Mid-week market update: Markets behave different at tops and bottoms. Bottoms are often V-shaped and reflect panic. Tops are usually slower to develop. Hence the trader’s adage, “Take the stairs up, and escalator down.”

I have been writing that the US equity market appears to be extended short-term and ripe for a pullback, but that was last week and about 1% lower (see Why the S&P 500 won’t get to 2400 (in this rally)). I stand by those remarks.

I could say that the Fear and Greed Index appears to be extended and historically stock prices have had difficulty advancing further with readings at these levels.

I could also say that Ned Davis Research Crowd Sentiment Poll is also extended. Historically, stock prices have exhibited a negative bias at these levels (via Tiho Brkan).

None of this matters much to short-term traders. That’s because sentiment and overbought/oversold indicators are less useful at tops than bottoms. While it may be timely for traders to tilt to the long side when panic starts to appear, market euphoria are not good trading signals of market tops. Savvy traders know to wait for a bearish break when the market gets overbought and giddy.

I am seeing some limited signs of a bearish break, but the trading sell signal is incomplete.

CBOE put/call sell signal

I recently highlighted the euphoric condition where the CBOE equity-only put/call ratio (CPCE) had fallen to below 0.60 for four consecutive days. A study showed that such overbought conditions resulted in subpar returns, but they were still positive.

The same study showed that when the market becomes overbought and mean reverts, CPCE rises above 0.60, forward returns tend to far more negative. That`s the bearish break that traders should be waiting for.

The signal appeared as of Tuesday’s close, when CPCE rose to 0.61 and Wednesday’s preliminary equity put/call ratio came in at 0.82. Those are sell signals.

Still waiting for other breaks

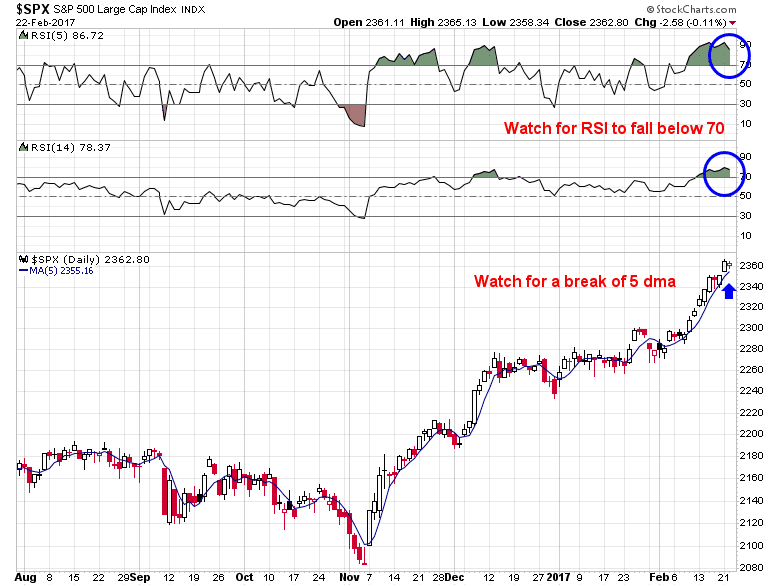

While the CPCE sell signal is encouraging for the bears, other short-term technical indicators have not flashed signals for my inner trader to commit funds to the short side. I am waiting for the SPX to fall below its 5 day moving average, which currently stands at about 2355. In addition, I am waiting for RSI-5 and RSI-14 to decline below 70 as signs of faltering momentum.

I would add that my cautiousness is tactical. Any pullback should be regarded as a correction within an uptrend unless proven otherwise.

My inner investor remains bullishly positioned. My inner trader is in cash, but he is waiting for a technical break to go short.

I am a student of behavioral economics. Michael Lewis’s latest book ‘The Undoing Project’ was a first-day purchase. So whenever my imagination dreams up new reasons to confirm my general beliefs, I am suspicious that my mind is doing a ‘confirmation bias’ trick.

With that preamble, let me outline a thought that is growing in my mind about the strange behavior of stock markets lately. Sentiment is acting very, very differently than normal. Sentimentrader.com has almost daily highlighted a wide variety of previously accurate sentiment studies that have said that markets should have peaked and fallen a month or two ago. And yet, the markets shrug off these warnings and march higher and higher with a dull consistency and lack of emotion. There are long stretches of positive days trading in an extremely narrow range. Is there something new afoot? Here is a possible answer.

To keep you in suspense just a bit longer, another preamble. I have studied momentum and think it works mainly because when a major change occurs, we humans take a long time to fully reflect the new fundamental values and then we overshoot. I’ve said that on the planet Vulcan of Star Trek, Mr. Spock fame, where the Vulcans have no emotions, Apple stock would have gone from $20 to $400 the day after they came out with the iPod and nobody would have batted an eye. We emotional humans take a huge length of time to get there.

So are there new unemotional forces acting on stock markets to befuddle us experienced observers? Yes.

The largest investment managers in the world are starting to use artificial intelligence. This is not the old quant black boxes. This the real thing, AI like IBM’s Watson. These are Mr. Spock-type unemotional agents. As they succeed, they will be used more. The owners will not announce what they’re doing or how much money is in play. Would you? We will have to detect their presence from market action. I feel it.

The other unemotional new force at play is the rise of ETFs. I use them more than any portfolio manager that I know. They allow for big, less emotional shifts in one’s portfolio at the press of a button. If I want to buy the airline industry after hearing Warren Buffett likes it, I buy the Airline ETF and use cash or the sale of another ETF to pay. In the past, I would have had to sell individual stocks I owned, each with its old, comfortable narrative and then look to buy individual airline stocks, each with an emotional, preconceived notion in my mind. In other words, a sentiment mess that could stop or slow my decision. An ETF is just a name that represents a logical industry, a style or a country. Buying and selling is tremendously less emotional.

It’s so easy to jump on the Trump favored industries now with ETFs. Investors just think, hell Trump will be great for banks, I’ll buy the Bank ETF. In the old days, the same person would be examining the individual bank stocks and find the PE is high and research reports on the banks show they are trading over the analyst’s target price. The decision to buy grinds to a halt or if the investor buys, they are scared holders who may bail if the stock falls a bit. ETF market = cool-headed big picture logic Old individual stocks market = Emotional swings.

A big ETF fresh buying push to the markets is likely individual investors switching from cash or fixed income to the general stock market index ETFs to take advantage of the “Trump Make America Great Bull Market”. Once again, buying an S&P 500 ETF is an unemotional way to dive in. There has been a huge flow of net money into ETFs since the presidential election.

Live long and Prosper

@Ken Interesting point of view and a joy to read. Your point on the ETFs having that effect on the market is very intuitive but AI wise I don’t think they’re close to Spock’s level yet and the potential career risk of being the only few Spocks in the market. There’s no precedence like Trump before in addition to the coinciding new market highs things might be different this time. Would love to see some market stats study on new highs. We’ll have to see if the difference from the norm is significant this time.

Is this finally what we have been waiting for: “THIS TIME IT IS DIFFERENT”. I guess only time will tell.

What is really different this time, is that we have been able to get through earnings season without the usual pre-earnings sell-off that have been kind of predictable in 2015 and 2016. My most important tool for timing the market is earnings season, individual stocks are most vulnerable during the pre-earnings quiet period and fear of negative pre-announcements have lead to market downturns shortly before earnings seasons in recent quarters. This time we had more of a sideway consolidation before earnings and when the reports came in that rally started this most recent leg up, I am also observing that the advance is slowing down, now that the most busy part of earnings season is behind us.

Maybe it is different this time and we will see market weakness followed by a rally into Q2 earnings, but for now I am not convinced that the market will turn short-term bearish (I see today only as a minor dip) with the good news from Q1 earnings fresh in memory and the risk of negative preannouncements far out in April.