I have tried to refrain from comment on the Brexit referendum vote until the situation had settled down a bit. Now that the campaign is in full swing, it`s time to consider how the markets might react as we approach the June 23 vote.

CNBC recently summarized the debate this way:

- First, the economy, and whether positives like free trade would exist outside of EU membership, and whether negatives like excess regulation would make a meaningful difference if removed.

- Second, migration of workers, and whether this helps offset Britain’s poor demographics, or acts as an excess strain on the welfare system.

- And third, sovereignty; is Britain ruled by the members of Parliament in Westminster elected last May by British voters, or by unelected bureaucrats in Brussels?

A probable roadmap

While I believe that the UK will ultimately vote to stay in the EU, there will many ups and downs to the debate. The addition of popular London mayor Boris Johnson to the Leave camp is undoubtedly providing a boost to the Leave vote.

Here is the likely roadmap of how opinions and the markets are likely to behave. Watch for the Leave side to gain the lead initially as Briton are guided by their hearts and emotions. As time progresses, “Project Panic” will kick in, just as it did during the Scottish Referendum (via Business Insider):

While few may be swayed by the lightly amended membership terms, a plunging currency, tumbling share prices and fears for property values could drive enough Britons to opt at the last minute for the status quo rather than a leap into the unknown.

That was how the British political establishment managed by the skin of its teeth to hold the United Kingdom together in 2014, when Scottish voters tempted by the centuries-old dream of regaining independence from England ultimately chose safety.

It is also a plausible scenario for the EU vote, especially since a decision to leave would reopen the Scottish question.

Ordinary Brits tempted to give the unloved “Europe” a kicking may plump for stability to avoid economic uncertainty rather than risk financial and political turmoil.

I also agree with Antole Kaletsky that UK citizens will ultimately vote to stay because of the enormous economic costs to the UK economy because of the loss of jobs in the services sector:

The economic challenges of Brexit would be overwhelming. The Out campaign’s main economic argument – that Britain’s huge trade deficit is a secret weapon, because the EU would have more to lose than Britain from a breakdown in trade relations – is flatly wrong. Britain would need to negotiate access to the European single market for its service industries, whereas EU manufacturers would automatically enjoy virtually unlimited rights to sell whatever they wanted in Britain under global World Trade Organization rules.

Margaret Thatcher was the first to realize that Britain’s specialization in services – not only finance, but also law, accountancy, media, architecture, pharmaceutical research and so on – makes membership in the EU single market critical. It makes little economic difference to Germany, France, or Italy whether Britain is an EU member or simply in the WTO.

Britain would therefore need an EU association agreement, similar to those negotiated with Switzerland or Norway, the only two significant European economies outside the EU. From the EU’s perspective, the terms of any British deal would have to be at least as stringent as those in the existing association agreements. To grant easier terms would immediately force matching concessions to Switzerland and Norway. Worse still, any special favors for Britain would set a precedent and tempt other lukewarm EU members to make exit threats and demand renegotiation.

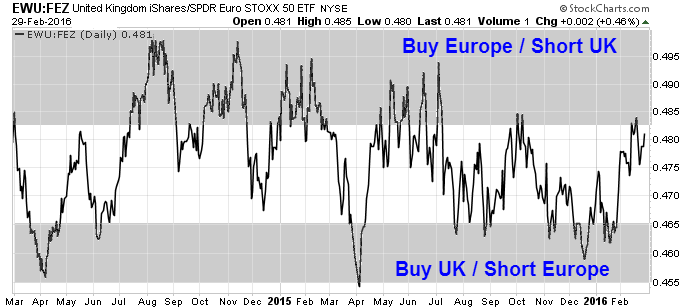

How to trade the vote

In effect, we will see a high level of market and public opinion volatility between now and June. The three likely phases are:

- Leave camp ascendant

- Market panic

- Last minute recovery for the Stay camp

I’ll bet the Scots are delighted and the English very sorry that the Scots chose to stay in the UK. The English economy massively subsidizes Scotland. Many Scots thought that with oil certain to stay above $100/barrel forever, they could live in the welfare state of their dreams all by themselves on oil royalties. Had they voted to leave, Scotland now would be running massive deficits, and its currency on its way to Venezuelan levels of collapse. So whether there is Brexit or not, the Scots will not bite the only hand feeding them anymore by bringing up independence again.

The UK is not subsidized by the EU. Quite the contrary. It would be much better off out of the EU, and the more that becomes likely, the stronger the pound will get versus the Euro, which will disintegrate thereafter. That is my current guess, anyway, but of course how this turns out will depend on decisions yet to be made.

Dear Rick,

I come from Czechoslovakia, that country was split into two states in 1993. There was a saying that Czech land is a locomotive and Slovakia is a vagon (Czech Rep subsidized the Slovak one) :-). After the split Czech economy really grows more then Slovak one, but after the entry EU (2004) this effect slowly disappeared.

My point of view is that such a notion that someone subsidize someone else is difficult to measure, because you have effect of bigger market 1+1=3 (not 2) :-). But in some cases split is inevitable if the nationalism is stronger than common sense.

In case of Brexit the smaller country (UK) will suffer more. Like Slovakia in case of Czechoslovakia. But in the longer term the UK can find much better deal to manage partnership with Commonwealth / former Commonwealth countries like Canada, US, India, … In my view EU is tailored for German companies that exported the goods to other EU countries and all the Brussels “administration” invent directives that conserves status quo in EU. As a result we (in EU) has higher cost of electricity (subsidized “green” energy), higher cost of labor (due to high social+medicare tax), inefective investments (your municipality build something (swimming pool, theater, etc. just because 75% of the investment will be funded from EU funds :-)). Therefore I agree with Brits that EU needs profound reform and I will understand them if they decide to leave. On the other hand the UK is not financing EU much – they have all possible exceptions.

Cam, in my view the bet on/against Brexit is interesting idea but to be honest I will most probably stay on sidelines.

Thank you for valuable article.

Petr

There is also the small matter of the democratic deficit. As it stands the Eurozone has a built-in majority on qualified majority voting and can in effect outvote non-EZ countries in nearly all matters. This explains the total loss of influence the UK has in legislative matters. But I guess nobody in the UK cares that much about this otherwise we would have rejected the Lisbon treaty like other countries. Oh, I forgot. We weren’t asked.

Bottom line from an investment standpoint is that an exit will not cause a recession in the U.S. Business generally around the world will continue with little or no effect. The media can hype some volatility for a month on either side of the event and then we will move on as if nothing happened.