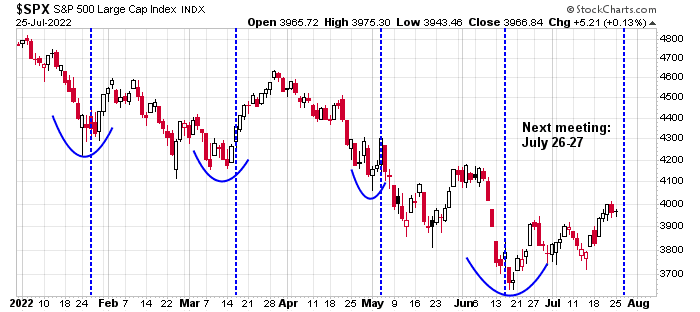

Anticipation is building over the FOMC decision, which is scheduled for this coming Wednesday. Leading up to the meeting, there had been growing speculation over whether the Fed would hike by 75 or 100 bps. Market expectations had been oscillating wildly, but it has now settled into a consensus of 75 bps, followed by a pause in late 2022 and rate cuts that begin in mid-2023.

In my opinion, 75 or 100 bps is the wrong question to ask.

Better questions to ask

The better questions for investors are:

- What’s the terminal rate?

- How long will the Fed pause?

- Most of all: Is the Fed willing to tolerate a recession?

As inflation indicators have been coming hot, or ahead of expectations, the Fed will undoubtedly employ tough hawkish language in its FOMC statement and subsequent press conference. A recent

speech by Fed governor Christopher Waller summarizes the Fed’s tough stance:

Congress did not say “Your goal is price stability unless inflation is caused by supply shocks, in which case you are off the hook.” We want to reduce excessive inflation, whatever the source, in part because whether it comes from supply or demand, high inflation can push up longer-run inflation expectations and thus affect spending and pricing decisions in the near term.

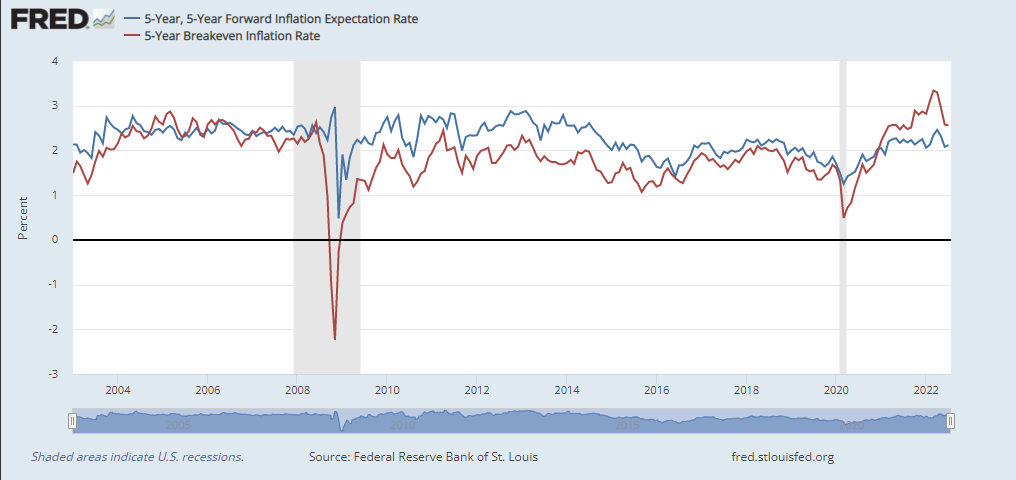

There are signs that inflation may be peaking. Both core CPI and core PCE, which is the Fed’s preferred policy metric, are rolling over. Investors will be scrutinizing the PCE announcement Friday. Market expectations call for stabilization in core PCE at 4.7%.

As well, inflation expectations are also under control.

Supply chain bottlenecks are beginning to ease, as evidenced by falling industrial prices in the G4.

Mentions of “shortage” in the Fed’s Beige Book have been trending down, indicating lower supply chain inflationary pressures.

While all of these signs are constructive, the

WSJ recently asked, “There Are Signs Inflation May Have Peaked, but Can It Come Down Fast Enough?” It’s a valid question. Ethan Harris at BoA pointed out that the market expects inflation to fall considerably over the next 12 to 24 months, but that isn’t how inflation (which is inertial) has historically behaved. What if inflation doesn’t tank? Are rate cut expectations all that realistic?

The policy conundrum

A recent

speech by Hyun Song Shin, Economic Adviser and Head of Research of the BIS, argued for front-loaded rate hikes because they were historically more likely to result in soft landings.

There are many ways of poking holes in the BIS study, mostly because the study period was concentrated in the inflationary 1970’s. A separate

paper by Luca Fornaro and Federica Romei argues that current policy has undesired recessionary effects from a global perspective.

During periods of global stagflation, central banks may tighten too much. The reason is that interest rate increases trigger exchange rate appreciations and trade deficits. While these two factors contain domestic inflation, they have the side effect of exporting inflation abroad. So when a central bank hikes, other central banks hike back to sustain their exchange rate and reduce imported inflation. As a result of this “competitive appreciations game”, interest rates end up being too high, and economic activity too low, compared to what would be optimal from a global perspective. There are thus gains from international monetary cooperation in times of high inflation.

In other words, while front-loading rate hikes may raise the odds of a soft landing, globally synchronized rate hikes have undesired recessionary effects. In all cases, it sounds like market expectations of rate cuts by mid-2023 are overly optimistic. Even if the economy were to plunge into recession, inflationary pressures may still be evident and not under control.

When does the Fed blink?

There is one exception to the anti-inflation fighting rule. The event that forces central bankers to spring into action and ease monetary policy is a financial crisis. It is said that the Fed will raise rates until something breaks. US corporate and household balance sheets are in strong positions this cycle and it’s unlikely anything will break, which argues for a continued hawkish Fed.

On the other hand, emerging market defaults have spiked to fresh highs, according to ASR Ltd., EM countries have been the canaries in the global financial coal mine in past cycles. However, ASR observed that contagion risk has been limited so far, “Default risk is mostly limited to smaller, less well-connected countries, limiting the spillover to the global economy. Turkey is the major exception.”

Nevertheless, hard currency EM debt issuance has now turned negative, which is a sign of a global credit crunch.

As the US PMI plunges into recession territory and the fragility of EMs becoming evident. While financial crises are by their nature discontinuous events and difficult to predict with any certainty, the markets are expecting a disorderly event by mid-2023. Will the Fed blink then?

Investment implications

Putting it all together, here is what this all means for investors. Economic data like Philly Fed, ISM, and PMI are all likely to be weak for the next few months. If there is even any hint of disinflationary tendencies, bond prices will rip, and yields tank.

In the past, peaks in long Treasury yields have preceded pauses in Fed Funds rate hikes by a few months. At a minimum, the market expectations of a pause by late 2022 should be correct. Keep an eye on the PCE report Friday.

Tactically, Rob Hanna at

Quantifiable Edges observed that FOMC days tend to be equity bullish if stocks decline into meeting days while confidence into meeting days has been disappointing.

Cam,

Reading your post and the WSJ article, I wonder if the right questions to ask are: (1) At what level of current inflation level and inflation trend will the Fed pause? (2) If the inflation does not come down sufficiently, what needs to break for the Fed to pivot? A severe recession in the US? Massive riots / social unrest / debt defaults in EM? Social unrest / riots in Europe as Putin continues to tighten gas flows with severe heat and winter approaching?

Anyways, here are things that stood out for me:

Ethan Harris of BofA: In our view, it is going to be extremely hard for the Fed to get inflation back to target in a two-year time space.

Inflation-based derivatives and bonds are projecting that the annual increase in the CPI will fall to 2.3% in just a year, around the Fed’s 2% target. “Optimistic but not totally implausible.”

Sarah House expects 4Q inflation between 7.5% and 7.8%.

In the past, peaks in long Treasury yields have preceded pauses in Fed Funds rate hikes by a few months. At a minimum, the market expectations of a pause by late 2022 should be correct.

====-===

Given the inflation is likely to remain elevated in 7-8.x range in 4Q, how can the Fed even think about thinking to pause by late 2022? This is not even accounting for possible commodity price shocks – an escalation of the Russia-Ukraine conflict, a hurricane that shuts down an oil refinery, or an outage at a key semiconductor or auto plant.

It seems more likely that the Fed will push the US into more than a mild recession, and break something either in EM or in W Europe.

There are two items left to determine the path: dwelling and salary/compensation. Other parameters are all in down trends. Unfortunately these two are very stubborn. Do you want to see them crash?

My wishes are totally immaterial. They don’t matter at all.

I’m just trying to figure out when the Fed will pause and/or pivot. If the inflation remains persistent like you and Ravindra say, at least in coming months, it is hard for me to see Powell pause or pivot unless there is a financial crisis.

Biden has declared that Fed is responsible for controlling inflation while Warren has declared that Fed will be held responsible for any recessions. So, why would Fed stop till there is compelling evidence that inflation is under control? Pedal to the metal.

Is Fed really concerned about Europe or EM? Only if it leads to financial instability. I think the bar is pretty high.

Tighten your seat belts for the resurgence of volatility.

As Cam mentioned above the emerging market defaults have already spiked to fresh highs. However, the affected EM countries are smallish with little linkage to the global economy.

Yup! The bar seems quite high for the Fed to pivot. The odds to revisit the lows or even make new lows seem substantial.

So far, Powell has been very Courageous in channeling Volcker. It is entirely possible he’s jawboning the market to submission to bring inflation under control.

Rising unemployment in the US or some signs of instability abroad, or just some pressure from fellow central bankers, he may start singing a mellower tune.

SPY hit my 390 limit order for a reentry – just a 20% allocation this time. I’m not inclined to add any further ahead of FOMC as it feels too much like a red or black bet. 80% cash feels right at this point.

Taking the position off after hours @ 392. Back to 100% cash.

https://www.blackrock.com/corporate/literature/whitepaper/bii-2022-midyear-global-outlook.pdf

This is well worth checking out. Blackrock expects inflation to continue and the Fed to accept a higher inflation rate.

Good reading! Thanks

Any bet(s) ahead of the FOMC leave me with the sense that one may be left regretting ‘if only I’d bet red.’

Why not wait for the announcement and then the fallout? Plenty of time to put money to work if the Fed pivots, and plenty of time to pick up the pieces if markets head south.

Very bullish for both equities and bonds (IMHO) if this transpires.

https://twitter.com/EconguyRosie/status/1551984838990876675

Watch the Fed abandon forward guidance and rate commitments and embrace data-dependency. This cycle of hikes ends at 2 pm tomorrow. Buy bonds.

Rosie was on target – at least partially with this.

It remains to be seen whether the cycle of hikes has ended.

Sounds like a potential pivot here. Long SPY.

Nice when you hit a pitch just right 😉

80% upside thus far.

It’d be nice to see higher volumes – although I suspect many traders are caught off guard.