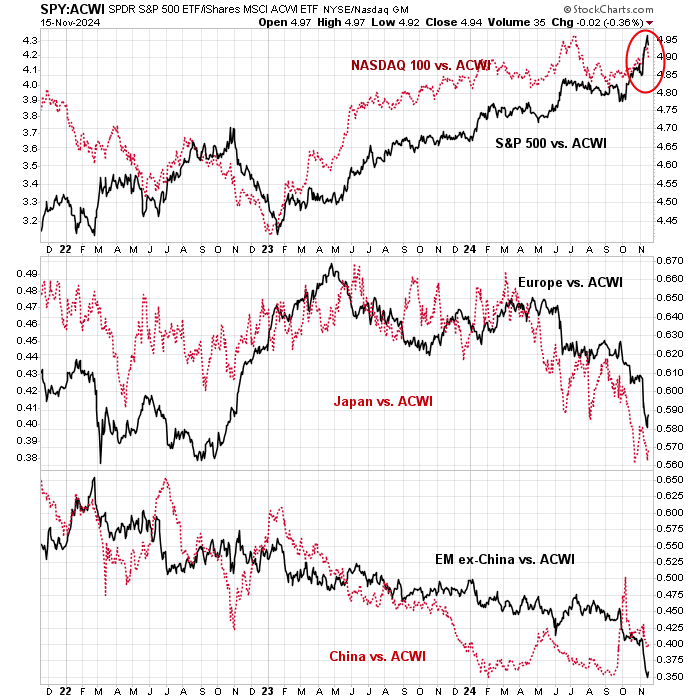

U.S. equity prices rose strongly in the wake of Trump’s victory. As the accompanying shows, both the S&P 500 and NASDAQ 100 surged on a relative basis, while other regions tanked.

Donald Trump promised to Make America Great Again. While he may have accomplished that task in the short run for U.S. stocks, can he do the same for all equities?

European and Asian weakness

Even as the S&P 500 and NASDAQ stocks soared to all-time highs, the price action for the rest of the world doesn’t look as bullish.

In Europe, both the Euro STOXX 50 and FTSE 100 are flat to down as both indices are trading below their respective 50 and 200 dma, indicating a loss of price momentum.

Over in Asia, the relative performance of Asian markets are also flat to down. Don’t expect global leadership to emerge out of Asia, especially in light of the well-known economic headwinds that faces China.

Commodity prices, which are market-based signals of global cyclical strength and Chinese cyclical strength in particular, are not showing any signs that a strong reflationary cycle is under way. The cyclically sensitive copper/gold and base/metal gold ratios (bottom panel) have traded sideways since August.

My Trend Asset Allocation Model applies trend-following principles to global equity and commodity markets to arrive at an overall risk appetite signal. It is therefore no surprise that the Trend Model is showing a neutral reading under these circumstances.

Can America stand alone?

The U.S. is the only exception to the sideways pattern of major markets around the world. Both the S&P 500 and NASDAQ stocks recently reached all-time highs. In other words, America stands alone, at least from the viewpoint of stock prices.

Can the bull continue? Here are the bull and bear cases.

The bull case is simple. Equity bulls care about two things: earnings growth and the cost of capital. Tax cuts will boost earnings growth. Deregulation could ignite the animal spirits in the markets. Specifically, less regulation should provide boosts for the technology, financial and energy sectors.

Falling interest rates lowers the cost of capital. The Fed began its rate cut with a half-point cut in October, followed by a quarter-point in November. Estimates of the neutral rate vary and range between 3% and 4%. Indicating there is more room for rates to fall.

Fiscal policy is stimulative and there are no signs of a recession on the horizon. The U.S. economy is firing on all cylinders. Real GDP growth is about 3%. The unemployment rate is about 4%. The AI revolution will boost productivity. Economic momentum is positive, as measured by the rising Economic Surprise Index, which measures whether economic statistics are beating or missing expectations.

What’s not to like?

The bear case rests mostly on valuation concerns. The S&P 500 is trading at a forward P/E of 22, which is highly elevated relative to its own history.

This is nothing like Trump 1.0 of 2017. When Trump first won the White House, the S&P 500 forward P/E was about 17. The corporate tax rate was 35% on its way to 21%, which was not expected by the market. The debt/GDP ratio was 98%.

Today, the S&P 500 trades at a forward P/E of 22. An extension of the TCJA, even with tweaks, is mainly a cancellation of an increase in the corporate tax rate. The debt/GDP ratio is 124% and expected to go even higher.

Trump’s tariff plan is not a free lunch. There will be retaliation. In addition, the interaction of TCJA and tariffs have had some unexpected results. While Trump’s tariff plan is to incentivize companies to re-shore manufacturing to the U.S., Brad Setser observed the enactment of TCJA sparked a surge in EU pharmaceutical exports, probably the results of strategies that offshored the production of drugs intended for the U.S. market to low-tax Ireland.

Moreover, tariffs are expected to be inflationary, which will tie the Fed’s hands in its easing cycle. As for Trump’s plan to incentivize companies to re-locate manufacturing facilities back to the U.S., the devil is in the details of any plan. Consider the decisions facing corporate boards that contemplate a plan to invest in manufacturing the U.S., or any location. Investment involves costs, which is relatively well-known, and an uncertain payoff. The risk/reward ratio has to be sufficiently favourable for a board to undertake such a decision. As well, companies have to consider secondary factors, such as the availability of trained labour, the productivity of the labour, and the existence of a supply chain ecosystem. After years of hollowing manufacturing, supply chains and trained personnel disappear. Technological leadership doesn’t just magically happen overnight.

This is a useful framework to think about how a re-industrialization process may play out. Investors need to consider a range of possibilities and how the demands of capital markets may drive corporate investment initiatives.

Cautious, but not bearish

Despite these risks, I am not bearish, but intermediate-term cautious on U.S. equities.

Stock prices depend on earnings growth and corporate funding costs. For now, forward 12-month earnings estimates are rising – and these figures were mostly taken before the election results were known.

While valuation concerns are valid, here are a range of possibilities of how earnings may change under Trump. Examples of conventional investment bank analysis from BoA and Goldman Sachs projects that cutting the corporate tax rate to 15% would boost S&P 500 EPS by 4%. All else being equal, today’s forward P/E of 22 would fall to 21.

Uber-bull Ed Yardeni raised his S&P 500 targets to 6100 for year-end 2024, 7000 to year-end 2025 and 8000 for year-end 2026. He raised his S&P 500 2025 and 2026 EPS from $275 to $290 and from $300 to $320, compared to a current consensus of $275 and $308, respectively, based on the promise of a corporate tax cut, deregulation and faster productivity growth. Similarly, Yardeni’s projections lower the forward P/E from 22 to 21.

Moreover, I am not seeing any signs of funding cost headwinds for stock prices. The accompanying chart shows estimates of the extremes of fund costs, as represented by junk bond yield spreads plus the 5-year Treasury rate (blue line) and the actual junk bond yields (red line). Overlaid on top of these yields is the NASDAQ 100 (black line), which is a proxy for the leading-edge public companies in the U.S. In the past two cycles, major NASDAQ bear markets were accompanied by increases in funding cost, which is not in evidence today.

In the short run, animal spirits are dominant in the U.S. I recently pointed out that the S&P 500 was testing the upper end of a rising trend line, and it was likely to pause and consolidate its gains. With the caveat that the NASDAQ Composite and the Russell 2000 have already overrun their rising trend line resistance, a projection of the S&P 500 trend line until year-end comes to about 6300, which could be an upside target should the combination of a FOMO buying stampede and Treasury liquidity flood continues.

Seth Golden came to a similar conclusion based on a study of post-election returns.

In conclusion, U.S. equities have surged in the wake of Trump’s electoral victory while stock markets in the rest of the world have been flat to down. While the combination of narrowing global leadership and elevated U.S. valuation are concerns, I remain cautious but not bearish on the U.S. and global equity markets. Fundamental and macro momentum are strong, and there are no signs of reversal in funding costs.

However, should the S&P 500 reach about 6300 by year-end, valuation pressures could put downward pressure on equity prices in 2025.