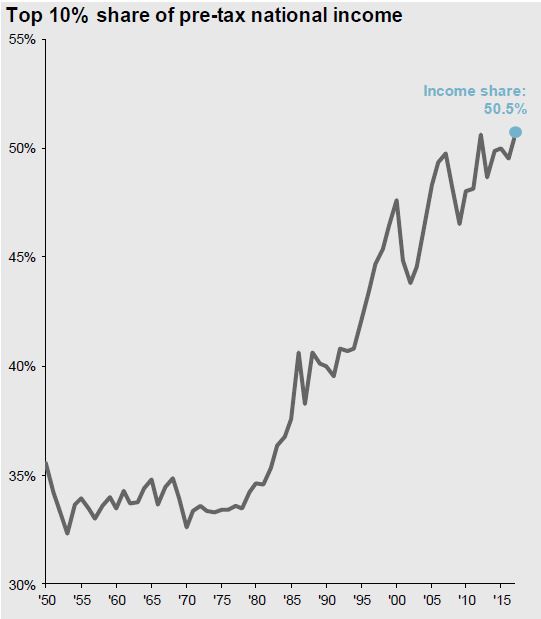

If you thought that Biden would govern as a centrist, you were wrong. In the wake of the passage of a $1.9 trillion stimulus package, President Joe Biden is planning to attack the enduring challenge of inequality by expanding government spending with a second ambitious $3 trillion economic renewal plan and a revamp of the tax code. It is intended to be a repudiation of the Reagan Revolution and the neoliberal consensus that has dominated economic thinking for decades. He reportedly decided to go big on reform for the following reasons:

- Biden is enjoying his honeymoon period, and his approval ratings are strong. The New York Times reported that a Republican pollster found that even 57% of Republican voters supported Biden’s recent $1.9 trillion spending package.

- The Democrats have full party control of Congress, and a short window before the mid-terms to enact legislation.

- The pandemic recovery is offering both economic and political tailwinds to enact legislation.

An attack on inequality

The basic framework of 1970s macroeconomics that framed Draghi and Yellen’s training and outlook, like that of the rest of their cohort, was that properly structured markets would take care of growth. Well-regulated financial systems were stable. The chief priority for economists was to educate and restrain politicians to ensure that inflation remained in check and public debts were sustainable.

In the 1990s, you didn’t need to be a naïve exponent of the post-Cold War end-of-history argument to think that the direction of travel for global politics was clear. The future belonged to globalization and more-or-less regulated markets. The pace was set by the United States. That enabled technocratic governments to be organized around a division between immediate action and long-term payoff. That was the trade-off that Draghi evaluated in his MIT Ph.D. in the 1970s. The drama of Draghi and Yellen’s final act is that for both of them, and not just for personal reasons, the trade-off is no longer so clear-cut. If the short-term politics fail, the long-term game may not be winnable at all. “Whatever it takes” has never meant more than it does today.

- A $2.25 trillion infrastructure plan whose details were announced by the White House last week. The spending would occur over the next eight years, and amount to $250 billion per year, or 1% of GDP. Its main initiatives are:

- Fix highways, rebuild bridges, upgrade ports, airports, and transit systems;

- Deliver clean drinking water, a renewed electric grid, and high-speed broadband to all Americans;

- Build, preserve, and retrofit more than two million homes and commercial buildings, modernize our nation’s schools and child care facilities, and upgrade veterans’ hospitals and federal buildings;

- Solidify the infrastructure of our care economy by creating jobs and raising wages and benefits for essential home care workers;

- Revitalize manufacturing, secure U.S. supply chains, invest in R&D, and train Americans for the jobs of the future; and

- Create good-quality jobs that pay prevailing wages in safe and healthy workplaces while ensuring workers have a free and fair choice to organize, join a union, and bargain collectively with their employers.

- A tax plan which is expected to raise $125 billion per year or 0.5% of GDP. Its major provisions include:

- Raise the corporate tax rate from 21% to 28%;

- Create a corporate minimum tax;

- Double the tax rate on Global Intangible Low Tax Income from 10.5% to 21%;

- Impose a 12.4% payroll tax on earnings above $400,000;

- Raise the top rate for individual taxable incomes above $400,000 from 37% back to the pre-Trump tax cut level of 39.6%,

- Tax long-term capital gains and qualified dividends at the ordinary income tax rate of 39.6% for incomes above $1 million; and

- Ramp up IRS enforcement.

- A second human infrastructure plan, with details to be announced later, with a focus on education, paid leave, and healthcare.

A supportive Federal Reserve

One of Mr. Powell’s greatest strengths may be that before joining the Fed he had not spent his career steeped in macroeconomics, as his two predecessors had. He’s been an avid learner, but also a critical thinker. In a 2018 speech that continues to age well, he took a tactful, almost playful, jab at the high priests of macroeconomics, criticizing some key metrics the Fed was using to guide its policymaking. Translated into plain English, he told them that many of the metrics are effectively made-up numbers.

It’s no accident that under his leadership the Fed adopted a new framework that emphasizes the employment mandate. It’s grounded in what he learned from people on a review tour called “Fed Listens,” which included community leaders and ordinary workers who pushed him to support more job creation among low- and moderate-income people.

Fed governor Lael Brainard made two speeches on the same day affirming the Fed’s support of Biden’s objectives. The first speech was to the National Association for Business Economics on March 23, 2021 in which she affirmed that the Fed is monitoring “shortfalls from employment” rather than a “maximum employment” benchmark.

The FOMC has communicated its reaction function under the new framework and provided powerful forward guidance that is conditioned on employment and inflation outcomes. This approach implies resolute patience while the gap closes between current conditions and the maximum-employment and average inflation outcomes in the guidance.

By focusing on eliminating shortfalls from maximum employment rather than deviations in either direction and on the achievement of inflation that averages 2 percent over time, monetary policy can take a patient approach rather than a preemptive approach. The preemptive approach that calls for a reduction of accommodation when the unemployment rate nears estimates of its neutral rate in anticipation of high inflation risks an unwarranted loss of opportunity for many of the most economically vulnerable Americans and entrenching inflation persistently below its 2 percent target.11 Instead, the current approach calls for patience, enabling the labor market to continue to improve and inflation expectations to become re-anchored at 2 percent.

Although the unemployment rate has moved down 1/2 a percentage point since December, the K-shaped labor market recovery remains uneven across racial groups, industries, and wage levels. The employment-to-population (EPOP) ratio for Black prime-age workers is 7.2 percentage points lower than for white workers, while the EPOP ratio is 6.2 percentage points lower for Hispanic workers than for white workers—an increase in each gap of about 3 percentage points from pre-crisis lows in October 2019.

Workers in the lowest-wage quartile continued to face staggering levels of unemployment of around 22 percent in February, reflecting the disproportionate concentration of lower-wage jobs in services sectors still sidelined by social distancing.5 The leisure and hospitality sector is still down almost 3.5 million jobs, or roughly 20 percent of its pre-COVID level. This sector accounts for more than 40 percent of the net decline in private payrolls since February 2020. Overall, with 9.5 million fewer jobs than pre-COVID levels, we are far from our broad-based and inclusive maximum-employment goal.

The Federal Reserve created a new Supervision Climate Committee (SCC) to strengthen our capacity to identify and assess financial risks from climate change and to develop an appropriate program to ensure the resilience of our supervised firms to those risks.6 The SCC’s microprudential work to ensure the safety and soundness of financial institutions constitutes one core pillar of the Federal Reserve’s framework for addressing the economic and financial consequences of climate change.

Climate change and the transition to a sustainable economy also pose risks to the stability of the broader financial system. So a second core pillar of our framework seeks to address the macrofinancial risks of climate change. To complement the work of the SCC, the Federal Reserve Board is establishing a Financial Stability Climate Committee (FSCC) to identify, assess, and address climate-related risks to financial stability. The FSCC will approach this work from a macroprudential perspective—that is, one that considers the potential for complex interactions across the financial system.

Measuring market impact

- If rising rates are primarily driven by expectations of higher real growth, the effect is more likely to be positive, as higher growth and margins offset the effect of investors demanding higher rates of return on their investments.

- If rising rates are primarily driven by inflation, the effects are far more likely to be negative, since you have more negative side effects, with risk premiums rising and margins coming under pressure, especially for companies without pricing power.

Another issue concerns globalization. A key reason for believing that inflation is about to rise comes from the Phillips Curve, which in simple terms posits a trade-off between unemployment and price increases. Reducing unemployment, as policymakers are determined to do at present, will lead to higher inflation, all else equal.

But all else isn’t equal, and for the last four decades at least we’ve had steady globalization. That means that in an open economy, fewer workers doesn’t mean higher pay, it means a greater likelihood that employers will look overseas. Indeed in Germany, unions negotiate to maintain jobs at the expense of wage rises, because they are aware of competition from abroad. Thomas Aubrey of Credit Capital Advisory in London shows that over time in the U.K., the curve is flatter (meaning there is less of a trade-off) when the economy is more open to trade. And it is a process that can repeat itself. Aubrey points out that textiles jobs in China are leaving for cheaper countries, now that wage demands are growing.

All of this suggests that the critical variable to watch in the next few years concerns trade policy, rather than fiscal or monetary policy. If the world really does reset into two rival blocs that attempt to minimize trade with each other, as is possible if U.S.-China relations come out at the worse end of expectations, then the logical consequence would be a return of inflationary dynamics to the West.

To mobilize against World War II, federal debt tripled, the Fed’s balance sheet swelled by 10-fold and the Fed capped both short- and long-dated interest rates below the rate of inflation. Granted, the current playbook isn’t quite that aggressive — the Congressional Budget Office’s forecast for the national debt in 2030 is only 6% higher than it was before the COVID-19 pandemic — but directionally it is similar.

I am raising my S&P 500 operating earnings forecast for 2021 from $175 per share to $180, a 27.8% y/y increase from 2020. I am also raising my 2022 forecast from $190 to $200, an 11% increase over my new earnings target for this year. I would have raised my 2022 estimate more but for my expectation that the Biden administration will raise the corporate tax rate next year…

One of my accounts asked me whether I should lower my outlook for the forward P/E given that I am predicting that the 10-year US Treasury bond yield is likely to rise back to its pre-pandemic range of 2.00%-3.00% over the next 12-18 months.

Normally in the past, I would have lowered my estimates for forward P/Es in a rising-yield environment. However, these are not normal times. In the “New Abnormal,” valuation multiples are likely to remain elevated around current elevated levels because fiscal and monetary policies continue to flood the financial

This sounds fairly similar to Japan or Greece’s attempt to stimulate the economy with infrastructure spending. How did Japan/Greece’s outcome result in deflation instead of inflation despite the massive infrastructure spending?

I’ve read some opinions on the internet about the whys, but was curious if you had your own take on those two countries failed attempts.

The “bridges to nowhere” strategy works in the short run but unproductive investment won’t work in the long run. In the past, periodic bouts of Japanese fiscal stimulus have produced short-term lifts which were bullish.

I don’t know if the Biden plan will work in the long run, but US airports like LGA is an embarrassment for a G7 country. So is rail transport. The upgrade of the electric grid and broadband initiatives are constructive. Assuming that we get wider electric vehicle adoption over the next 10 years, the grid needs an upgrade.

The short answer is fiscal stimulus almost always produces a boost to the economy, whether it’s in the form of tax cuts or government expenditure. For investors, my advice is to enjoy it while you can, and watch for signs of it to either take off or fizzle later.

Right on, Cam. Observe and adjust. Never take it for granted. Respect the price movements.

As for Biden’s plans, I have some personal opinions. Since coming to US at 18, I have lived here for 20+ years now. The change in US as a country has been dramatic, for the worst kind. US is increasingly phony and corrupt, and accompanying it very wasteful. The sense of honor and responsibility barely exists today, if at all. All I need is to bring up one example: SF Bay Bridge expansion span project. If you spend a little time and research it, you will be shocked by the whole thing. Multiply it by hundreds of examples across the whole US. Biden’s plan and budget is not going to accomplish much.

Then about education. This is supposed be the most important foundational work for any country. Let’s have one example too, LAUSD. This is a district whose students are 98%+ Latino. Two election cycles ago, CA voters are tricked into voting for a bond measure to increase funding. Then LAUSD used half of their share to purchase Ipads, one for every student, at 50% premium than store price. Kids use it to play games. Nothing changed. In fact it got worse. CA used to have HS senior exit exam. If you don’t pass you don’t get diploma. The level of difficulty is already watered down to ridiculously basic. Even at this level 95% of the students in LAUSD would not pass. So what happened. Jerry brown and state legislature (almost 100% D) got rid of the exit exam and called the exam discrimination and racist and culturally insensitive. All right this what we’ve got. Now do the same thing and multiply it across all major cities (pretty much all D). Tell me this is going to solve the problem.

Funding is a not a problem. It is the attitude. As it goes at present no amount of money can help much. As a US citizen, I have to accept that US is in serious decline. I don’t see any solution when you have such a stupid citizenry.

Again just observe and adjust. Nothing fancy about it. Always have a plan B in place.

You seem surprised! Stop drinking the American Koolaide.

Gosh, it’s human nature. You can’t change it. Old saying, “God helps those who help themselves” Exactly, those with the right attitude. How do you change attitude in someone else? You cannot.

Before long, you can get a burger made by a robot, served by a robot at the drive thru window, or you can pay more for one made by a teenager who was not paying attention etc etc. So what will you do?

70% service economy….you have to pay for service…can a 70% service economy stay afloat? Only if the other 30% is super productive. Of course it gets outsourced, things are cheaper over there and for ordinary things price matters.

So what’s going to happen to all these burger flippers, and collectors of groceries that are so prevalent nowadays at Walmart etc? When the robots can do it?

No way they can all be employed, unless we cut the work week to one day, then they won’t be good at what they do.

There will be some kind of universal basic income, or things will be chaotic and dangerous.

There will be a minority who provide services above robot level…the fortunate ones.

Those on UBI, will also be cost conscious, price matters….they will buy roboburgers too.

Attitude, only experiences, call it God if you wish, can change your attitude.

The main problem with the US (and Canadian) K-12 education is the faulty curriculum with regard to the STEM subjects. Then it is the lack of good textbooks.

Science subjects are not taught until HS, and then it is a la carte and usually in the wrong order (bio-chem-phys). Sure, there are classes called “science” earlier, but they don’t teach much other than a few definitions from a random array of topics.

Then students are expected to learn a science subject in only 1-2 years. It’s impossible! In my son’s HS physics class they are covering mechanics, thermal physics, optics, and electromagnetism in a single year. Add to this the horrendous textbooks – lengthy and messy. It’s impossible for students to excel without outside help – parents and/or tutors.

Math is usually only taught at the arithmetics level until HS. Then students are expected to reach calculus level in only 2-3 years. Similarly horrible textbooks. Also, math is not being taught in parallel with the science subjects, which would be very beneficial (e.g. vectors when studying forces in physics).

In my country or origin (Eastern Europe) algebra and geometry were taught from 4th grade. Physics and chemistry every year from 6th until 11th (2-3 classes/week). The textbooks are 150-200 pages. Each lesson usually 3-4 pages. Well organized, easy to go back and review the material. The honors math textbooks for 10, 11 and 12 grade from my country, combined(!), are less pages that the 10th grade pre-calculus textbook in my son’s US HS. And they cover more material, at higher level, better explained, and with more practice problems than the US textbook.

I’ve done some important work on equal weight indexes. They offer an extremely better view of stock movements as it relates to the evolving economic narrative.

Here is the most obvious example, Consumer Discretionary. The economy is posed to reopen and consumer spending will rise. The stocks in this index should be reflecting that narrative but the GICS index has been falling instead. Here is a chart of the weighted GICS Cons. Disc Index and the Equal Weight Cons. Disc. (rebased to the Vaccine Nov. Twist day)

https://refini.tv/3cMJOPr

Amazon and Tesla are 39% of the weighted index. This is so distorting.

I’ve also constructed equal weight Growth and Value Indexes from their S&P Pure Growth and Value counterparts. Here they are;

https://refini.tv/3duNSCP

Growth equal weighted is no longer distorted by the FAANG+ unwinding its overvaluation. Value is not distorted by the highly weighted banks and energy stock super charged gains.

What does this all mean? It means that low weighted company stocks are doing fine and reflecting the improving economic outlook. It says low weighted Value stocks haven’t gone up to extreme high-priced risky heights and low weighted Growth stocks were not caught up in the overvaluation of the popular ‘Stay at home’ stocks and hence not too risky to buy.

On my momentum work, I now use the equal weighted S&P 500 (symbol RSP). Here is my momentum chart on S&P 500 Weighted (SPY) versus equal weighted (RSP)

https://product.datastream.com/dscharting/gateway.aspx?guid=b98d2495-ebe1-4ed4-b0e1-d56169213a4f&action=REFRESH

The equal weighted has done 10% better than the market weighted!!!!

This is a much higher bar than the SPY to perform against. It also begs the question, “Why not just buy the S&P Equal Weight ETF (RSP) if you want to be lazy and just make a great return as the pandemic fades away?

China-related and this includes Emerging Markets are failing from a momentum perspective. Japan is as well. This may be a regional response to the Biden led multi-lateral confrontation with China.

Market gurus I respect have warned that the investment world is shifting to three regions, China-centric, America-centric and Europe. This narrative is showing up in my momentum work.

Ken from a technical perspective the dollar Index (DXY) has crossed above it 200 day moving average, which as you know is positive for the dollar. Hence, all Emerging Markets which have an inverse relationship to the dollar are getting affected.

When we talk about inflation hurting stock markets, I will keep reminding that inflation hurts inflation hating industries and helps inflation loving industries. In the high inflation 1970’s, the inflation loving, resource rich, Canadian stock market index QUINTUPLED while the U.S. DJII was FLAT for 16 years (earnings went up but they were offset by lower PEs).

Ken,

Thanks for all your constant, valuable insights. I, and I am sure all others on this site, really appreciate your hard work and sharing your work here to benefit all of us.

Ken, I second that sentiment. Thank you for sharing your insights. It keeps me grounded as the stock market twists and turns, and the narrative shifts from one minute to another.