Mid-week market update: Recently, there have been numerous data points indicating excessive bullishness from different segments of the market:

- Retail investors are all-in

- Institutional investor bullish sentiment is off the charts

- Cash is at a two-decade low in global investor portfolios

- RIA sentiment are at bullish extremes

- Hedge funds are in a crowded long in equities

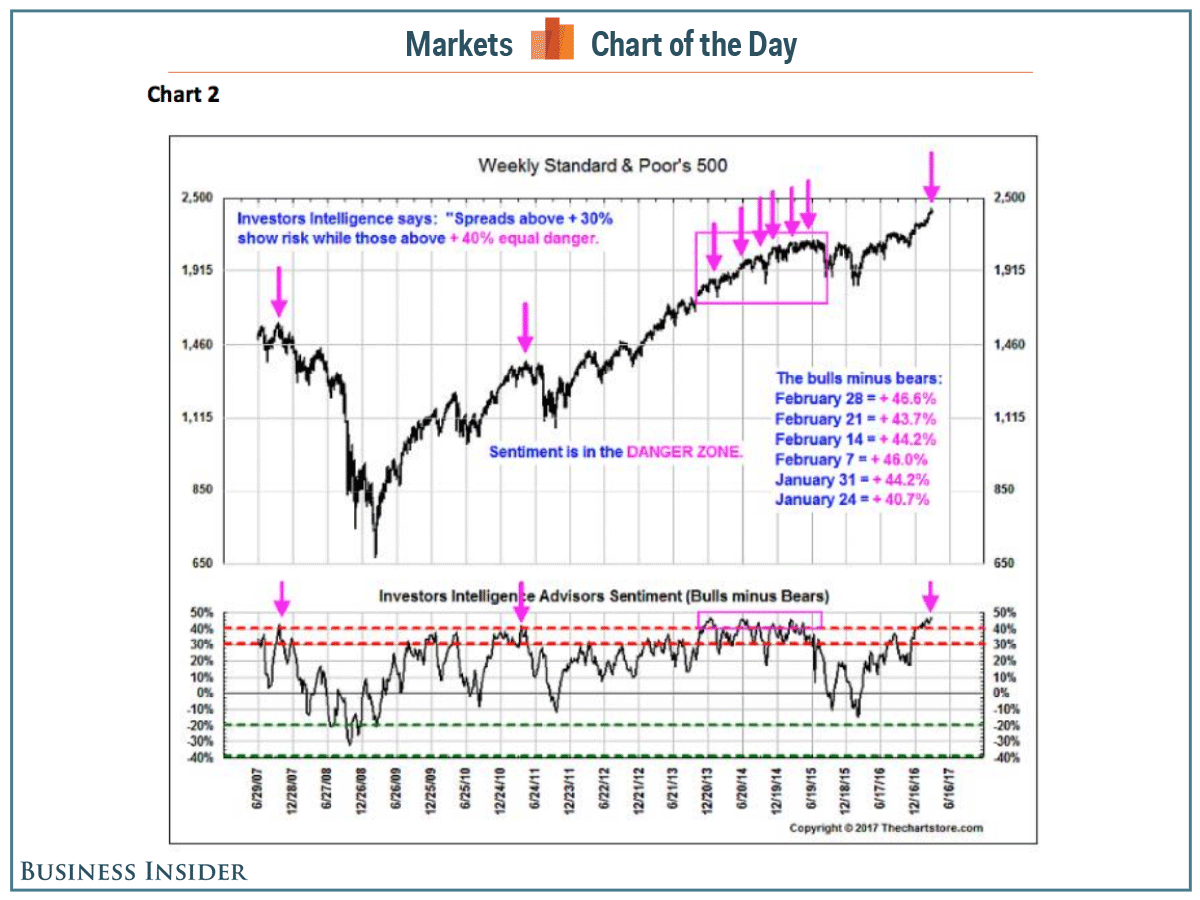

These giddy sentiment readings are comforting to the bear camp (chart via Business Insider) and it will be difficult for stock prices to advance under such conditions. When everyone is bullish, who is left to buy?

However, I would warn the bears that they should not go overboard and short the market with both hands. In the past, euphoric sentiment has not a good indicator for pinpointing market tops.

Too much bullishness

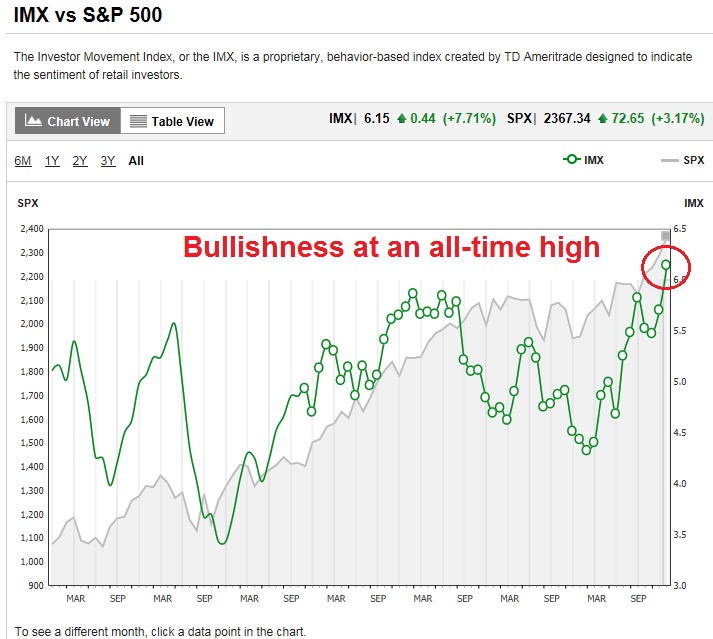

In the past few days, I have been surprised at the number of reports of excessively bullish sentiment. The latest readings from TD Ameritrade Investor Movement Index shows that retail investor bullishness at an all-time high (annotations in red are mine).

The Yale School of Management survey of investor confidence, which has been surveying investors for close to two decades, shows that both individual and institutional investor confidence have been surging. In particular, institutional confidence have risen to an all-time high.

Equally worrisome, Ned Davis Research found that cash is at historic lows in global portfolios (via Bloomberg):

Here’s another way of thinking about how far stocks have come in nine years. Relative to balances in money market funds and cash among mutual fund managers, the value of global equities is the highest in almost two decades.

That observation courtesy of Ned Davis Research, which framed the comparison as an indication “cash is underweight” in Planet Earth’s asset portfolio. Another way of describing it is that equities have risen so much from the depths of the financial crisis that their value is blotting out everything else to an extent not seen since the dot-com bubble…

In a Ned Davis calculation that treats the global investment portfolio as an amalgamation of stocks, bonds and cash, the latter now makes up about 17 percent of investor portfolios, less than half of its allocation in 2009 and close to the lowest since 1980. While bond holdings remained relatively steady over the same period, surging equity values pushed its share to about 60 percent, well above the long-term average.

As a sentiment gauge, the study is a distant relation of popular studies of investor and newsletter-writer optimism or even price-earnings ratios. In the options market right now, the CBOE Equity Put/Call Ratio fell to 0.53 last week, tied for the lowest since Dec. 9 and 20 percent below the measure’s one-year average.

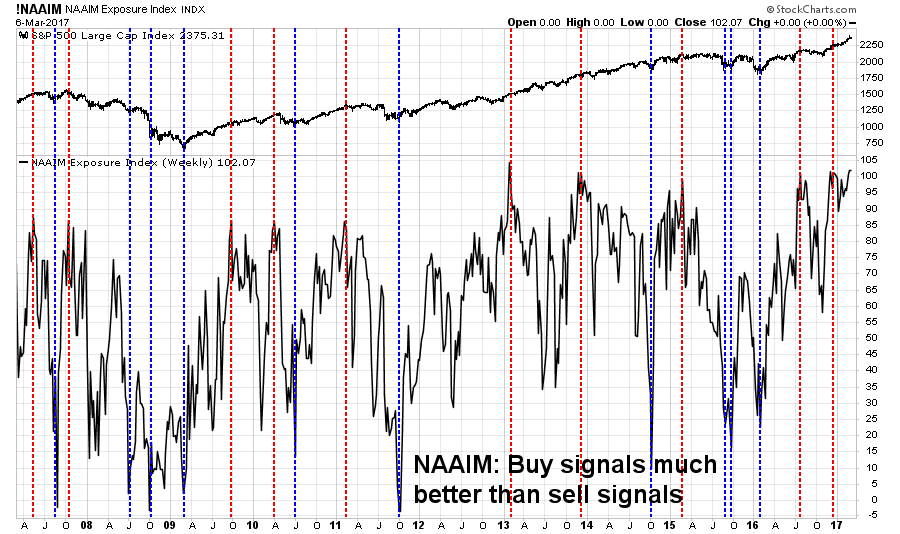

In addition, the latest NAAIM survey of RIAs, who manage the funds of individual investors, show sentiment to be at a bullish extreme (annotations in red are mine).

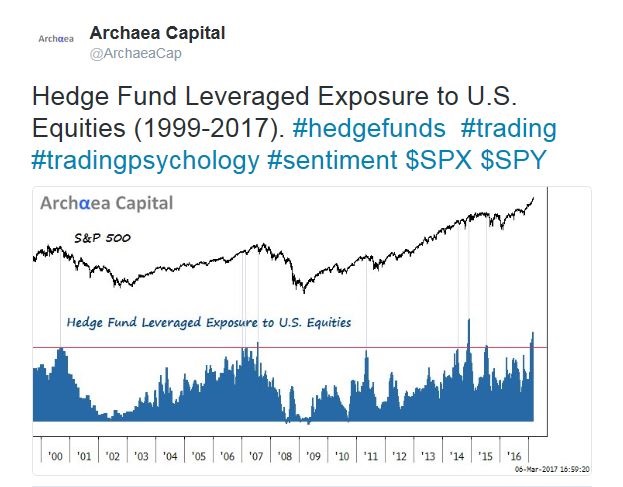

Finally, Archaea Capital recently observed that the implied equity exposure of hedge funds show a crowded long reading.

If the sentiment of individuals, institutions, RIAs, and hedge funds are all at bullish extremes, who is left to buy?

Sentiment an inexact top calling indicator

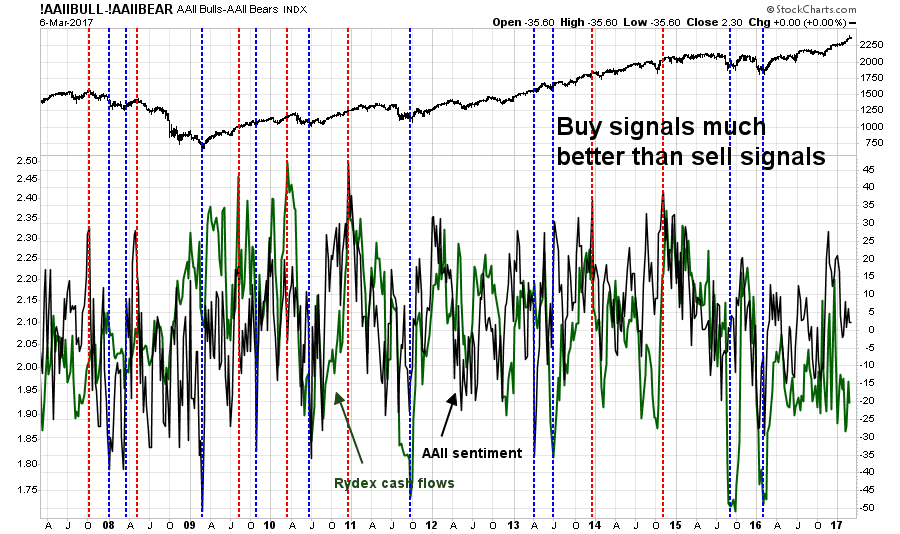

I would warn the bears, however, that sentiment models have a spotty track record at calling tops. Consider this chart of AAII sentiment (black) and Rydex cash flow sentiment (green). The blue vertical lines are the buy signals indicating periods of panic, while the red vertical lines show the bullish extremes. As the chart shows, the buy signals work much better than sell signals.

The same story holds for NAAIM sentiment. They are much better at calling bottoms than calling tops.

Caution, not panic

Most of these studies have only analyzed one single sentiment indicator in isolation. What happens when all the sentiment indicators show excessively bullish readings?

I have no good answer for that, but I interpret these conditions as the market poised for a correction. Ed Clissold of Ned Davis Research (see above) stated: “It’s a way of showing stocks are pretty stretched, but that’s not to say they’re going to go down tomorrow. It just means there’s not a lot of cash to act as a shock absorber. This measure does tend to mean revert over time, and we’re near the low-end of the range, so this ratio will go back up again.”

Art Cashin of UBS recently called for a 5-7% correction on CNBC.

As major indexes hovered in the red Tuesday and some stocks were coming off 52-week lows, Art Cashin told CNBC that the market could be setting a stage for a minor correction.

“It’s a mild warning signal, to tell you the truth,” Cashin told “Squawk Alley.” “When we’ve seen those kinds of moves before, the market has either stalled or actually pulled back somewhat. Not anything climactic, but you could be setting up for [a] 5 to 7 percent pullback.”

In light of the recent technical breaks by the major stock indices, that sounds about right.

Disclosure: Long SPXU, TZA

Hi Cam, TNA? Or you mean TZA. Thx. Petr

I expected new political problems would cause the markets to fall here. Now that Trump and the GOP are actually pursuing legislation in the form of changing Obamacare, there are huge factions aligning themselves against each other within the Republican representatives.

The Trump bull market has been based on passing business friendly legislation some of which are going to cause a big spike higher in the budget deficit. The fight on Obamacare tells us Trump’s agenda may bog down in the swamp just like every other new President.

Will investors start to question if business-friendly and economy-stimulating policies will survive?

Hi Cam,

I am a little perplexed why the VIX and the VXX are not going up as the market is pulling back. Till now the damage is mostly in the Russell while the S&P and the QQQ are showing relative strength. In the meantime the short term indicators are quite oversold. Any explanation?

Couldn’t it have something to do with lower correlations resulting in what is seen in the VIX or VXX as less volatility than when correlations have been higher?

i will add high yield is pulling back noticeably. thats not good for equity, although also somewhat leading.

This might be the answer to my question. Compliments of zero hedge:

http://www.zerohedge.com/news/2017-03-09/things-just-got-even-weirder