risk.

There is psychology that plays a hand in the markets.

Just like there are epidemics and pandemics, there is market panics and Panmarket panics….that’s when everything goes to 1.

But an example is the shift from SPYG to SPLV when things get stressed, or the move to precious metals when the S&P gets hit….doesn’t always happen.

So what could happen if BTC does a face plant is money goes to the US markets for relative safety but some possible gains….esp in the risky etfs like ARKK…in other words, anything is possible.

GME and AMC show us that markets can be manipulated beyond our wildest imagination….with something opaque like BTC the sky is the limit….it could go to 1million, or zero.

In 2020 we had a Panmarket panic that was halted with a hopefully once in a lifetime panic by the Fed and Gov’t and so much money got sprayed just about everywhere that things stabilized…imagine if we had shutdowns and no support to business and families….there would have been at totally different trajectory.

I don’t think that at present it is Panmarket, but this does not mean that it cannot become such a panic, after all the GFC started late 2007 high but did not really get moving for a good year. I think if all prices start to tank except bonds like TLT for example, then get really scared.

Risk control (or tolerance to losses) is personal and contextual. Each person has a different emotional and behavioral response to wins and losses. This response changes with recent experience. I tend to take more risk if I think I have a hot hand. Less risk on trades if my investments are fairing poorly. Revenge trade is another pitfall.

Each one of us develops and adapts to the changing conditions. Recently, I am cutting my losses quickly and taking profits just as quickly before they disappear.

I need to learn about momentum trading. Scaling in and out techniques. To keep my fear and FOMO in balance.

Learning a lot on these pages. Thanks to all who have shared.

Cam, regarding the signals for going long and exit. I have assumed that the signal is when your model first indicates a long and when the position is totally exited. Scaling in and out don’t generate any additional signals.

Is my assumption correct?

As I understand, the risks associated with the cryptocurrency ecosystem, do not interfere with our assessment of being bullish in the short term, so we can still trade the next positive wave. I also imagine that if we see a crypto collapse, it will have positive implications for stocks in the mid-long term since stocks would be one of the few options to defend investors from inflation

If Tether stable coin breaks down, stock markets will fall across the board. Cryptocurrencies will implode causing a $trillion black hole in the economy. Government bonds would be big winners.

Cam,

What’ll be the impact of the Fed stop buying treasuries and MBSs, i.e., the QT?

Thanks!

sanjay

Off topic.

https://www.sfchronicle.com/bayarea/article/Mill-Valley-teen-drummer-sits-in-with-Pearl-Jam-17173785.php#photo-22478641

Takes me back to the late Sixties, when anyone could and it seemed everyone did start a garage band. The first one I can recall was The Blue Voyage, started by a group of classmates in the eighth grade – they played everything from the Stanford Shopping Center to dances at the Burgess Gym. Rock ‘n’ roll is not hard to play, and their covers were often indistinguishable from the original recordings.

I didn’t get serious about it until the fall of 1970, when I happened to catch Elton John on TV (might have been the Ed Sullivan Show or Dick Cavett) playing ‘Your Song.’ We were living temporarily in Pittsburgh at the time, and my Dad drove me downtown to one of the largest sheet music stores in the country where I found a transcribed collection of John’s entire eponymous album. One of the best LPs ever recorded IMO. ‘First Episode at Hienton’ still drops me right into the winter of 1971 whenever I hear it.

Excellent article!

How to buy stocks on the brink of a bear market

https://www.cnbc.com/2022/05/15/how-to-buy-stocks-on-the-brink-of-a-bear-market.html

This article is out on 05/15. Tons of stocks are already deep in their own bear markets. It is a rolling bear market starting early 2021.

The macro has never been worse except for 2008. Indeed it is total chaos. Capital preservation should be first priority. Forget market timing.

The author is not calling for a bottom. It is a general discussion on strategies on how to buy (NOT buy, really) in a bear market.

Added back a third allocation to VT on the opening decline.

Closed within 15 minutes for a minor gain.

Will be trading around the position throughout the day.

Lots of backing and filling today. Bodes well for a continuation of the rally this week.

Felt like the bears tried to take it down four times and the bulls stood their ground.

Bulls stage an overnight blitz! – launching the ES above a six-day high.

Gun to head, I would say the pain trade is higher. Too many sidelined investors and an overnight gap up precludes an easy reentry.

Shanghai expects to fully reopen on June 1.

Flipping the third allocation of VT on the opening gap. (I traded VT four times on Monday – three for minor gains and closed flat the fourth and last time, which I decided to hold overnight.)

Now back to 40% bonds/40% VT.

I think the next debate will come down to whether it’s a bear market rally or the first leg of a return to new highs.

Re-up to 60% VT as the morning pullback retakes Monday’s closing price.

Locking in profits on the third allocation ahead of Powell’s comments. No idea what he’ll say or how markets will react.

Sensing a little FOMO for the first time in weeks.

Back to a traditional (and fully-invested) 60/40 complexion here. Yes, I’m a little worried. But the time to be really worried was in January – which is when I moved to cash. Still ahead of the SPX ytd by double digits. My time horizon is relatively short – a few weeks. I won’t hesitate to sell should markets prove me wrong. But I have decent buffer in place.

Get Shorty. The squeeze is on.

Obviously, I should have waited to up exposure to VT. Bonds taking the edge off this morning. No plans to make any trades right now.

All retests have to instill genuine fear – otherwise they’re not testing anyone.

The problem for traders is that there isn’t always a retest.

Fear and Greed back to 9.

Still an absence of panic, IMO.

Retesting Thursday’s lows. If successful, would clear the runway for a longer flight.