In the wake of my last post about whether USD assets and Treasury paper would remain safe haven and diversifiers in the next global downturn (see Will diversified portfolios be doomed in the next recession), I received a number of questions as to what investors should avoid. There is an obvious answer to that question.

Call them the new Fragile Five.

The pro-cyclical Fragile Five

Loomis Sayles made the case for these countries to be the New Fragile Five, based on unsustainable real estate bubbles:

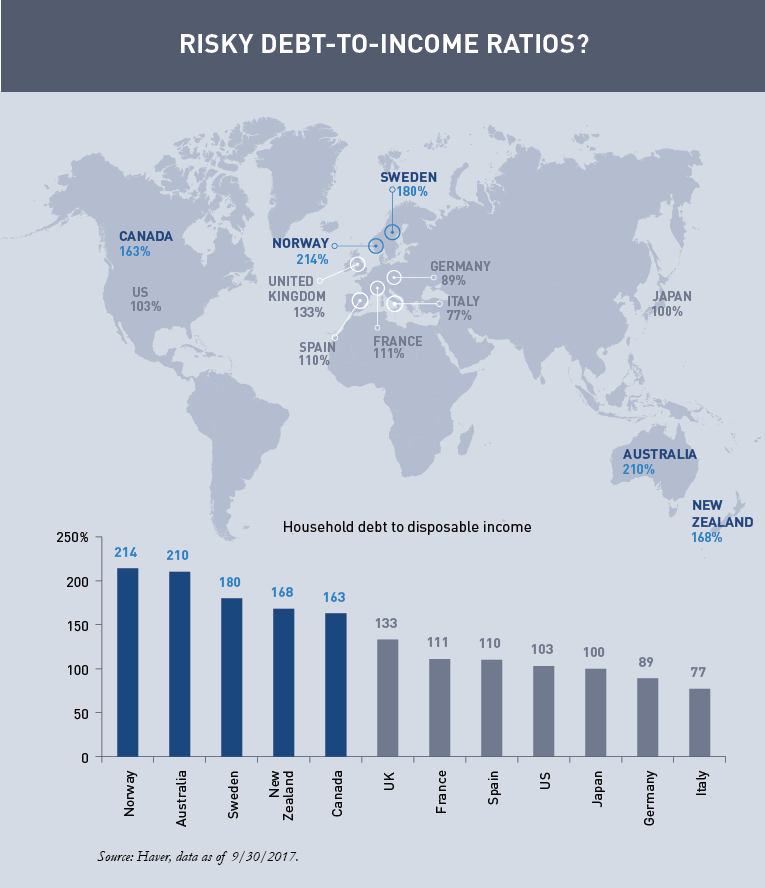

Cracks are starting to appear in five highly leveraged economies: Canada, Australia, Norway, Sweden and New Zealand. For several years following the global financial crisis, these five countries all shared a common theme—a multi-year housing boom, fueled by low interest rates, which resulted in very elevated levels of household debt.

This boom is starting to dissipate in all five markets. House prices have largely reversed course, be it slowing appreciation or outright decline. Moreover, this is occurring even as interest rates remain at or near record lows and labor markets continue to be robust. Importantly, this is a correction that many thought could not occur given the otherwise strong economic growth backdrop in these countries. But we take a long-term view of house prices, and began highlighting affordability problems in these markets several years ago.

Here in Vancouver, I can personally attest to the insanity of local property prices. As an example, here is the cheapest listing of a single detached house that I could find. You can have this beauty for about USD 1 million!

Oh, don`t miss the view from the back.

In addition to highly elevated property prices, the New Fragile Five also suffers from the doubly pro-cyclical characteristic of being resource based economies. If the Chinese economy were to slow significantly, these economies would also be hurt by plunging commodity prices. As the chart below shows, these currencies are highly correlated to either oil prices. or the CRB Index, which are expected to fall in a pro-cyclical fashion during a global downturn.

Falling property price AND falling commodities in commodity sensitive economies? Ouch! As a Canadian resident, I will be maintaining a USD position in my portfolio for precautionary purposes.

Cam, my sympathies to you. You are always welcome to come to Georgia — it was a cool 58 degrees today and I will try to post a pic of my home which is around $300K. Only 3100 ‘ ft. We actually had a sprinkle of snow one day in Jan.

Cam given the outlook on housing what are your thoughts on the CDN banks? Thanks

Under those conditions, Canadian banks are likely highly vulnerable.

Is there an entity that underwrites Canadian mortgages?

Not sure what you mean by “underwrite” mortgages. There isn’t a large active secondary mortgage market in Canada in the same way as the US.

If you are looking for a way to short Canadian real estate, that’s not very easy either. Canadian mortgages with high leverage ratios are required to have mortgage insurance, but the vast majority of insurance is issued by the Canadian Mortgage and Housing Corporation (CMHC), which is owned by the Federal government.

Genworth (Ticker MIC) is the largest private mortgage insurer. The biggest subprime lender is Home Capital (HCG), which tanked last year but was rescued by Berkshire Hathaway.

For more insights, you might want to follow the following people on Twitter:

Ben Rabidoux @BenRabidoux

Marc Cohodes @AlderLaneeggs

Thanks. Yes, shorting the counterpart risk holders like an underwriter (insurer) that is exposed to such risks is what I was alluding to. There is probably more than one (tortuous) way to achieve the same goal. Doing this based on Canadian housing may not be easy as you have quoted. That said, some of the smaller markets/countries like say New Zealand, may be a better shorting opportunity at some point. Thanks for the twitter feeds.