Japan saved the world in the aftermath of the Crash of 1987. When the panic selling of stocks cascaded around the world, the Nikkei Index bent, but did not break (via the FT):

The Nikkei tumbled 15 per cent on its “Black Tuesday” in the wake of Wall Street’s violent collapse and lost a further 5 per cent before global markets regained their feet in mid-November.

Yet, even though the crash knocked $500bn off corporate Japan’s market value, Tokyo’s fall was mild compared with those in the US, Europe and elsewhere in Asia – where some bourses plunged as much as 40 per cent. By the spring of 1988 the Nikkei was back up to a 15-year high, from which it would continue soaring for another 20 months.

“I don’t remember anybody in the office panicking,” Soichiro Monji says of the turbulent weeks that followed the October crash. Mr Monji, then a dealer at Daiwa Securities, Japan’s second-biggest brokerage house, now plans equity strategy at the group’s asset management arm.

“The economy was in good shape and the stock market had momentum. We thought, ‘There must be days like this sometimes’.”

Daiwa and Japan’s other big brokers were in any case sitting tight, having been ordered by their regulators in the Finance Ministry not to sell into the panic – an act of intervention that “would be inconceivable today”, notes Mr Monji.

Kiichi Miyazawa, the finance minister and later prime minister, who died earlier this year, told all who would listen that calm would soon return.

The government’s tactics helped stem the Nikkei’s fall, although a rosy growth outlook, low interest rates and a rising yen probably played a bigger role. The market’s structure helped: two-thirds of all company shares were held not by profit-seeking investors but by allied companies seeking to cement business ties.

In many ways, the panic was arrested in Japan and saved the world, but it paid a price later in that decade when the Japanese market collapsed and began the Lost Decades.

Fast forward to the Great Financial Crisis of 2008. The Chinese authorities ordered the banks to lend, and local authorities to spend. In many ways, China saved the world. As the American economy starts to show evidence of late cycle behavior, a recession is sure to follow some time in the future. Can China save the world again?

Vulnerable China

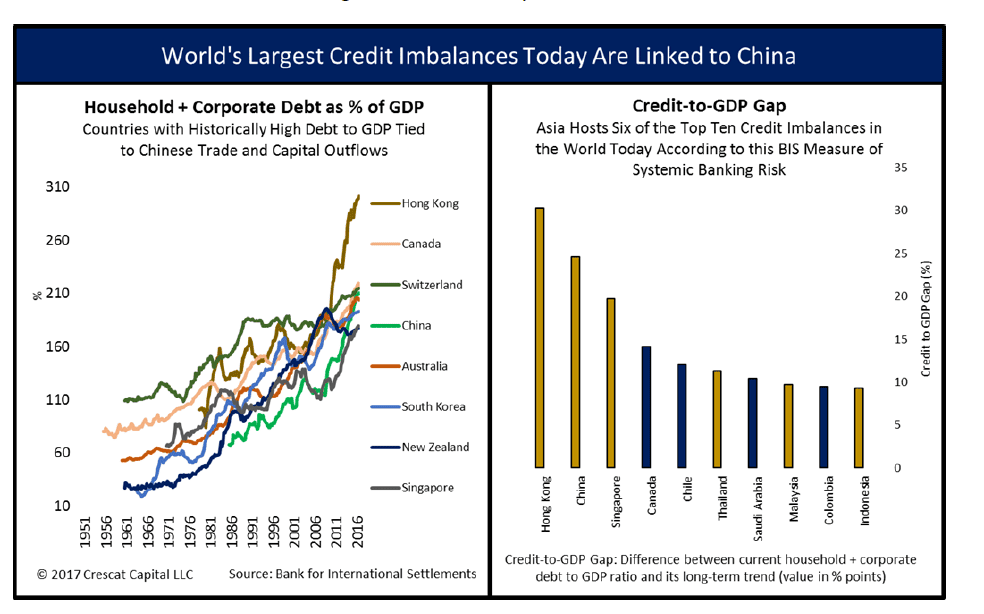

China today is vastly different from the China of 2008. This chart from Kevin Smith of Crestat shows how much more leverage there is in the Chinese financial system today compared to 2008.

The debt bubble is not only isolated just in China, but it has migrated to other countries.

Daniel Moss, writing at Bloomberg Views, recently asked the chilling question, “Global growth depends on China’s debt. Can it muddle through? The world should hope so.”

There are others ways that China is more vulnerable to a shock than it was in 2008. A SCMP article indicated that, despite the multi-decade boom and export miracle, Chinese firms operate on extremely thin margins, which makes them vulnerable to external shocks such as the global effects of rising US interest rates:

Chinese business owners say their profit margins have been “squeezed to the extreme” by rising rent and labour costs – and 80 per cent want taxes and levies cut to ease their burden.

That’s according to the results of a nationwide survey of 14,709 companies released on Tuesday, relating to the three years from 2014, by the Chinese Academy of Fiscal Sciences, a think tank affiliated with the Ministry of Finance.

Their sentiments reflect limited progress in the push to “cut costs for business” – one of the biggest economic goals under President Xi Jinping, along with reducing excess capacity and cutting debt levels.

Mitigating factors

Despite these concerns, there are a number of mitigating factors. First, most of the debt is held domestically, and therefore any crisis can be largely contained within Chinese borders. If there is a crisis, it won’t be your father’s emerging market debt crisis.

The latest update of Chinese GDP shows no signs of slowing growth. As well, Fathom Consulting’s projections of Q3 GDP shows a growth acceleration to levels well above the market consensus.

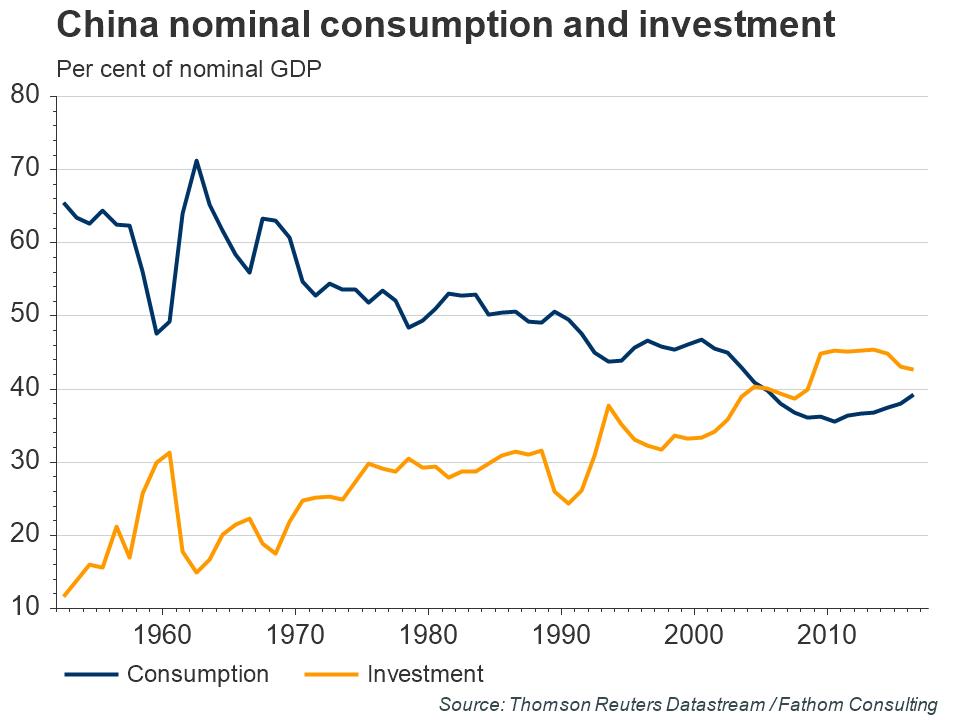

Moreover, China has been successfully rebalancing its economy, from credit driven infrastructure to a more sustainable domestic household driven growth.

As good as it gets?

That’s the good news. Here is the bad news. Business Insider reported that China analyst Charlene Chu is calling for a slowdown that begins late this year:

In her latest note to clients, she warns that the “Chinese medicine” that seems to be stabilizing the country’s financial sector for now — a “prescription of less excessive behaviour and a rebalancing of energy” — isn’t going to work forever

In fact she sees its usefulness fading fast. That’s because as this medicine takes effect, China’s monster credit machine must slow, and that will start to show in the economy as early as 2018.

“Our Autono credit impulse points to GDP growth peaking in 3Q17 at 10-10.5% (rolling 4-quarter yoy),” she wrote in her note.”This is a high figure, and there is room for deceleration before it starts to feel painful. We expect growth in 2018 will be under pressure, as a negative credit impulse by year-end begins to pass through to economic activity. Although new credit based on the official TSF has been strong this year, we are anticipating 12% less new credit in 2017 versus 2016 based on our Autono-adjusted TSF [total social financing].”

Expect that slow down to be felt the world over. China led the rebound in global banking activity in early 2017, according to recent data from the Bank of International Settlements, and without its demand global GDP will undoubtedly take a hit.

Instead of become a global savior, China is likely to be a drag on global growth in 2018. Analysis independent of Chu from Macrobond agrees with that assessment. Chinese credit growth is slowing, and it’s a leading indicator of GDP growth.

What deleveraging?

In the latest series of reforms, Beijing has made a lot of noise about creating sustainable growth through deleveraging. But Christopher Balding pointed out that while a lot of debt has been reshuffled around, there has been no actual deleveraging:

In reality, though, there’s been no deleveraging to speak of. New total social financing grew by 14.5 percent in the first half of 2017, up from 10.8 percent in the same period last year and rising roughly 3 percent faster than nominal gross domestic product. It’s true that measures such as credit intensity and the stock of total social financing to GDP have flattened or declined somewhat. But this was due to a temporary surge in commodity prices, now receding quickly.

China isn’t so much deleveraging as changing who borrows. Loans to non-financial corporations, for instance, have in fact been scaled back: They’re up a relatively modest 8 percent. But total loans to households are up 24 percent. “Portfolio investment” — code for bank holdings of wealth-management products — is up 18 percent. Combined, household debt and portfolio investment are now 13 percent larger than non-financial corporate debt, and growing by 20 percent on an annual basis. These aren’t small numbers.

Just as worrisome is where this debt is flowing. Wealth-management firms are routinely encouraged to push up commodity prices to drive growth. Total capital inflows from WMPs into commodities rose by 772 percent between January 2015 and June of this year. By tonnage, iron-ore futures trading on July 31 exceeded China’s entire iron-ore output for all of 2016. Given this flood of capital, it’s not surprising that iron-ore future prices are up 87 percent since December 2015. The government is trying to solve its overcapacity problem by having investors and banks prop up prices — even if output and consumption are stable or declining. Relying on triple-digit gains in commodities isn’t a good way to promote stability or sustainable growth.

Another concern is that the mythically prudent Chinese household is no longer quite so prudent. Total household debt now exceeds 100 percent of income. Most of this debt is flowing into real estate. Although gains in so-called tier-one cities have subsided — from year-over-year increases of 30 percent in late 2016 to 10 percent now — prices in tier-three cities are stirring, up more than 8 percent from a year ago and still rising.

In other words, China is spreading the debt burden from corporations to households. Although this might forestall a domino effect should one of China’s big companies start teetering, it’s far from a long-term solution.

Balding’s concerns about rising household debt could be one way that China is kicking the can down the road. Andrew Brown of Shorevest Investment Partners, writing in SCMP, recently asked if the Chinese consumer market might become the next debt bubble:

The only segment left that is not over-leveraged is the Chinese consumer market. In fact, household leverage is extremely low. Household debt-to-GDP ratio is only 40 per cent, among the lowest in the world. For comparison, the US is at 79 per cent while Australia is at 124 per cent.

The consumer market has the capacity to service higher debt. Household debt-to-disposable income is 56 per cent, which is also among the lowest in the world. For context, the US peaked at 123 per cent, and Australia is now at a worrying 168 per cent.

China could double its household debt ratios and still be “average” in a global context. Admittedly, this is a multi-year process, but with an US$11 trillion economy, this implies an additional US$4 trillion in purchasing power in today’s terms.

This is a staggering number and has powerful global implications. For context, the fourth-largest economy in the world is Germany with a GDP of US$3.5 trillion.

We expect the initial mode of consumer finance to be point-of-sale vendor financing, rather than a rapid increase in residential mortgages, given the concerning rise in residential property prices.As such, the biggest near-term beneficiaries from a leveraged consumption boom are likely the providers of this credit in the form of consumer credit companies, and the providers of “white goods” such as household appliances and consumer electronics, as well as the entire global supply chain to manufacture these products.

Other areas will include education, travel and leisure, cosmetics, etc. The providers of consumer data analytics will be in high demand to develop infrastructure.

Over the medium term, this should be good for the stock market, as same-store sales growth begins to accelerate at consumption-related companies, and then financial intermediaries such as brokers and asset managers will benefit as the positive wealth effect kicks in.

Could this be how China saves the world in the next global downturn? The Chinese consumer steps into the breach?

What rebalancing?

While that scenario is within the realm of possibility, implementation of such an initiative is far more difficult than the shock and awe stimulus in the wake of the Great Financial Crisis. In a command economy, Beijing could order government owned banks to lend, and local authorities to spend. It’s far more difficult to command individual consumers to spend. How do you enforce or incentivize such a edict to buy appliances, to travel, or to buy things?

Moreover, there are signs that much of the so-called rebalancing may be a mirage. Tom Orlik recently pointed out that Chinese infrastructure spending has rebounded to a post-crisis high. Is this what rebalancing looks like?

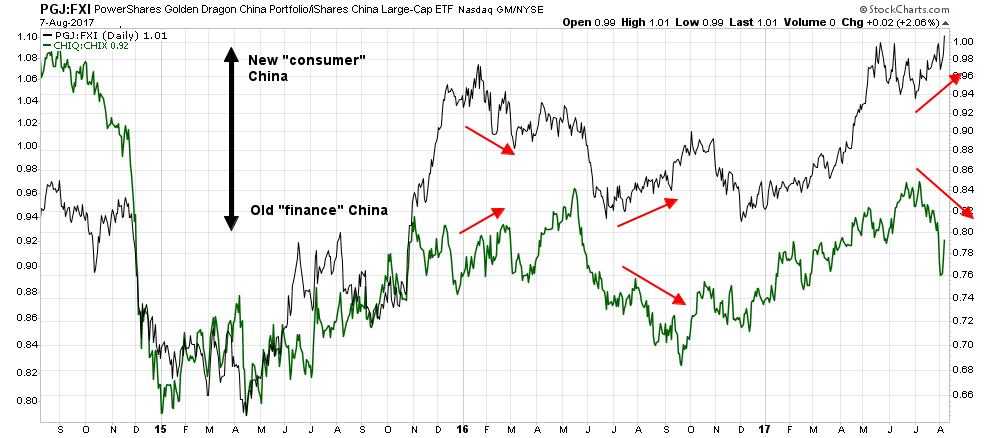

Tactically, a couple of pairs trades give us a real-time market based indication of how well the Chinese economy is rebalancing, and the verdict is decidedly mixed. The black line in the chart below shows a pair consisting a long position in the Golden Dragon China (PGJ), which is a tech heavy ETF with tilted towards the consumer such as Baidu and JD.com, and a short position in iShares China (FXI), which is heavily weighted in finance. The green line shows a pair with a long position in GlobalX China Consumer ETF (CHIQ) against a short position in GlobalX China Finance ETF (CHIX).

While these two pairs tend to move in lockstep, they have diverged recently. they have diverged recently. While these divergences have occurred in the past, I interpret these conditions as an uncertain verdict on how well the Chinese economy is rebalancing.

In short, China’s capacity to cushion the global effects of the next economic downturn has been greatly compromised by its debt expansion. While it is theoretically possible that the Chinese consumer could step up and “save the world” in the next recession, the chances of such a scenario is slim at best.

Cam

Thanks for posting graphs/charts on Chinese and non-Chinese global debt? How does one hedge against a melt down from such profligate debt? After all, a day of reckoning is coming, isn’t it?

The most obvious hedge against a Chinese downturn is US Treasury paper.

Having said that, it’s hard to know the timing of a Chinese implosion as it is becoming a short-JGB widowmaker trade. It will also depend on how a crisis, if and when it occurs, unfolds. The Chinese government has many levers to prevent a hard landing, but that doesn’t mean that they won’t pay the price in the form of extended soft Lost Decade like growth.