As 2015 draws to a close, this would be a good time to review how I did during the year. As regular readers know, I have two personas, my inner investor and my inner trader. My inner investor had a decent year, while my inner trader had a year that he would rather forget.

What went right

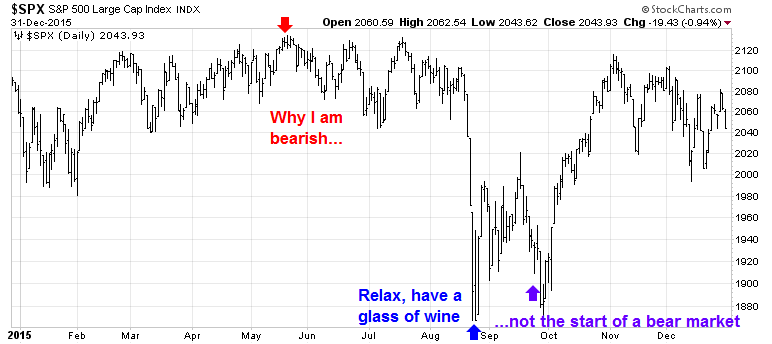

First the good news, I was mostly correct in calling both the top and the bottom in 2015. I was cautious in the spring. My bearishness was contrarian enough that I got a ton of hate mail. In response, I wrote a post entitled Why I am bearish (and what would change my mind) in May 2015 (red arrow below).

As the stock market weakened in August, my fundamental models identified the episode as a correction and not the start of a bear market, which was contrary to the atmosphere of panic at the time. See Relax, have a glass of wine (blue arrow below) and Why this is not the start of a bear market (purple arrow below). All turned out to be prescient calls.

What went wrong

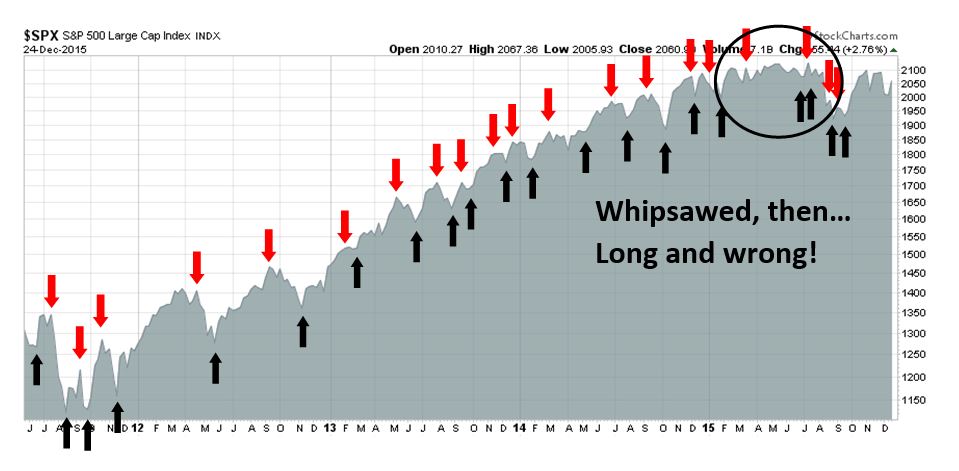

By contrast, 2015 was a difficult year for my inner trader, who used the trading model of my Trend Model. To explain, the Trend Model applies trend following principles to global equity and commodity prices to arrive at a risk-on (buy) or risk-off (sell) signal on US equities. Further, I found that changes in Trend Model readings, e.g. a “buy” signal getting less strong or a “sell” signal getting less weak, can identify short-term market turning points – and that formed the main basis for the trading model. In addition, I supplement trading model signals with overbought-oversold and sentiment indicators to spot market extremes.

The chart below of past trading model signals shows the limitations of this approach. When the market is trending, the trading model had superb results. In a sideways choppy market, trend following models get whipsawed, as it did during the summer of 2015. Worse was the behavior of the trading model during the August sell-off. Despite my general bearishness throughout the summer, sentiment models moved to a crowded short reading in the initial phase of the decline. As a consequence, my inner trader was “long and wrong” during this period.

To be sure, my inner trader did spot the Zweig Breadth Thrust and correctly bought into the subsequent rally (see Bingo! We have a buy signal!). However, those gains weren’t enough to offset the damage caused by the combination of the summer market whipsaws and being “long and wrong” during the August sell-off.

Lessons learned

As a result, both my inner investor and inner trader learned some valuable lessons in 2015.

My inner investor learned that once you have constructed a well thought out macro case for taking a position, the amount of pushback and hate mail can be a positive contrarian sign that you are likely correct, though early in your analysis.

My inner trader learned that not all models work all the time. He learned that all models have limitations. Trend following models are known to perform poorly during sideways markets like the summer of 2015. Moreover, overbought-oversold models identify market extremes, but overbought markets can get more overbought and oversold markets can get even more oversold. My inner trader learned both those lessons in 2015.

Both learned the valuable lesson of model diversification in portfolio construction.

What was happening in the summer was the start of a new phenomena; market sector economic discord. Heathy sectors of the US economy were doing fine while those in recession (commodities in particular) were falling. Bull and bear markets simultaneously. The general market just seemed to levitate along sideways as groups went VERY different ways. The harmonic discord was unlike anything I’ve seen. Playing THE MARKET using a previous successful Fourier analysis style when the underlying waves are out of tune became random.

I have come to believe that tracking THE MARKET the way we experienced players used to, will just frustrate for the next few years. I will track sectors. They will have their more predictable industry specific technical chart patterns and very differing and surprising fundamental trends.

Previous post discussion about breadth, and Ken’s comment about discord connect with John Hussman’s big learning point: these are indicators of risk aversion (together with increasing spreads.) When overvaluation and hubris meet risk aversion, markets are most dangerous (his opinion of the current state.)

Someone please construct an index for this!

It seems to me that your inner investor will in general do better than your inner trader. The Inner Investor sees the big picture more accurately and is therefore more likely to be correct. Getting out early after a gain is no sin, not really an error in the strict sense. Finding the best places to invest and above all avoiding the most vulnerable is the hardest and most important work in investing. In 2015 the majority of stocks either do not very well or were in serious bear mode. Hence the S&P went nowhere. Robert

Congrats on your inner investors calls. How could they have been better?

I have parsed your “Groundhog Day” post of August 16, as I think this where you may wish you had a do over. I suggest you avail yourself of the Rydex Ratio, the ratio of total money actually invested in long market positions in the Rydex funds to that invested in short positions. This ratio is devoid of what people think and reflects what they are doing with their money. They can (and do) shift from one fund to another daily.

Had you looked at this, I doubt that you would have concluded that the short position was crowded. This is not in any way intended to be critical, as I guess we are all here to learn, and in that spirit, I hope this helps.

I would give you a URL for Rydex if I had one (I think Stockcharts follows this), but I get my information from a subscription service. You will probably need to detrend the data (I suggest comparing 3 weeks to 39 weeks) as the total in the funds can vary substantially and of course the majority is always on the long side.