FactSet reported last week that bottom-up aggregated earnings estimates have been skidding rapidly for both 2020 and 2021.

Forward 12-month EPS estimates are falling even as stock prices rose.

Do earnings matter anymore?

Flying blind

What is the market discounting? At this point, any estimates that analysts make are only wild guesses. No one can tell you the future (sorry, my time machine is still in the shop). We are all flying blind.

Those of us who are old enough may remember the 1996 plane crash of Clinton era Commerce Secretary Ron Brown on a hillside just outside Dubrovnik (see Politico story). The weather was bad, and the aircrew was unfamiliar with the navigation aids in the area.

Yes, today’s market conditions are like that. The WSJ reported that even Charlie Munger, Warren Buffett’s longtime partner, sounded a cautious tone:

In 2008-09, the years of the last financial crisis, Berkshire spent tens of billions of dollars investing in (among others) General Electric Co. and Goldman Sachs Group Inc. and buying Burlington Northern Santa Fe Corp. outright.

Will Berkshire step up now to buy businesses on the same scale?

“Well, I would say basically we’re like the captain of a ship when the worst typhoon that’s ever happened comes,” Mr. Munger told me. “We just want to get through the typhoon, and we’d rather come out of it with a whole lot of liquidity. We’re not playing, ‘Oh goody, goody, everything’s going to hell, let’s plunge 100% of the reserves [into buying businesses].’”

To be sure, there is a variety of opinions. An article in Barron’s pointed out an unusual reading in the University of Michigan Sentiment Survey. While sentiment for current conditions had deteriorated, future expectations are still bright. Is that what’s holding up stock prices?

What are companies saying?

As we go through Q1 earnings season, companies usually offer guidance for Q2, as well as for the rest of the year. What are companies saying about the outlook?

FactSet reported that, as of April 24, 122 companies have reported, and 50 companies had commented on EPS guidance. Of the 50 companies, 30 (60%) were either withdrawing guidance or had withdrawing previous guidance for the year. The two sectors that had the biggest ratio of withdrawn guidance to providing guidance are industrial and healthcare companies.

For more color, I turn to The Transcript, which transcribes earnings calls. Here is what some executives said two weeks ago about business conditions.

Consumer spending is getting crushed

“We’ve entered into a world we haven’t seen before. Much of the economy is essentially closed. Consumer spend is down over 25% year-over-year this past week with food and drug increasing and other spend down significantly. New auto sales in the month of March were down at 32%” – Wells Fargo (WFC) CEO Charlie Scharf“if I think about kind of the last week of March. the card spend activity, just broadly for us was down about 30%, U.S. spend by category down total of 30%. The big categories, if you will, impacted are not going to be of any surprise to you, travel down 75%, dining and entertainment down some 60%, discretionary retail, which would include apparel, department stores, etc, down 50%, essentials were up 10%.” – Citigroup (C) CFO Mark Mason

Most companies seem to be modeling a recovery by the second half of the year

“Both scenarios, though, do include a recovery in the back half of the year.” – JPMorgan Chase (JPM) CFO Jennifer Piepszak“we see the environment showing near-term disruption and turbulence, but expect the longer-term to present opportunities to capitalize on many of our existing priorities” – J B Hunt Transport Services (JBHT) CEO John Roberts

“based on the data that we’re seeing from – that we’re collecting on a daily basis, is that we can see a recovery into Q3 and into Q4, especially for these more elective procedures…our modeling here suggest the kind of recovery that I’ve just described.” – Abbott Laboratories (ABT) Wyatt Decker

However, there are many reasons why this may not be a V-Shaped recovery

“It is not going to be what happened then, which was a very, very quick return to normalcy. That is not going to happen. At best, we’ll have kind of a rolling way out. As far as travel is concerned, while I’m absolutely optimistic that at some point, but I don’t think soon, I don’t think it’s until probably September, October, November, December, really get life back. And in order to travel, you’ve got to have that. So, they’re totally different situations. This is not analogous. I don’t think it’s analogous to anything. Certainly not analogous to 9/11 and to the financial crisis in ’08″” – Expedia (EXPE) Chairman Barry Diller

Here are some excerpts from the latest week’s earnings calls, which show a more nuanced interpretation of the gloom, as well as some signs of stabilization.

The question is how long will the decline last?

“our earnings will be driven by the answers to two questions that no one can now – no one yet can answer. First, when and how strongly does spending rebound as the global economy recovers? Second, how long do the challenges of high unemployment levels and small business shutdowns last, perhaps softened by the record levels of government support and what does that mean for our credit losses?” – American Express (AXP) CEO Stephen SqueriThe major forces at play are non-economic

“A lot of what will happen in the coming weeks and months will be dictated by governments, medical experts and circumstances that are completely unpredictable and out of our control.” – Moelis & Company (MC) CEO Ken MoelisSome hard hit industries are seeing trends stabilize

“Delivery and carryout mix are holding relatively steady on average. Weekday sales have been significantly up, while weekends have generally been more pressured. Lunch and dinner dayparts are up, while late night had been more pressured, and we are seeing larger order sizes throughout the week.. we’re finding, at Domino’s, and I think some of our peers in the restaurant industry are finding, people are ordering extra food to have leftovers around also, which is a really interesting dynamic in the market today.” – Domino’s Pizza (DPZ) CFO Jeffrey D. Lawrence“I’m pleased to report that only about 100 restaurants are fully closed at this time. These are mainly inside malls and shopping centers as well as 17 locations in Europe, while the rest of our restaurants remain open…as COVID-19 restrictions became more prevalent, our comps deteriorated and ended up declining 16% for the month, with the week ending March 29 being the trough at down 35%…April has seen our comps improve with the most recent week adjusted for Easter being in the negative high-teens range.” – Chipotle (CMG) CEO Brian Niccol

“Thus far through April, our in-patient admissions are running about 30% below the prior year. Our emergency room visits are running about 50% below prior year as our in-patient surgeries. Our hospital based outpatient surgeries are running about 70% below our prior year as most elective procedures have been deferred. We have started to see these volume declines stabilize over the past week.” – HCA Healthcare (HCA) CFO Bill Rutherford

As different countries and US states tiptoe towards reopening their economies, FT Alphaville reported that Jeffries had commissioned a private poll of 5,500 consumers in 11 countries about their spending intentions in a post-lockdown environment. As FT Alphaville put it, “For those hoping for a uniform V-shaped recovery, look away now.”

The challenges of forecasting

I recognize that forecasting the trajectory of the global economy for the next two years is a tremendous challenge right now.

FactSet reported that forward 12-month P/E is now at the nosebleed level of 19.1, with earnings estimates still falling. Even if you accept the premise that investors are looking over the 2020 valley, the P/E ratio based on 2021 estimates is 16.6, which is just below the 5-year average of 16.7, and above the 10-year average of 15.0.

Still this makes no sense, as valuations are clearly elevated. Why would you buy the market at about the 5-year average forward P/E given the high level of uncertainties facing investors?

The FT’s Martin Wolf recently unpacked the IMF’s forecasts for 2020 and 2021 before the virus, and after the crisis. The outlook does not look good, especially for the advanced economies.

Moreover, there is considerable uncertainty around the forecasts, depending on differing scenarios.

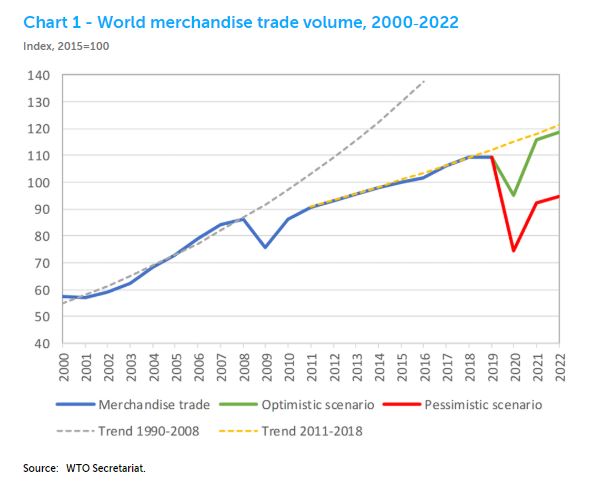

The WTO’s trade forecasts are all over the place.

Could that explain the disconnect between the stock market’s elevated levels? Is the market just discounting the best case scenario and ignoring the risks of the worst case?

Narrow leadership and market concentration

Here’s is how I square the circle of dire economic outlooks and buoyant stock prices. The stock market isn’t the economy, largely because of the narrow leadership of the megacap stocks and their market concentration.

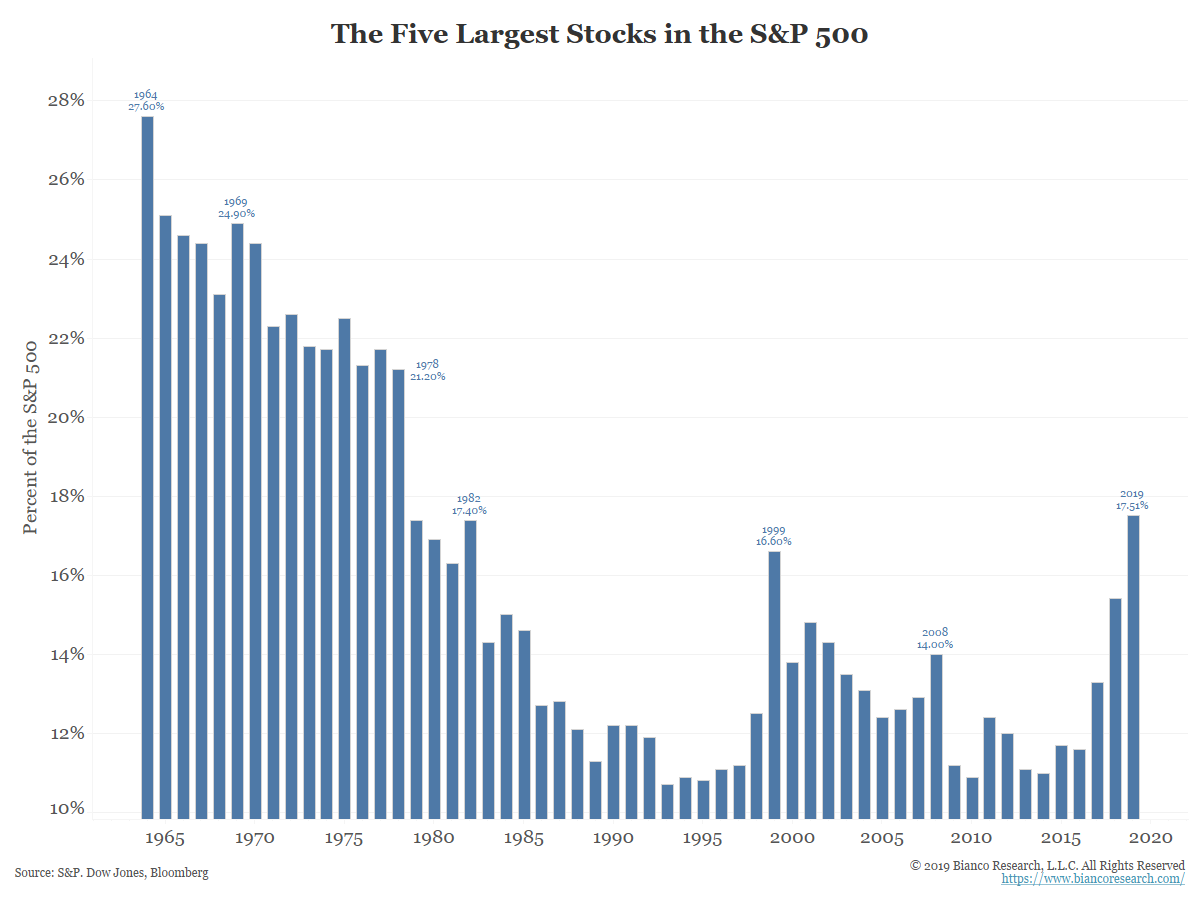

I wrote yesterday about the risks of narrow leadership (see Factor review: Narrow leadership and its implications). Michael Batnick documented how the top five stocks in the index equal the weight of the bottom 350.

Zero Hedge (bless their eternally bearish and Apocalyptic hearts) seized upon a report from Goldman Sachs calling for an imminent momentum crash owing to narrow leadership, but I consider that a “this will not end well” story that can last a long time.

High market concentration is not necessarily bearish. This kind of concentration is unusual in today’s era, but it was not unusual back in the 1960’s and 1970’s. That’s why the DJIA was an important market benchmark back then, because the big stocks were the market.

I asked rhetorically at the beginning of this publication whether earnings matter. Yes, earnings matter, but the analysis so far confuses the market with the economy. The stock market does not represent the economy because of the narrow market concentration, and the leadership of the megacap stocks.

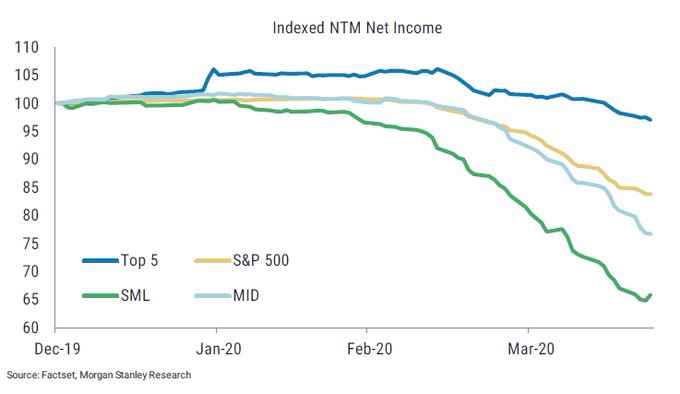

The megacap leadership stocks are reporting earnings this week, namely Alphabet (Tuesday), Microsoft and Facebook (Wednesday), and Apple and Amazon (Thursday). Analysis from Morgan Stanley concluded that the index gains by the top five companies have “been driven more by relative earnings resilience rather than valuation as forward net income estimates have come down far less than the market”. These earnings reports may determine the short and medium term tone of the market.

In the short run, that’s how earnings matter.

I am discounting the probability of a really bad economic outcome due to the ‘Cold War’ to get a vaccine/treatment (and Fed action). US and China are very very motivated to find a treatment. Also whilst things may be horrible for the real economy, for tech even negative trends in short term earnings is far outweighed by the valuation effect of 30yr rates. Additionally death rates in places like Sweden that haven’t closed bad aren’t that bad.

Looking at the below sentence, I completely agree :

“Still this makes no sense, as valuations are clearly elevated. Why would you buy the market at about the 5-year average forward P/E given the high level of uncertainties facing investors?”

Now, we could answer : because the cost of opportunity in investing in IG bonds is clearly very low, we don’t get anything there.

Now, you could argue : “How about HY ?”. Maybe going into HY is actually providing the same downside than stocks, but with limited upside. Just playing the Devil’s advocate here…

Why would you buy the market at the 5-yr average forward PE given the level of uncertainty? This is an excellent question. One response might be because the market can continue to become much more overvalued over a long period of time. Recall that during the majority of the last decade-long bull run the PE was above 15 (and above 20 for the last 5 years). You would have missed the entire bull market.

You are confusing forward 12m P/E, which is 19 and higher than it’s ever been since the Tech Bubble, with a P/E based on FY2 earnings.

Buying on FY2 P/E of 16.5 requires a level of certainty that doesn’t exist today.

Fair point. To clarify, i wouldn’t (and am not) be buying here. I did buy at 20% down and 32% down. I’ll likely hold currently allocation and trim down (from 75/25 equity/cash) to 60/40 if US markets go up another 5-10% from here as my concerns mirror your own.

I’ve been thinking of a pre-mortem (looking back from a future where an idea went wrong) of today’s market price going up rather than down. The only thing is monetary debasement and the growth of investment targeted savings.

We know that the market after the GFC has been 90% correlated to the level of the Fed balance sheet. We also know that institutions need to invest their money into some financial asset with cash to be avoided. We see may investors simply buying Vanguard ETFs every month following the averaging mantra. We can see the strong possibility that consumers will reduce spending to build an emergency savings fund and that means more cash in the financial system. It also means that demand inflation won’t happen with the high money supply growth, at least for a long while.

All this to say that the level of the stock market as an asset class could float higher on the exploding amount of cash being injected into the economy rather than an evaluation of the business merits of the companies.

If you want to see extreme examples of this phenomena, look at the stock market indexes of Venezuela and Argentina. They go up and up and up every week come rain or shine.

Is money globally being debased to the degree that stocks float on a sea of a rising tide?

We will know next year, looking back on our pre-mortem.

Ken, what you are saying is just more fuel for my thoughts below that the Fed has turned the stock market into the equivalent of a penny stock market.

Ken is right that in the past when Latin American countries have gotten into economic trouble and had to devalue and inflation ran wild, local equities have soared. The catch is they soared in local currency terms, and not necessarily in USD terms. That’s because businesses, if they are viable, act as inflation hedges if they can pass on rising costs to their customers. They can do this in two ways, by being exporters, or passing through inflation to local consumers.

This is not the case today.

So, the FANGs ARE the market now.

I mentioned this a week or so ago that I think the stock market has also turned into a penny stock market. What In a penny stock market there is no valuation. There are no earnings. It’s the greater fool theory that keeps prices rising. As long as there is more new money finding its way into the market the prices go up.

The Fed has created a penny stock situation or Greater Fool Market. There are trillions of dollars injected into the economy chasing stocks. In addition to the stimulus, the Fed is pumping $51 Billion every day into the banking system. That money goes somewhere and that somewhere is primarily the stock market. There is a constant supply of “Greater Fools” so the market goes up regardless of valuations or earnings.

A penny stock market can climb for months or even years. But when the party is over (all fools are in) watch out for the crash. In our case, watch out for the Fed withdrawing QE (or what ever you want to call it) because the party will be over.

Stock Up!!

“Tyson Foods (TSN) is warning that “millions of pounds of meat” will disappear from the supply chain as the coronavirus pandemic pushes food processing plants to close, leading to product shortages in grocery stores across the country.”

https://www.cnn.com/2020/04/26/business/tyson-foods-nyt-ad/index.html

Maybe what investors are focusing on is dividends. Many conservative investors have been happily ‘buy-and-holding’ a portfolio of ‘safe’ stocks. They aren’t selling. One reason is capital gains taxes that would be payable. The other is a strong builtup belief in sticking with the program..

Massive dividend cuts along with falling stock prices of these ‘safe’ stocks would shake this complacency.

I saw a reference to a futures market on dividends of S&P 500 for year end 2021. It had fallen 50% the last couple of months. In other words, experts are expecting massive dividend cuts in the near future.

I see that dividend ETFs have about 20% of their dividends from energy companies. That is an obvious problem. Banks dividends are a risk.. The ECB just mandated all European banks must stop paying dividends. For any company, does it make sense to borrow to pay dividends.?

When dividends start getting cut, stocks could see some pressure.

Banks and Small-caps doing very well today as compared to the other indices.

Sector/style rotation?

New Zealand Says It Has Won ‘Battle’ Against COVID-19

https://www.npr.org/sections/coronavirus-live-updates/2020/04/27/845304917/new-zealand-says-it-has-won-battle-against-covid-19?utm_campaign=storyshare&utm_source=twitter.com&utm_medium=social

Dividends are being cut, so it’s not an “if” at this point. But some corps do have “safer” dividends than others. There are also the preferreds, even if having rate reset structures rather the “real” preferreds.

But doesn’t:

• profits -> losses or

• profits -> decreased profits or

• losses -> greater losses

fot growth companies equal dividend cuts for dividend paying companies? It seems to me that share valuation over the long term must depend on the profitability / cash flow capability of a corporation.

So, isn’t the question on profits:

How low will profits go and for how long?

We know they are going down, so the only unknown is “for how long?”

Cam, you had said that we should follow small caps and treasuries to get a sense of short term directionality. Small caps are rallying now– does this affect your short term/ medium term outlook? TIA

Using treasuries as a guide is not working. Check the Fed bond buying program. Traders would front run the Fed, causing TLT price increase. This has been demonstrated during past QE operations. Treasuries as a hedge has declined to very low level since early March. Now it is affected by Fed and front-running traders mainly.

Thank you @Ingjiunn!

ICYMI: A discussion of covid-19 super-spreader events in 28 countries.

https://quillette.com/2020/04/23/covid-19-superspreader-events-in-28-countries-critical-patterns-and-lessons/

I skimmed through the very long piece of research article. In essence author is guessing that main mechanism of covid19 spread is through high velocity ballistic transmission of larger droplets? If that’s the case using some cheap reusable masks would still show some significant effects.

“…the virus is unlikely to be eradicated, despite costly lockdowns that have brought much of the global economy to a halt. ”

“So globally, even during the summer, the chance of cases going down significantly is small.”

https://www.bloomberg.com/news/articles/2020-04-28/virus-is-here-to-stay-and-likely-seasonal-say-china-scientists?srnd=premium

To be honest this is a lesson of a pain trade. I have never imagine that SPX / ES can reach 2900 in April(!). As I am short it is a painful experience for me but no pain no gain.

I agree it’s quite painful and simply strange to see the mkt climbing back while the econ is deteriorating. I will wait it out and see if the “sell in May..” saying really holds some truth.

Same here…. Mr Market… I’m seriously questioning your rationality….lol

If the us brings UBI I guess the market will not go down in this crisis anymore. Especially if the fed finances it by buyint treauries.

Universal Basic Income? Pelosi is dreaming. It’s not going to happen in my lifetime.

Thanks for the inner-trader update, Cam. That was tough one.

I have to quote what Ken wrote in the last one: “Investors are blind to the damage that the FED foresees and only see the medicine.”

And an eye-opening experience, also known as an epiphany, can come like a bolt of lightning.

States are just beginning to open up. I think we have to watch the infection rates in the coming weeks. The market may anticipate any relapse in infection rates.

This all makes my head hurt. I’ll leave it to Cam to sort this out. He’s better at it than any of us.

And of course, the market turns negative now. This is the classic case of Market making fools out of everyone at one time or the other.

So, hopefully the market will do another high tommorow (FED) and we will be able to load up the shorts as the negative divergences will form.

Germany (better healthcare system and public health than US) is scaling back reopening plans again after seeing a resurgence of cases weeks after reopening. Lol that was quick.

I respect your opinion Ellen, and thanks for the update. But coming from a family of surgeons and nurses, and being treated myself in the Mayo’s system, I think I’d rather stay in the U.S. when it comes to most healthcare issues.

No worries– my larger point is that reopening the economy here with less healthcare and testing infrastructure is precarious at best. I’m a physician myself occasionally working on front lines when necessary, respect your opinion too. When it comes to COVID, Germany’s outcomes are clearly superior to US, stats do not lie. To each their own!

Not wrong, just early.

Agree. I think Cam has nailed the big picture. The market will ultimately retest the lows (and IMO the decline will exceed the March lows). But how and when is anyone’s guess. We’re all guessing when it comes to market moves. Cam just does a better job of deciphering the clues.

To combat the coronavirus pandemic, Pfizer Inc. said it could have a vaccine ready for emergency use by the fall, according to a report.

https://www.foxnews.com/health/pfizer-coronavirus-vaccine-could-be-ready-by-this-fall-for-emergency-use

*could*

“The race for a vaccine to combat the new coronavirus is moving faster than researchers and drugmakers expected, with Pfizer Inc. joining several other groups saying that they had accelerated the timetable for testing and that a vaccine could be ready for emergency use in the fall.

Pfizer said Tuesday it will begin testing of its experimental vaccine in the U.S. as early as next week. On Monday, Oxford University researchers said their vaccine candidate could be available for emergency use as early as September if it passes muster in studies, while biotech Moderna Inc. said it was preparing to enter its vaccine into the second phase of human testing.”

Lots of hope.

We’ll just have to wait and see but I’m sure many market participants take this sort of news as mostly going to happen in just a few months.

I respect all of the views expressed on this group, and concur with Cam’s essential view about the recession. Full stop.

Another voice, that I happen to agree with is Scott Galloway of NYU Stearn, who eloquently waxes on about how this pandemic is not simply a “pause” on the old normal; rather it is a catalyst for the acceleration of the future. A winner-take-all, re-order of those who can innovate in a time of crisis, and those who will be left behind.

I am mostly in cash, except for my long term bets on those tech trends that will endure 1-5-10 years forward.

He’s often a bit crude, but tune in if you’re in need of entertainment: http://www.westwoodonepodcasts.com/pods/the-prof-g-show-with-scott-galloway/

Details on Texas reopening: https://gov.texas.gov/organization/opentexas

Stay at home orders end May 1, and businesses (restaurants, malls, movie theaters) may reopen at 25% capacity.

A nice perspective from John Authers:

Going by the Conference Board’s consumer confidence index, consumers feel better now than they did during the GFC (from 2007 thru 2013). Interesting!

We have almost unlimited help from the Federal Reserve. The actions also averted a credit collapse.

At least in the initial “panic” stage, much of the selling was driven by personal immediacy or a “me, here, now” mentality. Consciously or unconsciously, the more scared you are that you have Covid-19 yourself, the more this will affect your actions.

I fear that the market rally has been driven by people for whom the virus seems less immediate and close, and who have moved from excessive fear to over-optimistic forecasts that the disease will now disappear.

https://www.bloomberg.com/opinion/articles/2020-04-29/stocks-rally-has-roots-in-waning-fear-of-coronavirus?srnd=premium

My expectation is that today we will be hearing from Mr. Powell about the details of the Fed’s corporate bond buying program – and tomorrow we will be hearing from Luca Maestri how he is going to use those funds to buy back more Apple shares. Now, of course there are some fig leaves implemented to cover up what is happening – the Fed’s corporate bond buying is limited to companies with “significant operations in and a majority of its employees based in the United States”. This, even though it does not truly reflect the real circumstances (Apple actually supports more jobs in China than in the US) is factually true for Apple which has about 80k people directly employed in the US compared to the total number of 137k (as reported in 2019) I wonder for how long they are planning to keep this going.

This is how big data algos shaping the investment landscape. Do not put yourself in detriment. Everything happened and what we have learned in the last 10 years are all applied instantly this time around. Fed also runs one of the biggest data bank in the world. They have algos too. This is how Powell and gang responded: at lightening speed. It will be proven as right moves.

I remember when Bernanke got on CBS 60 minutes after GFC and talking about green shoots, and received plenty of jeers from pundits everywhere. Bernanke was proven right even it was the first time in US history with so many programs established at the same time trying to combat the situation.

I think people need to accept the concept of asset administration by government. This is not about taking a red or blue pill. It is about recognizing the reality and adapting. Also accept the fact that markets are algo-driven and that centers around volatility.

https://www.yahoo.com/news/6-monkeys-given-experimental-coronavirus-094138199.html?guccounter=1

https://www.yahoo.com/news/worlds-largest-vaccine-maker-producing-095749870.html?guccounter=1

Massive efforts are now being made globally to come up with a vaccine against this virus. What happens to the stock markets if one or more of these is successful?

U.S. first-quarter GDP contracts 4.8%

E-Mini S&P 500 Futures are up on the above news!

2,895.25

+ 28.05 0.98%

Consumer spending falls 7.6% in first quarter

S&P 500 futures are now up 50 points!

The worse is the situation the bigger must be FED reaction. It was also the motto of one political party: The worse, the better. Hope I have translated it well.

That’s right Petr. It’s the ol’ “Bad News is Good News” and the Fed speaks today.

You are right. And I do think that the road ahead is now open to MA200 = 3006. (SPX).

Given that stocks are a risk-free investment, why is there such a thing as an equity risk premium? Trade wars, recessions, pandemics, negative oil – all that is apparently meaningless for the stock market. So why do we even calculate things like P/E ratios? Should we be rethinking our traditional valuation models? Yes, we are getting close to the “new paradigm” phase.

Hi Jan, new paradigm name for stock would be casino entry ticket?

It’s not a casino if you can’t lose money. There may be bear markets for individual stocks, but for the entire market apparently not.

I’ve seen a lot of talk of retail investors piling in: Record new accounts at E-trade, TDA, Robinhood, Schwab. Record trading activity, inflows to firms & ETFs. Lots of people home with time to watch stocks.

Doesn’t seem to be much of a factor compared to a 25% one month rally. Just the sell side selling?

Retail flows are just a drop in the bucket compared to institutions. However, many retail traders are trading the tape like its the gambling salon.

In Cam’s 4/26 report, institutions are still defensively positioned, which represents most of the liquidity in the market.

Germany is starting to lock-down again after they opened the economy a little. Their Coronavirus (CV) infection rate is starting to climb again. But I don’t see the DAX reacting to this development.

Is the same thing going to happen in the U.S. as we start reopening in May? What are the odds infections will get worse again?

And, if we have to start closing again is this going to be the catalyst to send the market down for a retest?

I wonder about this here in Minneapolis, MN. Our numbers are 1/10th (per capita v. roughly) neighboring cities but we’ve been in “stay at home” for 7 weeks and due to expire in a week. Iowa, N & S Dakota, Nebraska haven’t and have much higher numbers. It’s gonna kill so many businesses. Ex: a survey said 50% of craft brewers here will close with 2 more weeks closed. I can’t see how cases don’t increase, perhaps dramatically. People can’t be bothered to wear masks (about 50% do) so great depression effects seem just a matter of time by lockdown or fear.

As for a the market down? It’s F-ing nuts. It may be making ATHs.

Yeah, what he said. (better put than me, and he’s a real virologist!)

Trevor Bedford, UW virology lab…

https://twitter.com/trvrb/status/1255976675252158465

Wally, I cannot confirm what you are saying about Germany. Not sure where you have been reading those reports.

The DAX has been underperforming so far and is trying to play catch-up the NDX and SPX, like small-caps, financials, energy and cyclicals in general.

Germany is taking small-steps opening up again, but there is no “lock-down again” so far. The infection rate climbing again was yesterday’s news, the market didn’t care.

We have a lot of data coming up, Fed, ECB, earnings and China PMIs – all those can be positive catalysts.

https://www.the-sun.com/news/753568/germany-bring-back-coronavirus-lockdowns-cases-surge/

Thanks for the link, the official numbers in Germany come with a delay of a few days, so we will see soon. Small retail shops have been allowed to open since Monday, the problem is that shoppers are still somewhat reluctant to spend.

Interesting times.

Christian Drosten who has become Germany’s most popular podcaster warns against reopening the country too soon.

https://www.sciencemag.org/news/2020/04/how-pandemic-made-virologist-unlikely-cult-figure?utm_campaign=news_daily_2020-04-29&et_rid=60658150&et_cid=3307615#

I think you may be right Wally about rising infection and re-closings being a catalyst. (whether by gov’t order or lack of business) When? idk but around a few weeks I would think. I see a lot of the medical/epi folks saying this.

I’m surprised the market is acting a little negatively to the Fed announcement. Maybe it is that $6.5 Trillion balance sheet they have now.