Is good economic news good news for equities or bad news? We know how to interpret macro news for the bond market. The Citi Economic Surprise Index (ESI), which measures whether top-down economic releases are beating or missing expectations, has been a bit weak. Historically, a weak ESI has meant lower bond yields.

What does it mean for equities? Investors saw a string of weaker-than-expected macro prints last week, starting with an anemic ISM PMI on Monday, followed by a miss on job openings in JOLTS Tuesday and another miss on ADP employment Wednesday. In each of those cases, bond prices rallied and equities initially weakened, followed by price recoveries later in the day.

I interpret events from the perspective of three trading desks: bonds, commodities and equities.

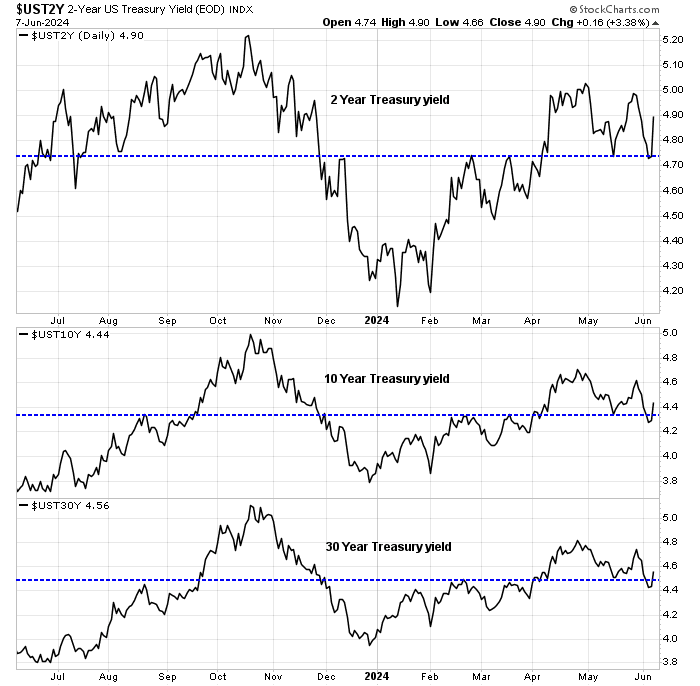

The bond market reaction

The closely watched employment picture is showing mixed signals. Fed Chair Jerome Powell has cited the number of job openings per available worker as an indicator of labour market tightness. The April JOLTS report shows that this metric has normalized back to pre-pandemic levels.

Even though the headline nonfarm payroll establishment survey and average hourly earnings release surprised to the upside, the noisy household survey was deeply negative and the unemployment rate actually rose. As well, the quits to layoffs ratio, which is a leading indicator of nonfarm payroll employment, has flatlined since last summer, with the caveat that this is a noisy data series.

How should investors interpret this data? For now, the consensus view is mildly dovish. Fed Funds market expectations calls for the first cut expected at the September FOMC meeting and almost a coin flip as to whether we will see a second cut at the December meeting.

The commodity market reaction

Commodity prices have been either trading sideways or in decline, depending on what index you use. The headline commodity indices, which tend to be heavily weighted in energy because of their higher liquidity, have been falling in the wake of last week’s OPEC+ decision to gradually allow the potential return of OPEC barrels to production. The cyclically sensitive copper/gold and base metals/gold ratios are also pulling back after a surge during the April–May period.

Precious metal investors were blindsided when the PBOC announced that it had stopped buying gold after an 18-month stretch of accumulation.

However, investors may want to take the commodity desk’s view of cyclical weakness with a grain of salt. Commodity prices are undergoing a period of negative seasonality, which should end about mid or late July.

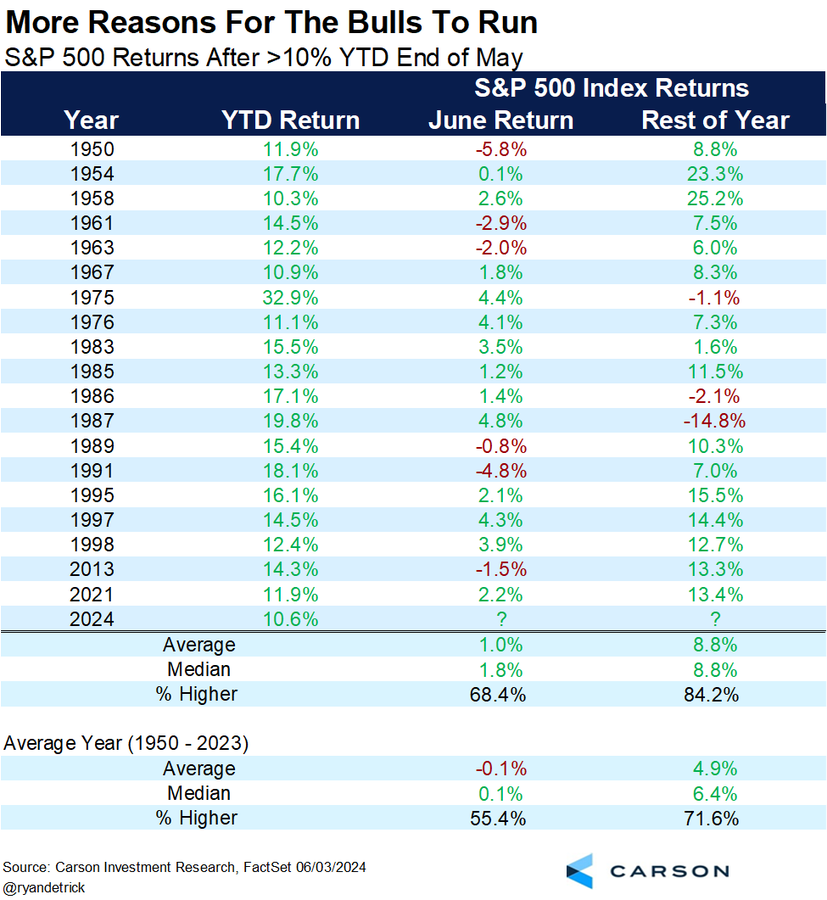

The equity market reaction

By contrast, the view from the equity desk is bullish.

Analysis from John Butters of FactSet confirms this view. S&P 500 EPS estimate revisions have been strong.

Moreover, references to the term “recession” on earnings calls are fading.

The market’s price momentum has been strong. Ryan Detrick pointed out that the historical evidence indicates that strong price gains tend to beget more price gains.

Growth deceleration or disinflation?

In summary, the bond and commodity markets are signaling weakness while equity markets are signaling growth. How should you reconcile these disparate views?

Your chart of job openings to workers ratio shows that we are at a higher level than for most of the time since 2000.

It could go back to historical norms.

It also shows it plateauing for a period pre-pandemic, which makes me wonder what would have happened had there been no pandemic with it’s accompanying massive stimulus.

But the ratio did decline for the bear of 2002 (Dotcom) and 2008 (GFC).

Will it continue in it’s decline?

What I like about large scale charts is the noise shows a lot less, but the flip side to that is that the noise is still there and hard to handle. To make matters worse, even on large scale charts there are trend changes, so how to know bad noise from a trend change?

Ten years from now the gold smash we got on Friday may barely show, like the ’87 flash crash barely shows, but anyone who bought gold Thursday is feeling it.

The S&P on a monthly chart is in an uptrend, but that does not mean it cannot get a 65% haircut.