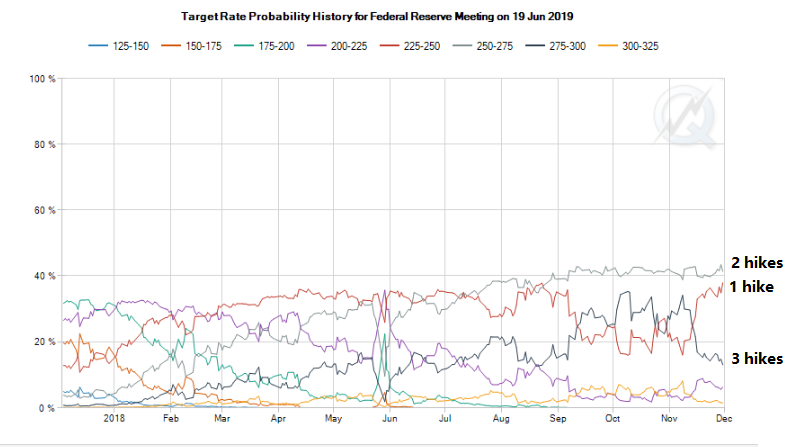

Mid-week market update: In the wake of the Powell speech last week and the FOMC minutes, the market implied odds of rate hikes have plunged. While the base case calls for two rate hikes by June, the odds of a once and done policy after a December hike is rapidly increasing, while the probability of three more hikes by June has plunged.

Curb your dovish enthusiasm.

The Fed is abandoning forward guidance

I believe the market is reacting erroneously to the Fed’s new policy of abandoning forward guidance. They simply are not going to tell you where they think rates are going anymore.

The initial reaction to Powell’s speech was the Fed Funds rate was just below neutral. What he really said was:

Interest rates are still low by historical standards, and they remain just below the broad range of estimates of the level that would be neutral for the economy‑‑that is, neither speeding up nor slowing down growth.

There is a huge difference between “just below neutral” and “just below the neutral range”. What Powell said is factually correct. The Fed Funds rate target is currently just below the neutral range of 2.5% to 3.5%. However, raising rates to the middle of the range would still involve three rate hikes, which is higher than the market consensus.

As the Powell Fed struggles with its communication policy, there is bound to be some market confusion. I would pay the most attention to speeches by the triumvirate of Powell, the chair, Clarida, the vice chair, and Williams, the New York Fed president, who are all permanent voters on the FOMC. Then focus on the speeches of other Fed governors, who are also permanent FOMC voters, and lastly the regional presidents, who all have influence on policy, but they do not have the same resources as the Fed governors.

Please be reminded of Fed governor Lael Brainard’s September speech, where she stated that there are actually two neutral rates. There is a long-term neutral rate, which is specified by the “dot plot”, and there is a short-term neutral rate that is more responsive to current market and economic conditions:

Focusing first on the “shorter-run” neutral rate, this does not stay fixed, but rather fluctuates along with important changes in economic conditions. For instance, legislation that increases the budget deficit through tax cuts and spending increases can be expected to generate tailwinds to domestic demand and thus to push up the shorter-run neutral interest rate. Heightened risk appetite among investors similarly can be expected to push up the shorter-run neutral rate. Conversely, many of the forces that contributed to the financial crisis–such as fear and uncertainty on the part of businesses and households–can be expected to lower the neutral rate of interest, as can declines in foreign demand for U.S. exports.

In many circumstances, monetary policy can help keep the economy on its sustainable path at full employment by adjusting the policy rate to reflect movements in the shorter-run neutral rate. In this context, the appropriate reference for assessing the stance of monetary policy is the gap between the policy rate and the nominal shorter-run neutral rate.

In other words, the short-term neutral rate can rise above the long-term neutral rate in a hot economy. Another demonstration of Brainard’s hawkish views can be found in her speech this week on Treasury market structure, she sneaked in the phrase “with the economy now at or beyond full employment and inflation around target”.

What data dependence really means

Fed watcher Tim Duy thinks that the Fed is now data dependent and anything can happen. Policy will evolve in accordance with how the data comes relative to the Fed’s own estimates, which calls for a slowdown in 2019 to 1.8% growth:

The Fed is data dependent. Growth will almost certainly slow in 2019. If it looks like to slow sufficiently to halt the slide in the unemployment rate while inflation remains low, the Fed will slow the pace of rate hikes. If unemployment continues to slide while inflation remains low, then the gradual pace of rates will continue longer. If unemployment slides and inflation ticks up, the Fed will probably hike a little faster.

Luke Kawa of Bloomberg thinks that the market should be prepared for a hawkish surprise [emphasis added]:

Minutes of the Federal Reserve’s November meeting, released Thursday, showed that optionality is the name of the game. The word “neutral” was mentioned only once, showing the shift in focus away from this unobservable measure for the benchmark rate. Moreover, the Fed is discussing whether to change language in the policy statement about the need for “further gradual” rate hikes. Even if Fed officials’ dot-plot projections might suggest more hikes, when it comes to the statement it doesn’t make sense specifying that expectation if policy makers want to give the impression their position is flexible, based on the evolution of data and financial conditions. The spread between Eurodollar futures expiring next month and those due a year later — a proxy for Fed rate hikes priced for 2019 — fell below 25 basis points. Another bit of compression and the gap will have gone back to pre-taper-tantrum levels. But the minutes also hint that market participants may have gone too far in betting that the 2019 dots won’t be realized. Only “a couple” of Fed officials think that the policy rate is currently close to neutral — so it’s not a consensus view that the level at which these central bankers might be inclined to consider a pause is just around the corner. As such, traders are either very stubbornly fighting the Fed or will be vindicated in December, should the central bank shift its dot plot towards the market-implied view. Whatever the case, there’s scarcely any more room to price-in a less aggressive Fed without starting to discount rate cuts. Some strategists and investors argue that this means a further dovish tilt might be received negatively by risk assets, as it would imply a meaningful deterioration in the economic outlook.

In this era of reduced guidance and data dependence, investors will be better served by monitoring the evolution of growth, inflation, and rate projections in the Summary of Economic Projections (SEP) released after each FOMC meeting.

A Jobs Report preview

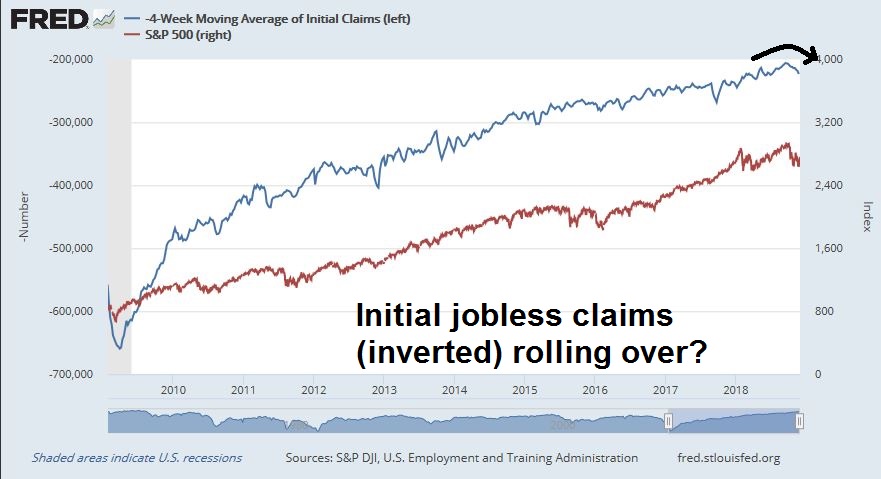

The yield curve has been flattening dramatically in the last few days, which is freaking the market out. The upcoming Jobs Report will represent a more sobering perspective and key input to Fed policy. Initial jobless claims have been weakening (blue line, inverted scale) for several weeks, and they have been inversely correlated to stock prices (red line). This trend represents a warning for investors of possible weakness in employment next year.

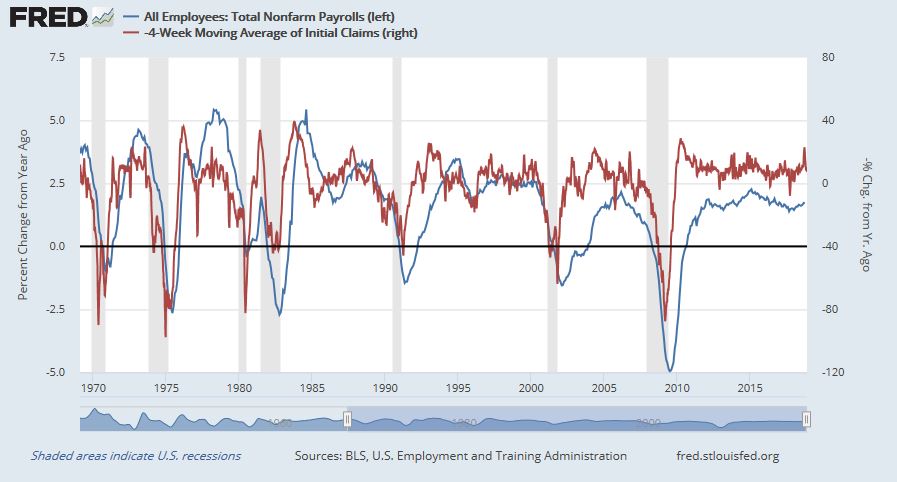

History shows that there is a strong but noisy correlation between the changes in initial claims (red line, inverted scale) and Non-Farm Payroll (blue line). However, initial claims data tends to be noisy. Moreover, weakness in initial claims has either been coincident with NFP weakness, or led NFP peaks by as much as a year.

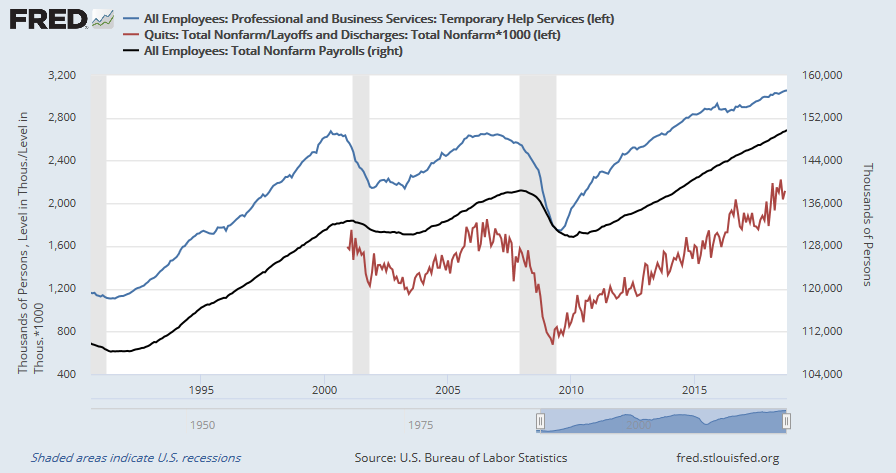

Will the NFP report disappoint? There are some reasons for optimism, growth in temporary employment and the quits to layoffs and discharges ratio has historically led NFP, and there has been no indication of weakness from those leading indicators.

Keep an open mind, but if NFP employment or Average Hourly Earnings were to come in above expectations, watch the market’s dovishness disappear like the morning mist.

For investors, the most important indicator will be the market reaction in the aftermath of the Jobs Report. Will the yield curve flatten further, or steepen? What will it tell us about the market’s growth expectations?

I have found many valuable clues in statements from the Bank of Canada in the past about global and North American macroeconomic directions. The BOC clearly communicates with the Fed and other global Central Bankers in forming their policy.

They have just made an extreme change in their outlook. Just six weeks ago, they were very hawkish in their statements. Canadian economists braced for rates in Canada to go up with American. That has now changed to a very dovish statement given with their policy decision today.

Today the Bank of Canada policy committee met and kept the official interest rate unchanged at 1.75%. Six weeks ago the said, “the global outlook remains solid” now they say “the global economic expansion is moderating”

They say now part of oil price weakness is due to “uncertainty about global growth forecasts.”

They go on to say, “… signs are emerging that trade conflicts are weighing more heavily on global demand.”

The futures markets in Canada for future rate hikes is falling just as they are in the U.S. for Fed rates.

I’d suggest listening to the BOC on global economic weakness in 2019.

Canadian GDP growth QoQ was 0.7% in Q2, vs 4.2% in the US.

Yes, there were Canadian economic forces at work that were mentioned in the press release that were a big bearing on the decision to not raise the Canadian official rate.

But I referred only to the international economic references here in the blog.

Huawei CFO arrested on Dec 1 in Canada for violating U.S. sanctions on Iran.

https://www.reuters.com/article/us-usa-china-huawei/huawei-cfo-arrested-in-canada-for-violating-u-s-sanctions-on-iran-report-idUSKBN1O42S1?il=0

This goes down in history as another chapter of the ‘you can’t make this stuff up’ with the Trump administration.

Just when trade negotiations were moving well, THIS?????

Some are suggesting that the CFO was arrested to scare US executives from visiting China and therefore investing in China (in long-term), and forcing them to relocate their supply chains out of China. That seems to align very well with the goals of hawkish elements in the Trump administration.

No wonder China sought to reassure US executives as concerns rise of retaliation over Huawei CFO’s arrest.

https://www.scmp.com/news/article/2176981/china-seeks-reassure-us-executives-concerns-rise-retaliation-over-huawei-cfos

It was probably a total independent action by the DoJ, just the timing turned out to be very bad. John Bolton was aware of this arrest while Trump may not have been.

I think we have to view the trade war from the perspective of the intersection of intellectual property theft and the development of artificial intelligence so scary, it’s clearly represented in our most frightening action movies. We simply cannot continue to allow China to force American companies working in China to turn over their intellectual property to them. Viewed through this lens, aggressive actions like arresting Meng could be viewed as constructive.

I’m not all in on that view, but I have read about Huawei networking devices having the capacity to spy on American conversations and data for the Chinese government. The problem with the hard line with China is the possibility of it escalating into a hot war, and I don’t understand the probabilities there. I just don’t want them stealing bat crap crazy robot tech from us, and I believe Trump will let some, if not all, of his demands on Chinese tariffs slide, if we get the intellectual property thing resolved, and then zoom, we’re bullish again.

Filled SPXU Buy 35.24 xx@ 35.2335 Day 12/03/2018 15:34:52

Filled SPXU Sell 41.24 xx @ 41.24 Day 12/06/2018 11:05:56

+17%

Covered most of the shorts earlier in the day. In recent weeks (10/29, 11/20, 11/23) if NYSE Above 200 DMA issues fell below 550, the buying comes back in. This morning it fell to a low of 515 for the first time since 11/23.

Cam, if some profits were taken on SPXU at lower levels should we be cautious following the large reversal today or should we prepare to reload for more downside?

I would watch Friday’s NFP report. If it comes in hot, we could see more downside.

The latest Beige Book report showed anecdotal evidence of a tightening labor market and likely rising wage pressures – so watch Average Hourly Earnings closely. There were reports of ghosting, where employees would just stop showing up without warning because they’ve gone elsewhere. This only happens in tight labor markets, which indicates that strong positive internals for wage pressure.

That said, short-term breadth is oversold, so I wouldn’t overstay a short position.

Cam, your thoughts on the short term breakout on the gold futures? if it’s short term bullish, buy the miners or the metal? The miners (gdxj) dont look quite right to me on the charts?

Thanks