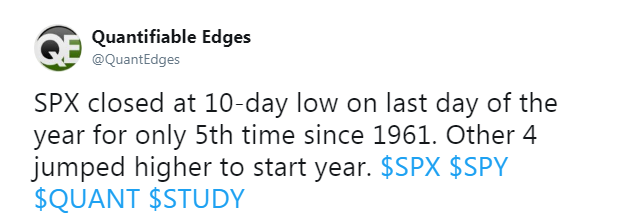

Mid-week market update: The stock market began the year by roaring out of the gate. This was not a big surprise. Rob Hanna at Quantifiable Edges tweeted on New Year’s Eve that the market has rallied strongly when it closed at a 10-day low at the end of the year.

Though the sample size is small (N=4), past episodes has been stock prices advance for a minimum of four consecutive days before pausing.

Hanna followed that tweet with a post which observed that positive momentum on the first day of the year usually leads to follow through for the next two days (which would be tomorrow, or Thursday).

Another bullish seasonal sign come from Jeff Hirsch of Trader`s Almanac.

The first indicator to register a reading in January is the Santa Claus Rally. The seven-trading day period begins on the open on December 22 and ends with the close of trading on January 3. Normally, the SP 500 posts an average gain of 1.3%. The failure of stocks to rally during this time tends to precede bear markets or times when stocks could be purchased at lower prices later in the year.

The SPX returned 1.1% during the seven-day period, which is positive but below average. This is a preliminary sign which should be enough to get traders and investors excited about 2018.

What happens now? Can equities continue to rise after these seasonal tailwinds?

Frothy sentiment

In the short run, sentiment is getting frothy. The CBOE equity put/call ratio (CPCE) closed at an astoundingly low 0.47 reading yesterday. As of this writing, the interim estimate is 0.75. In the last 10 years, CPCE has fallen below 0.50 only four times. Past returns have been mixed, as the market weakened shortly after these readings in two instances, and continued to advance in two others, though the cases where the market rose were clustered together.

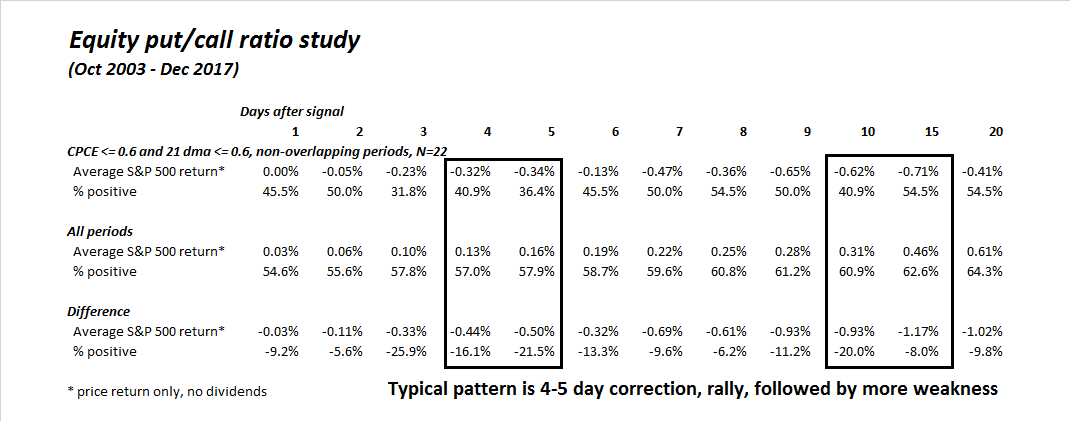

There were very few historical episodes where CPCE saw such low readings. I went back to 2003, where the CPCE data set began, and looked for cases where both CPCE and the 10 day moving average of CPCE fell below 0.60. If history is any guide, the market weakened for 4-5 trading days, rallied, and then fell further with a bottom in the 10-15 day time frame.

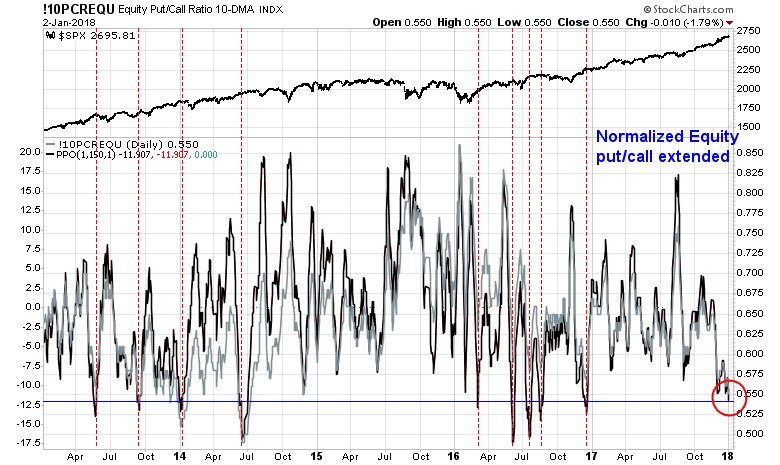

Normalized CPCE is showing a similar level of complacency. Even though these readings do not guarantee a correction, past episodes has seen the market struggle to advance.

SentimenTrader came to a similar conclusion as my analysis of option sentiment.

The VIX term structure is another way of analyzing option sentiment. Readings are also at extreme levels indicating greed. In the past, the market has encountered difficulty from these term structure levels.

In conclusion, option sentiment can only be described as frothy.

Negative divergences

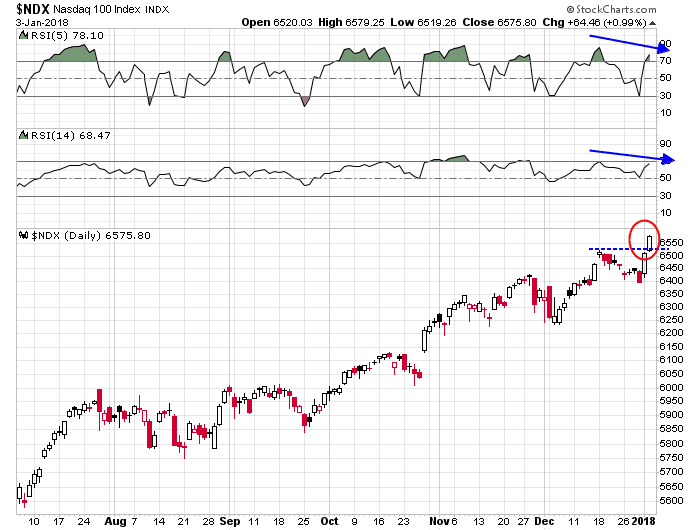

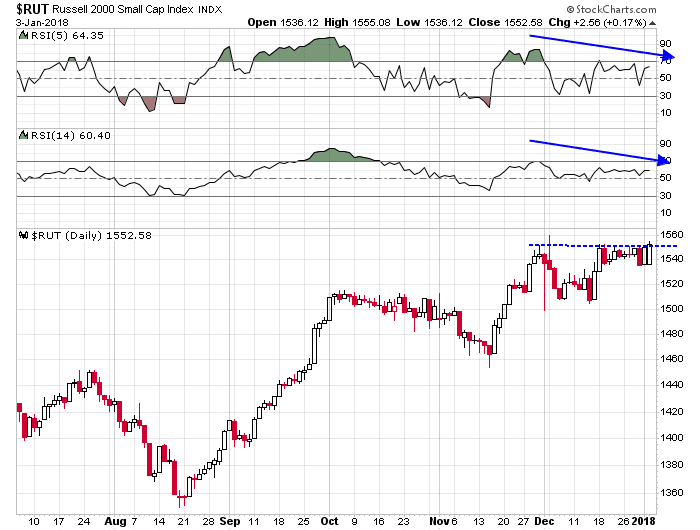

Another disturbing signs for the bulls is the appearance of negative divergences in both 5 and 14 day RSI as the market rallies to fresh highs.

These negative divergence can also been seen in the NASDAQ 100…

…and the small cap Russell 2000.

Pay attention to risk management

What does this mean? Is the market about to correct?

The experience in 2017 showed that we are in a momentum dominated environment. Despite these technical and sentiment warnings, it may not be prudent to go short without some visible sign of a downside break. On the other hand, traders who are long may wish to pay close attention to risk management. Either tighten up on your stops, or pay attention to factor behavior.

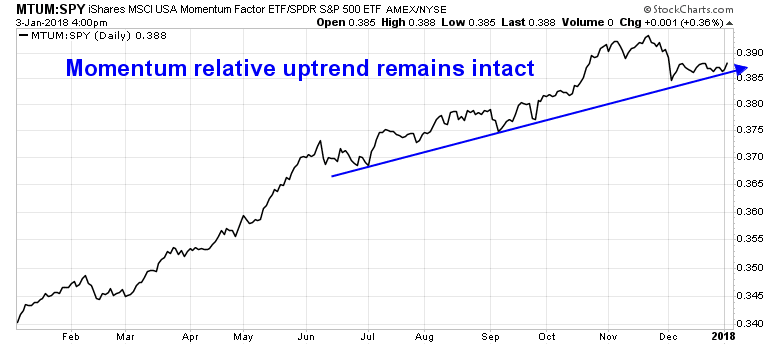

As long as price momentum remains in a relative uptrend, which it is…

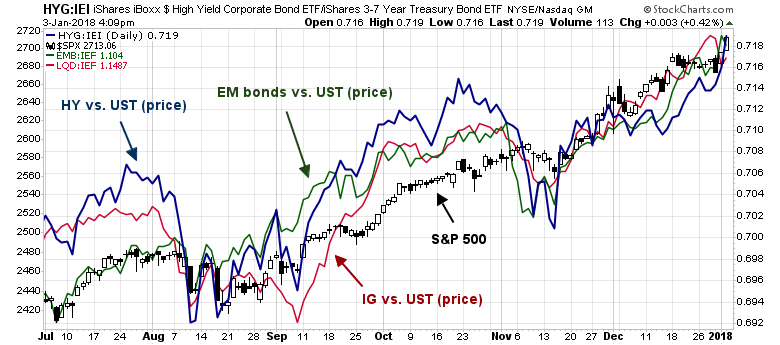

And credit market risk appetite remains healthy, which it is…

Any weakness is likely to resolve itself with either a sideways consolidation, or shallow correction.

My inner trader is long the market, but he may lighten up his positions should stock prices continue to rally into the weekend. As ever, he remains “data dependent”.

Disclosure: Long SPXL

Questions:

The market has a rhythm, as reflected in the MACD. If Christmas happens to be on a MACD rising phase, we get the “Christmas Rally”, other times not so much. Over time, year-end may occur at the lower turn of the MACD cycle, as cited above, and we may see subsequent gains. Should we not rather just heed the MACD? Is there perhaps some effect that tries to align the market and MACD with Christmas?

The RSI is a momentum indicator, with some EMA built in. If the slope of the (S&P500) chart moderates, the RSI will drop towards the middle of the range. The chart trends up, the RSI goes down, we have a divergence. Are we not making too much of divergences, when to the eye the slope is maintained and still probably greater than earlier in 2017? (The discrepancy is an artefact of the EMA requiring more samples.)

Different models for different styles:

MACD is a trend following model. Trend following models will not get you out at the top, nor will they get you in at the bottom.

RSI is a momentum and OBOS model, designed to spot OB and OS conditions. As well, they are designed to spot changes in momentum. That said, overbought markets can get more overbought and oversold models can get more oversold.

Nothing is perfect.